Brazil

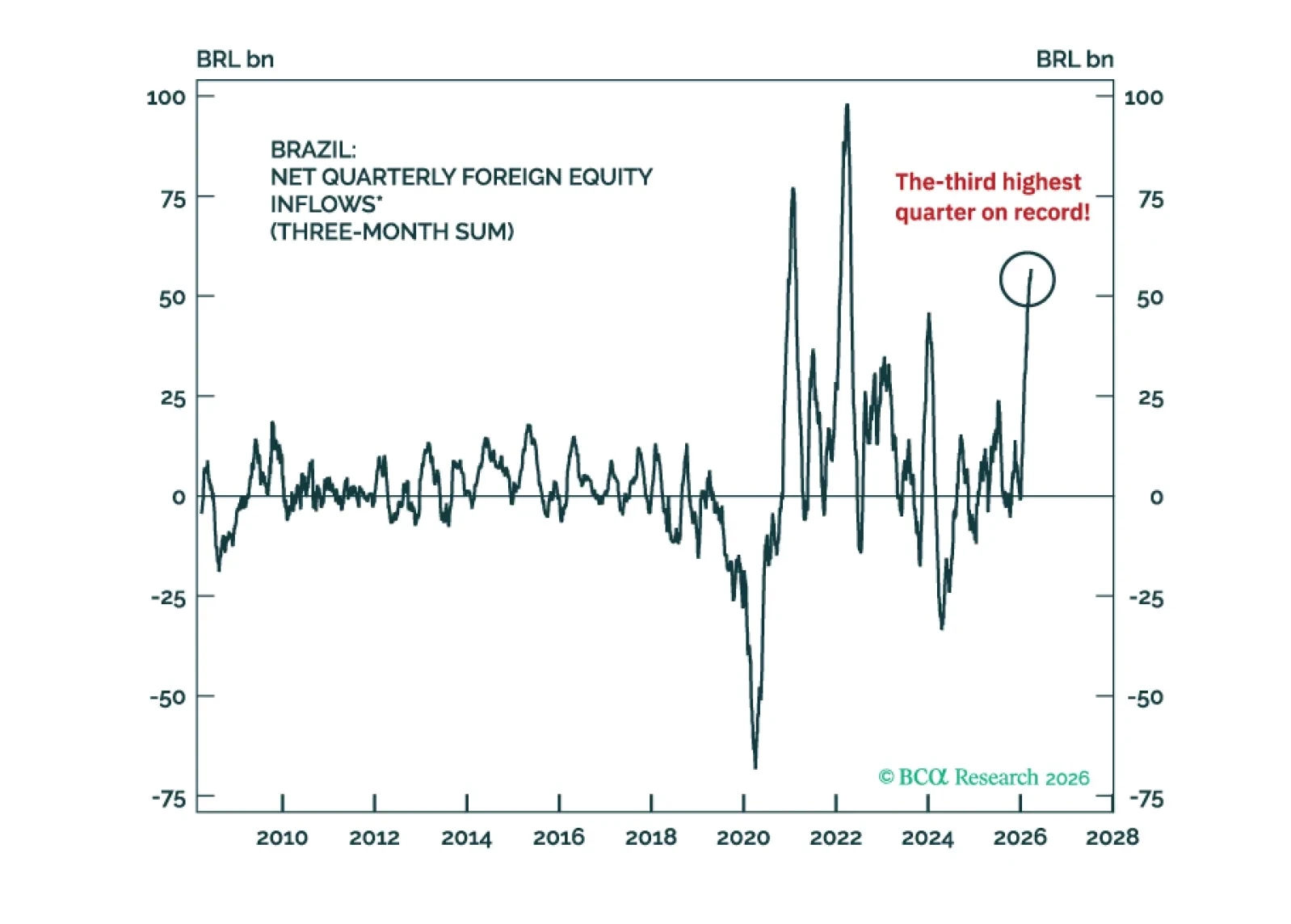

Overstretched foreign inflows into Brazilian markets will reverse, while soaring oil prices will not benefit Brazil in the near term. Avoid the country’s risk assets and the BRL, and stay underweight Brazilian equities and fixed income relative to EM. We also recommend paying 10-year Brazilian swap rates.

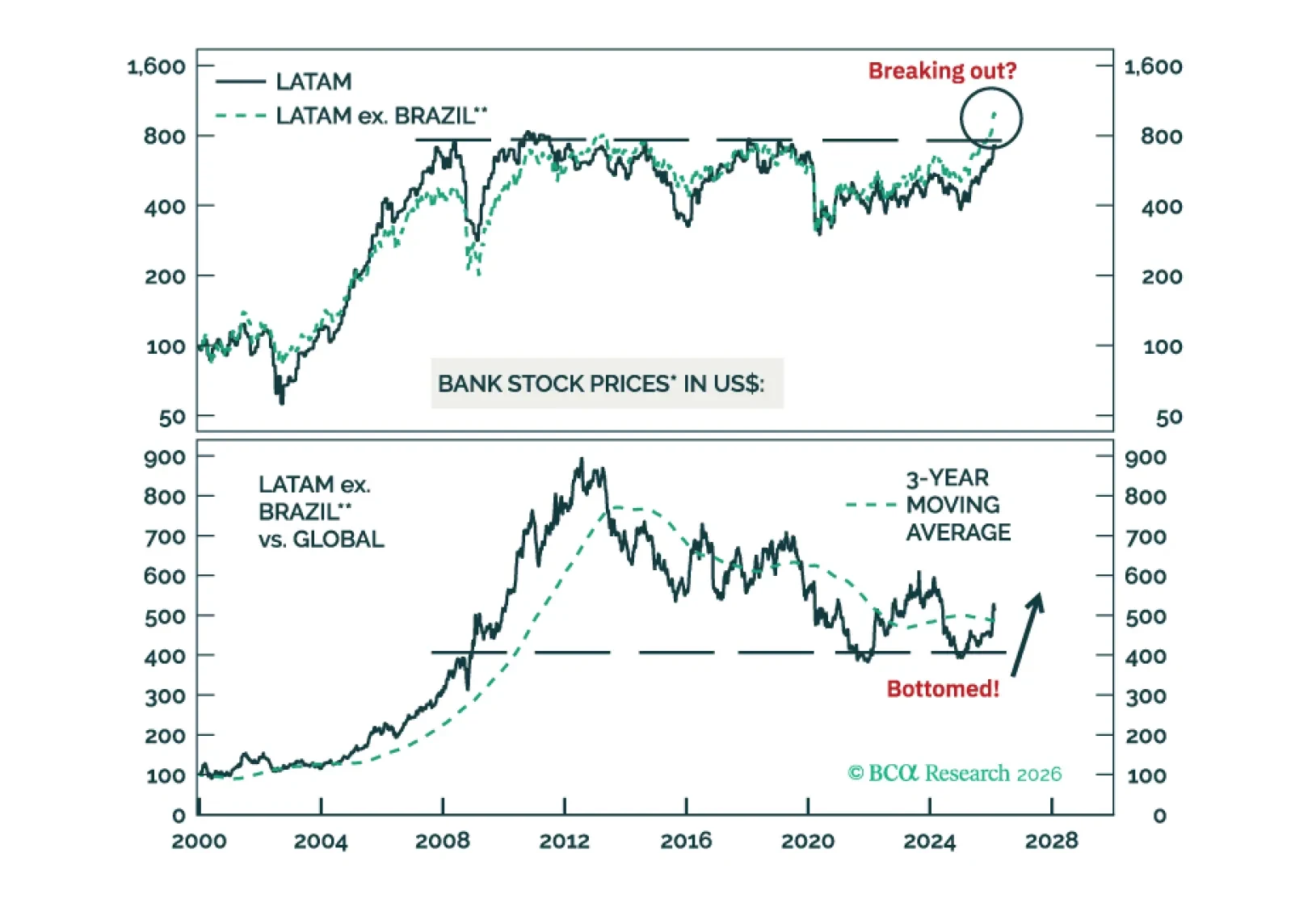

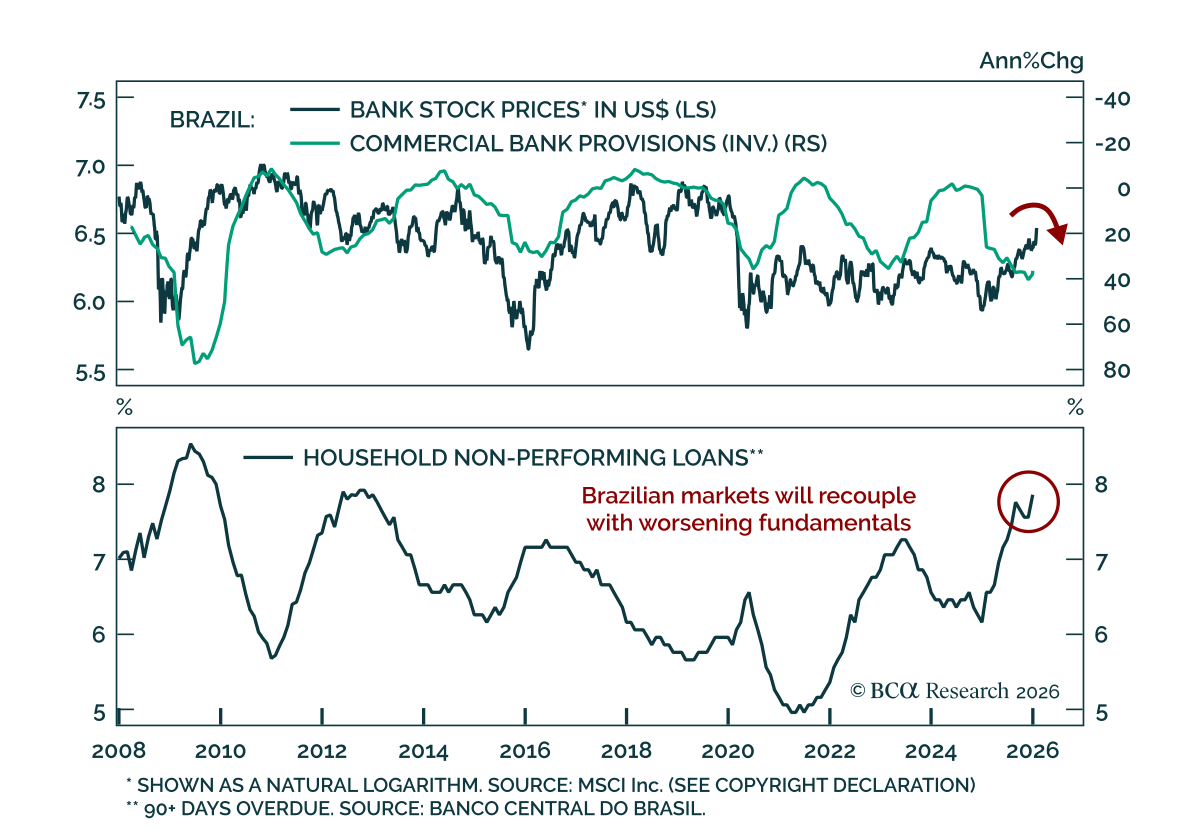

Go long LATAM ex. Brazil banks / short global bank stocks. Brazilian bank equities will underperform due to poor and worsening macro fundamentals.

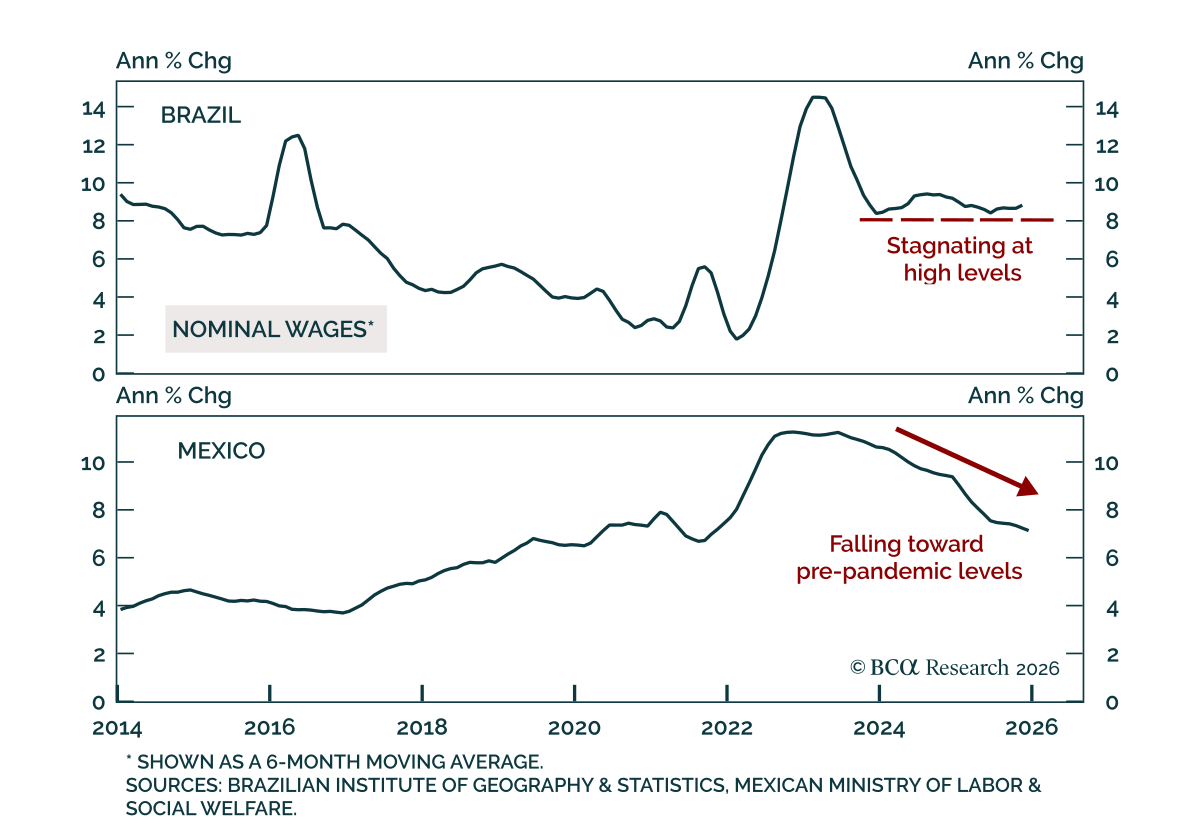

Despite similar headline inflation, underlying dynamics favor Mexico over Brazil across EM assets. Brazil’s latest CPI print was in line with consensus at 4.44%, near the upper end of the target range. In Mexico, inflation surprised modestly to the downside…

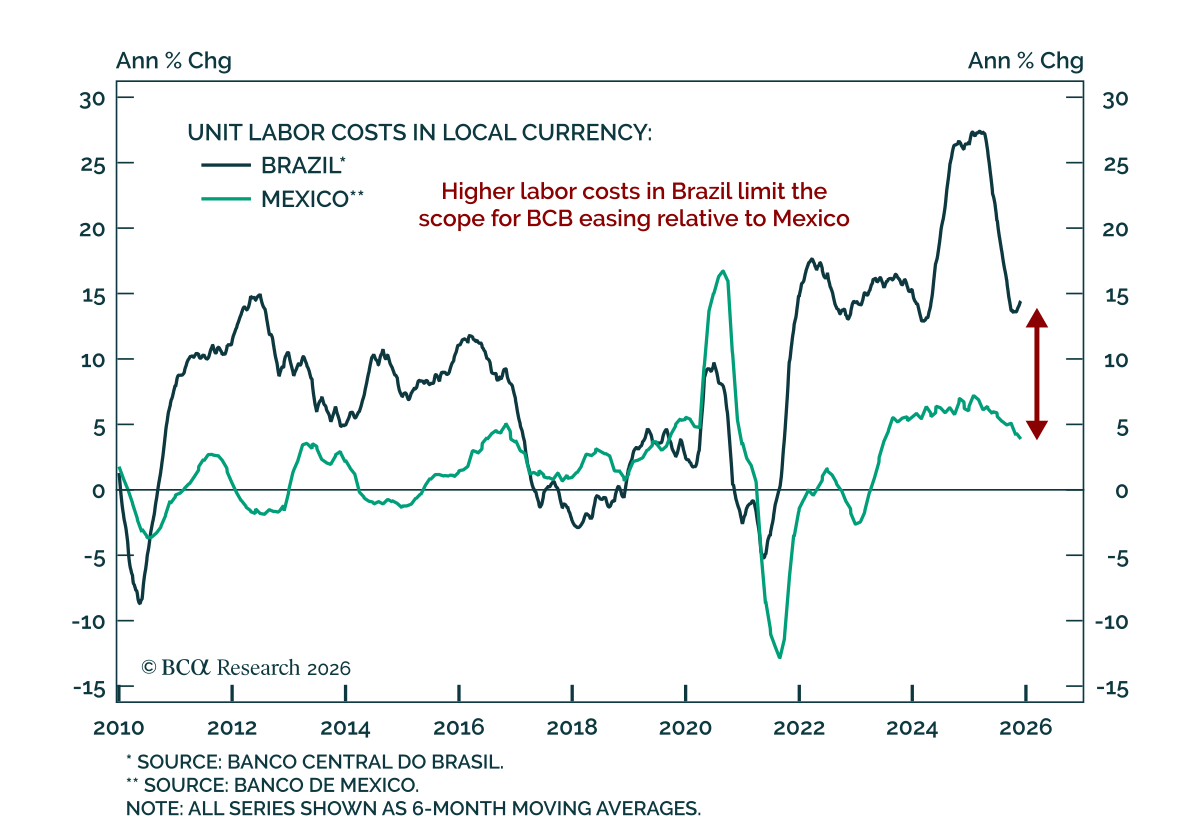

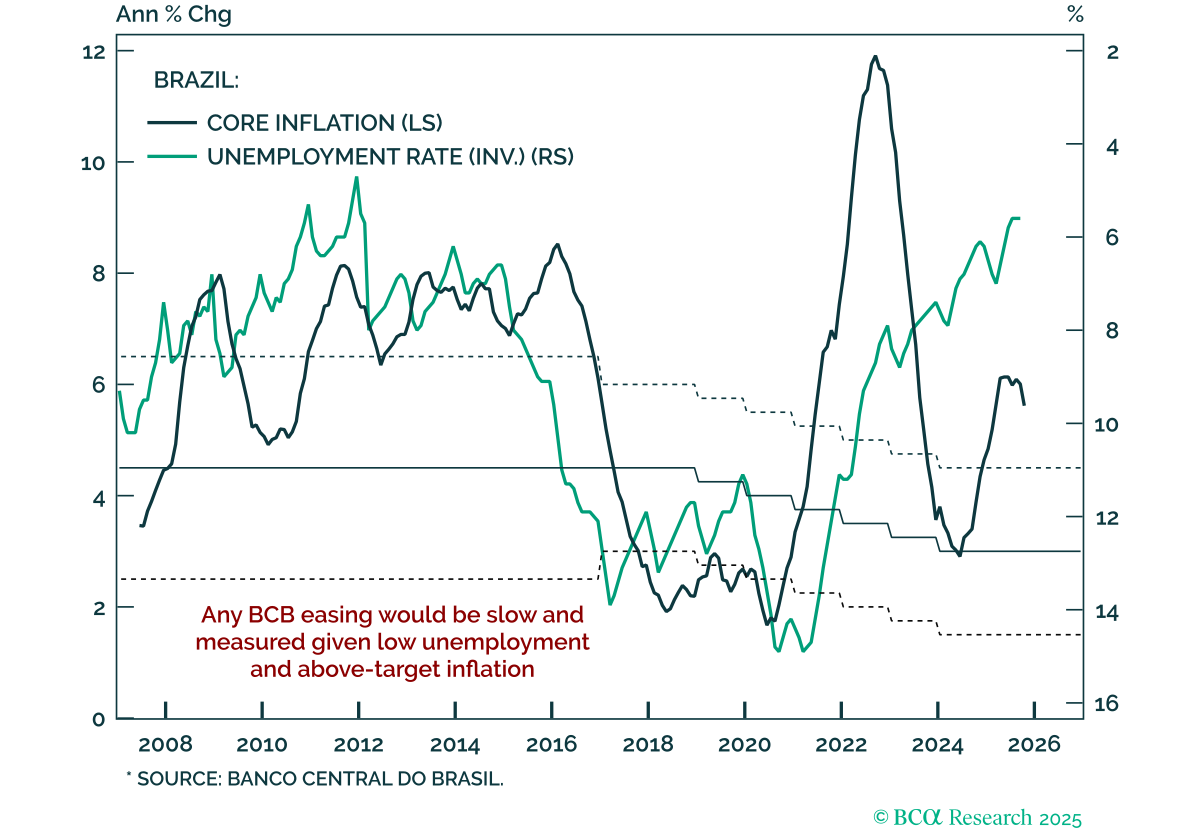

Brazilian risk assets will underperform global peers on the back of ultra hawkish monetary policy. The Brazilian Central Bank (BCB) opted to hold interest rates at 15% due to still elevated inflationary pressures. The decision will reinforce a…

Although inflation has fallen within the upper end of the target range in both of LatAm’s largest economies, our EM strategists are more constructive on monetary easing and financial markets in Mexico than in Brazil. Mexico’s latest CPI prints surprised to…

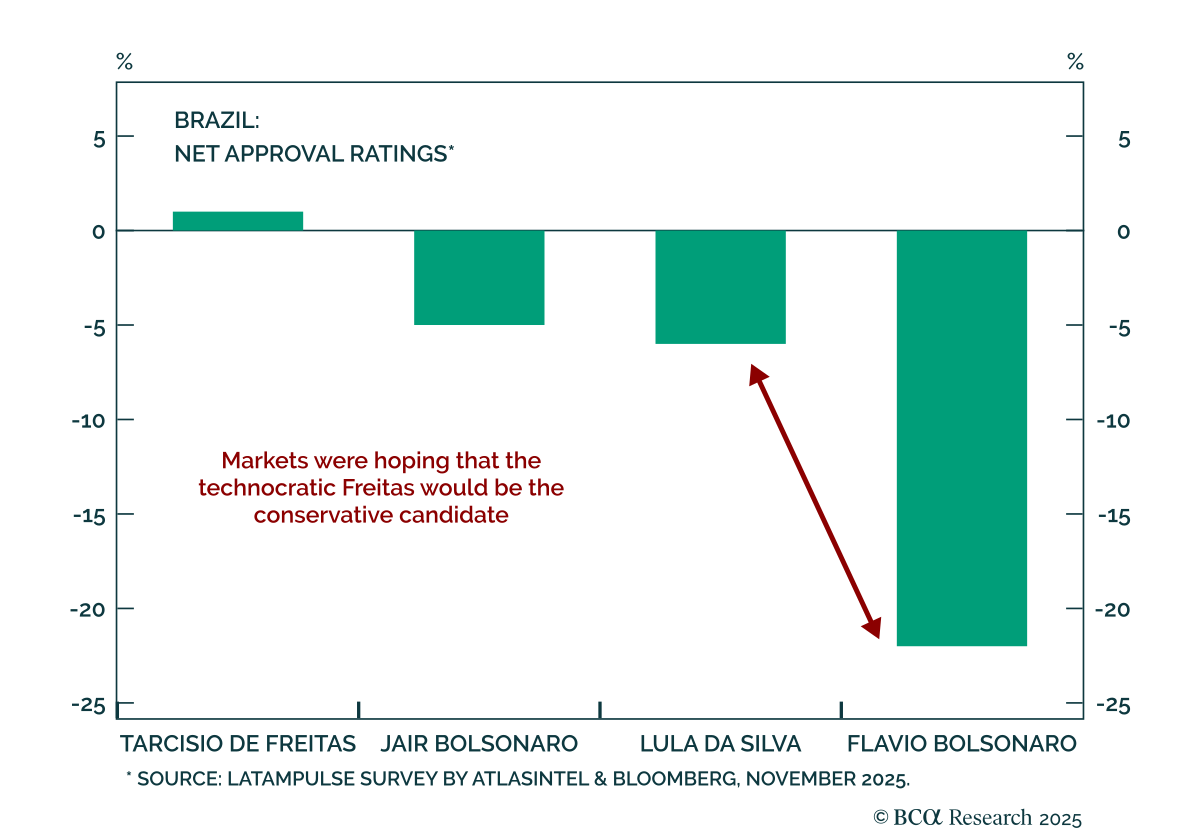

Brazil’s financial markets are on shaky ground following the central bank’s hawkish meeting and disappointing political developments, reinforcing our negative view on the country’s risk assets. The three pillars of this year’s rally in Brazilian risk assets…

Despite a shift toward an easing bias, a December cut remains unlikely in Brazil. A BCB committee member stated the tightening cycle has ended and the next move could be a cut, shifting the bias from tightening to easing. But a single voice does not influence…

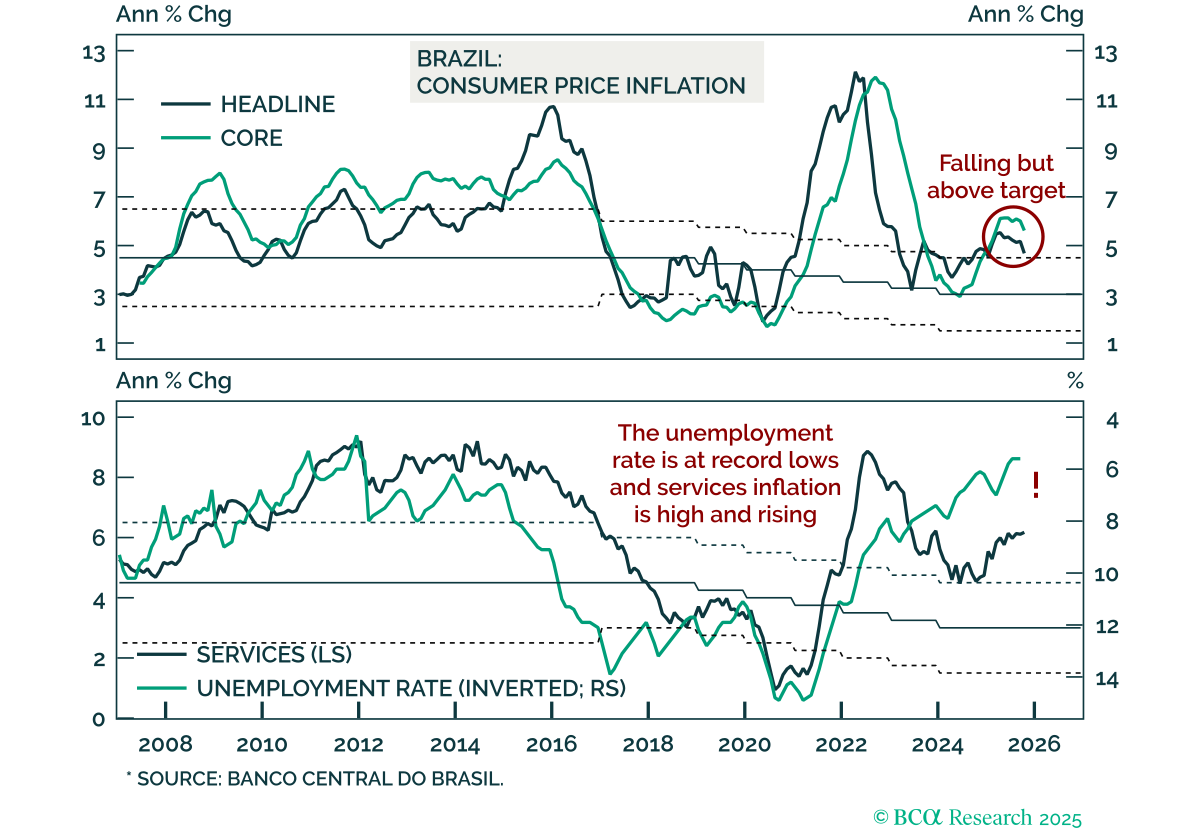

While Brazilian inflation has surprised to the downside, odds are the BCB will not ease anytime soon, creating a headwind for Brazilian markets. The October headline CPI print came in below expectations at 4.68%, lower than the 5.17% recorded in September.…

Our GeoMacro, Geopolitical, and EM strategists remain underweight Brazilian equities, local bonds, and sovereign credit over the next 6–12 months, as structural and macro constraints weigh on the outlook. Brazil has made some reform progress, but changes…

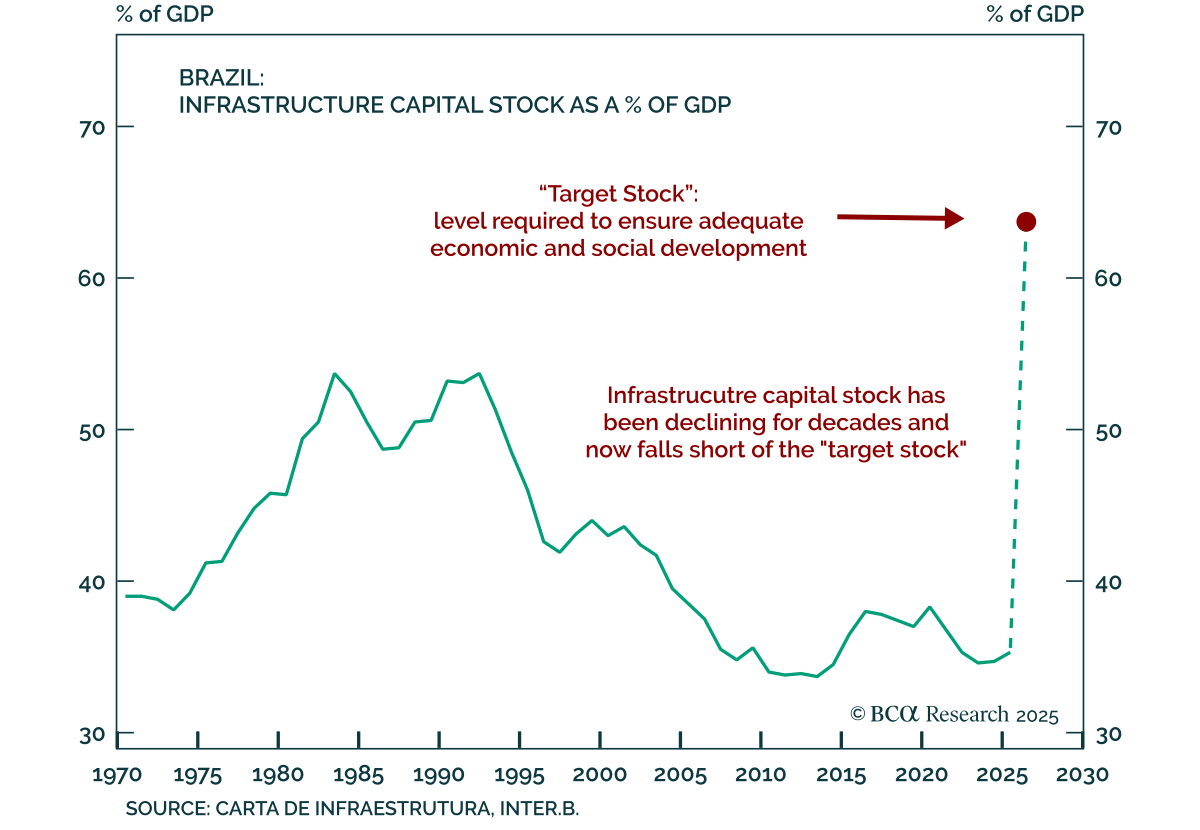

Brazil’s bleak macro outlook persists – rising debt, weak productivity, and political inertia. With 2026 elections looming, genuine reform seems unlikely, though Argentina’s bold turnaround could pressure Brasília to rethink its cycle of governability over growth.