Australia

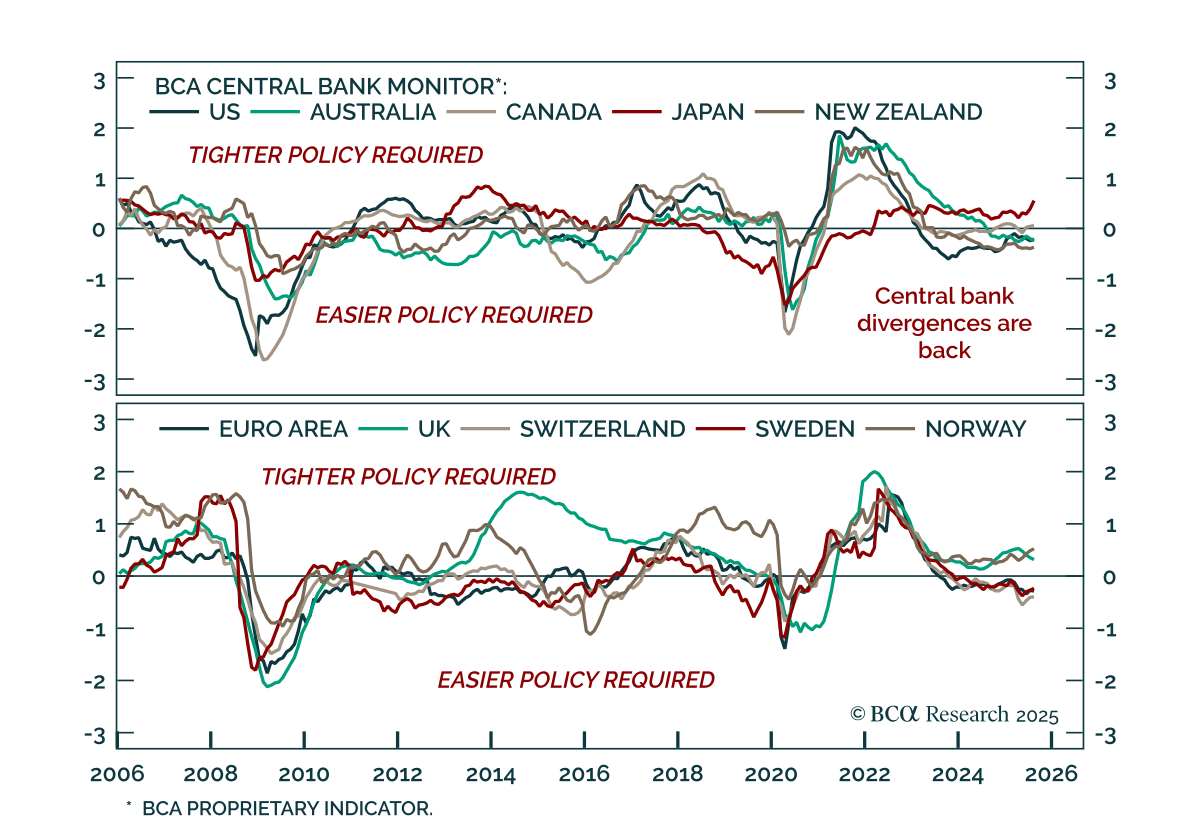

Our DM strategists recommend regional bond overweights in the UK, Canada, and Sweden, and express policy divergence through tactical FX trades: long USD, underweight GBP and SEK, and long JPY vs. EUR. Most G10 central banks are nearing neutral, but their next…

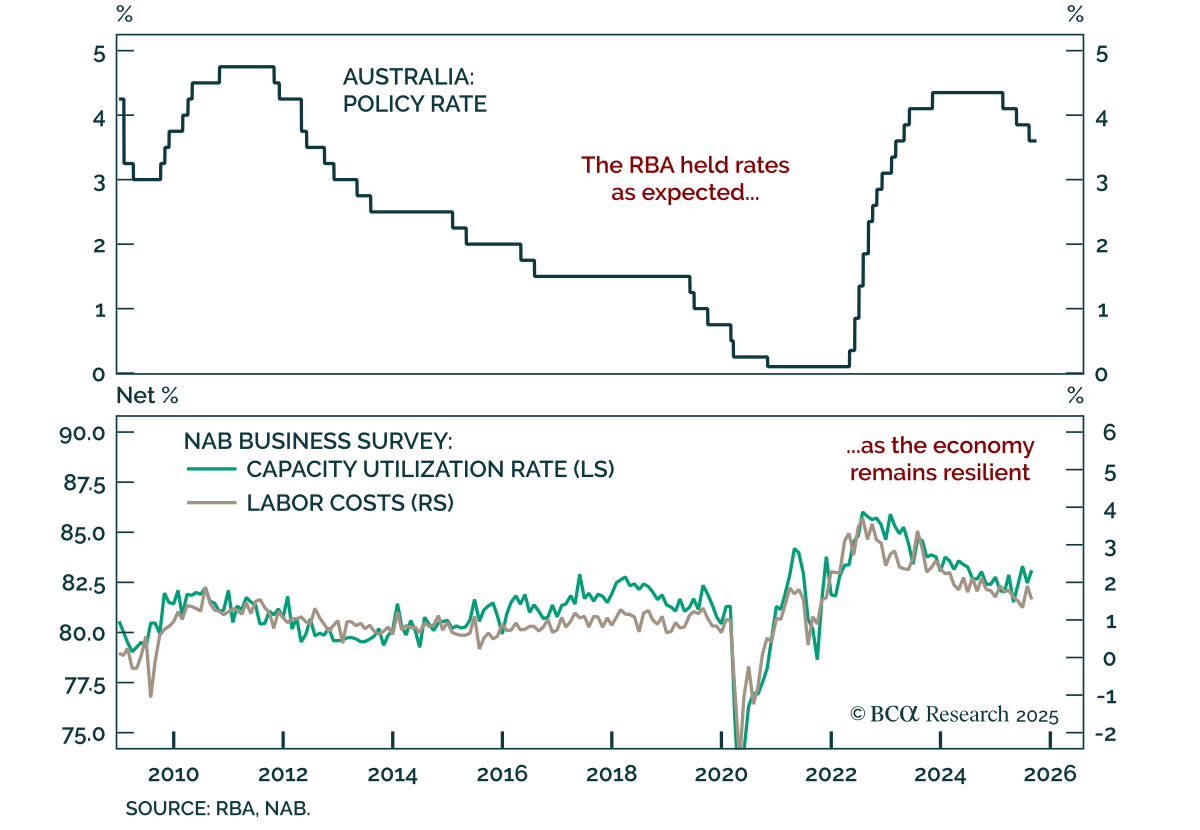

The RBA held rates at 3.6% as expected, maintaining caution as inflation could prove stronger than expected. Policy remains slightly restrictive, and at most one additional cut is on the table as the central bank has achieved a soft landing. While the RBA has…

Monetary policy divergences are re-emerging. We rely on BCA’s Central Bank Monitor to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.

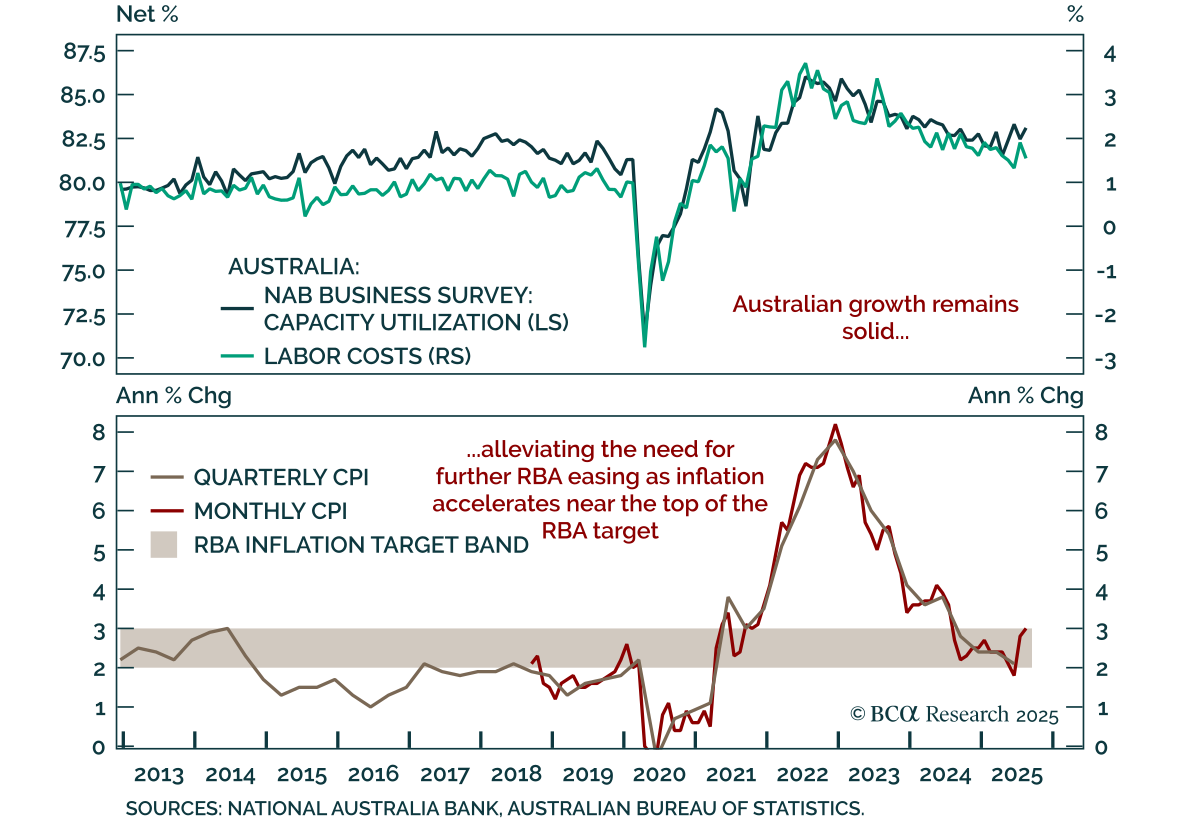

Australian inflation surprised higher in August, validating the RBA’s cautious stance and supporting an underweight on ACGBs. Headline CPI rose to 3.0% y/y from 2.8%, the highest in a year and at the top of the RBA’s 2-3% target range. While the central bank…

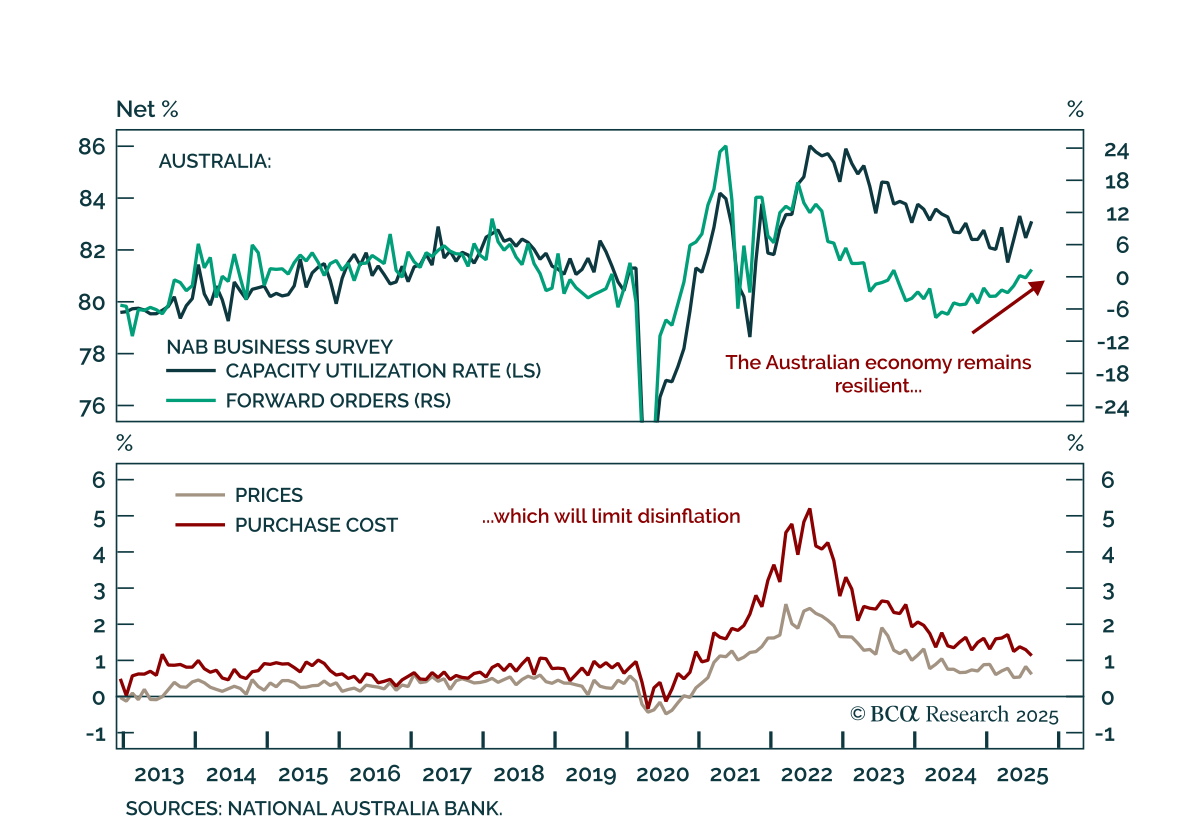

Australia’s NAB survey shows underlying resilience, reinforcing our underweight on ACGBs and the case for AUD flatteners vs. CAD steepeners. The August survey was mixed, with current conditions improving to 7 from 5, while business confidence softened to 4…

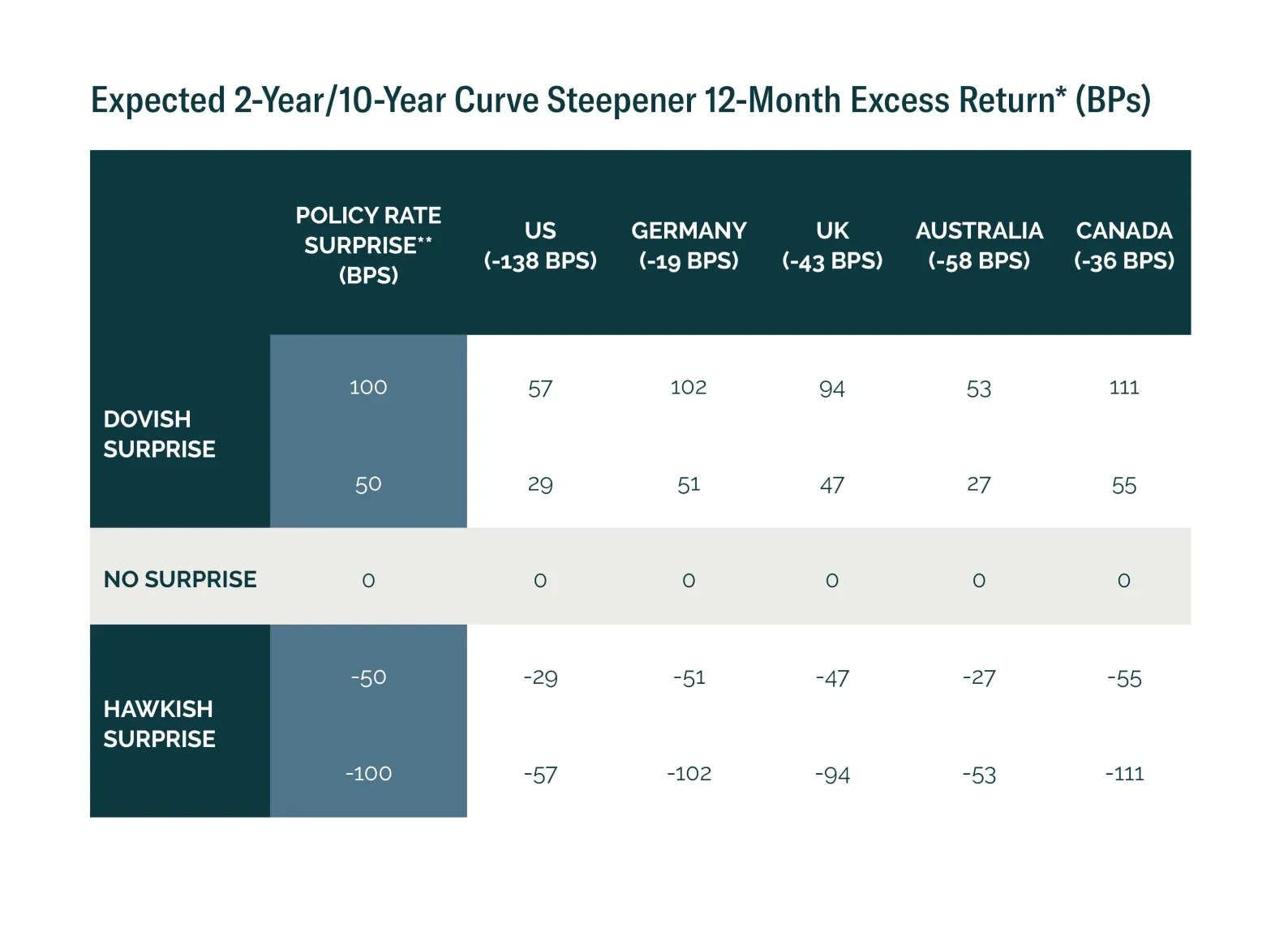

Monetary policy surprises shape curve trade returns. We show where steepeners and flatteners offer the best risk-reward in today’s market.

Australia’s July CPI surprise does not justify the aggressive easing priced, keeping us underweight ACGBs. Headline inflation accelerated to 2.8% y/y from 1.9% in June, with trimmed mean rising to 2.7% from 2.1%. Despite the rebound, inflation remains…

The RBA delivered a widely expected cut to 3.6%, but resilient data warrant an ACGBs underweight. The 25 bps cut was the third this year and Governor Bullock’s guidance was consistent with a cut every other meeting, keeping ACGB yields roughly…

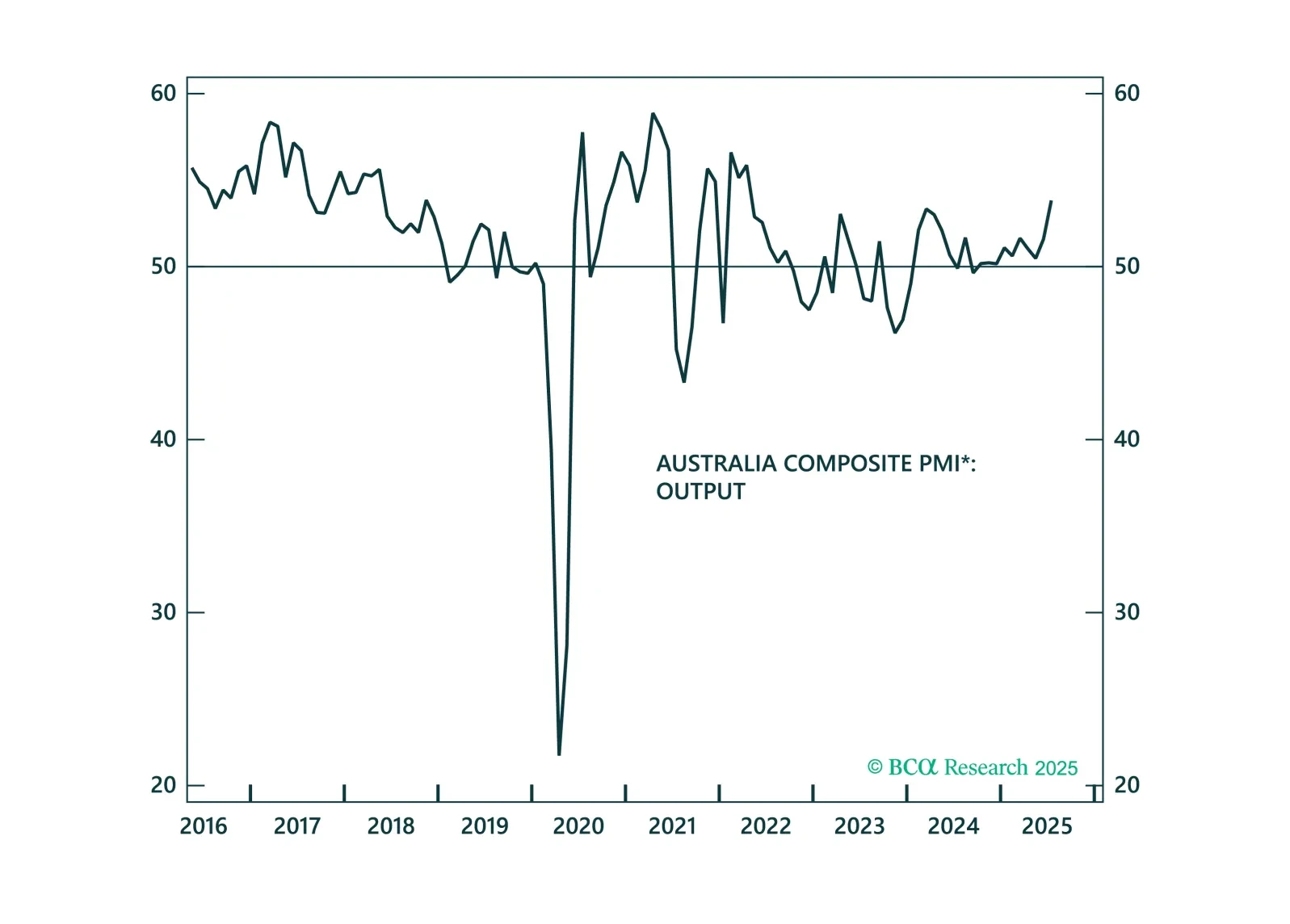

In a widely anticipated move, the RBA resumed cutting rates. However, with housing, consumption, and PMIs improving, we see little scope for the RBA to ease beyond market expectations.

RBA minutes confirmed a cautious approach to easing, reinforcing our underweight in ACGBs and long AUD/NZD stance. The decision to hold at 3.85% surprised markets expecting a 25 bps cut. Governor Bullock had framed the decision as one of timing, but…