Australia

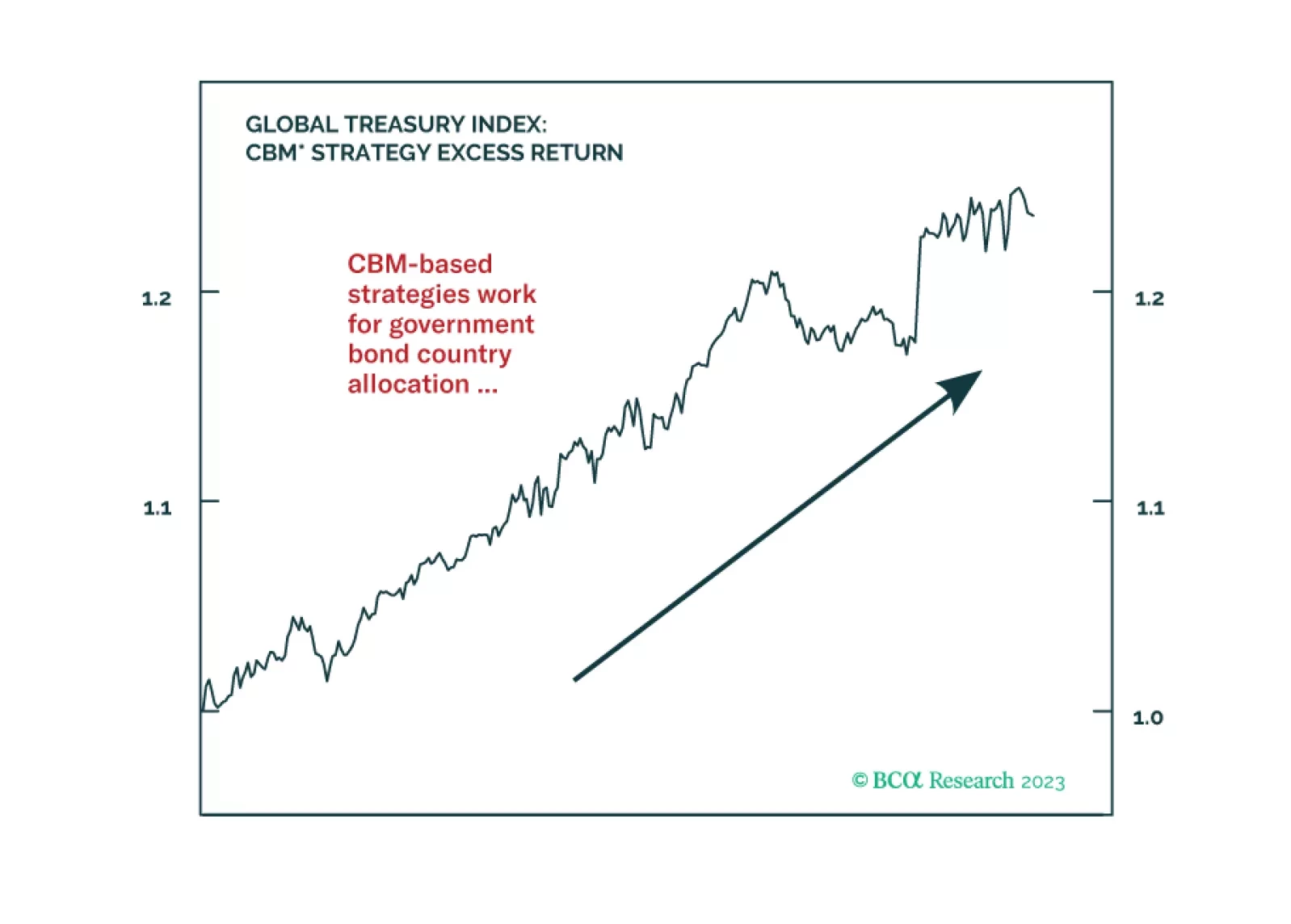

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

In this report, we present the quarterly review of the Global Fixed Income Strategy Model Bond Portfolio. The portfolio remains positioned for slower global growth momentum over the next 6-12 months, favoring government bonds over corporate debt. The portfolio also favors government bonds in countries flirting with recession where policy rates are too high (core Europe & the UK).

A global recession continues to be likely over the next 12 months. The impact of tighter monetary policy is slowly being felt. Government bonds look increasingly attractive as a safe haven.

A global portfolio is likely to return only 5.3% a year over the next decade, compared to 6.7% in the past. Investors either need to lower their return expectations, or take more risk. Our total return methodology remains consistent with previous editions, with changes limited to the Alternatives section.

In this report, we assess the best opportunities in inflation-linked bonds in the major developed economies, based on trends in growth, inflation and the stance of monetary policies in each country. We conclude that the environment is turning more challenging for European inflation-linked bond performance versus nominal government bonds, while the opposite is true in Japan. In the US, US TIPS breakevens have likely peaked, particularly at the short end.