Australia

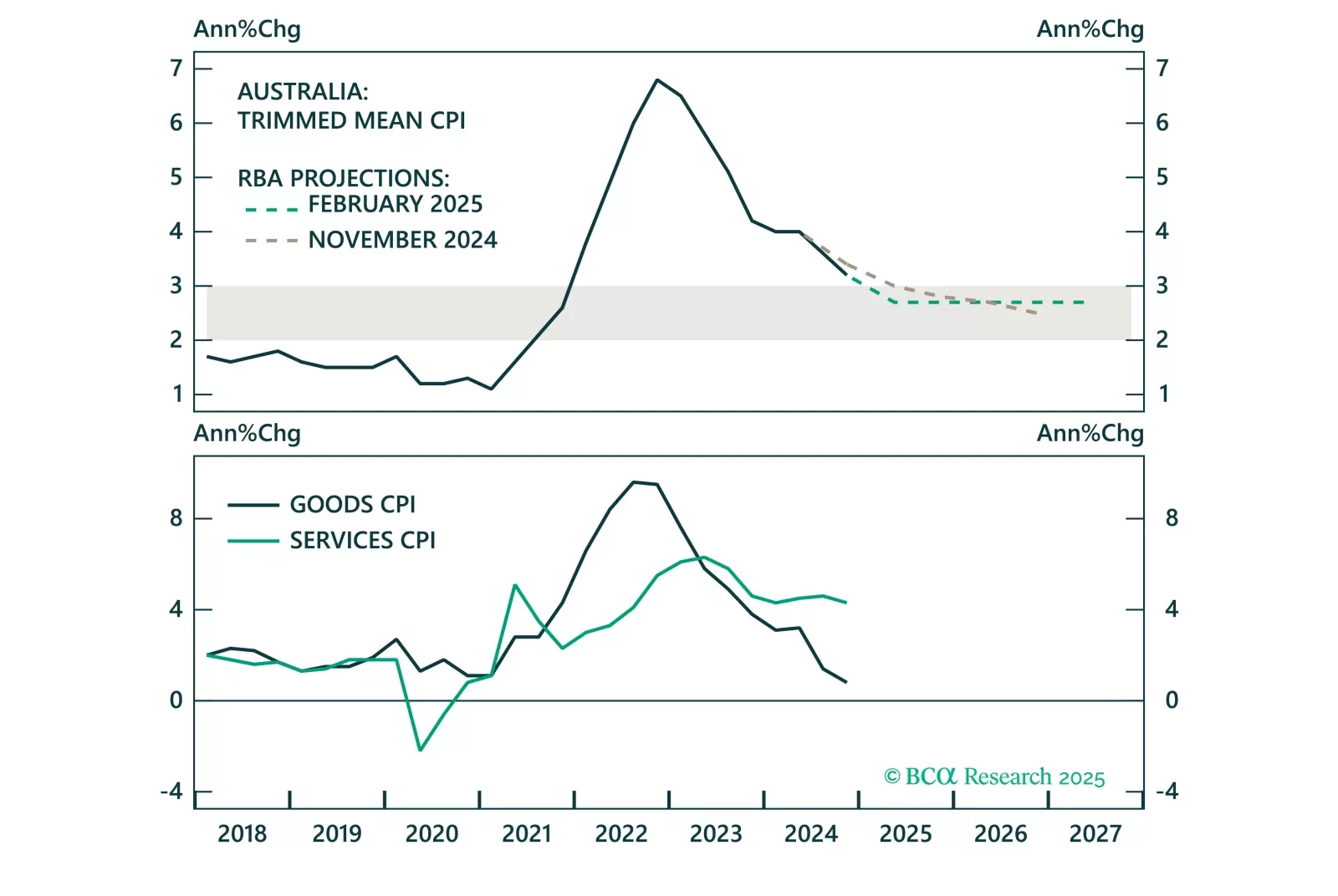

Overnight, the RBA cut the cash target rate for the first time since 2022, marking the beginning of the policy easing cycle in Australia. However, the RBA will proceed cautiously with further rate cuts, given a tight labor market and still elevated services inflation. This will keep Australian government bond yields elevated versus global yields, benefitting the Australian dollar.

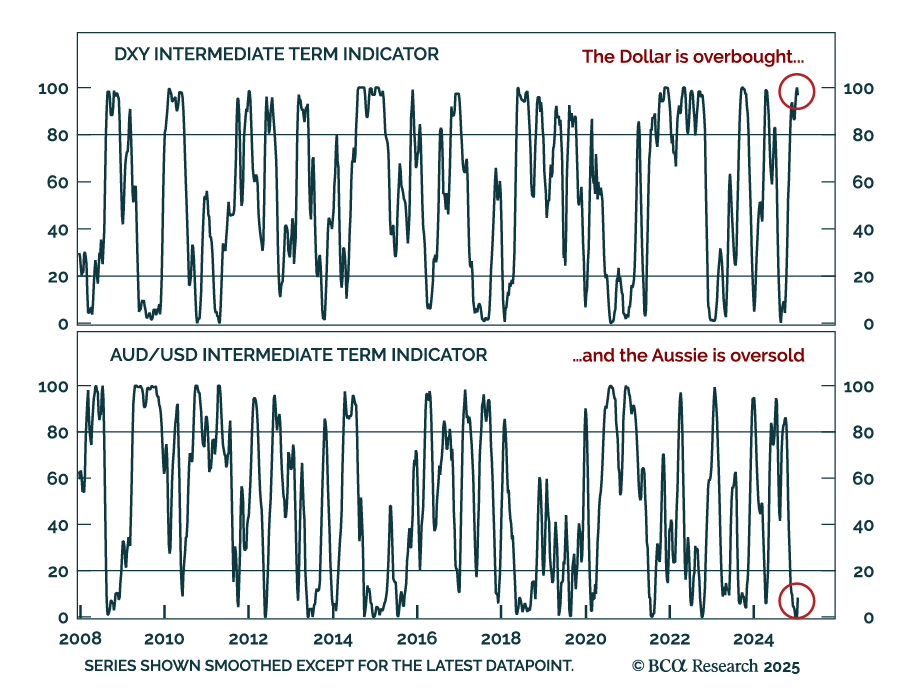

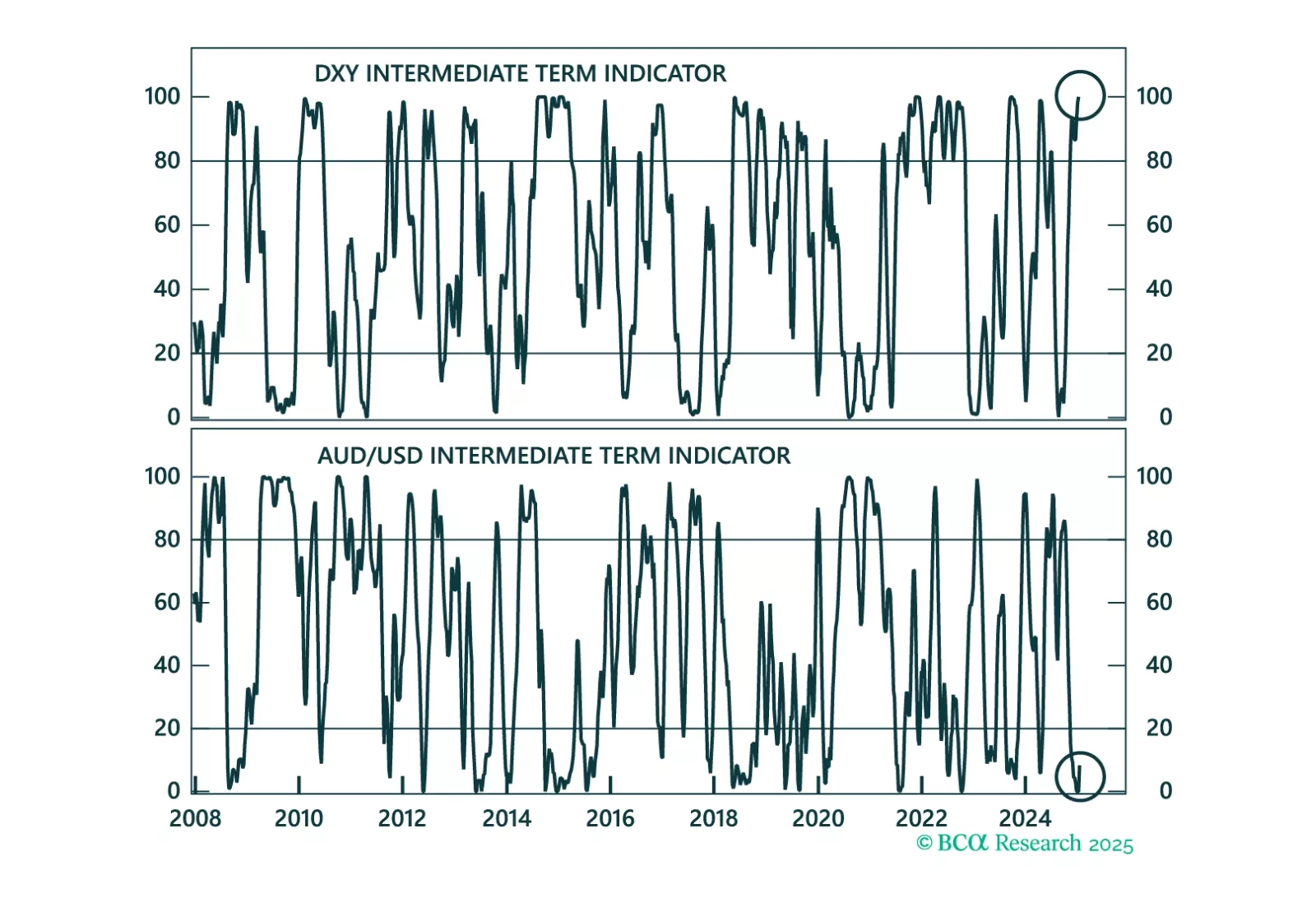

This week’s report looks at the US dollar, from the lens of one very cyclical currency – the Australian dollar.

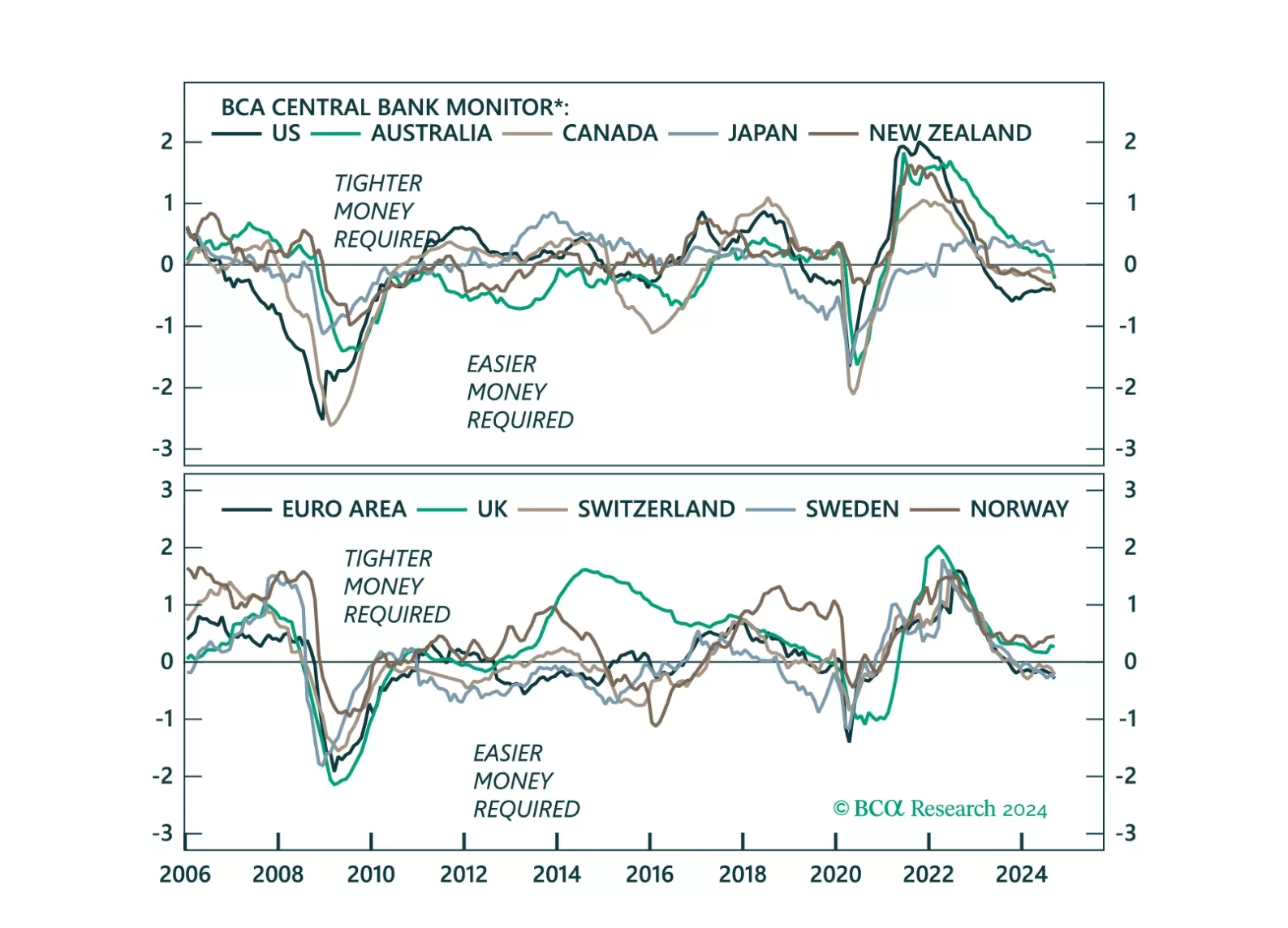

This week, we update our Central Bank Monitors (CBMs), that help us calibrate how monetary policy should be adjusted in developed-market economies. Our conclusion is that while overall, easier monetary settings are required, there a few trade ideas that arise from the divergences in signals amongst G10 countries.

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

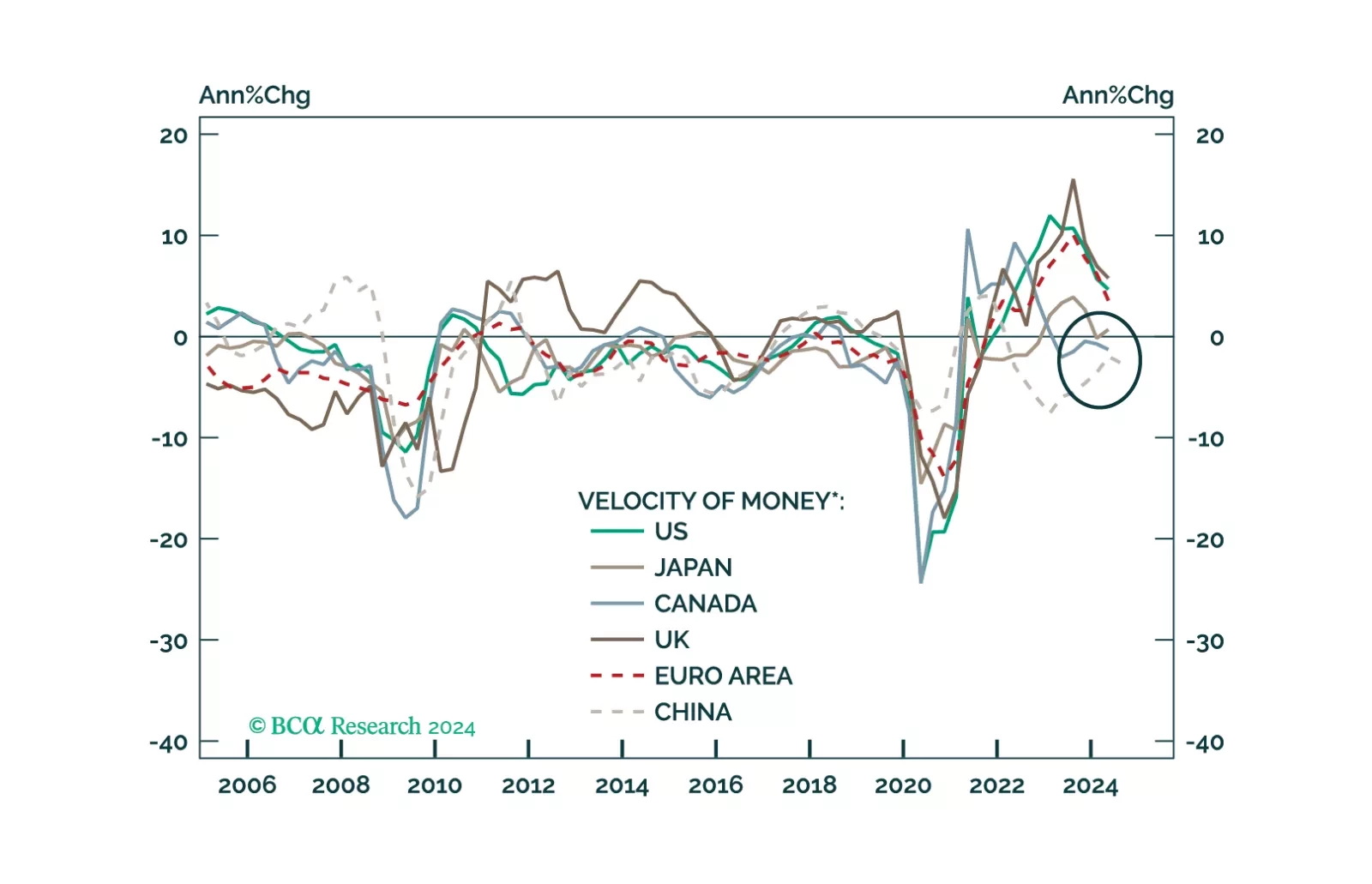

This Insight looks at the likely direction of bond yields and the dollar, from the lens of money velocity.