BCA Indicators/Model

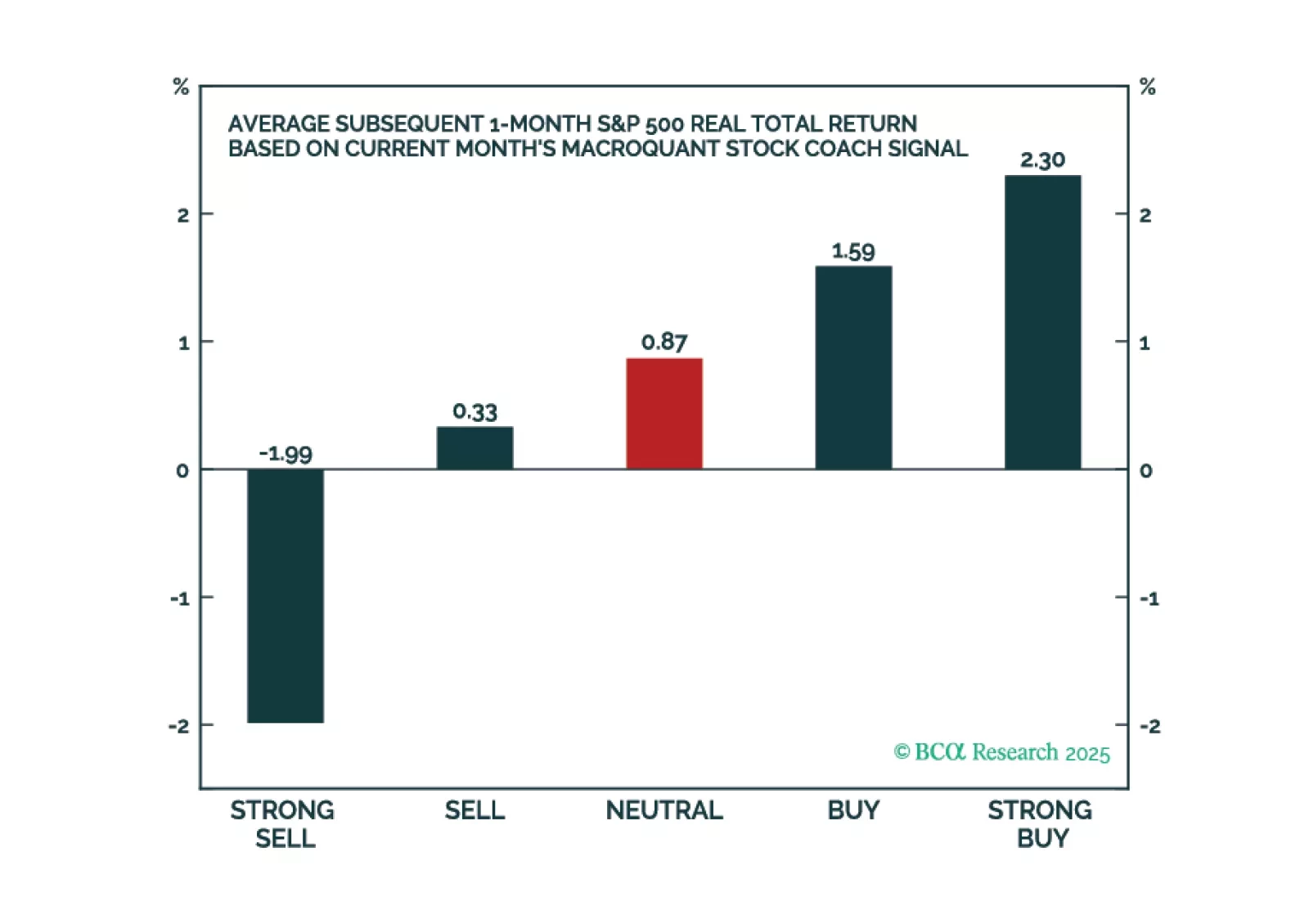

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

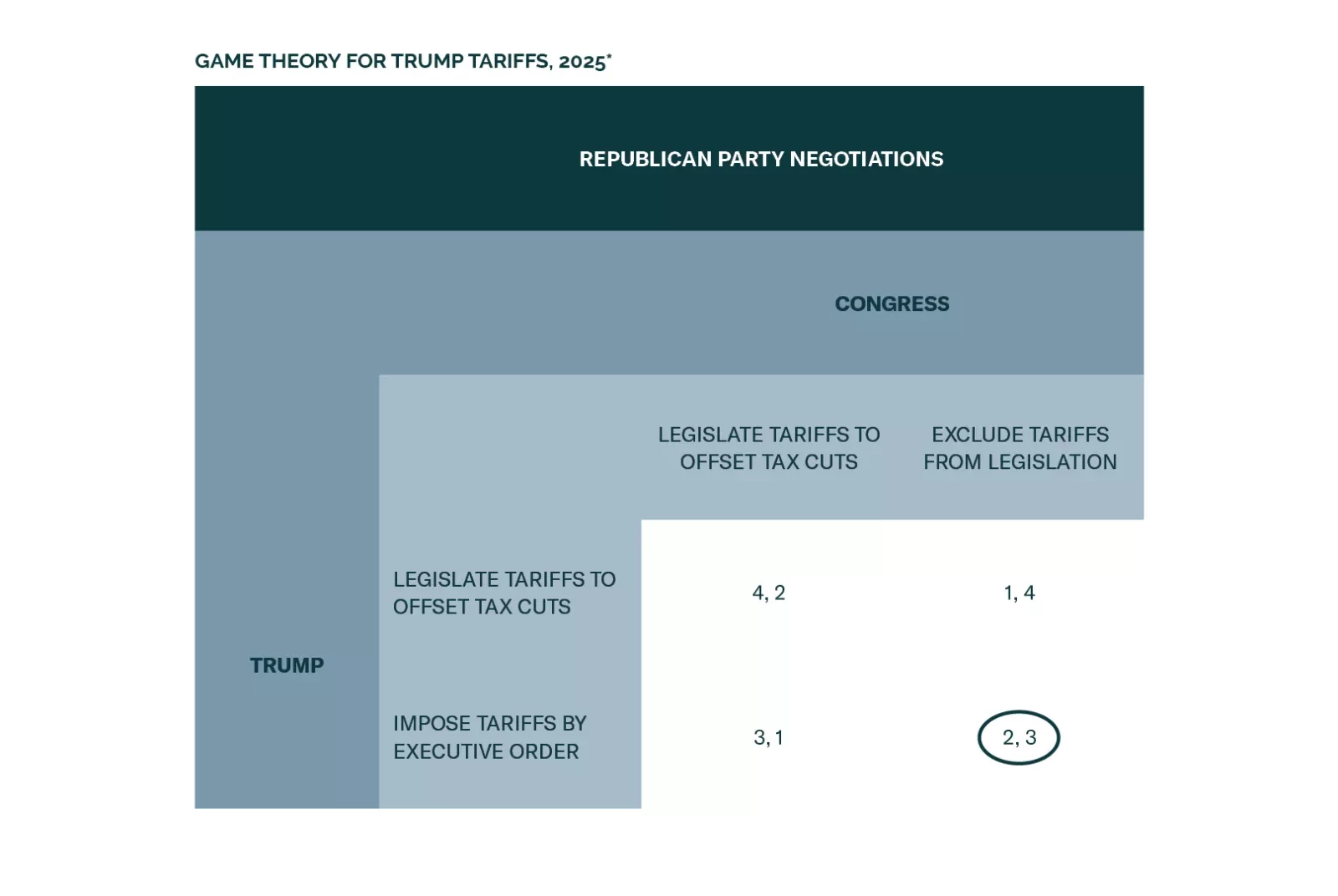

Simple games allow us to model several of the Trump administration’s most disruptive policies in 2025. We find that markets face an increase in volatility as Congress expands the budget, Trump implements tariffs on the world, China retaliates, and Taiwan tensions persist. A ceasefire in Ukraine is a marginally positive outcome for Europe, although it is not a long-term peace treaty.

We examine Treasury market valuation and look for indicators that could help us time the next peak in yields. We also update the forecasts from our Treasury yield model.

Inauguration Day or shortly thereafter will see either a global tariff of 10% or targeted but substantial tariffs on China, Mexico, and Canada. Treasury yields will rise on tax cuts, the dollar will stay strong, yet oil will also continue to rally, causing equity volatility in the near term.

To kick start our new research agenda at Equity Analyzer, we welcome you to our weekly screener report. Each week we will deliver three screeners highlighting stocks exposed to various macro and investment views and themes, that have either been suggested by various BCA strategies, such as the Global Investment Strategy, or are based on research by the Equity Analyzer team. In our first installment, we take a look at US Tech stocks, equity sentiment, and quality "bubble" stocks.

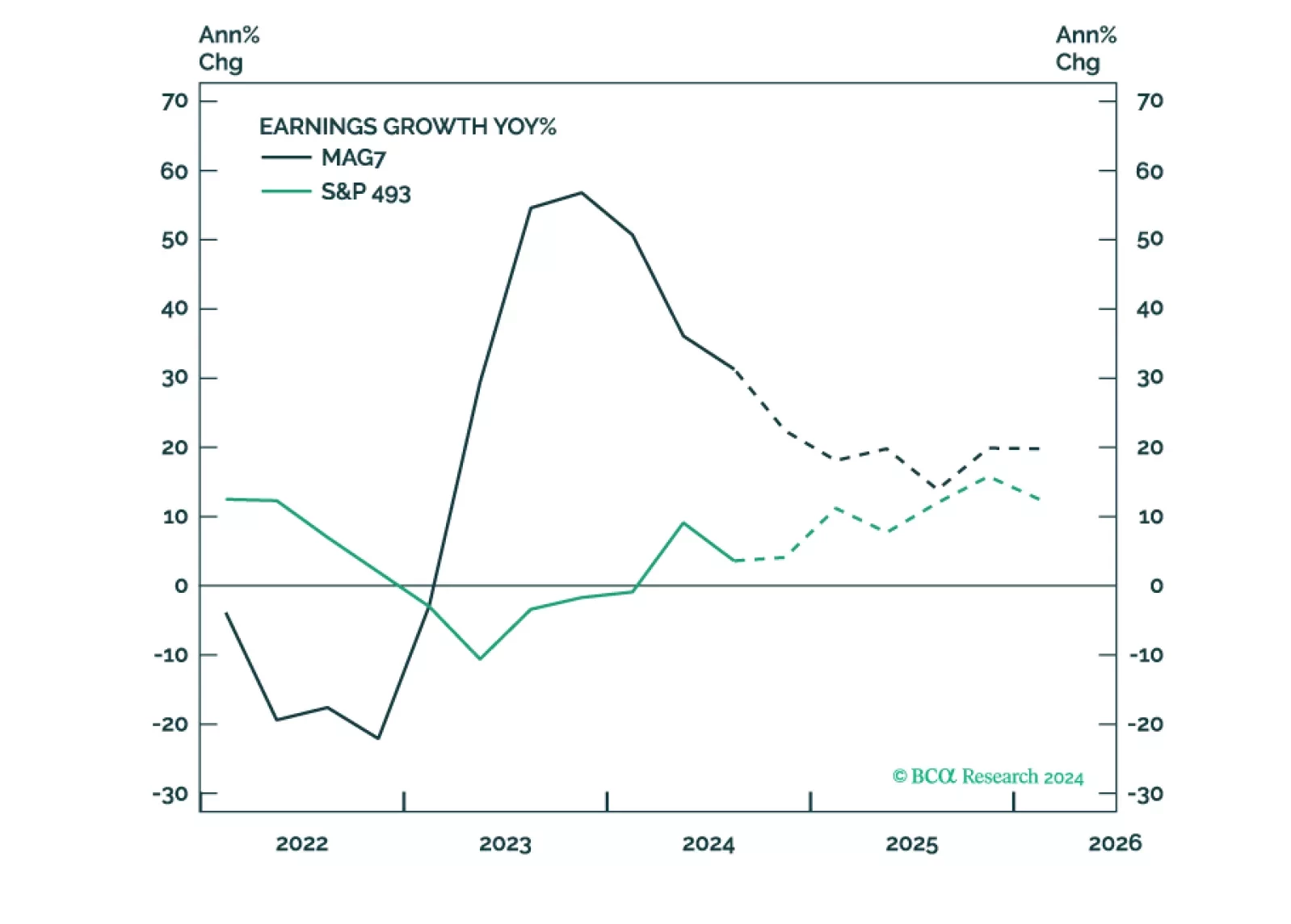

Trump's policies aim to support domestic producers and will be pro-growth and inflationary, at least initially. This environment is supportive of equities. Earnings will likely be strong, but elevated valuations make equities prone to a correction. Earnings growth broadening will translate into performance broadening – the S&P 493, Cyclicals, Value, Small and Mid are likely to outperform.

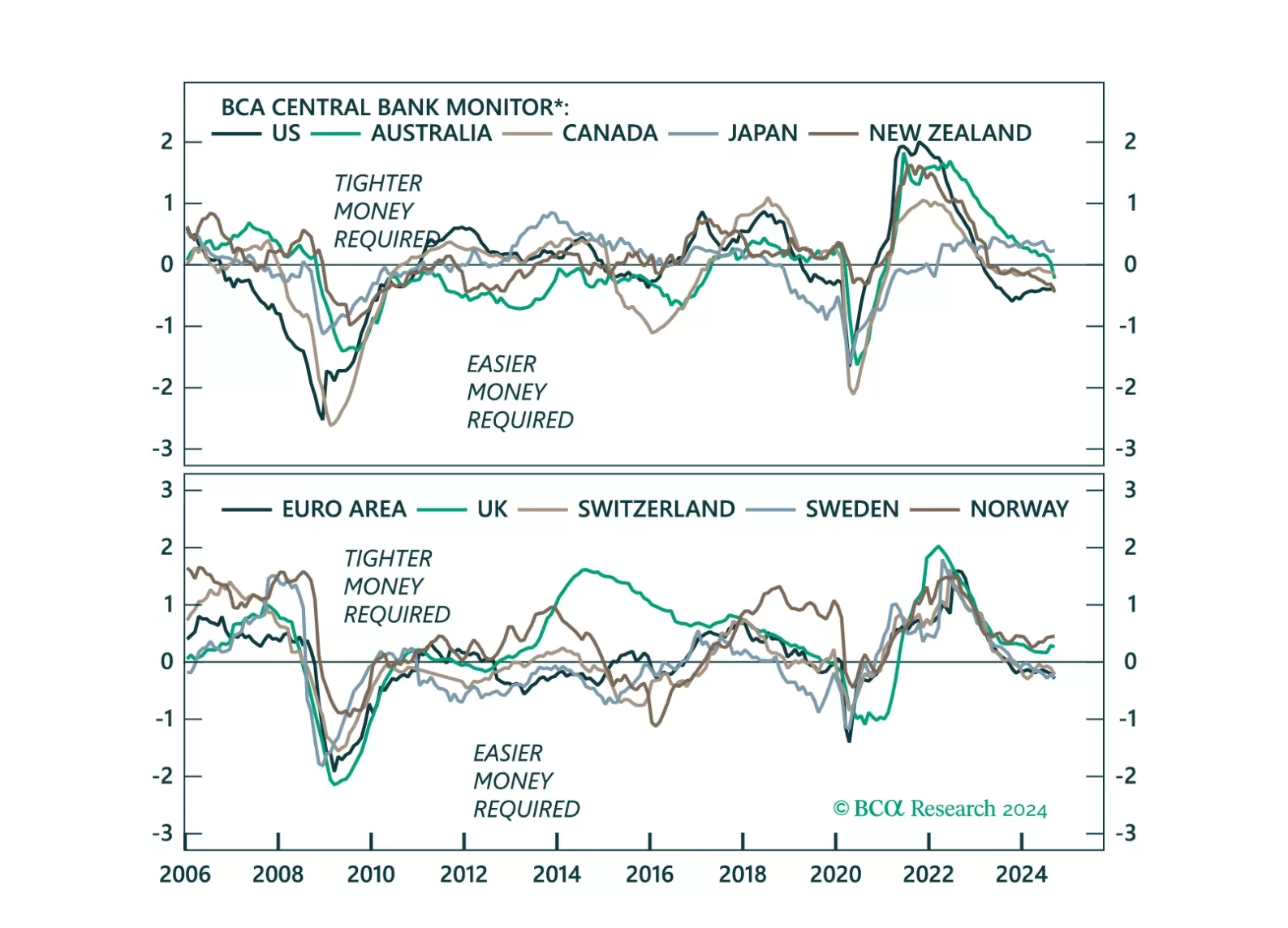

This week, we update our Central Bank Monitors (CBMs), that help us calibrate how monetary policy should be adjusted in developed-market economies. Our conclusion is that while overall, easier monetary settings are required, there a few trade ideas that arise from the divergences in signals amongst G10 countries.

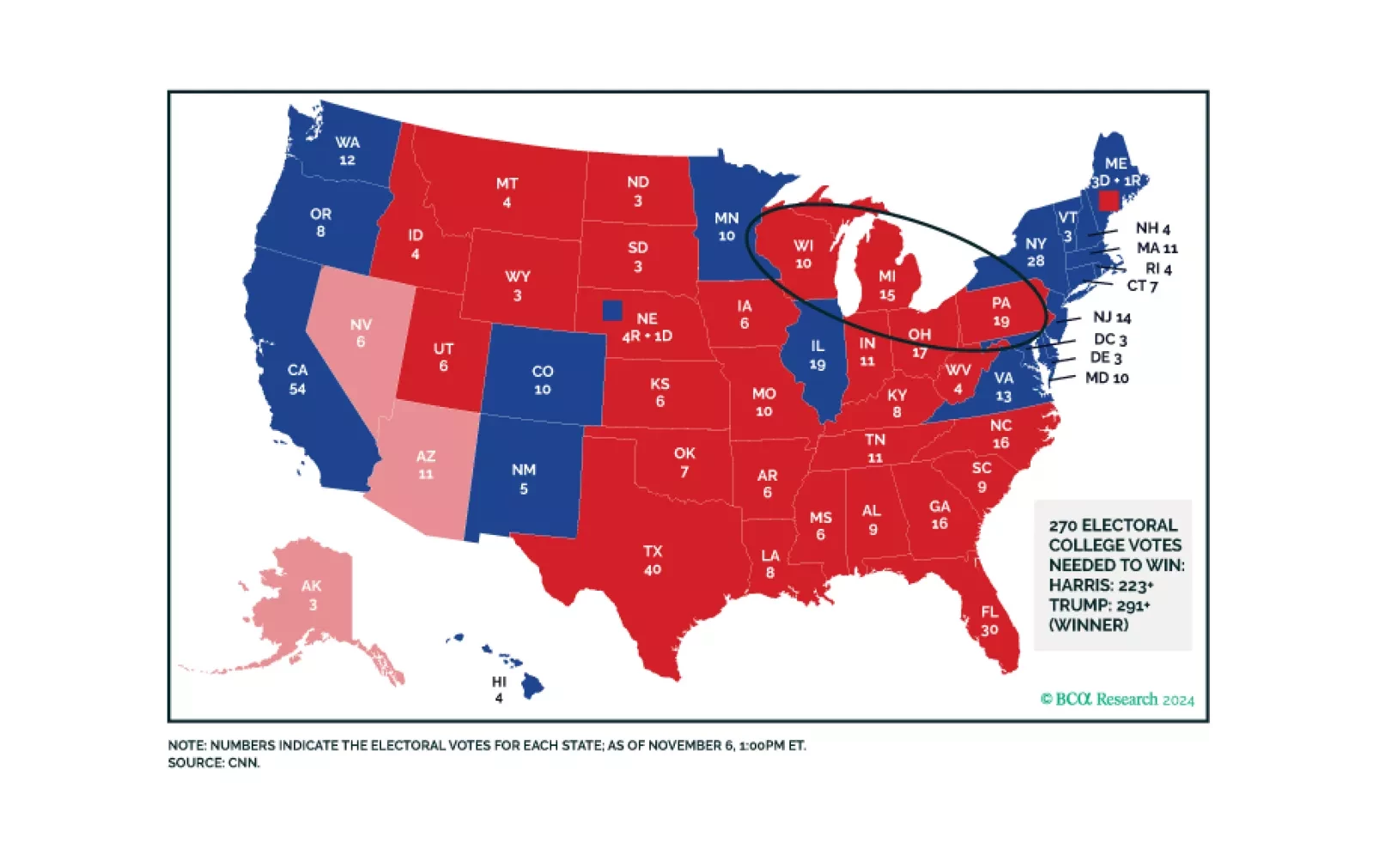

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.