Business Cycles

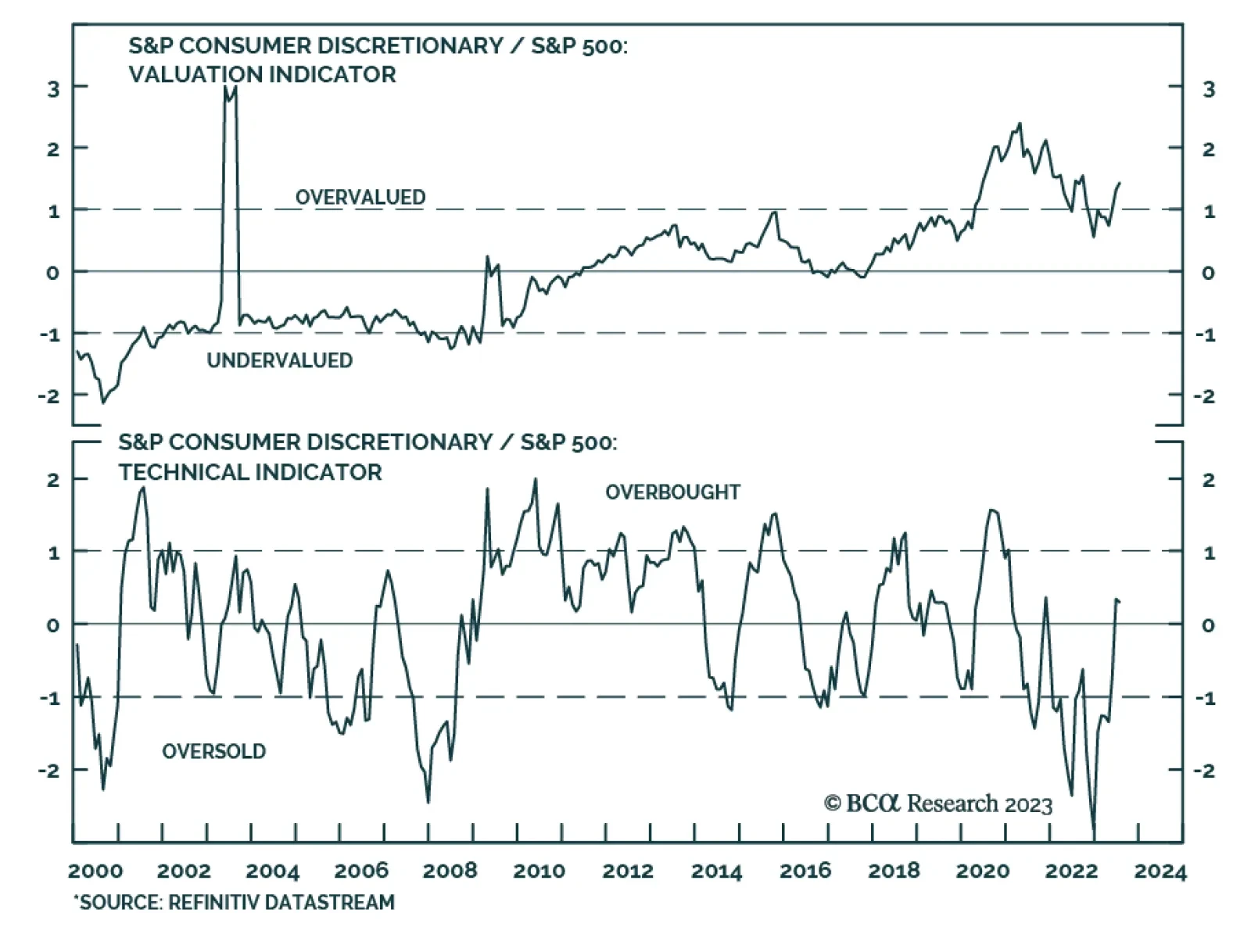

In the first five months of the year, optimism about GAI (generative AI) drove a narrow rally in US equities. The three sectors that contain companies that are most exposed to this dynamic were the only ones that experienced price gains. IT, Communication…

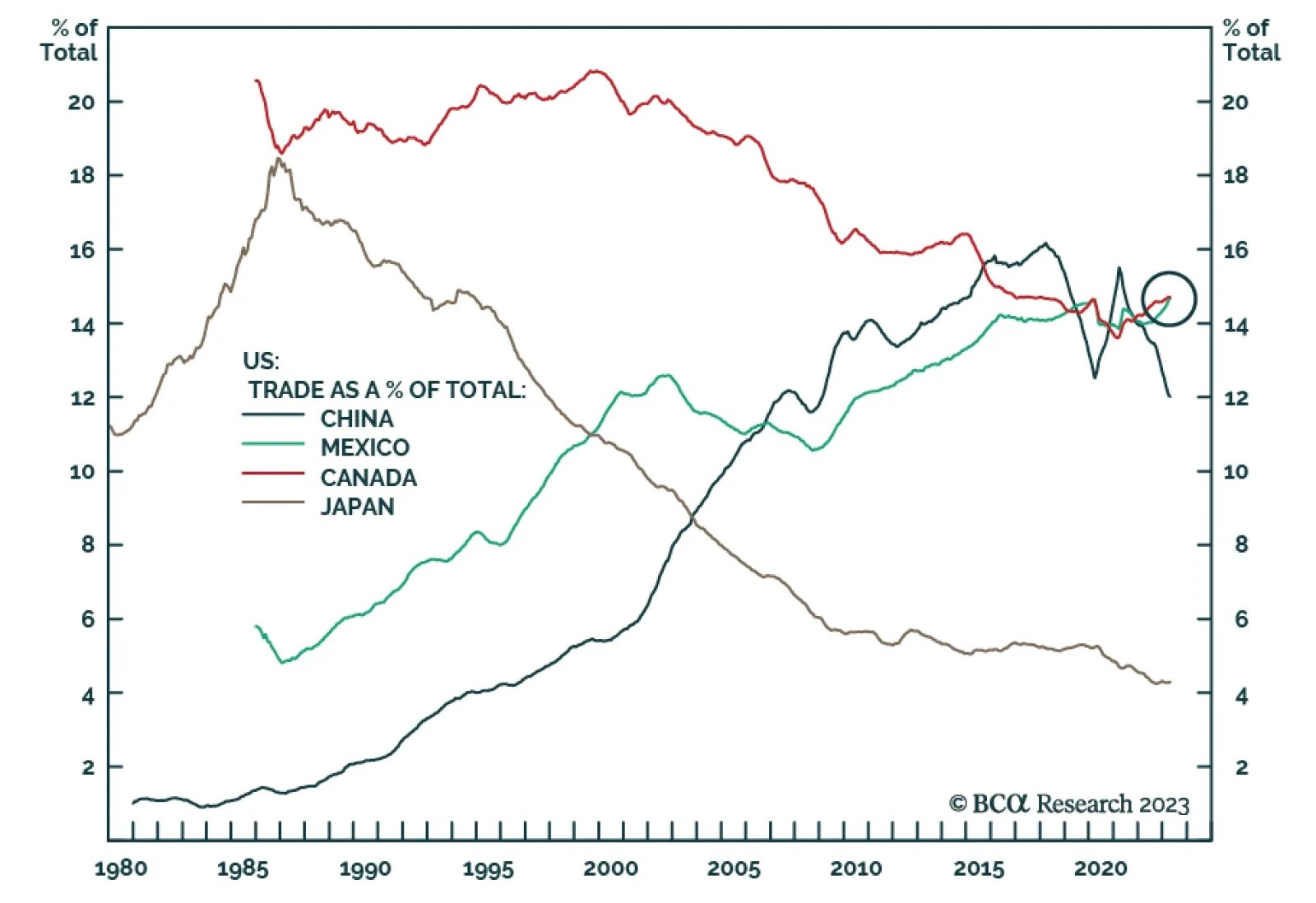

China’s slowdown confirms BCA’s Geopolitical Strategists’ view that persisting structural challenges would cause China’s economic reopening to disappoint (see The Numbers). In this context, Canada and Mexico are two notable markets that are largely…

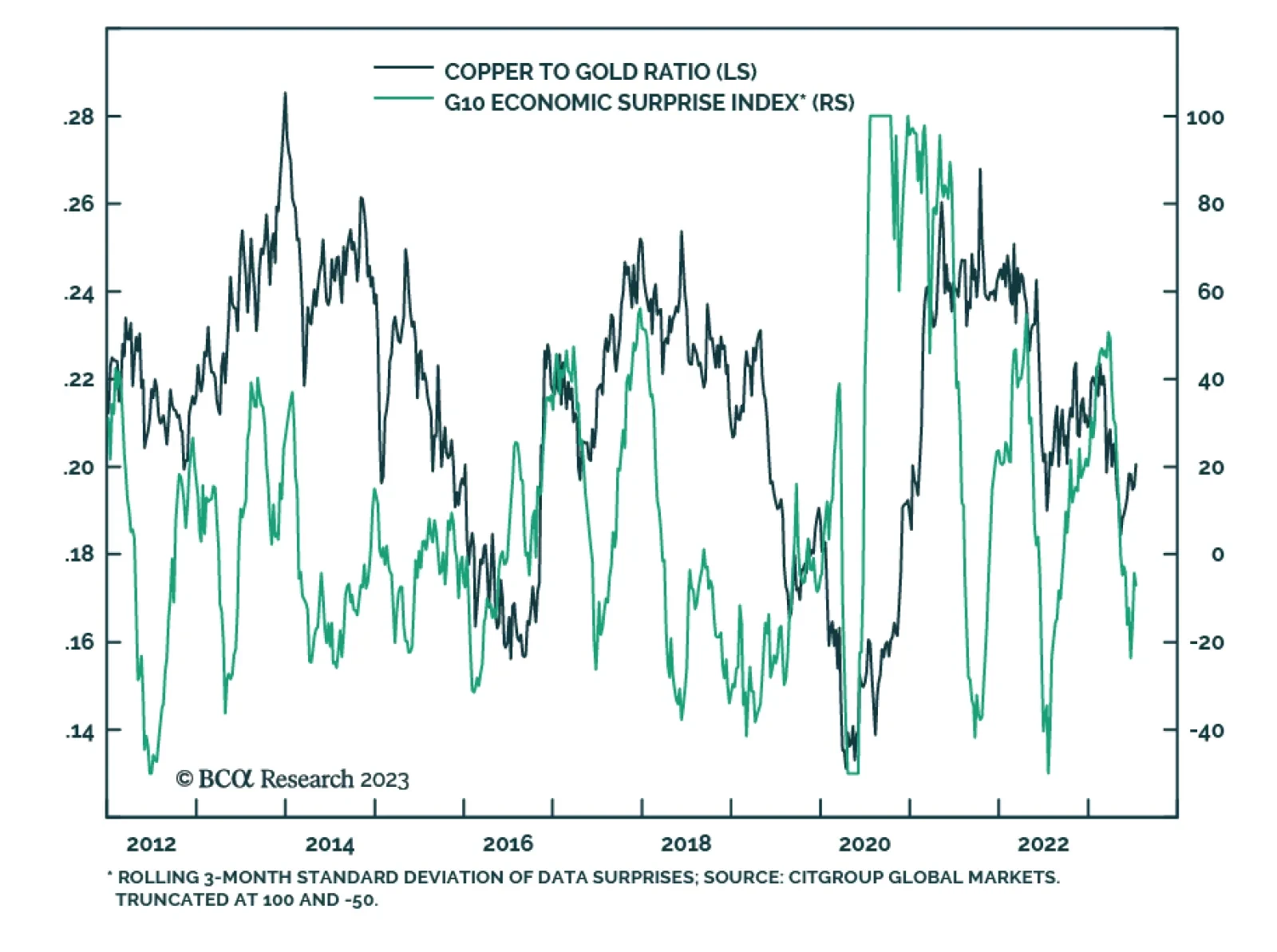

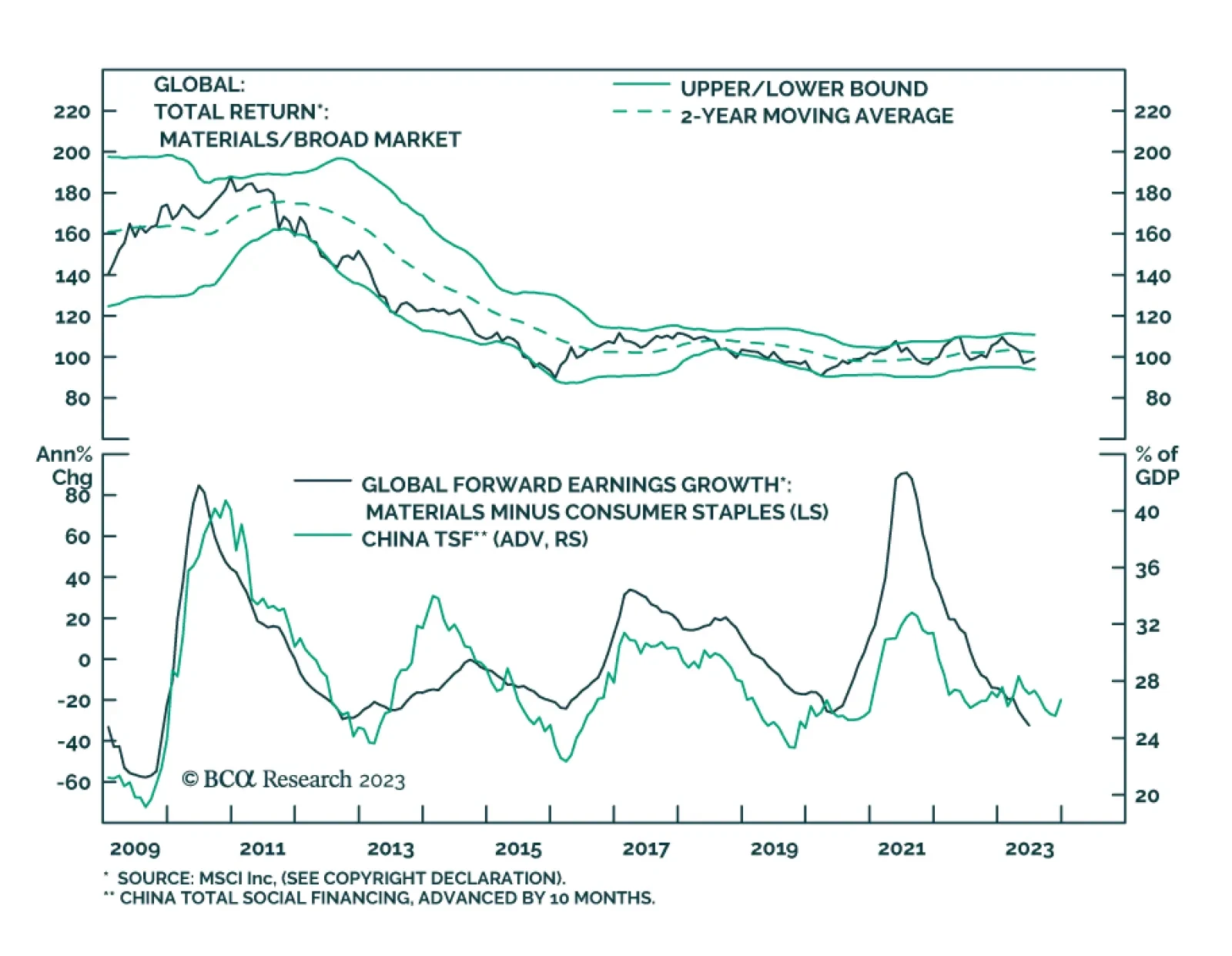

Copper rallied to a two-month high by the end of last week. Importantly, this move did not occur in isolation. It coincides with greater optimism about the prospects of a soft landing. Indeed, the US economic surprise index is solidly in positive territory…

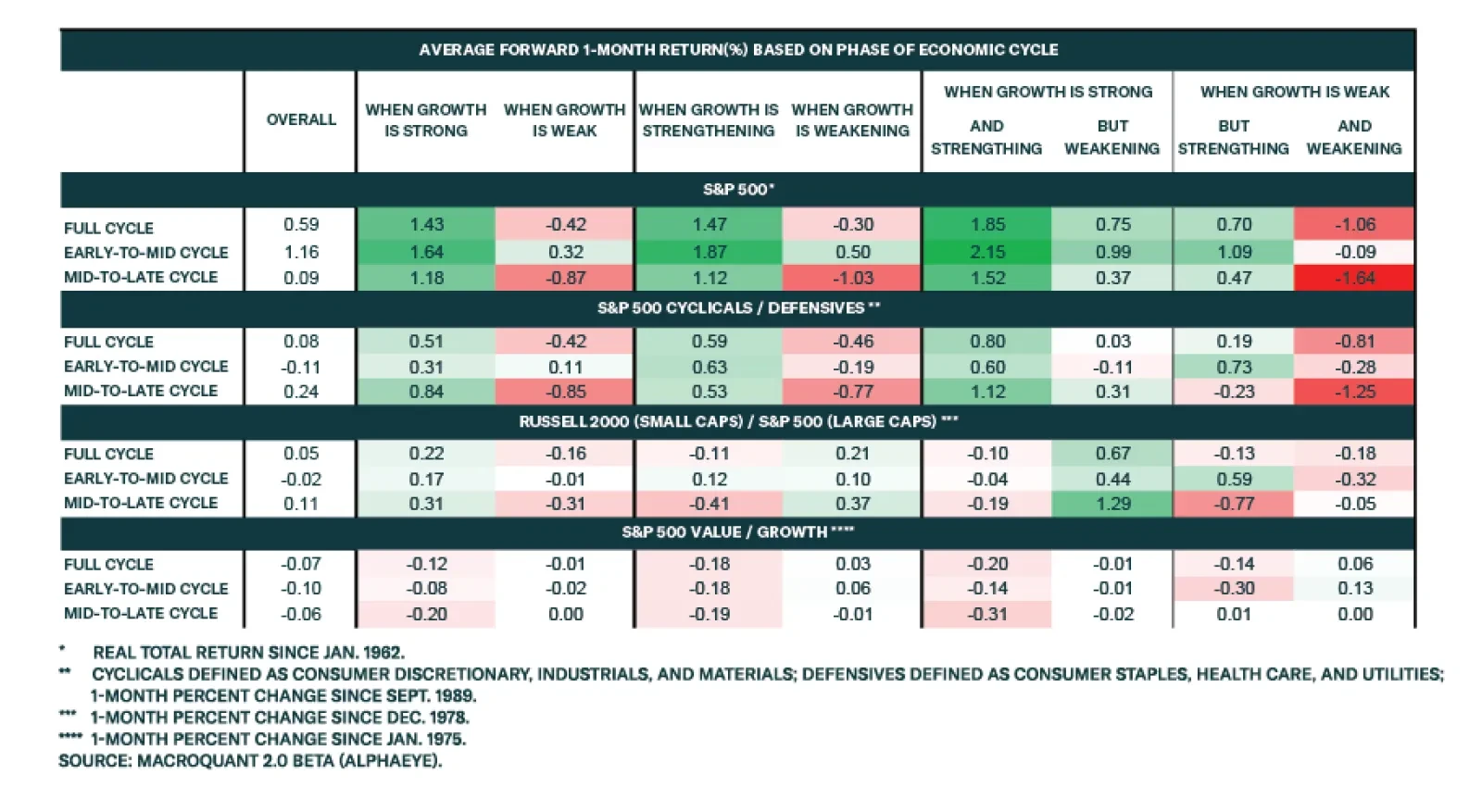

According to BCA Research’s Global Investment Strategy service, stocks fare best when there is plenty of slack in the economy and growth is strong and getting stronger. In classical physics, the trajectory of an object can be described by its position,…

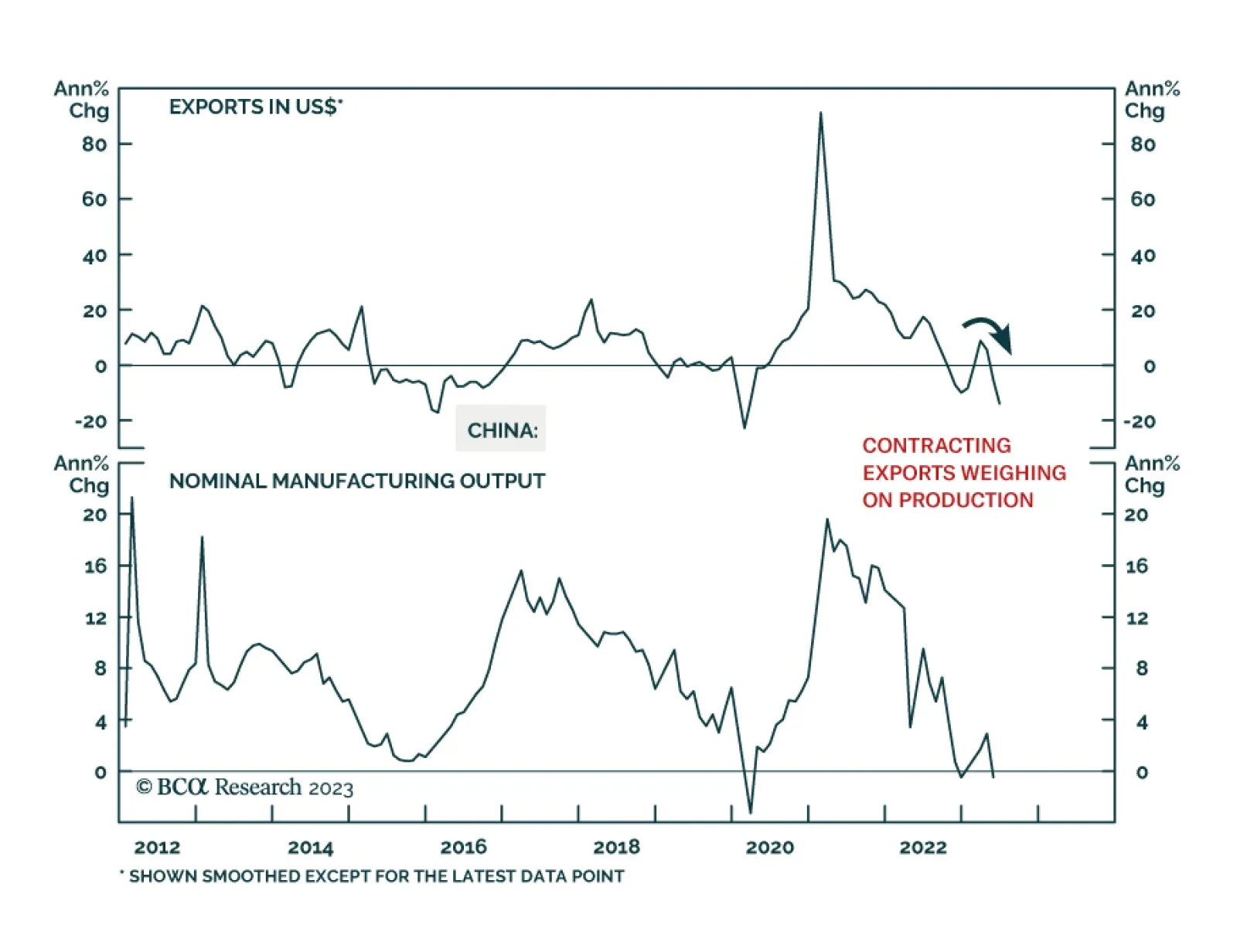

China’s June export data sent a negative signal about global manufacturing conditions. The -12.4% y/y drop in the dollar value of Chinese exports fell below expectations of a -10% y/y decline, registering the steepest annual contraction since February 2020.…

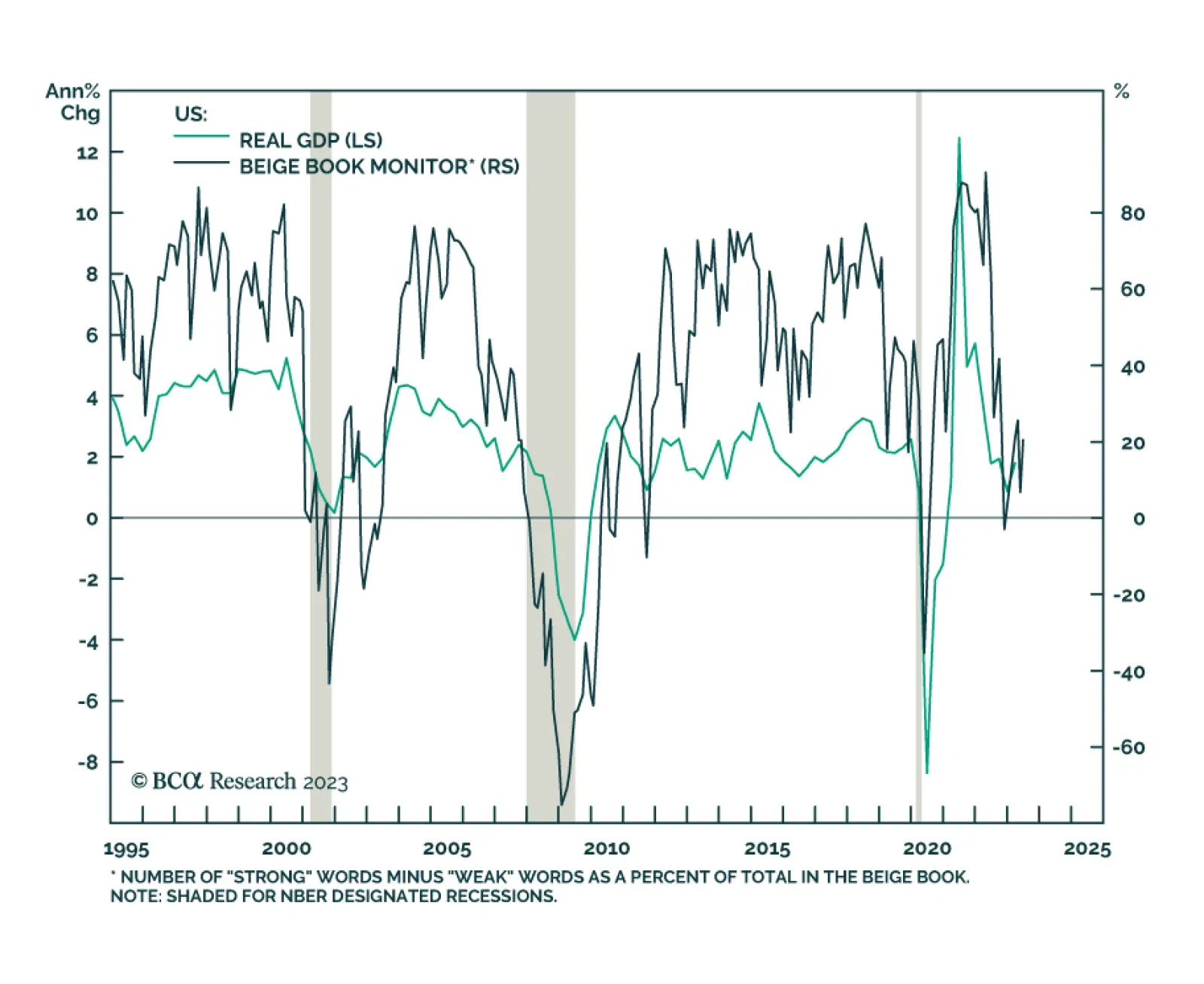

The Fed’s latest Beige Book reveals that economic activity rose slightly in recent weeks. The results are based on surveys and interviews conducted across 12 districts through June 30. In particular, two of the districts experienced “slight and modest…

BCA’s Global Asset Allocation service (GAA) recommends a defensive multi-asset portfolio allocation due to a high probability of recession. However, our colleagues also add a hedge to manage upside risk because they do not expect recession to start until…

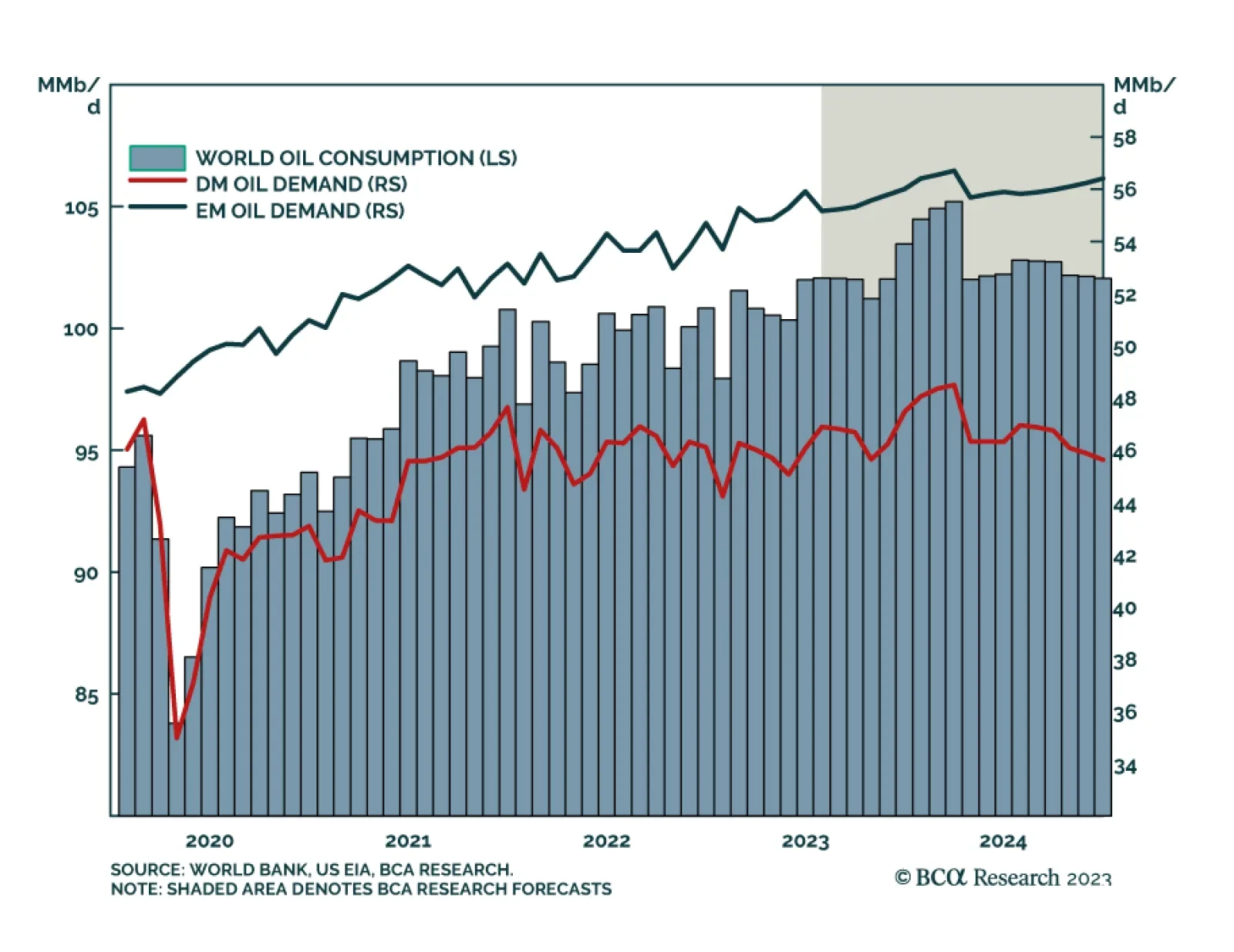

BCA Research’s Commodity & Energy Strategy service concludes that strong EM demand coupled with OPEC+’s production cuts will help boost oil prices in the coming months. EM oil demand growth continues to power global consumption higher. The latest…

In this report, we explore Brazil’s inflation and monetary policy outlook, the Lula administration’s back-and-forth between pragmatism and populism, and how these factors will affect Brazilian financial markets going forward. All in all, we believe Brazilian risk assets will be in a trading range relative to their EM peers in the next 12 months.

Falling inflation enables central banks to pause rate hikes, which is good news. But time goes on. Restrictive monetary policy, Chinese debt-deflation, energy supply shocks, US and global policy uncertainty, and extreme geopolitical risks will undermine hopes of a soft landing and beautiful disinflation.