Australia

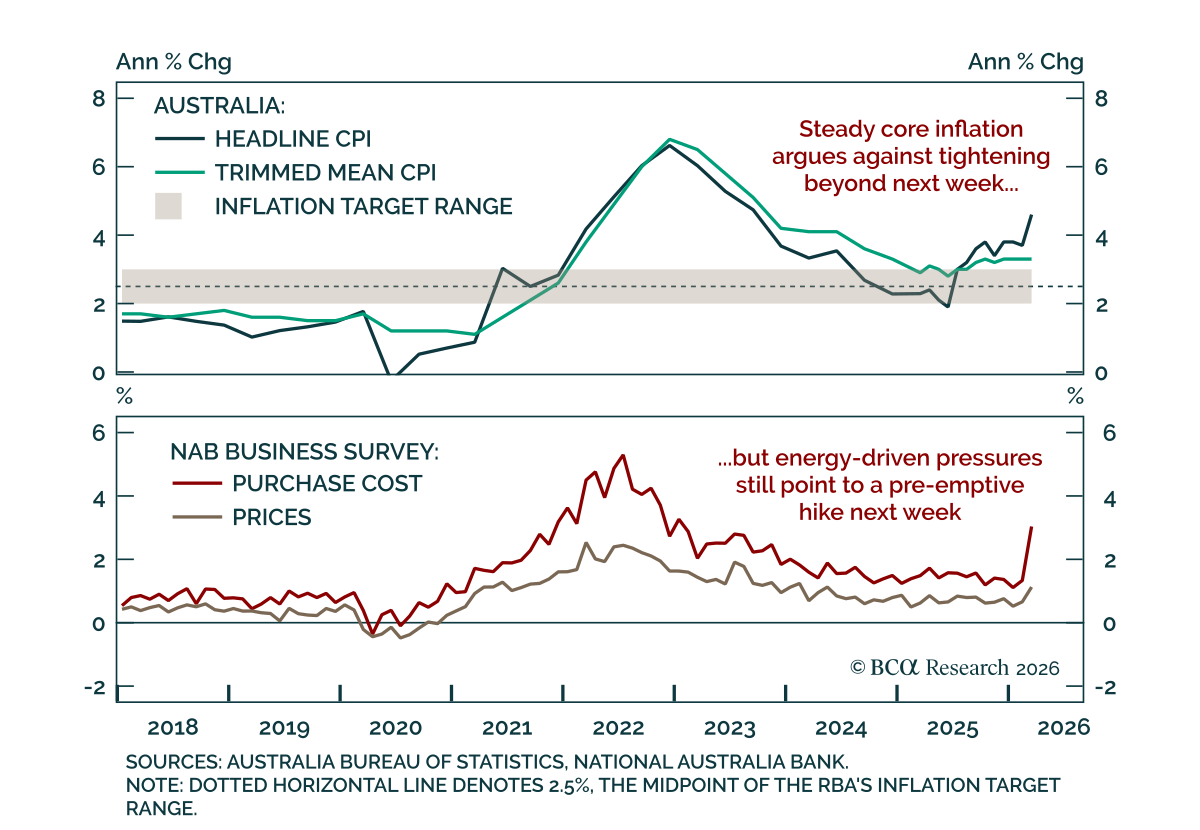

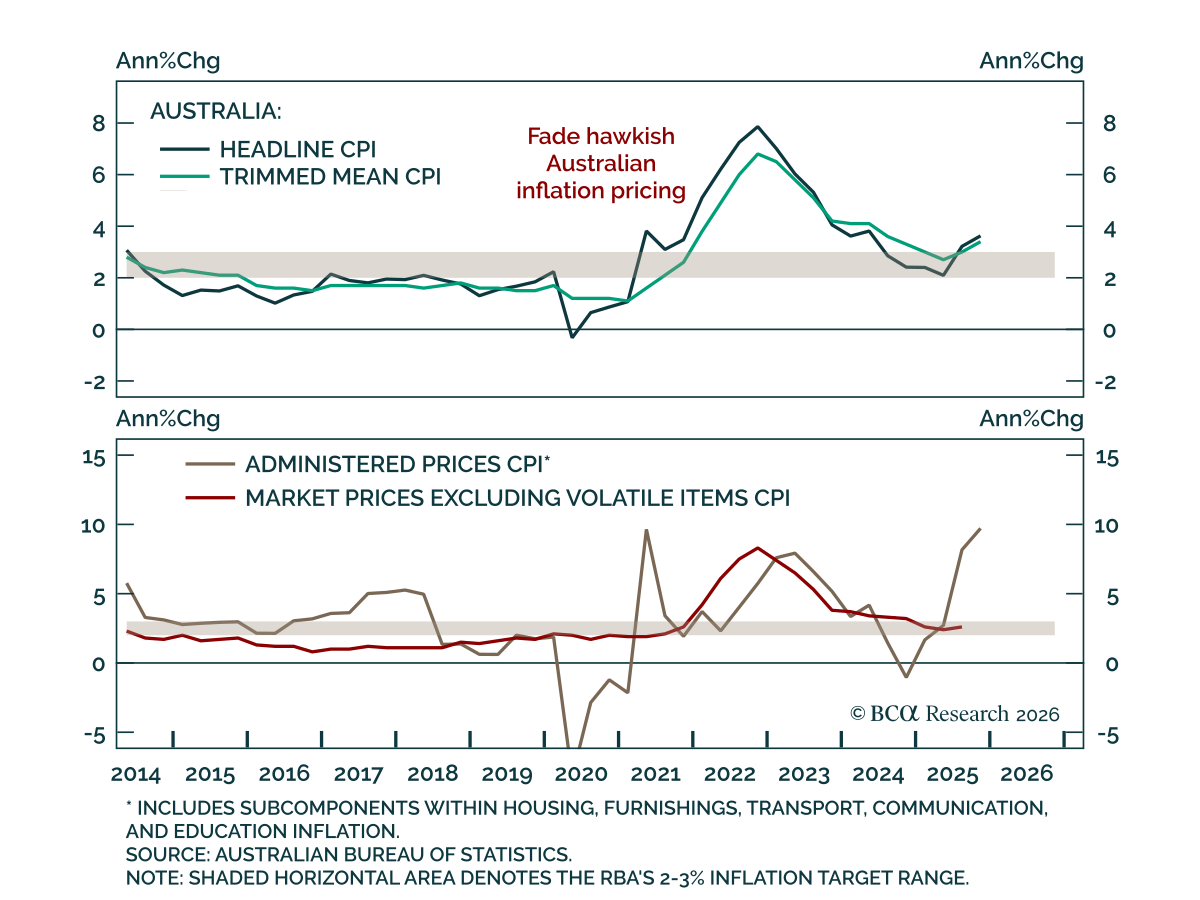

Australia's Q1 CPI showed energy-driven headline acceleration, but steady core inflation suggests markets are over-pricing RBA tightening. Headline inflation accelerated to 4.1% y/y (1.4% q/q) from 3.6% (0.6%), while the trimmed mean was largely unchanged at…

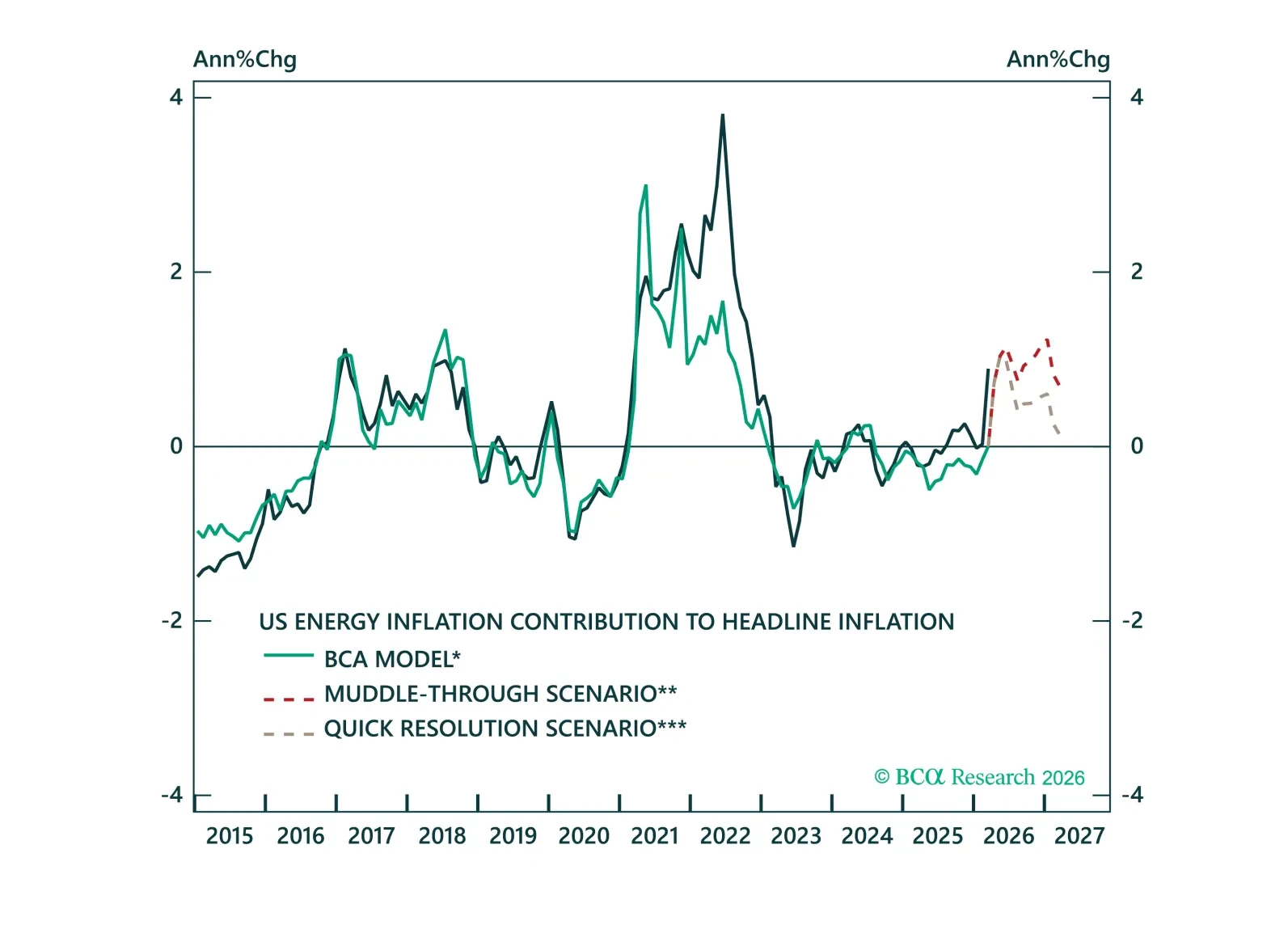

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

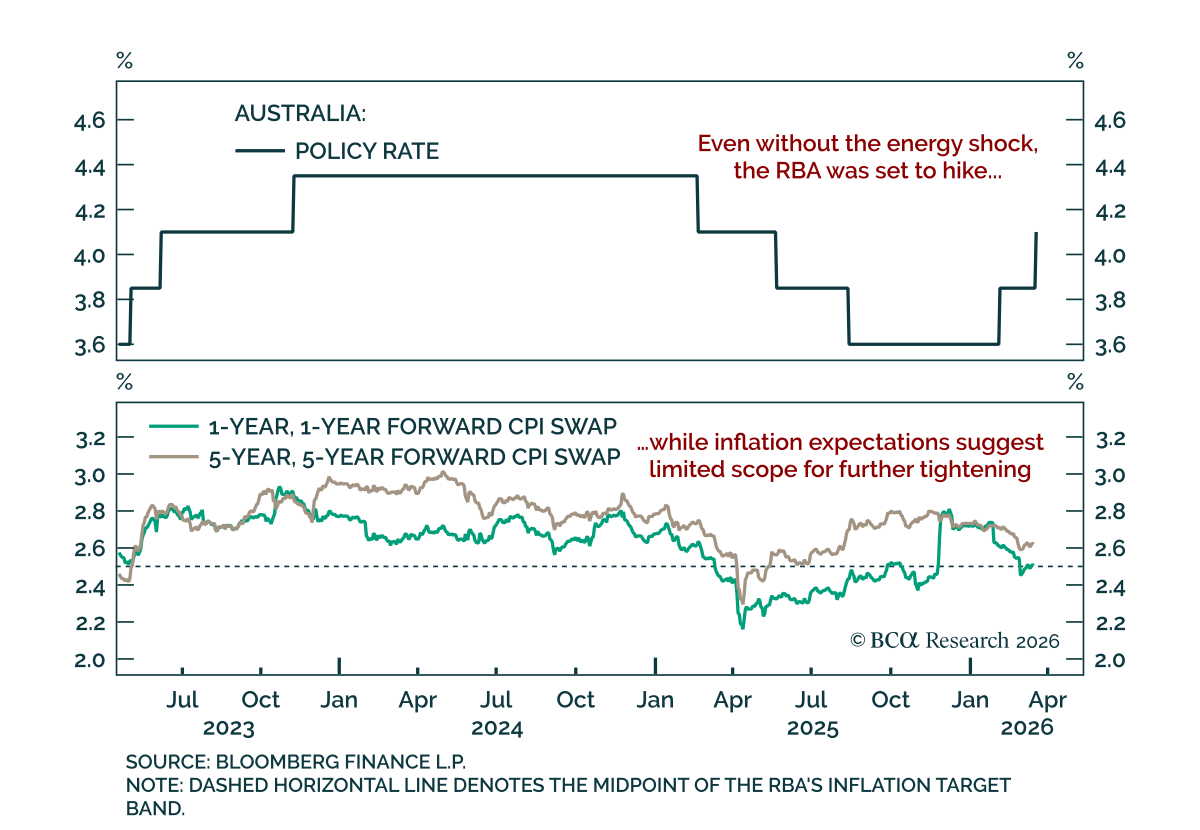

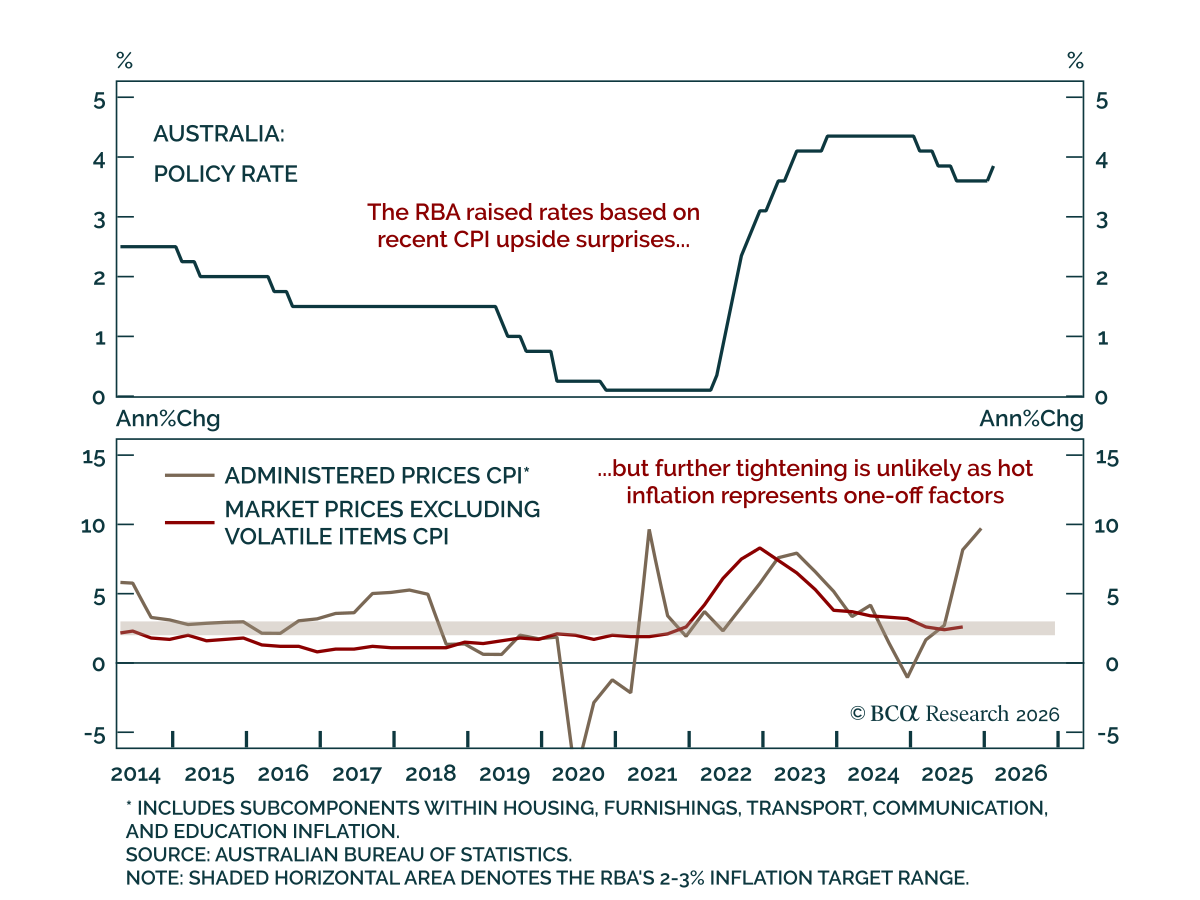

The RBA delivered a second rate hike this year, but markets may be overpricing further tightening. The RBA raised the policy rate by 25 bps to 4.1%, in line with expectations. Tightening was anticipated regardless of the energy shock. The vote was split 5-4,…

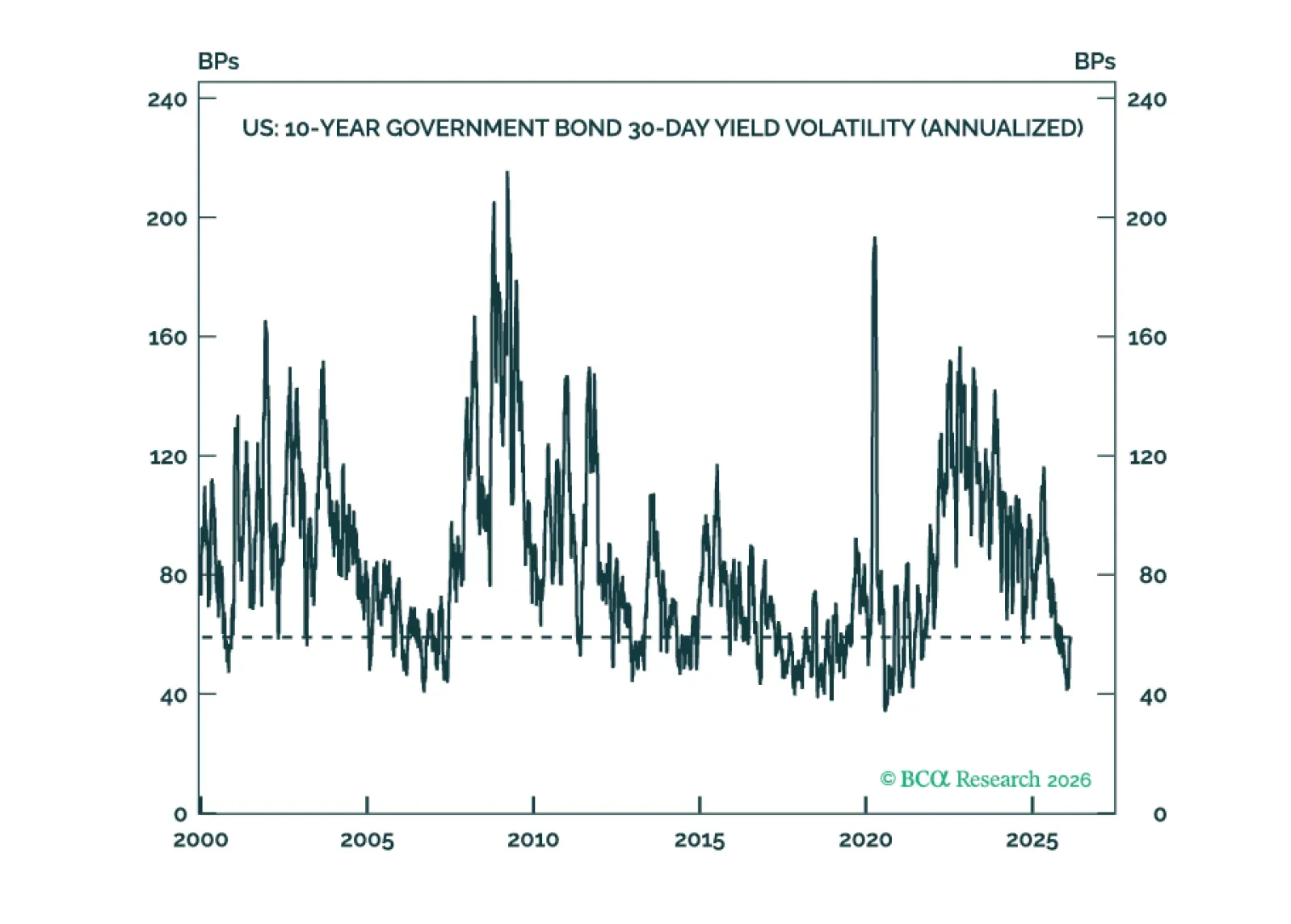

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.

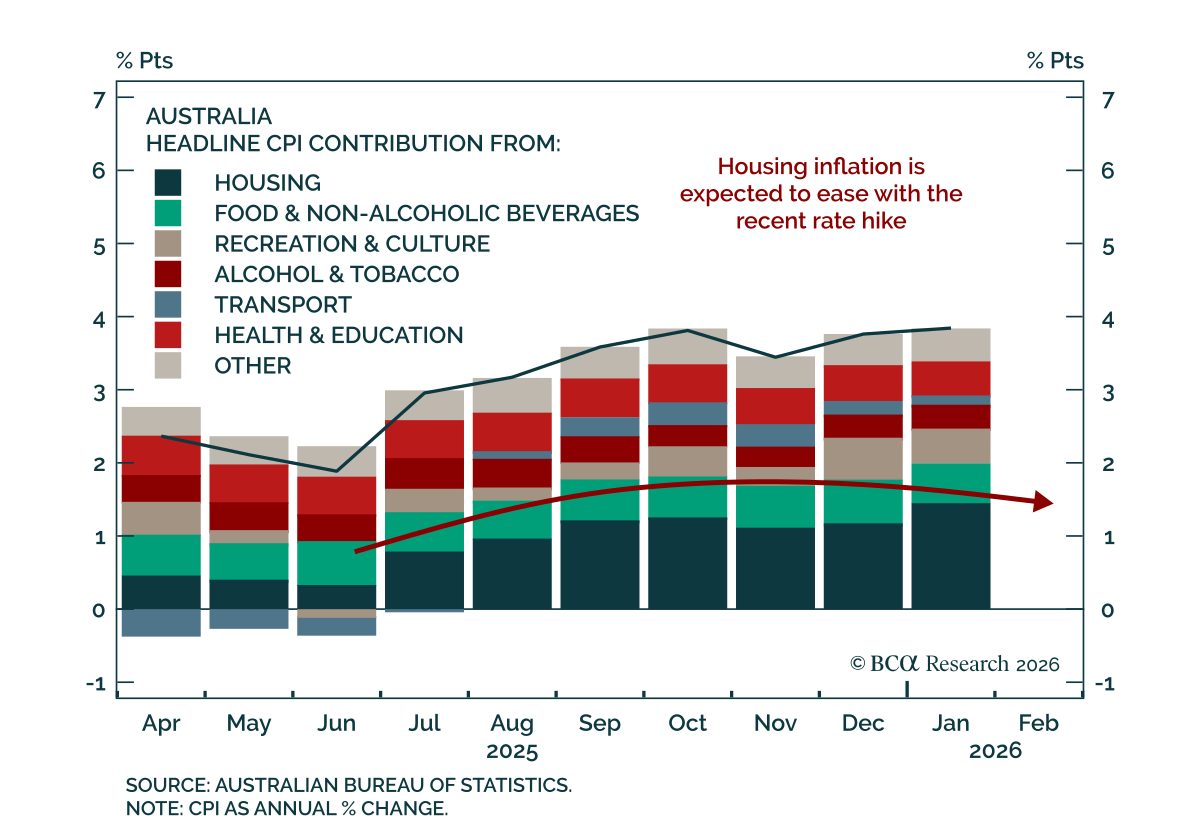

Australian January CPI surprised slightly to the upside, but underlying inflation pressures remain modest. Headline inflation was steady at 3.8% y/y, while the trimmed mean rose to 3.4% from 3.3%. The odds of a May rate hike increased to above 70% following…

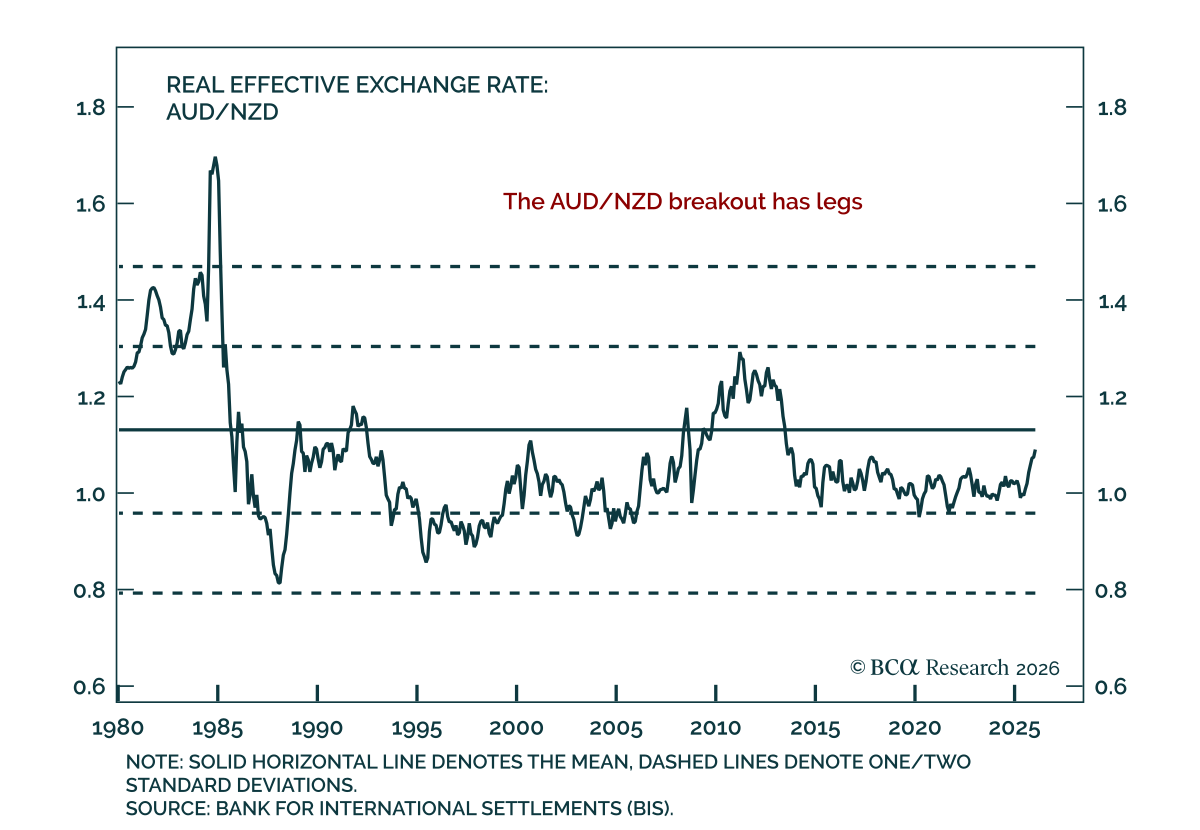

AUD/NZD has broken out to a decade high after trading sideways since 2015. Our Chart Of The Week comes from Chester Ntonifor, GeoMacro and Access strategist. Given that the momentum of the move has been sustained since last April (the longest stretch outside…

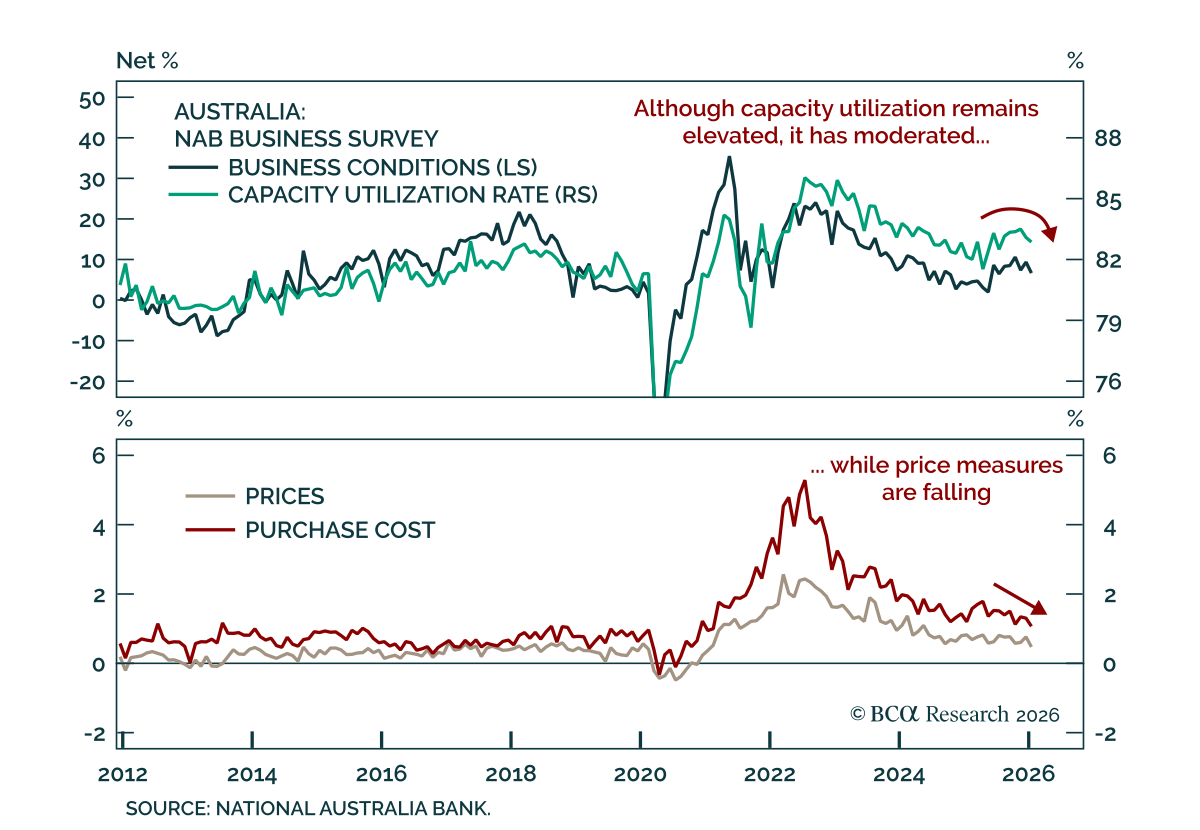

The NAB January survey points to easing Australian inflation pressures, despite recent hot inflation data. Growth signals were mixed: Business conditions eased to +7 from +9, close to the long-term average, while business confidence edged up to +3 from a…

Stay long Australian rates as market expectations for further RBA hikes have overshot. The RBA raised its policy rate by 25 bps to 3.85%, as expected, following upside surprises in recent CPI prints. The accompanying statement acknowledged that inflation is…

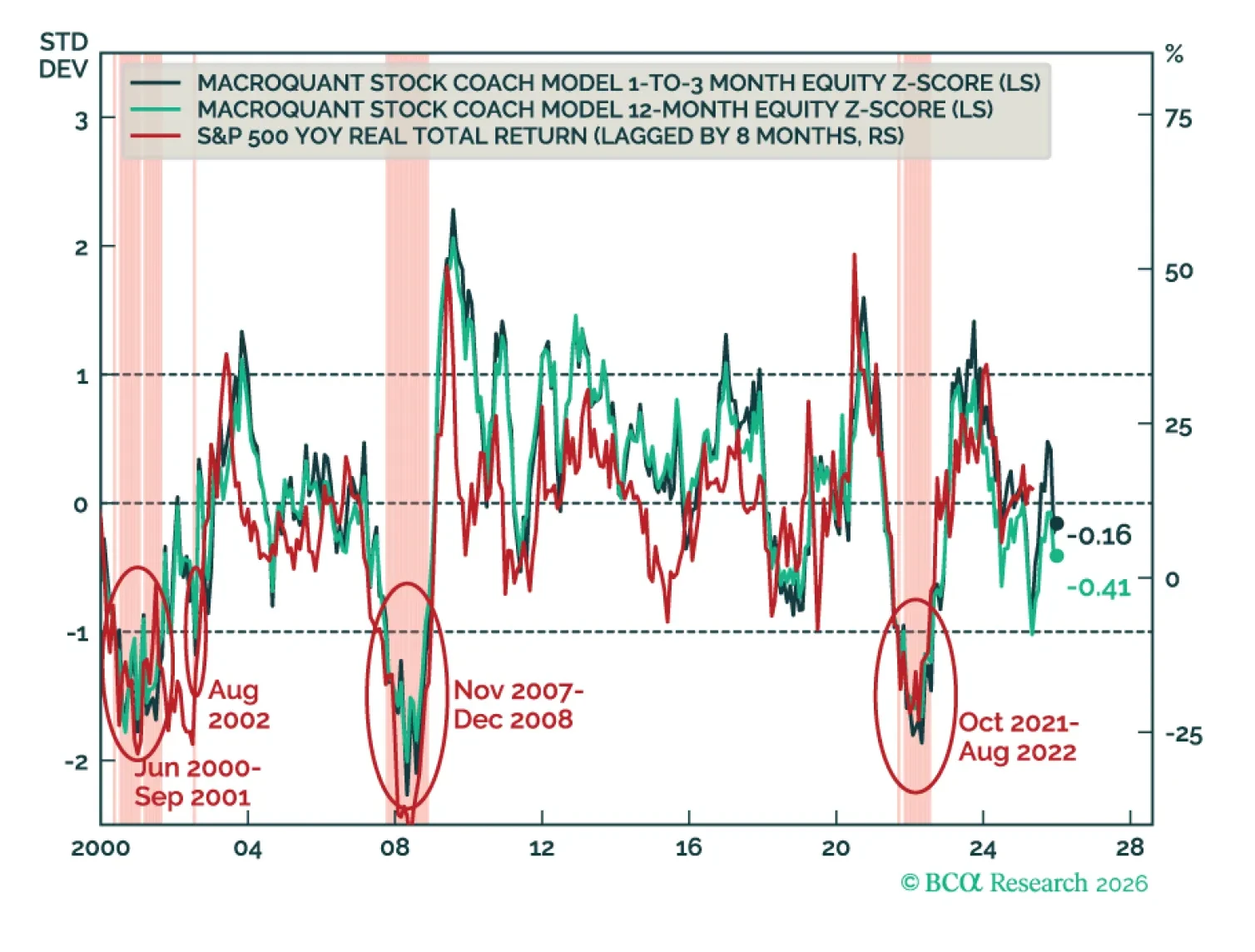

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

Stay long Australian 10-year government bond futures and underweight inflation-linked bonds as market expectations are overly hawkish. Australian Q4 inflation printed hotter than expected, with trimmed-mean inflation rising to 3.2%. Inflation is now back…