Business Cycles

Over the past two months, copper has rallied alongside risk assets and now stands 9% above its late-May trough. Here, the outlook for China’s economy – which accounts for over half of global refined copper usage – is key to whether the red metal will continue…

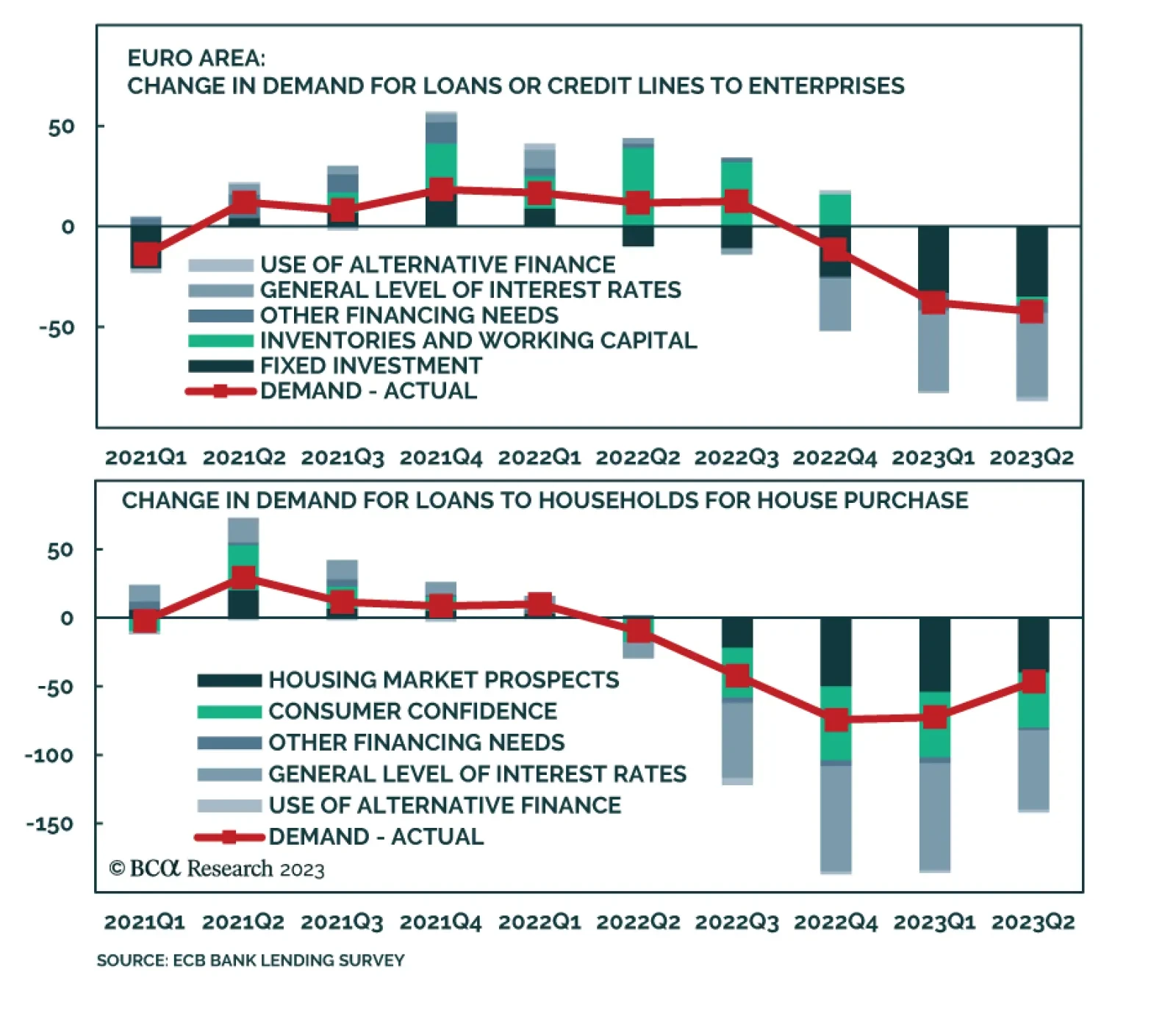

Results of the ECB’s bank lending survey (BLS) show the impact of the central bank’s aggressive tightening cycle on the region’s economy. Uncertainty about the economic outlook, borrower-specific dynamics, lower risk tolerance and higher cost of funding…

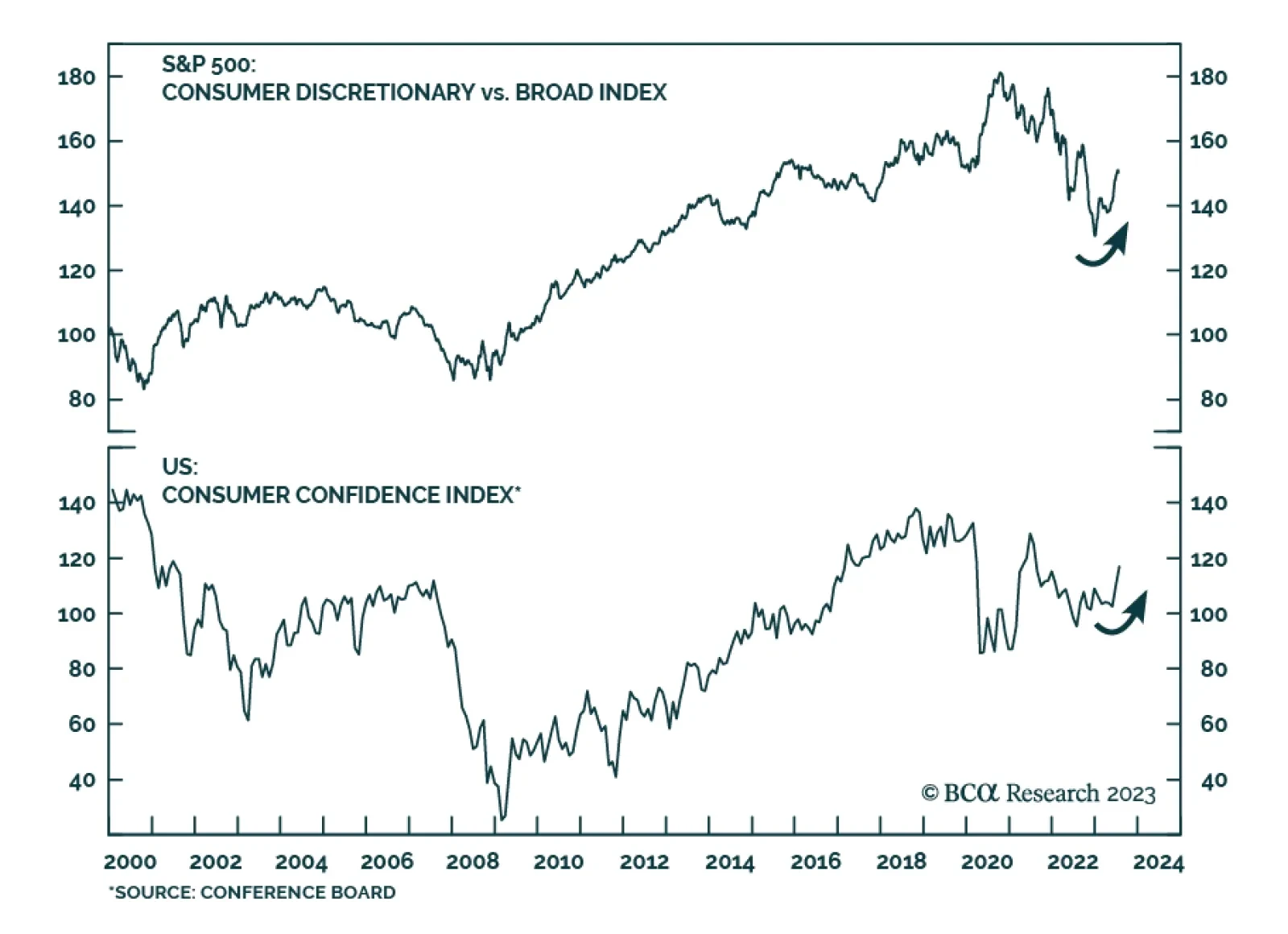

The US Consumer Discretionary sector has been one of the top winners since the equity rally broadened two months ago. Its 13% gain since the end of May outpaces the S&P 500’s rally by 3.8 percentage points This outperformance comes despite last week’s…

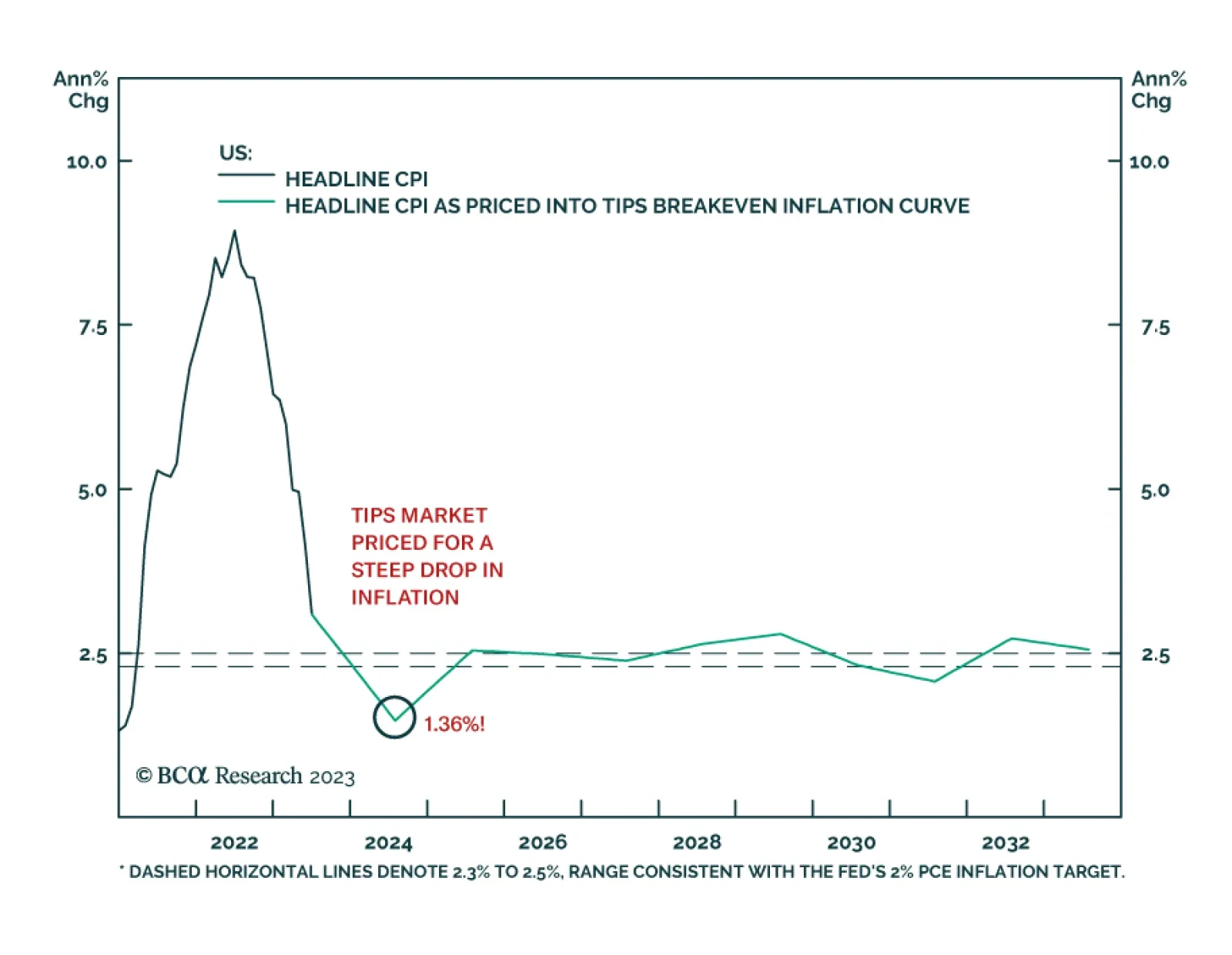

According to BCA Research’s US Bond Strategy service, inflation will fall during the next 12 months, but not by as much as markets expect. Investors should take advantage of this valuation opportunity by entering 2-year/10-year TIPS breakeven slope…

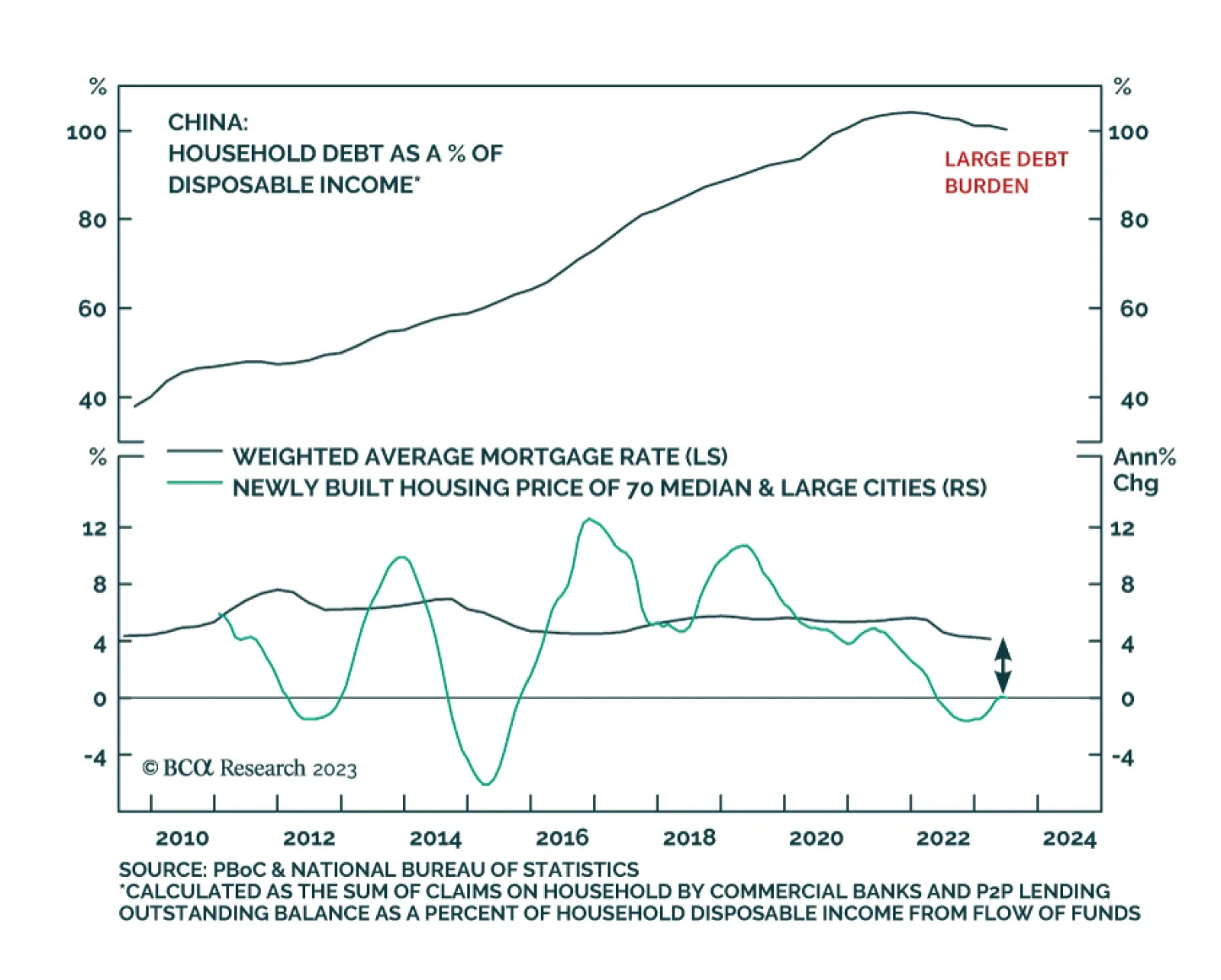

Stay cautious on Chinese stocks. Equity investors should use any rebound in onshore stock prices to downgrade A-shares from overweight to neutral within global and EM equity portfolios. Remain underweight Chinese investable/offshore stocks. Onshore bond yields will drop to all-time lows. Continue receiving 10-year swap rates. The currency will continue depreciating versus the US dollar in the coming months.

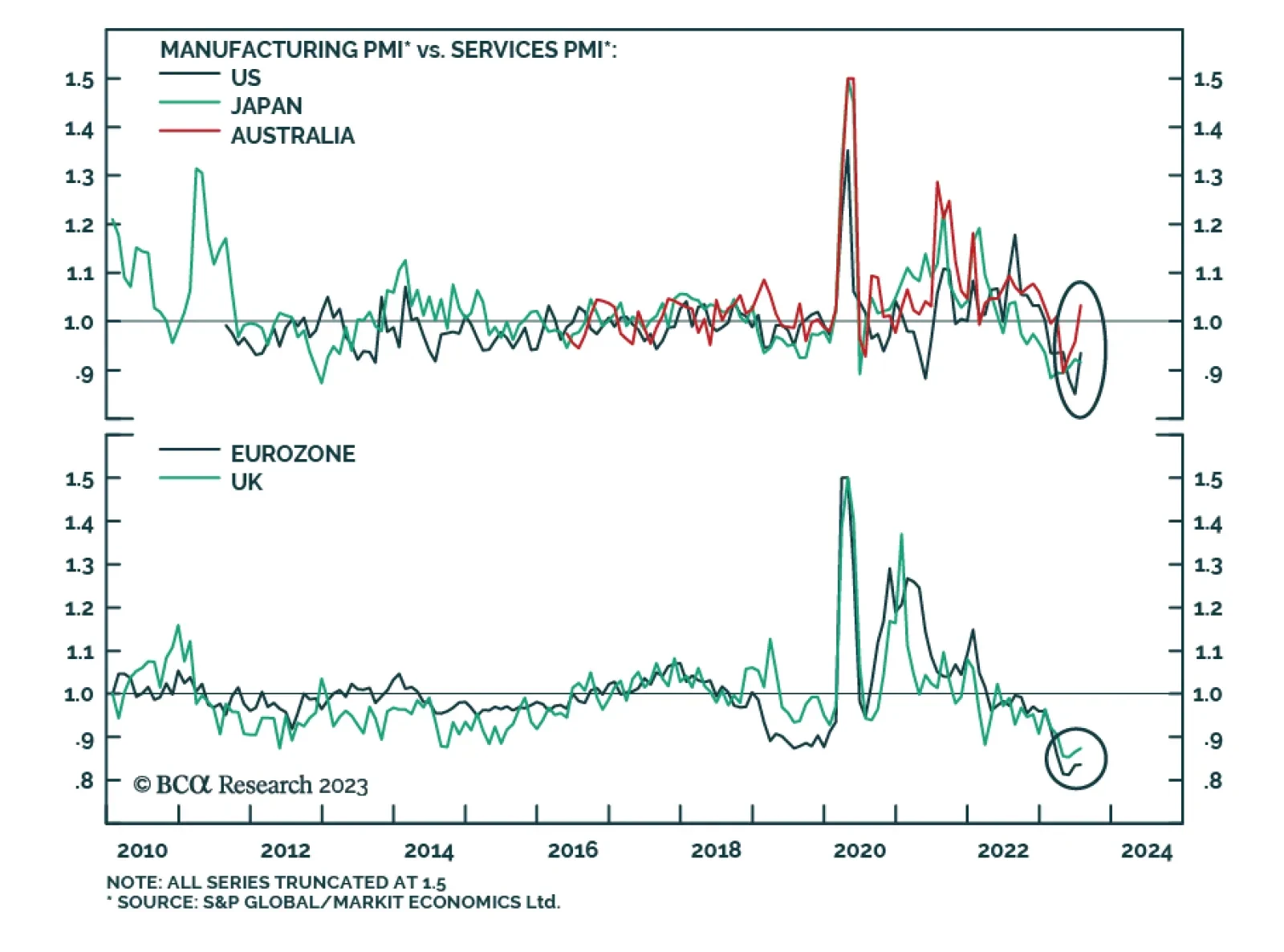

Flash PMIs sent a mixed signal about manufacturing and service sector conditions across DM economies in July. The Euro Area release was particularly weak. An unexpected 0.7-point decline in the Manufacturing PMI and a 0.9 point drop in the Services PMI…

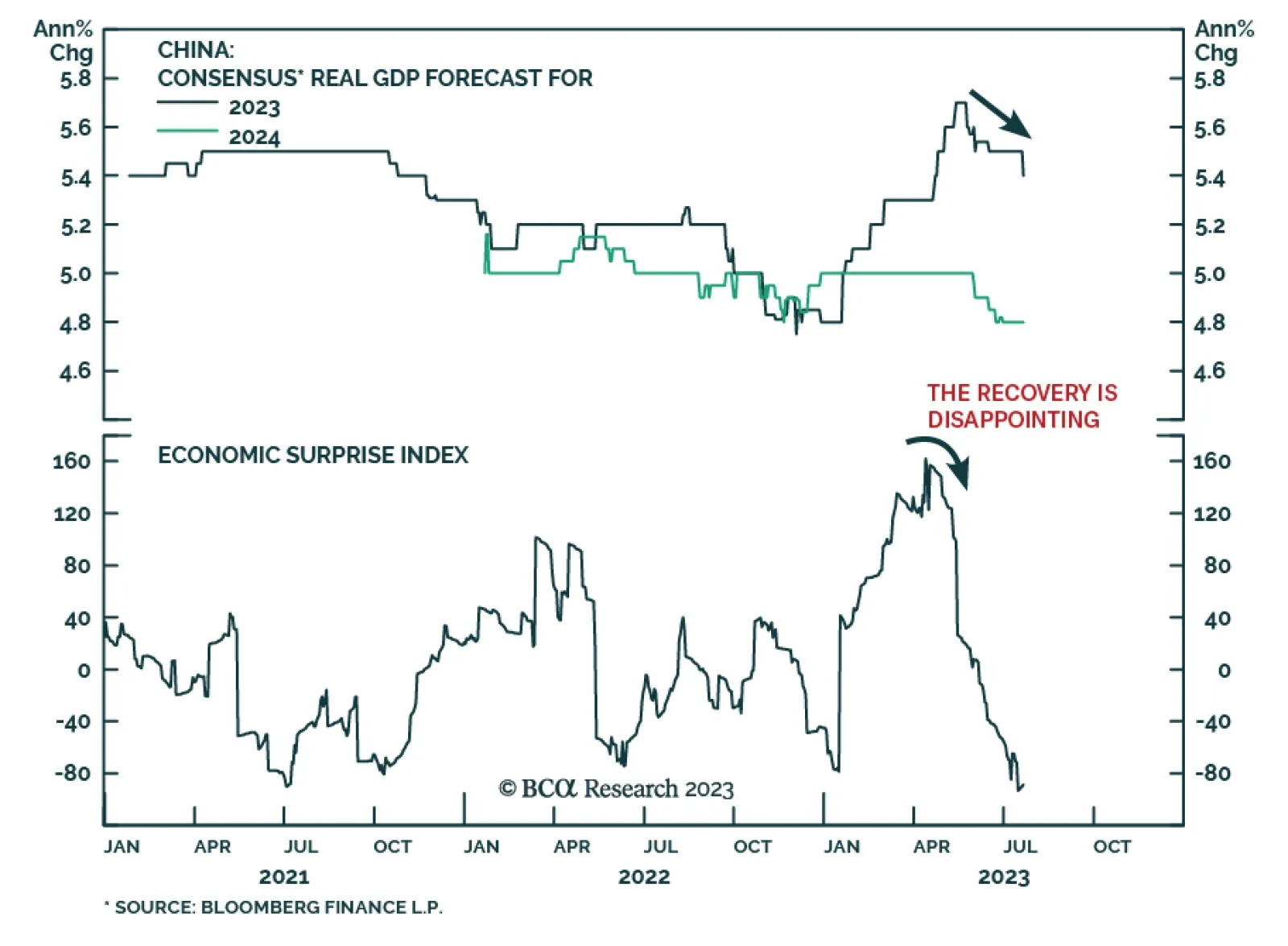

China’s Politburo meeting delivered a disappointing signal about Beijing’s willingness to deliver meaningful stimulus. Although policymakers pledged support for domestic demand, consumer sentiment, and risk prevention, they underscored that the measures will…

Equity investors resoundingly approved of the large-cap banks’ second-quarter earnings reports: in the seven sessions since C, JPM and WFC kicked off 2Q23 earnings on July 14th, the S&P 500 Banks Index rose 6.3% to the S&P 500’s 1%, with all but two…

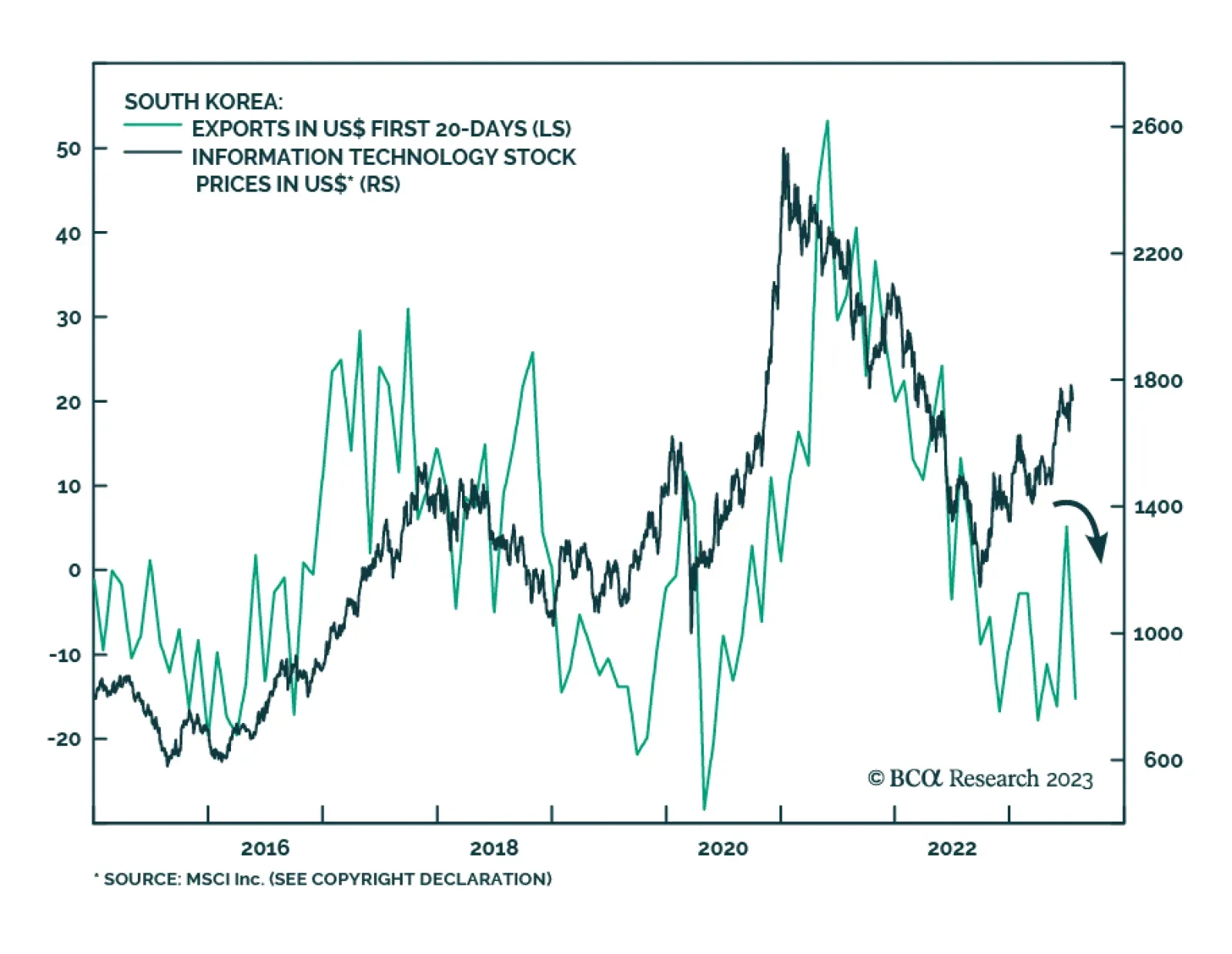

South Korean exports in the first 20 days of July corroborate the signal from Taiwanese export orders that Asian trade conditions remain weak. The former declined by -15.3% y/y, undoing the optimism following a 5.3% y/y increase in the first 20 days of June.…

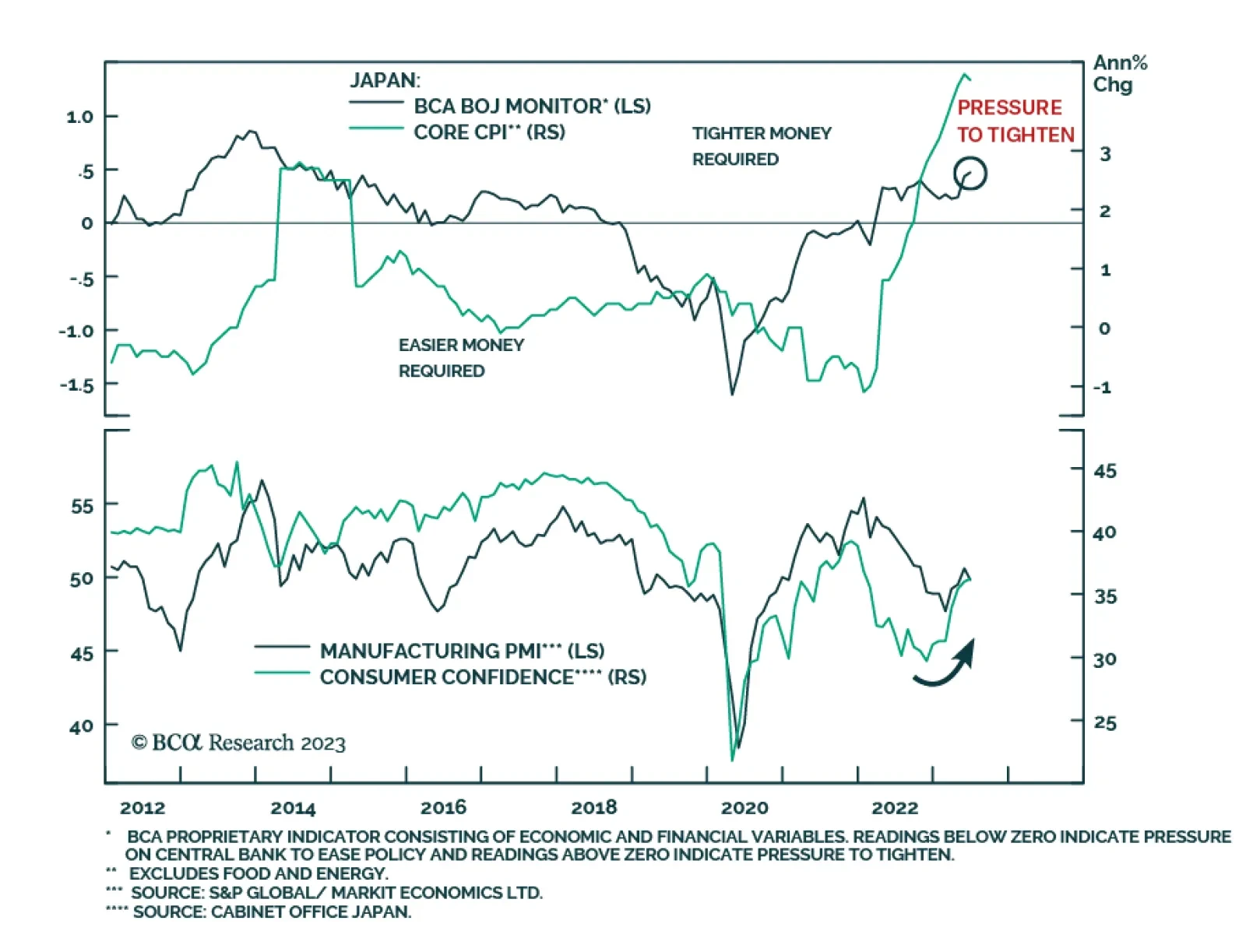

The Japanese yen slid by 2.1% vis-à-vis the US dollar last week, reversing the prior week’s rally. This latest bout of weakness comes on the back of speculation that the Bank of Japan will keep policy unchanged at its Friday meeting. On the one hand, both…