Business Cycles

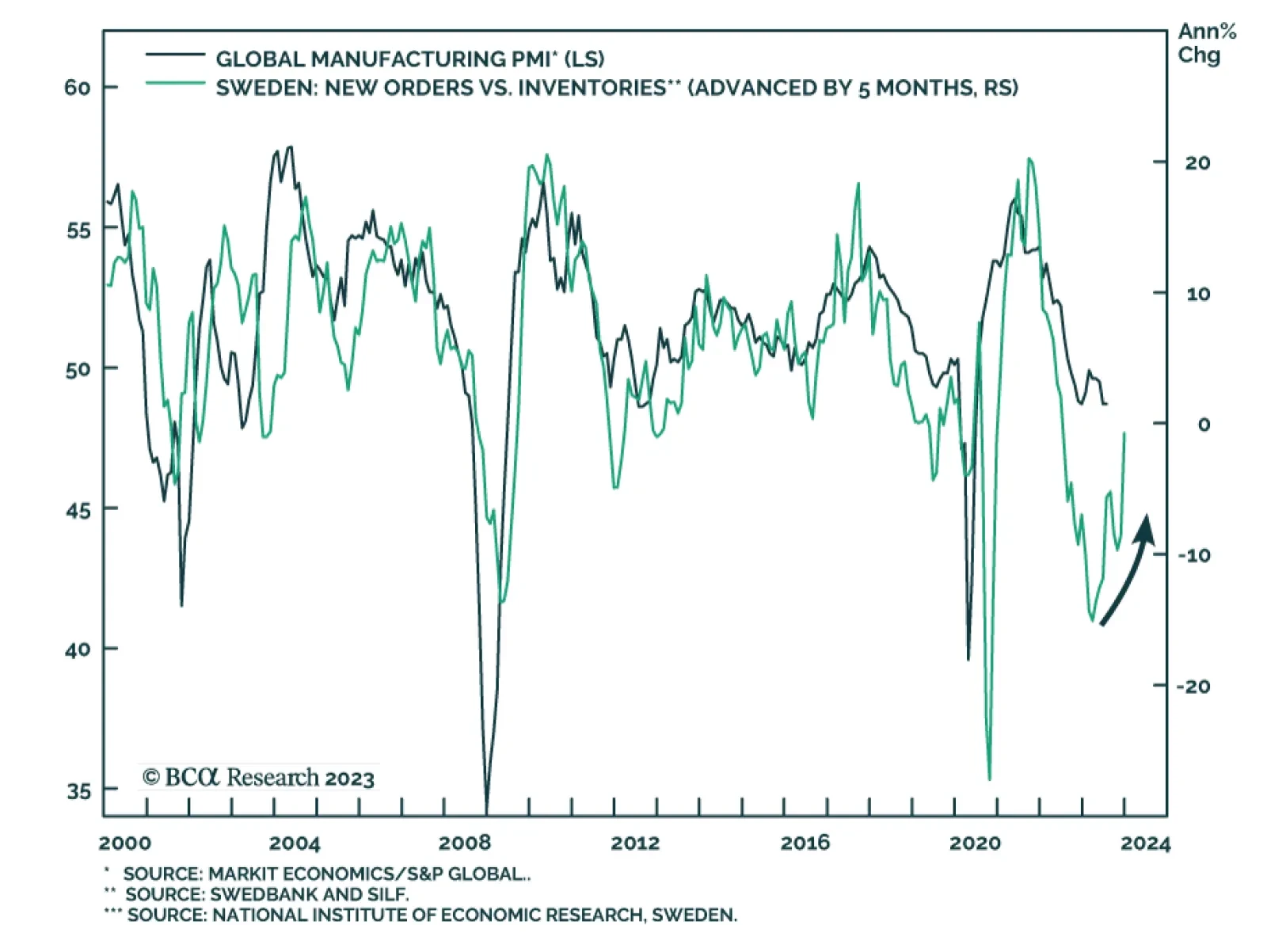

The Global Manufacturing PMI remained unchanged at 48.7 in July, indicating that the pace of decline steadied at the start of the third quarter. The details of the release show accelerating rates of decline in production, new orders, and new export orders.…

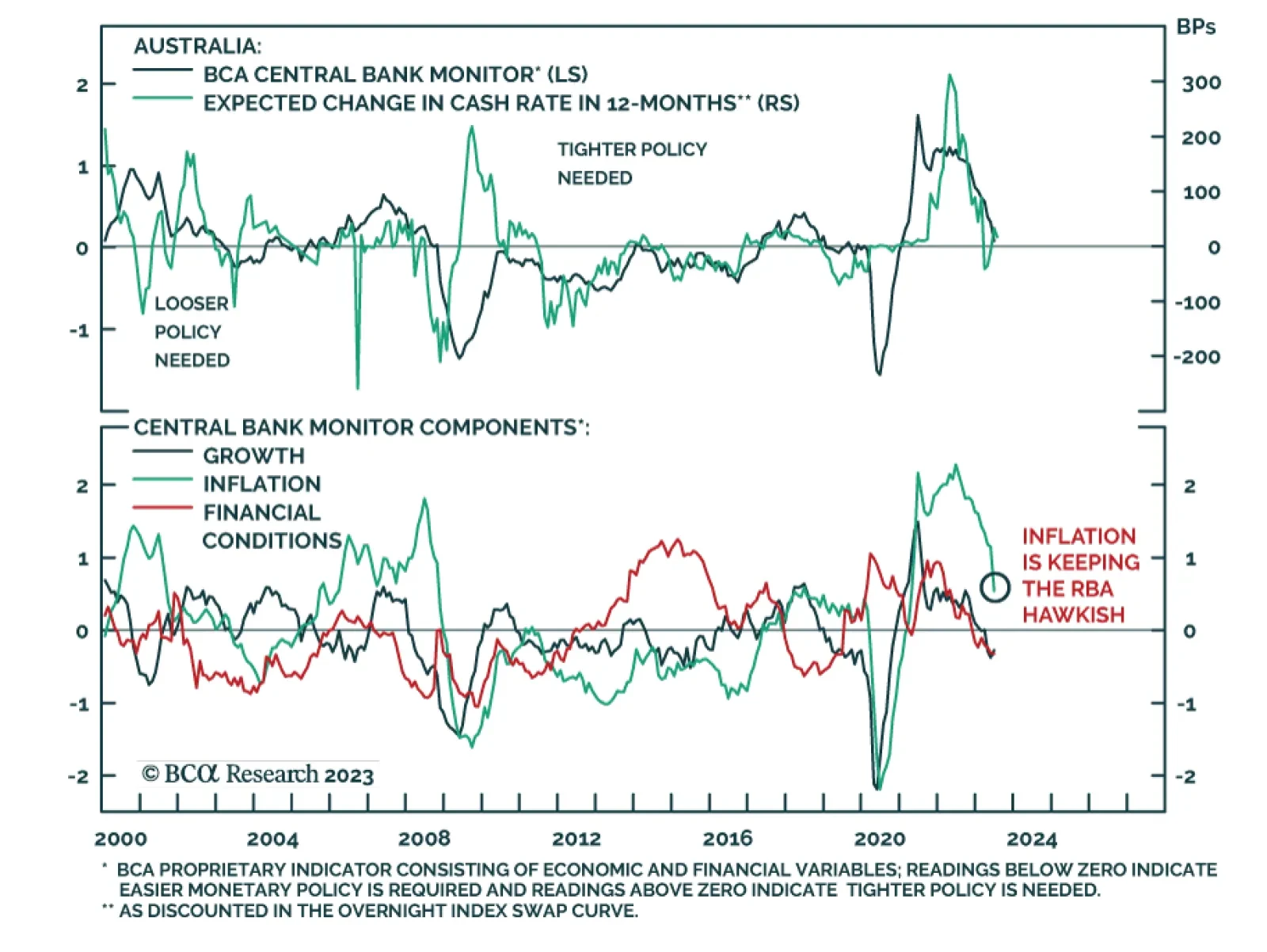

The Reserve Bank of Australia kept interest rates on hold at 4.1% on Tuesday, surprising expectations of a 25bps increase. Governor Philip Lowe’s statement underscores that the decision “will provide further time to assess the impact of” the 4 percentage…

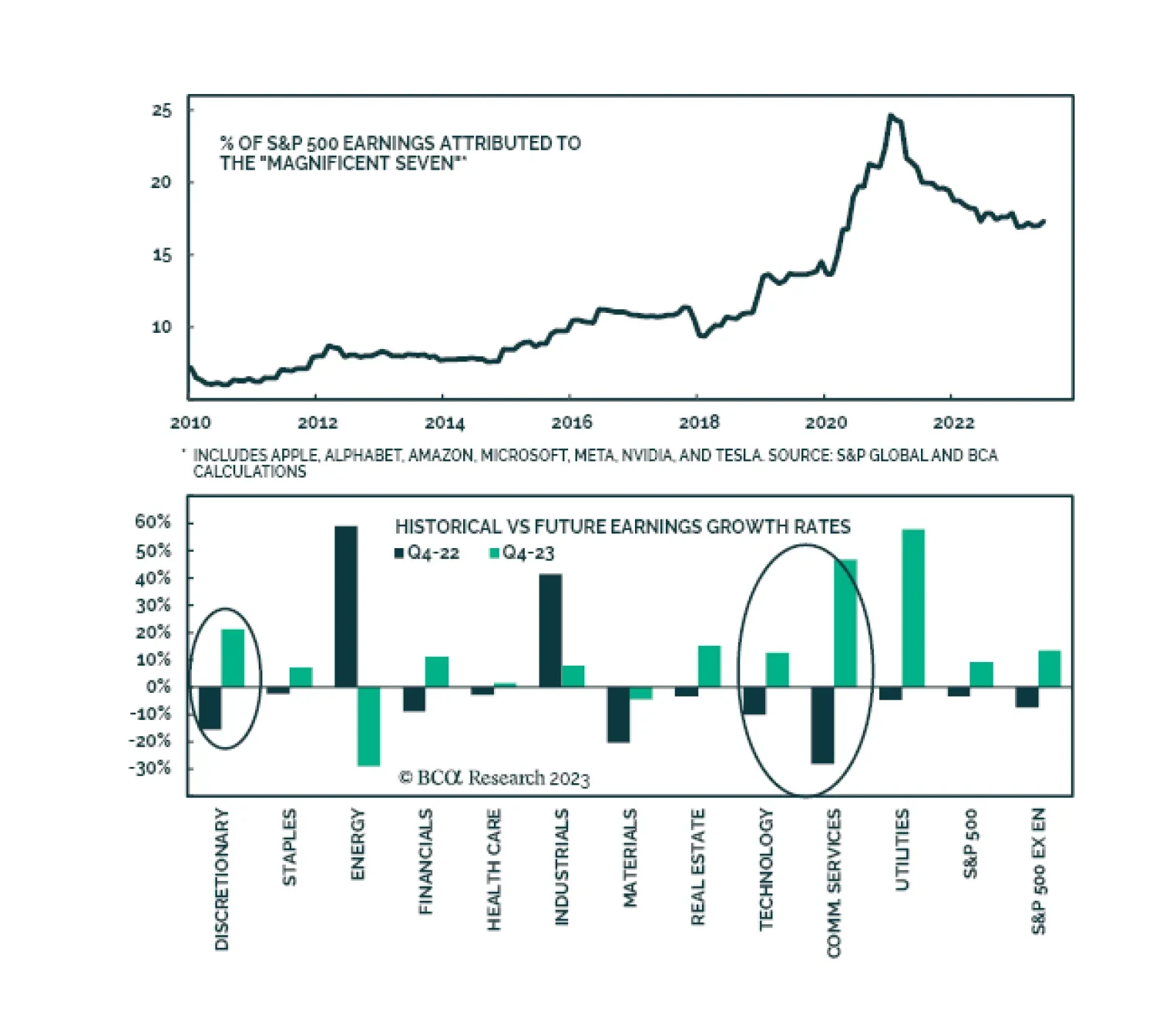

It is widely expected by consensus that earnings growth will rebound into the year-end and into 2024. Multiple factors will drive the reacceleration in earnings growth. Sales growth will pick up: In the remainder of the year, sales growth will pick up from…

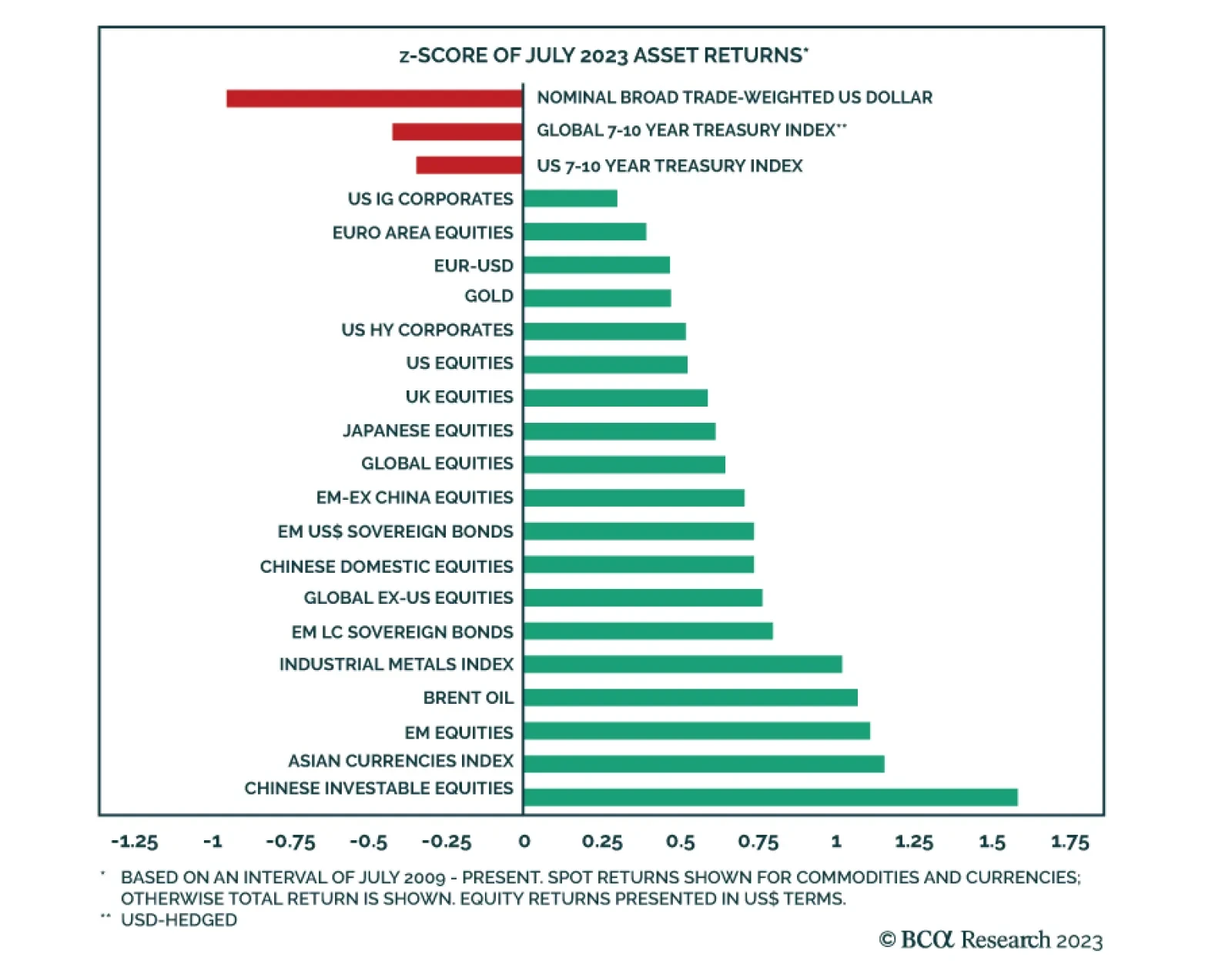

The performance of global financial markets continued to improve in July, with most of the major financial assets we track generating positive abnormal returns for the second consecutive month. Asian markets led this dynamic with Chinese investable stocks…

Some investors have thrown in the towel on investing in Chinese equities, instead deploying capital in EM ex-China – or at least contemplating doing so. This report examines the merits of investing in EM ex-China stocks and concludes that EM – whether including or excluding China - will continue underperforming DM equities.

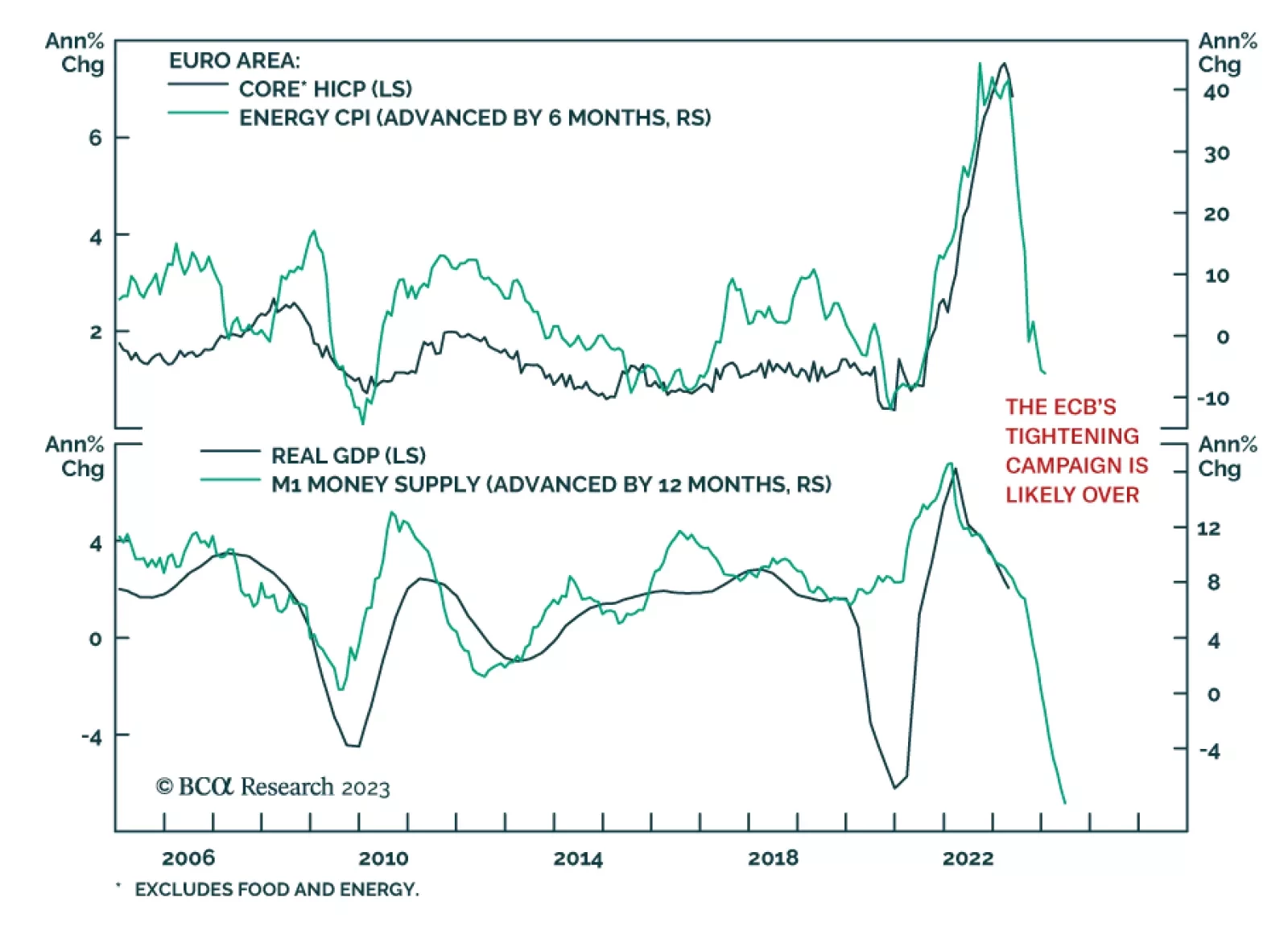

The Eurozone economy returned to expansion in the second quarter with real GDP rising by 0.3% q/q – beating expectations of 0.2% q/q. This follows an upwardly revised 0.0% in Q1 and a 0.1% contraction in Q4 2022. In particular, Ireland (+3.3%) and Lithuania,…

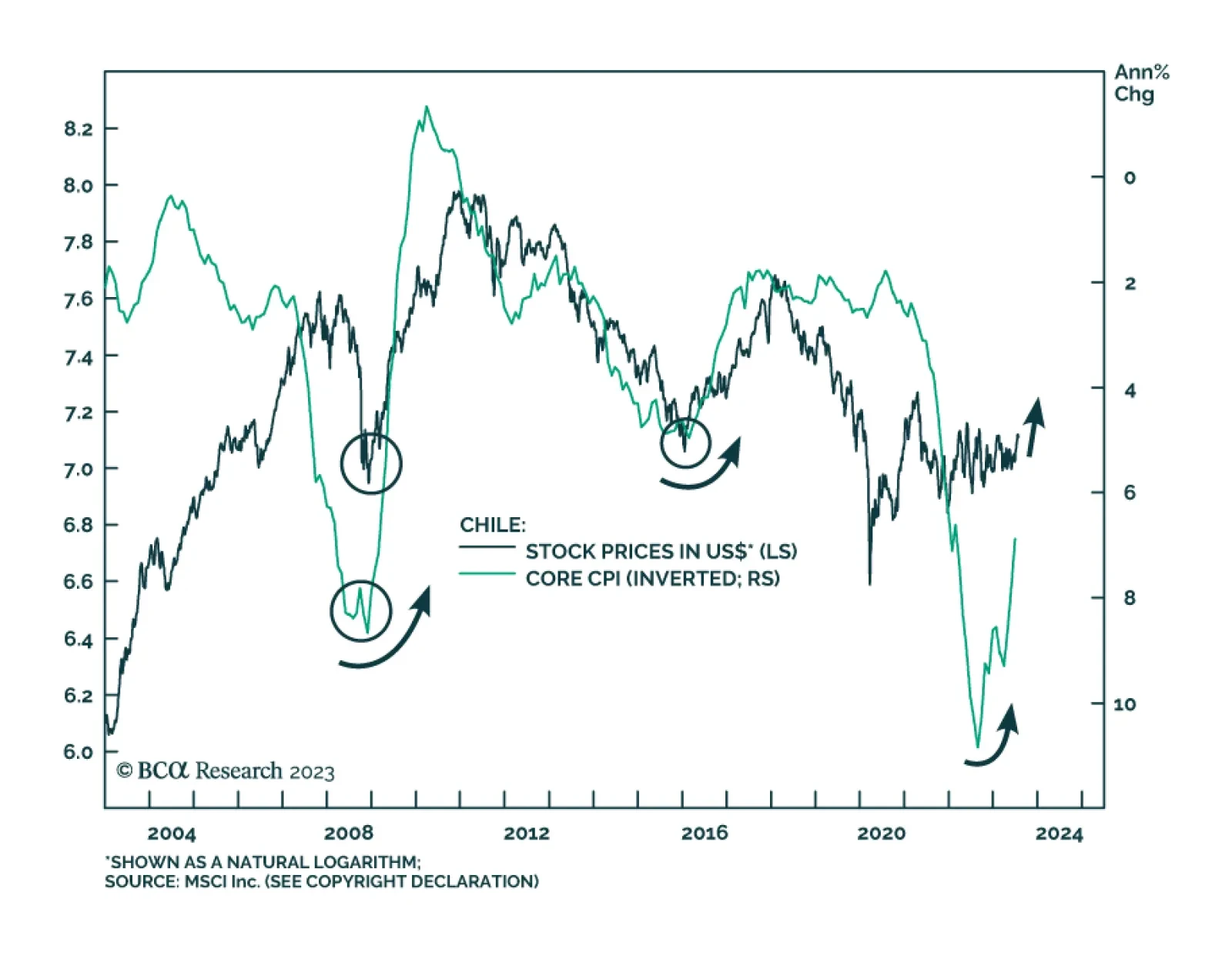

Last Friday, the Central Bank of Chile became the first major Latin American monetary authority to cut rates, thereby beginning the EM monetary easing cycle. In its latest meeting, board members decided to reduce the policy rate by a whopping 100 basis…

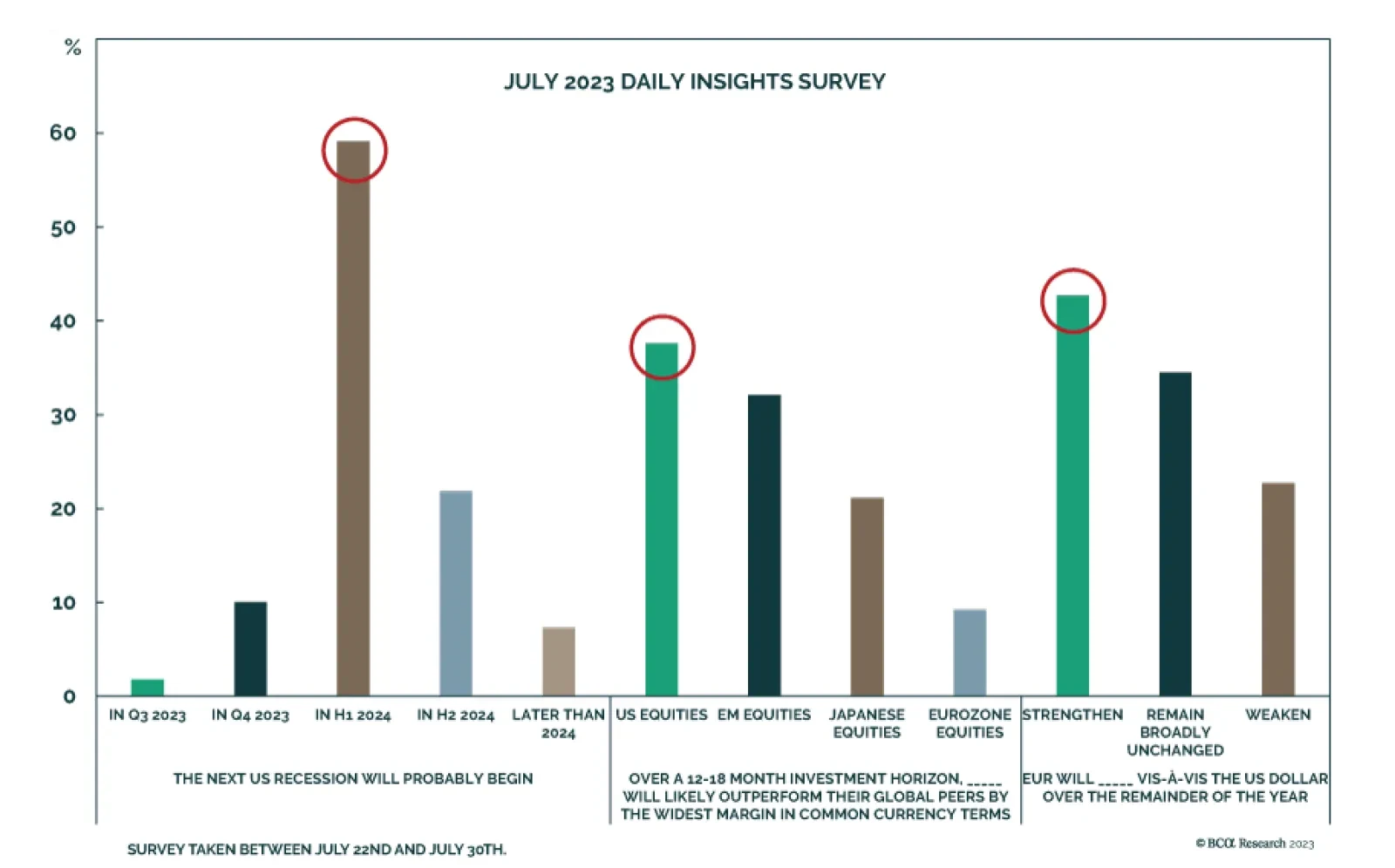

In the monthly Daily Insights Survey we conducted over the past week, we asked about our readers’ outlook for the US economy, regional equity allocation, and EUR/USD. On the outlook for the US economy, the majority of respondents (59%) expect the next…

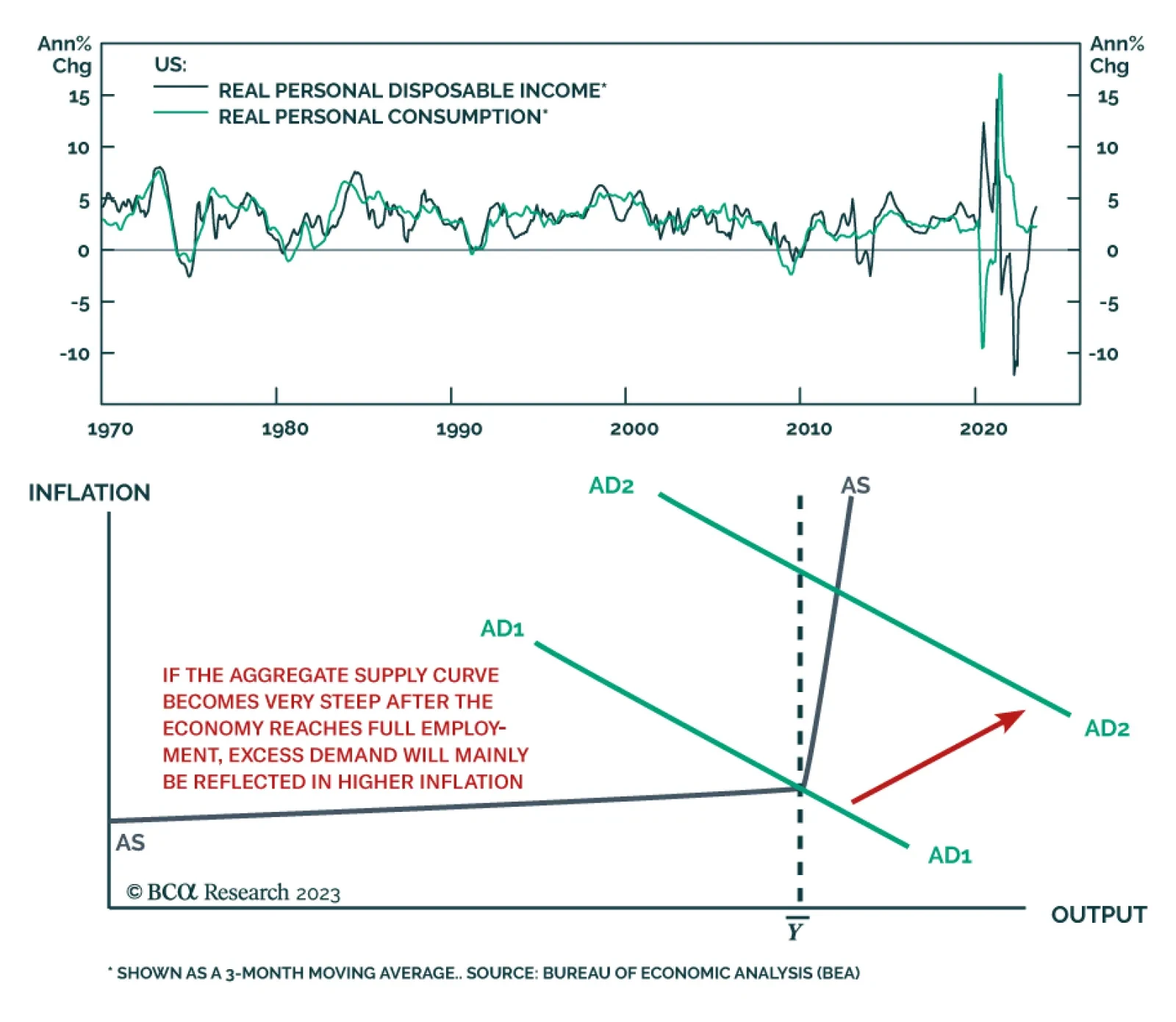

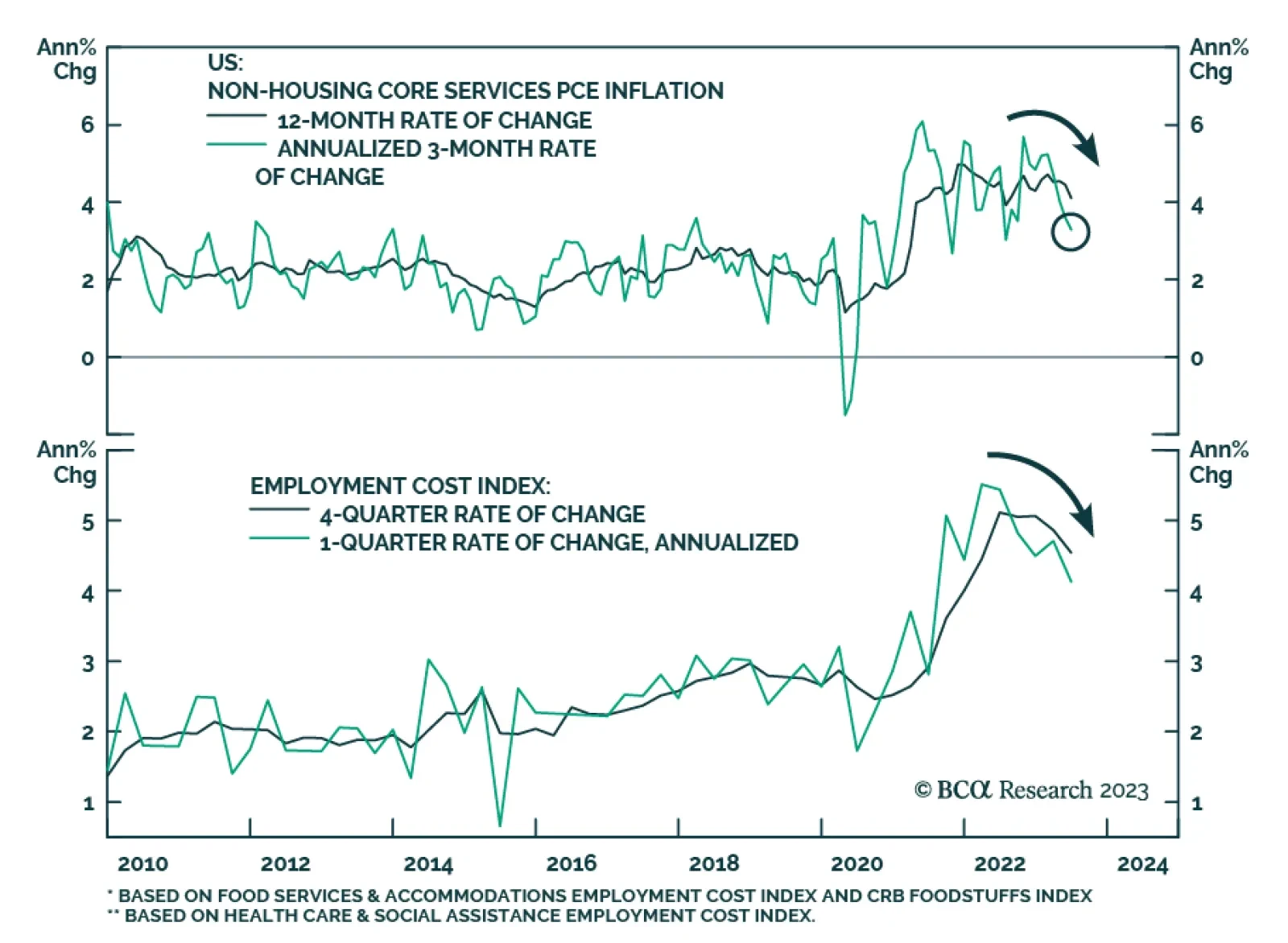

According to BCA Research’s Global Investment Strategy service, it is too early to conclude that the Fed can stop raising rates. Consumption and real income growth are highly correlated. If inflation continues to fall, real wages will rise further. If that…

US economic data released on Friday continued the string of good news about the US economy. On the inflation front, core PCE inflation – the Fed’s preferred gauge of underlying price pressures – softened to 0.165% m/m in June. On an annualized basis, this…