Base Metals & Iron Ore

Industrial metals returned a whopping 6% over the past week. Bullish investor sentiment is likely driving these gains. The soft-landing narrative has been gaining traction in recent days with markets pricing in increased odds of an outsized 50-bps Fed rate…

As an industrial metal, copper acts as a barometer of economic activity. Silver and gold are safe-haven assets with inflation-hedging properties, though silver is relatively more sensitive to global growth developments given that industrial applications…

According to BCA Research’s Commodity & Energy Strategy service, central banks will continue to be a key source of gold demand. Central bank purchases in the first half of this year exceeded first-half purchases in every year they’ve been tracked going…

The Q2 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Nearly 80% (60%) of companies have topped earnings (sales) expectations in Q2, according to Factset. Excluding Materials and Real…

Industrial metals were one of the worst performing asset classes last month. Have prices declined enough to make them an attractive investment? The outlook for industrial commodity prices is bearish over a 12-month horizon given we expect the US economy to…

Chinese exports in USD terms missed expectations in July, growing by 7.0% y/y, down from 8.6% in June. Conversely, imports rebounded smartly from a 2.3% contraction, rising by 7.2% in July and upending expectations of 3.2%. Slower export growth is…

According to BCA Research’s Commodity & Energy Strategy service, robust iron ore imports are sending a false signal about steel demand. Instead, these supplies are being used to restock inventories. By the end of last year, iron ore stocks at Chinese…

Brent prices have fallen 6% so far in July, reversing their June gains. Interestingly, these losses are occurring despite escalating Middle East tensions and quickening Chinese industrial profit growth in June (see The Numbers), both of which are…

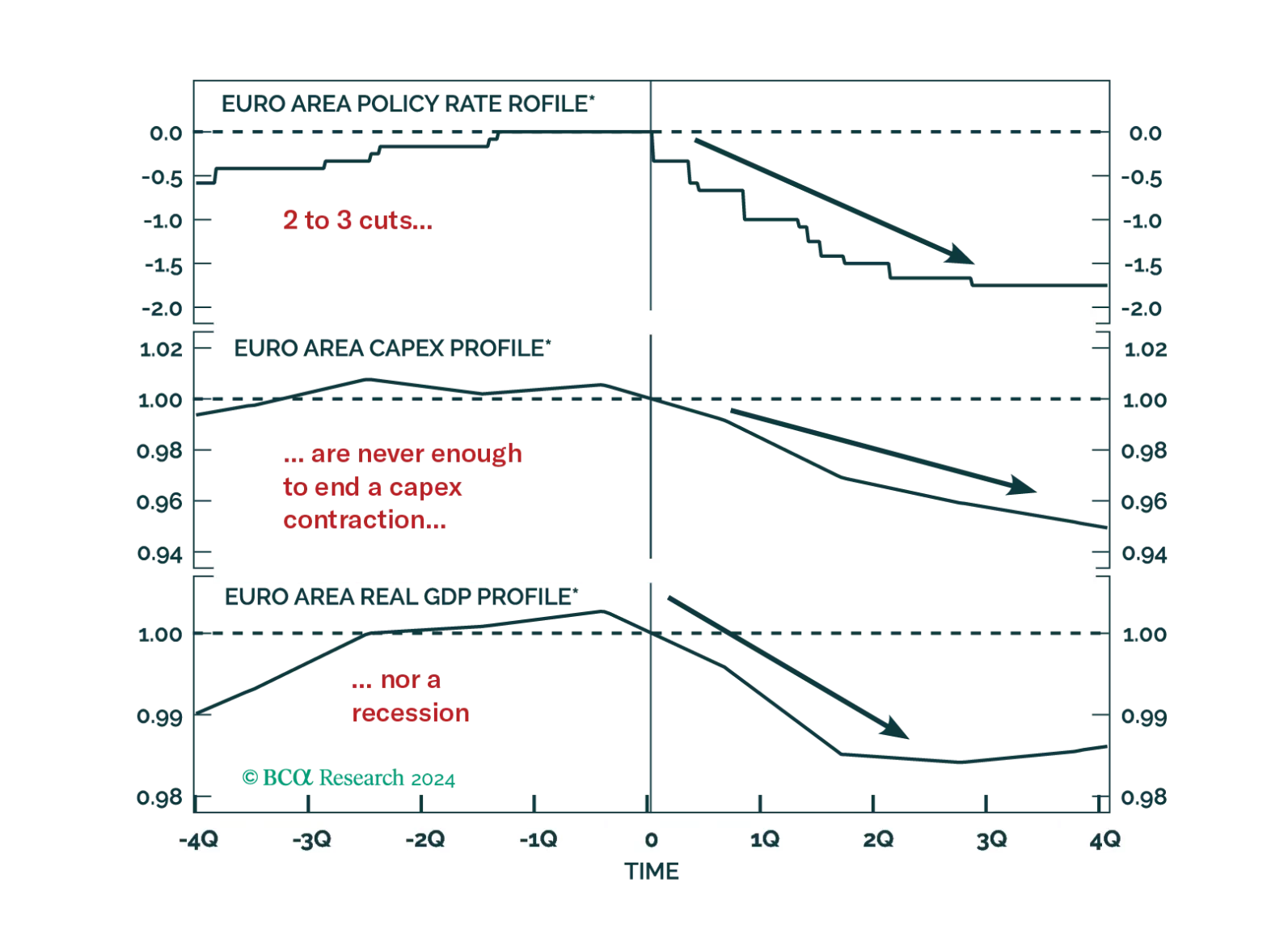

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

Copper has experienced a roller-coaster ride so far this year, with front-month futures on the Chicago Mercantile Exchange gaining nearly 40% from early February to late May, tumbling nearly 15% in just over five weeks, and bouncing around 7% over the last…