Base Metals & Iron Ore

In this Special Report, we outline the three themes that we believe will drive commodity markets this year: (1) demand growth will remain sluggish across cyclical commodities (2) supply-side developments will ultimately be bearish for oil prices, and (3) traditional relationships between commodity prices and financial variables may not hold.

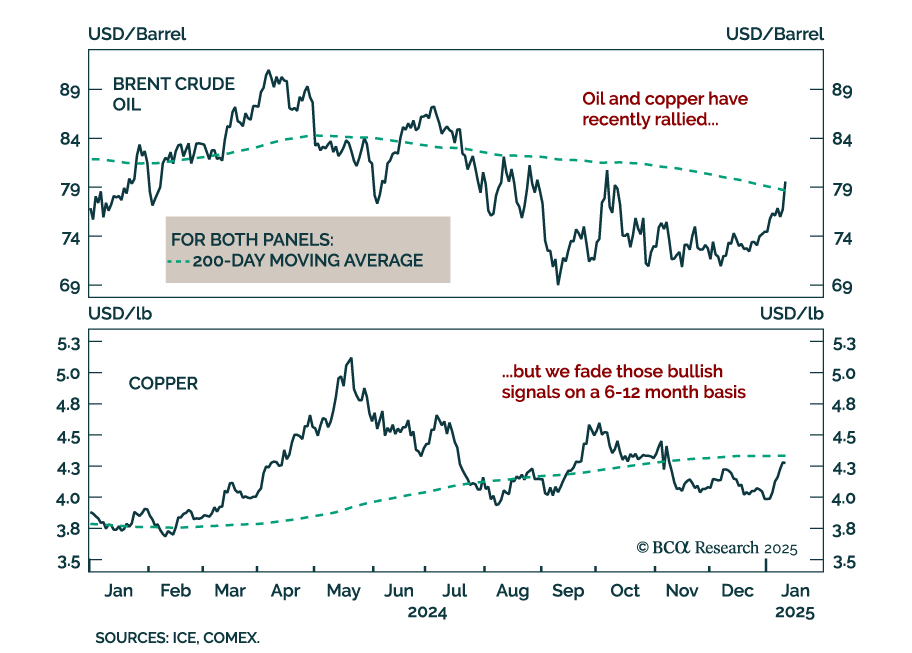

Despite a strong dollar, rising yields, and falling equities, oil and copper prices have recently risen. Oil has broken out above its 200-day moving average, while copper is currently testing its own. Oil’s bullish price action is explained by…

Our Emerging Markets, China, and Commodities strategy teams published their 2025 joint outlook. Our colleagues remain bullish on the US dollar for now but see rising odds of the Trump administration actively pursuing greenback devaluation. To avoid steep…

Our Commodity & Energy Strategy team evaluated the impact of president-elect Trump’s policies on commodity markets. Trump’s energy policies, while promoting increased domestic oil production, are unlikely to drive immediate growth in US crude output.…

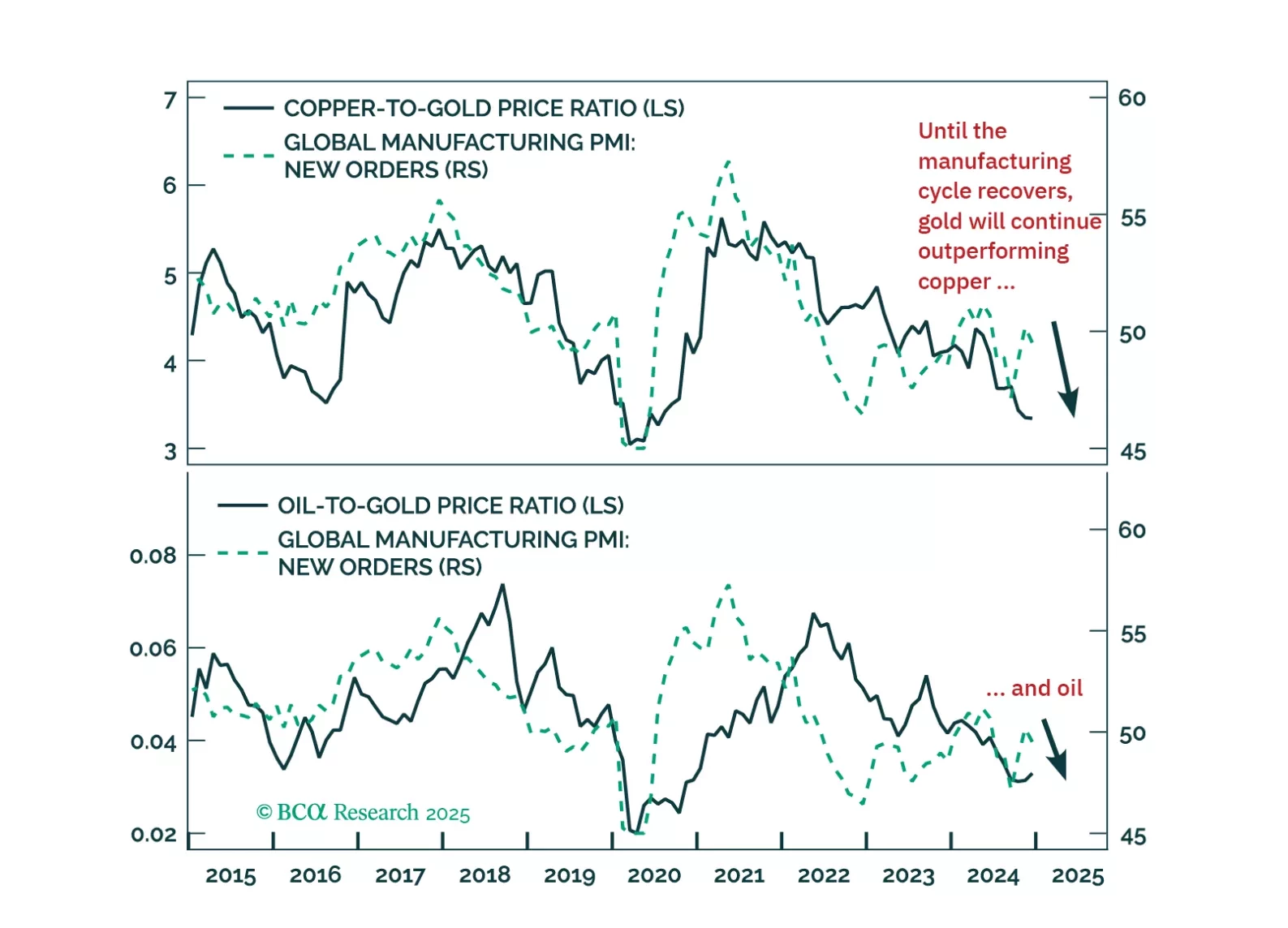

Our Commodity and Energy strategists believe a supply-demand deficit will emerge in 2026, and widen into the end of the decade. Copper demand is set to grow over 4% annually between 2025 and 2030, fueled by the green energy transition, data center…

Speculators have supported copper prices as demand growth slowed below the pace of supply growth. Our Commodity and Energy Strategy colleagues believe this does not bode well for the metal. The copper market faces a situation where demand growth will be…

In a trendless yet volatile year for oil, Israel’s retaliatory attack on Iran this weekend is a reminder the outlook is fraught with geopolitical risks. Risks are usually expressed as a geopolitical price premium, but this weekend’s events point to a…

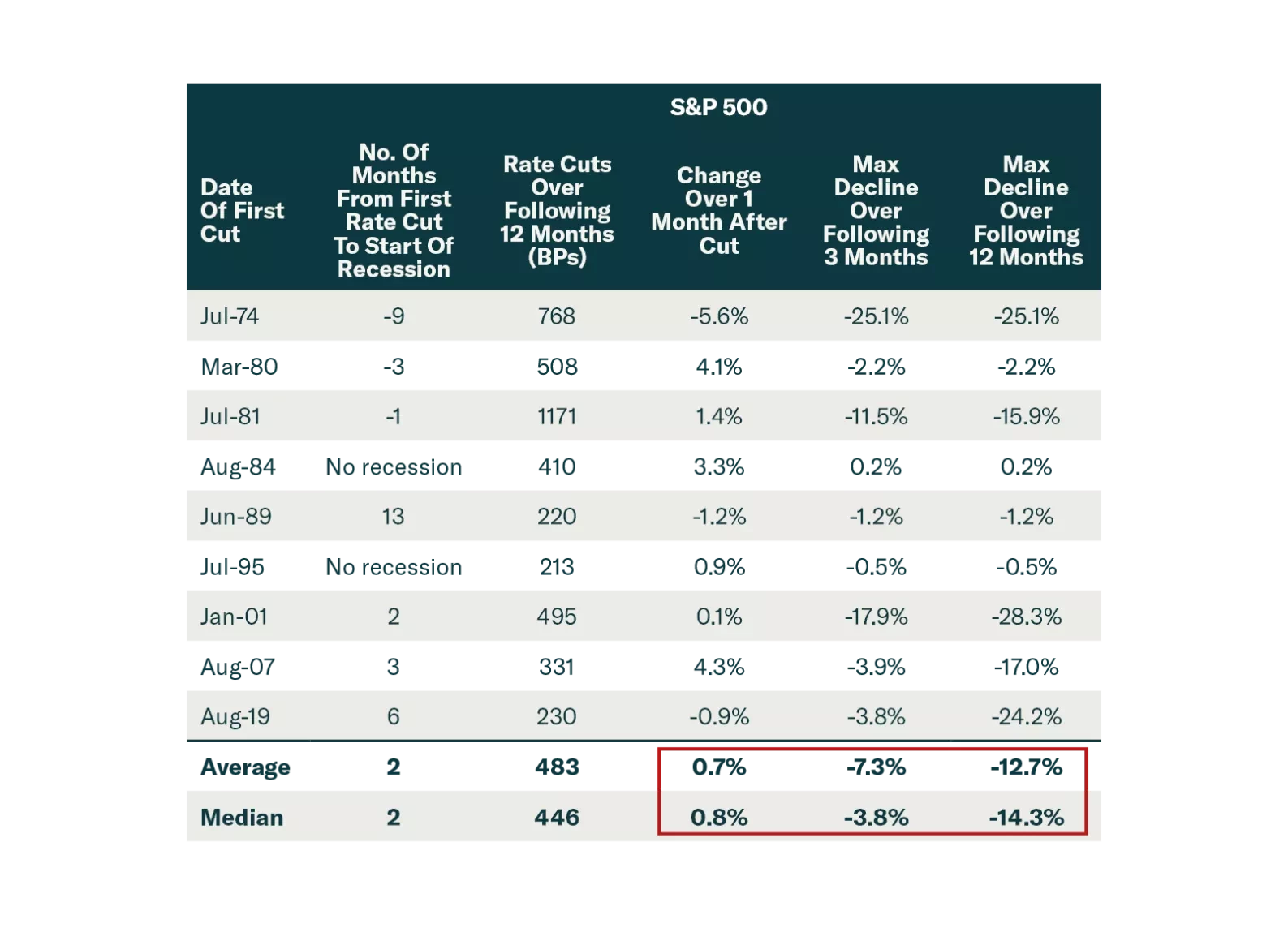

The market got excited by the 50 bps Fed cut and China stimulus. But these are a recognition that economies are slowing significantly. Stocks often rally after the first Fed cut, before falling sharply. Investors should stay defensive.

One commodity that has not reacted to the bullish demand-side news from the Politburo (see The Numbers) is crude oil. Brent shed over 2% on Thursday, in sharp contrast to Copper’s gains. Oil markets seem to be reacting to a bearish supply-side development…

The PBoC announced further measures to stimulate the economy on Tuesday. It lowered the reserve requirement ratio from 10% to 9.5%, cut the 7-day reverse repo rate by 20 bps (following Monday’s 10 bps cut to the 14-day reverse repo rate), lowered borrowing…