British Pound

This report looks at the latest developments in G10 economies and implications for bond and FX market strategy.

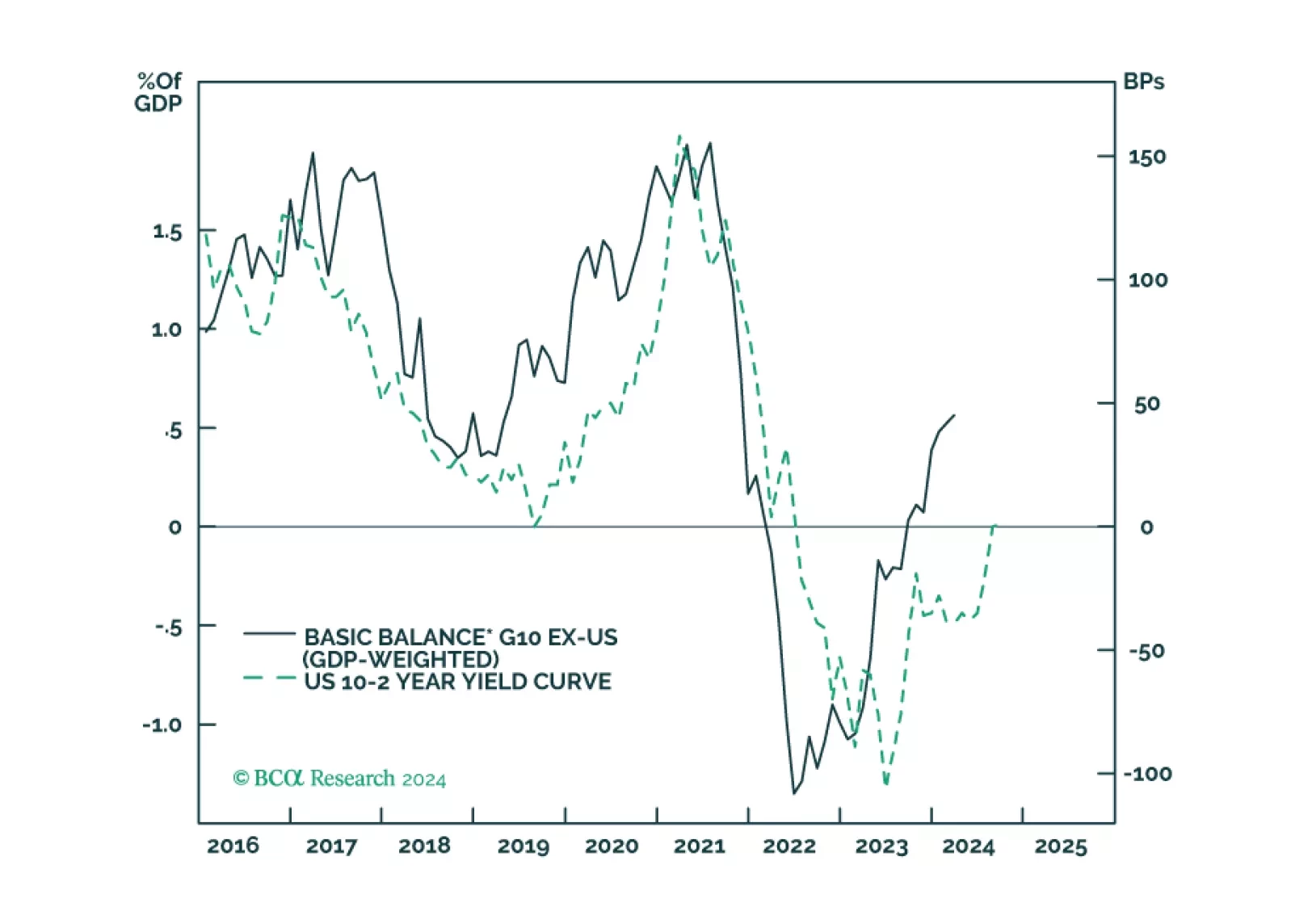

In this monthly review, we give our take on where bond yields and the dollar are headed. This is within the lens of revisiting our fundamental indicators.

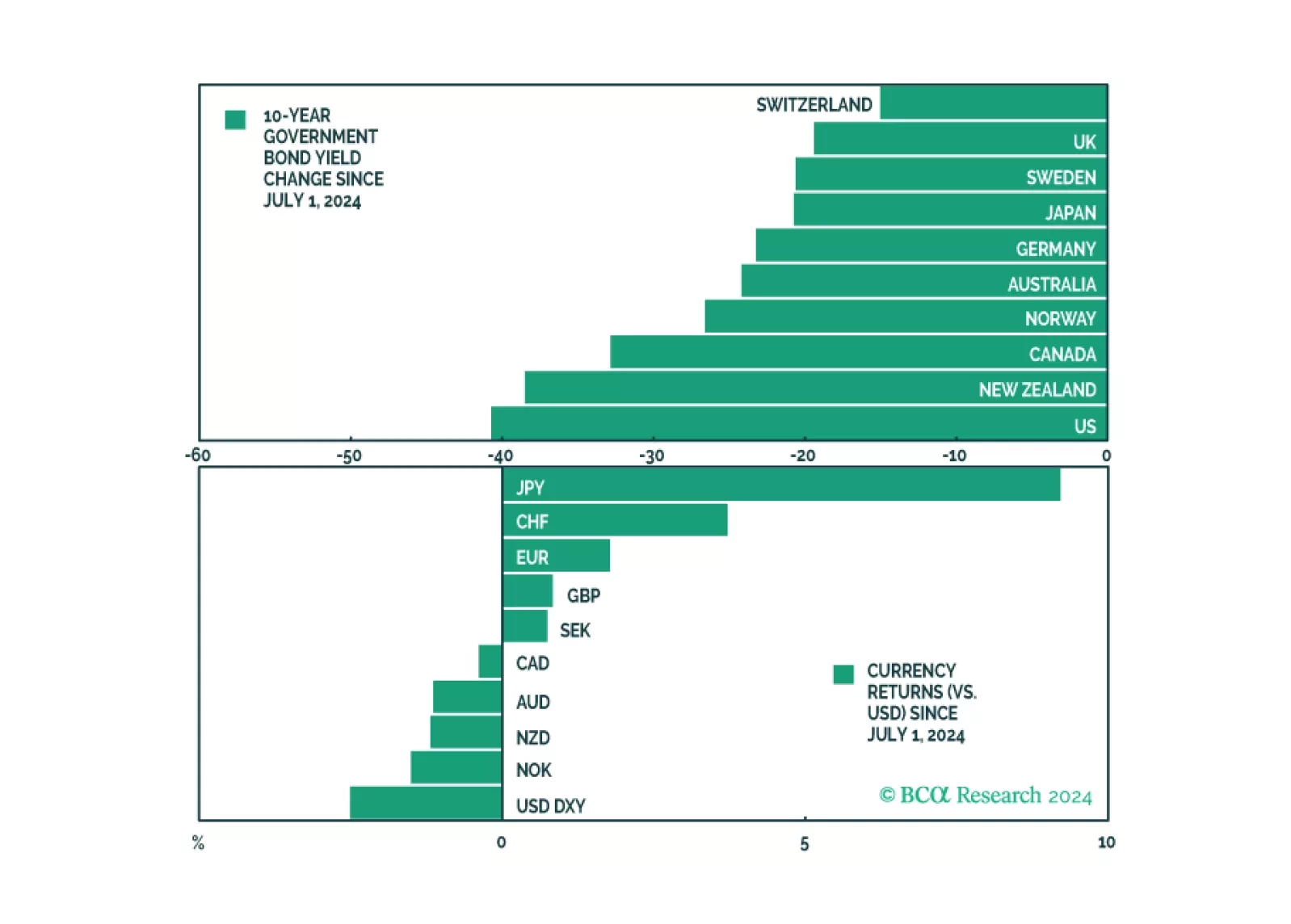

We review some of the key data releases this week that we find have an impact on our currency strategy. Long yen positions make sense today. Long sterling and the euro bets are more of a judgment call, and we will fade any strength in these currencies. This report delves into these nuances, and suggests a few trade ideas.

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.

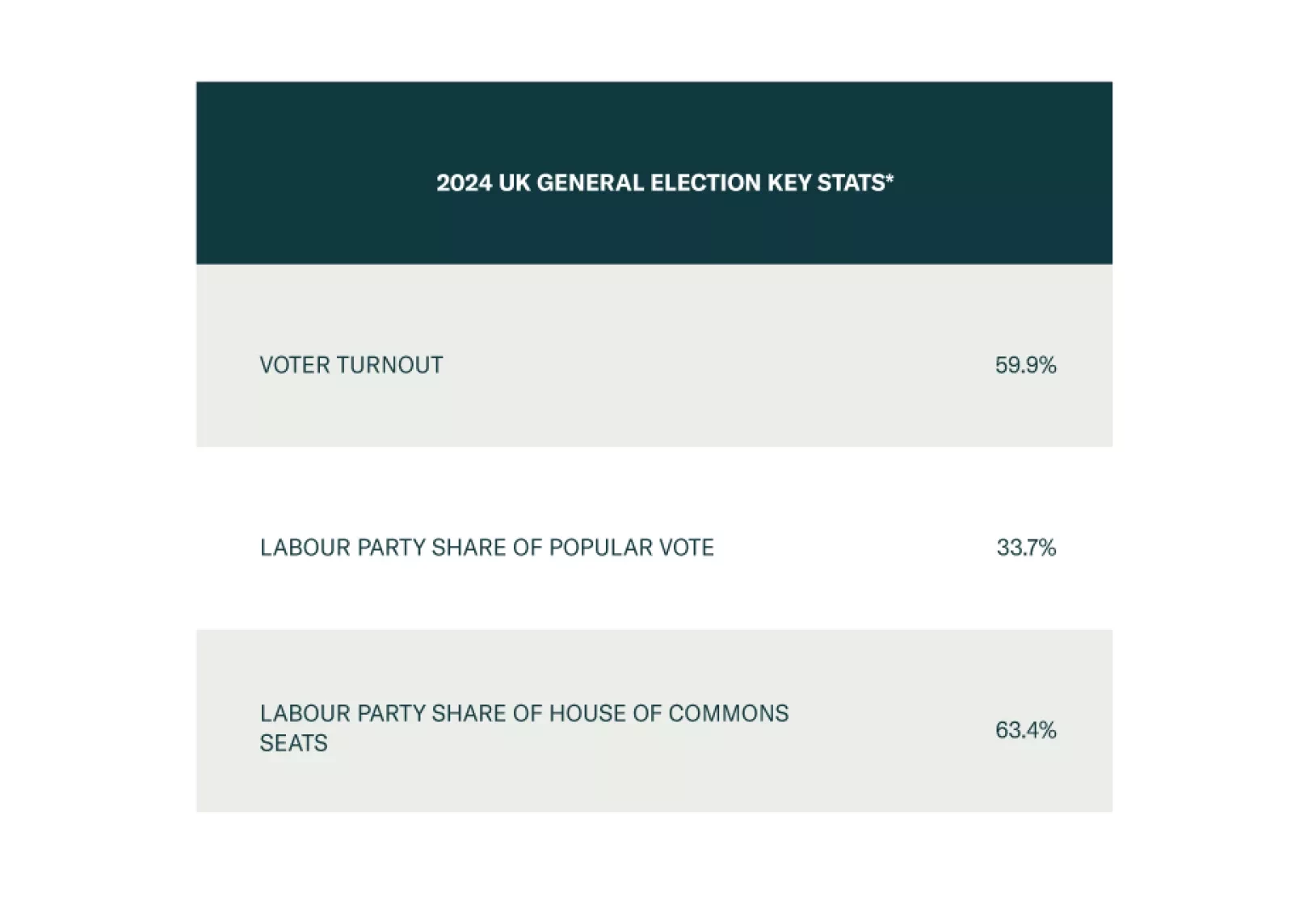

The new Labour government will have flexibility to respond to macro shocks, which is positive for the UK in general, namely GBP-EUR, and also gilts in absolute terms. But over the long run, tax hikes will likely surprise to the upside, which poses a risk to corporate earnings.

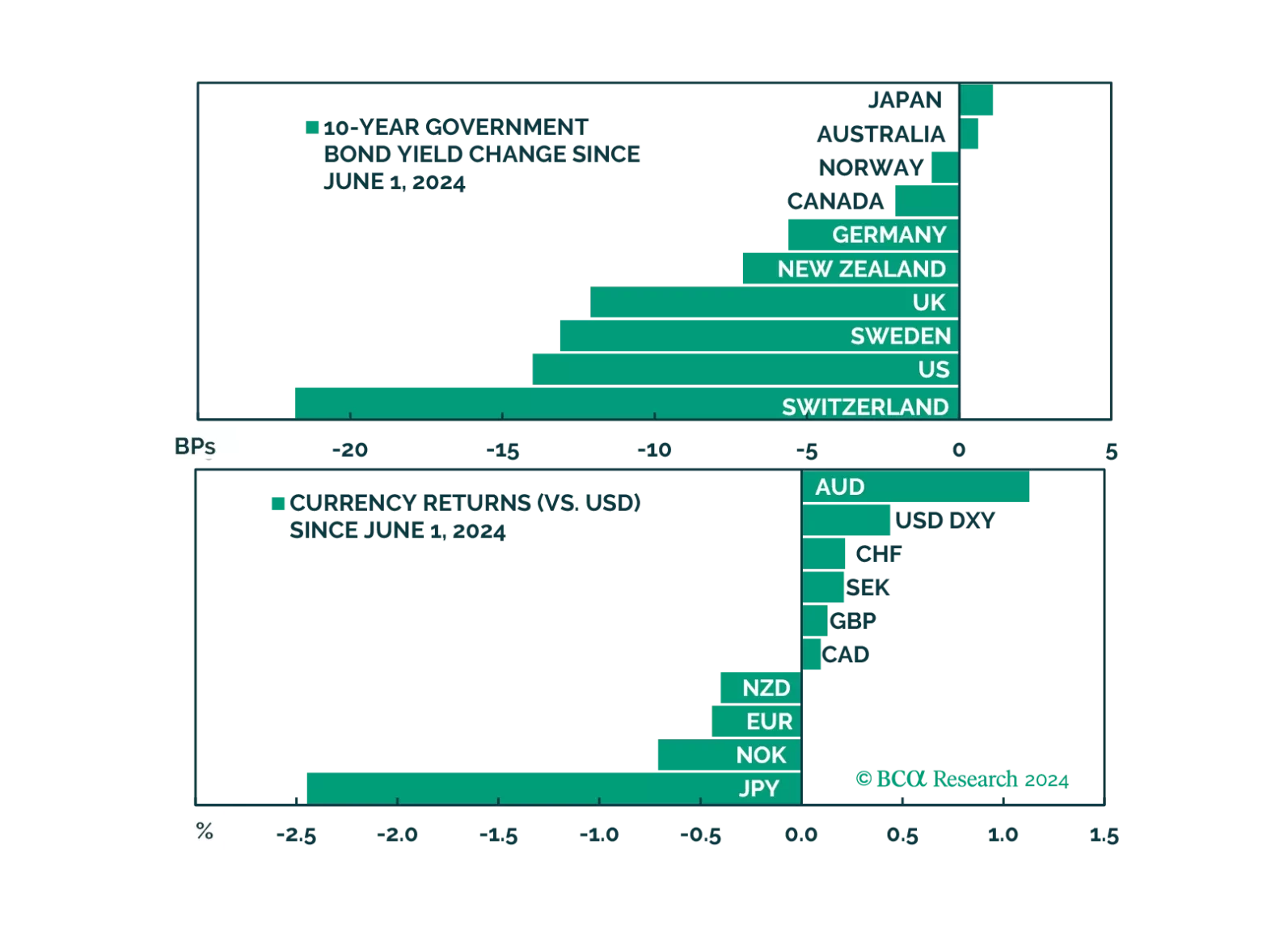

We look at the implications a various European central bank meetings this week, for currency strategy.