Business Cycles

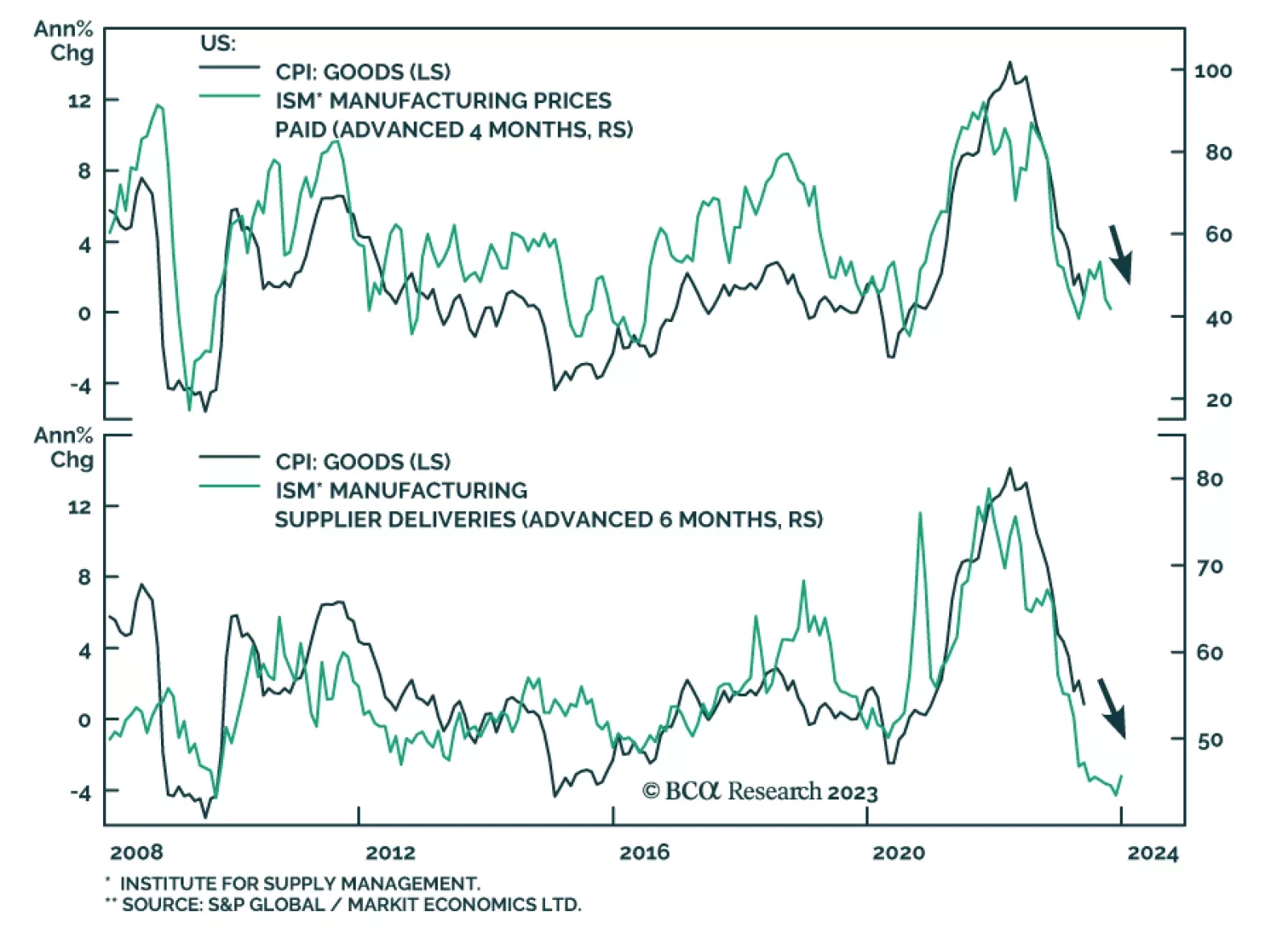

The ISM PMI sent a pessimistic signal about US manufacturing conditions in June. The headline index dropped 0.9 points to a 3-year low of 46.0 – it eighth consecutive month below the 50 boom-bust line. This is consistent with the S&P Global PMI which fell…

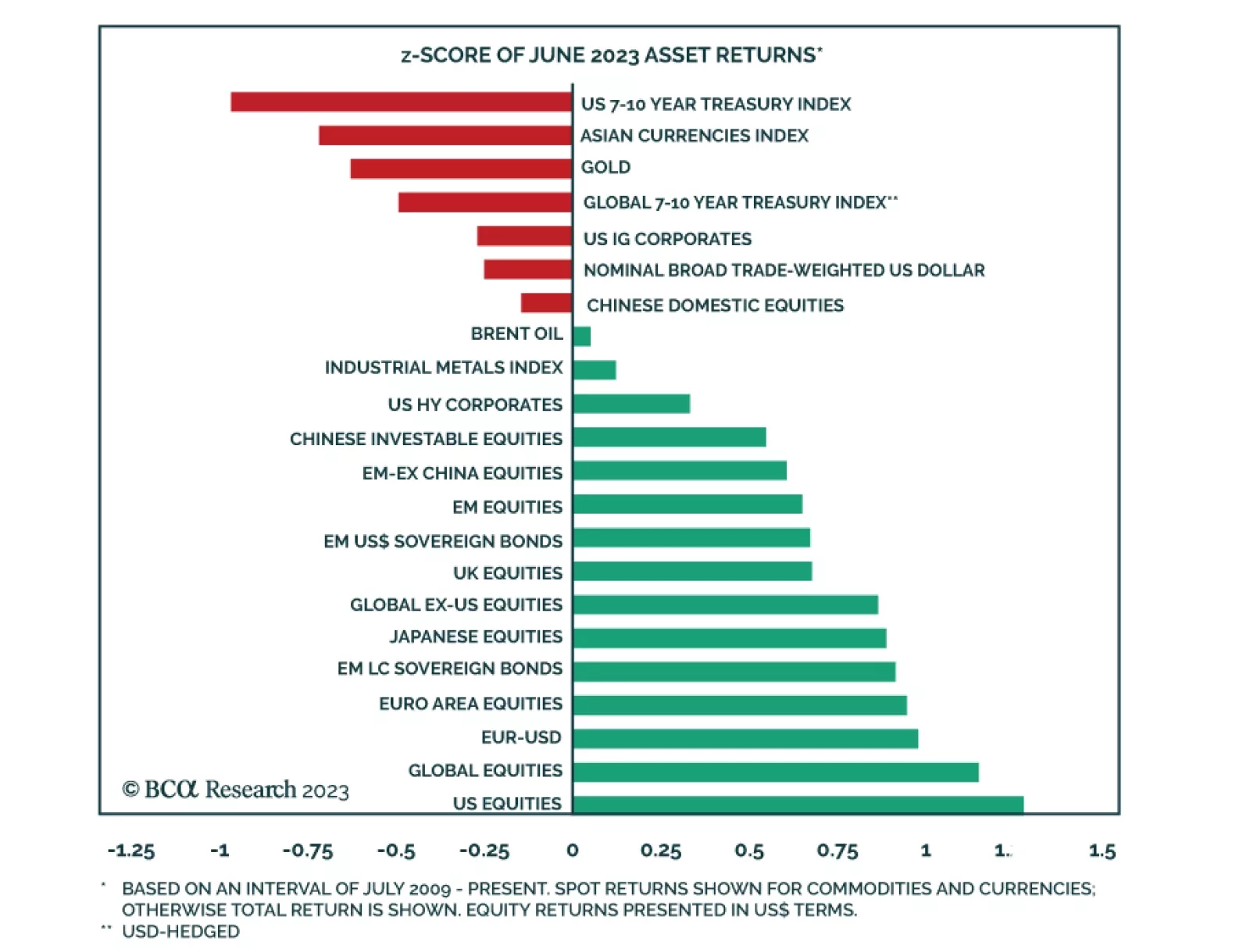

The performance of financial markets continued to improve in June, with most of the major financial assets we track generating positive abnormal returns. The US equity rally – which had been narrowly concentrated among tech stocks for most of the year –…

On a 12-month investment horizon, BCA Research’s Global Asset Allocation service recommends a defensive stance: Overweight government bonds, and underweight equities and credit. The US stock market trades on 19x forward earnings (and that is based on…

This report reviews our key calls for major currencies, in light of recent data releases.

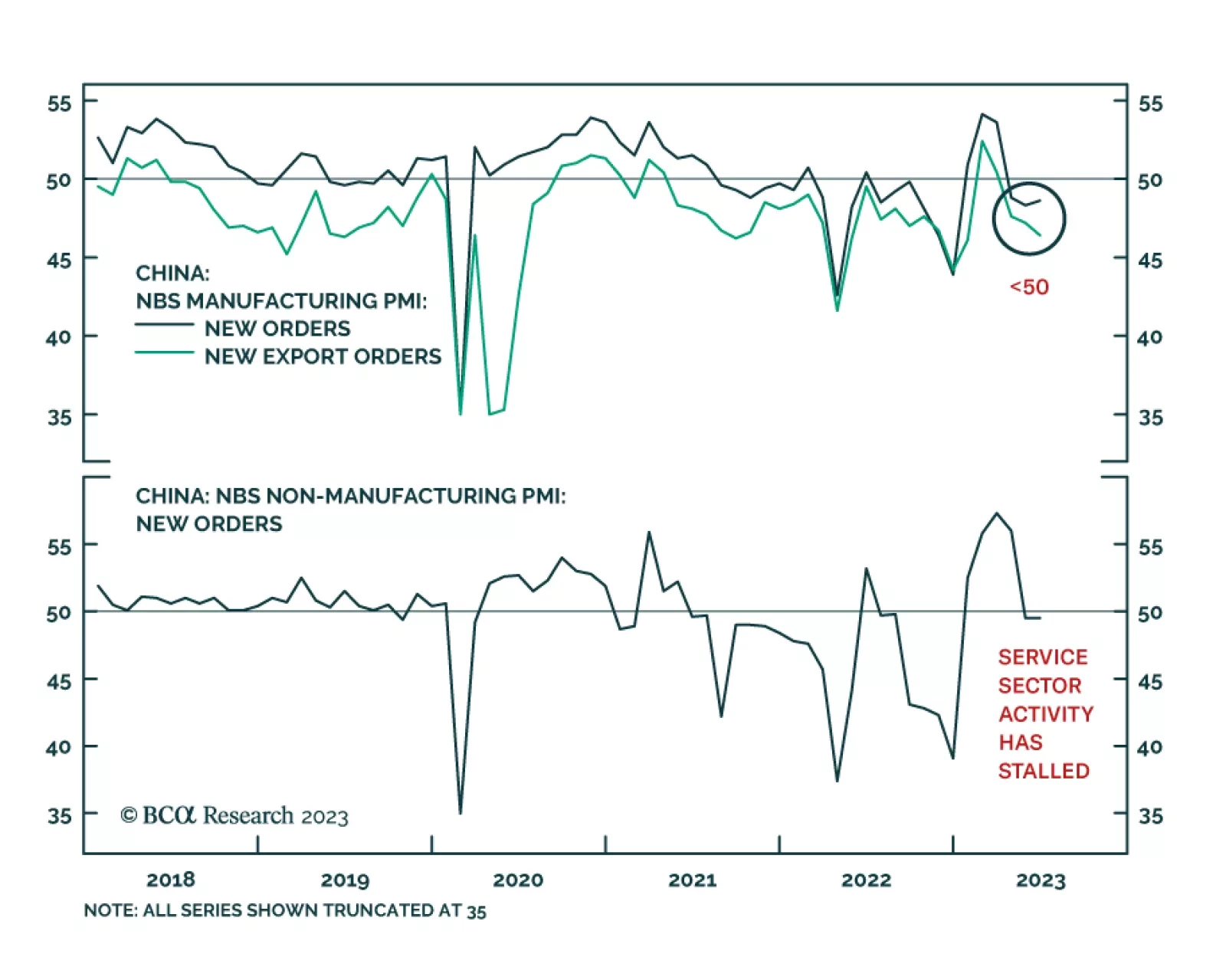

The June NBS PMI data revealed that growth conditions have deteriorated on the margin. The new orders and exports for overall manufacturing as well as for services have not improved and remain below 50. In addition, the import component of the…

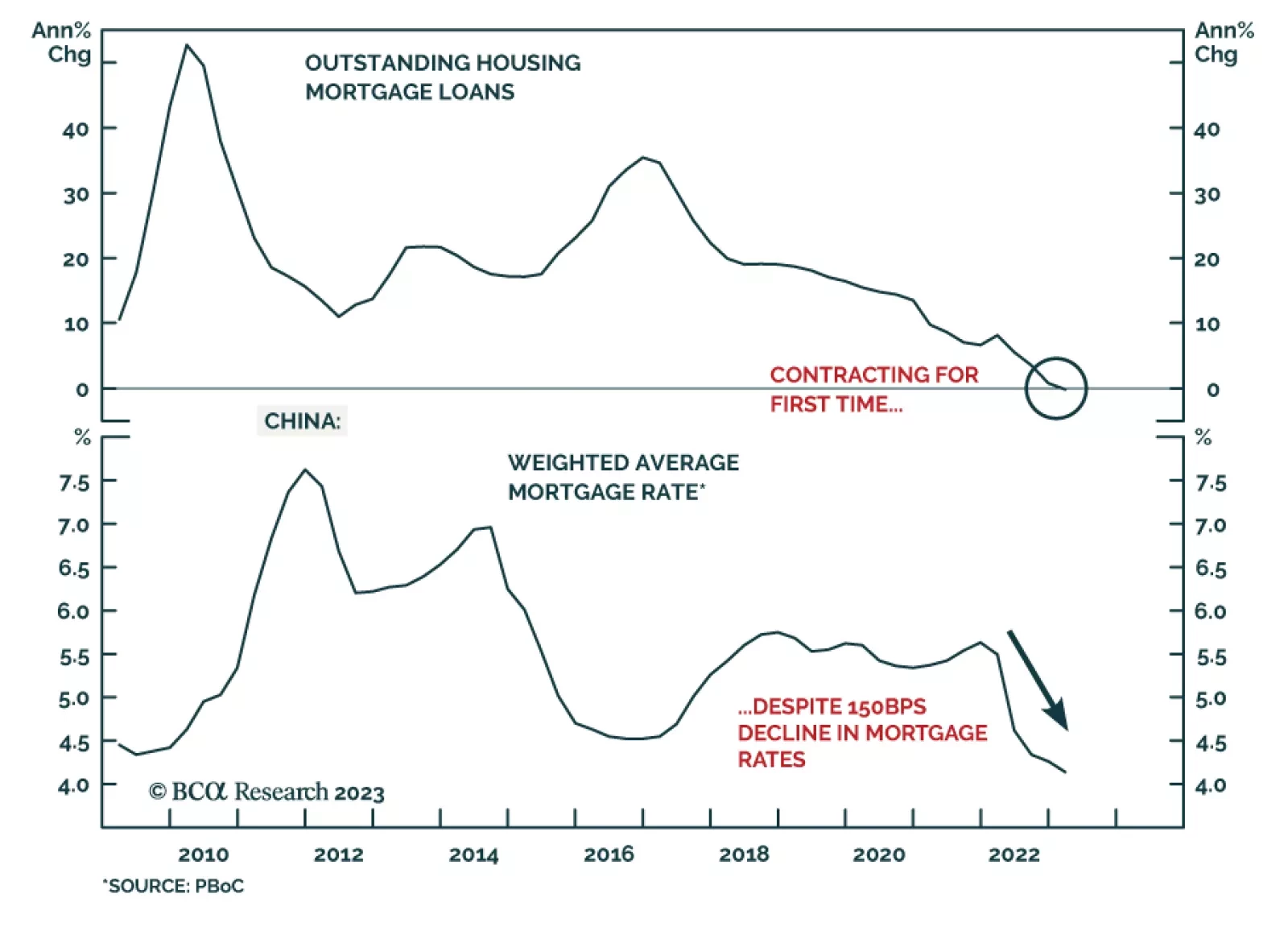

In a recently published report, our China Investment Strategy team revisited the issue of a liquidity trap in China. A liquidity trap is a condition that occurs when lower borrowing costs are unable to boost credit demand and economic growth, i.e., when low…

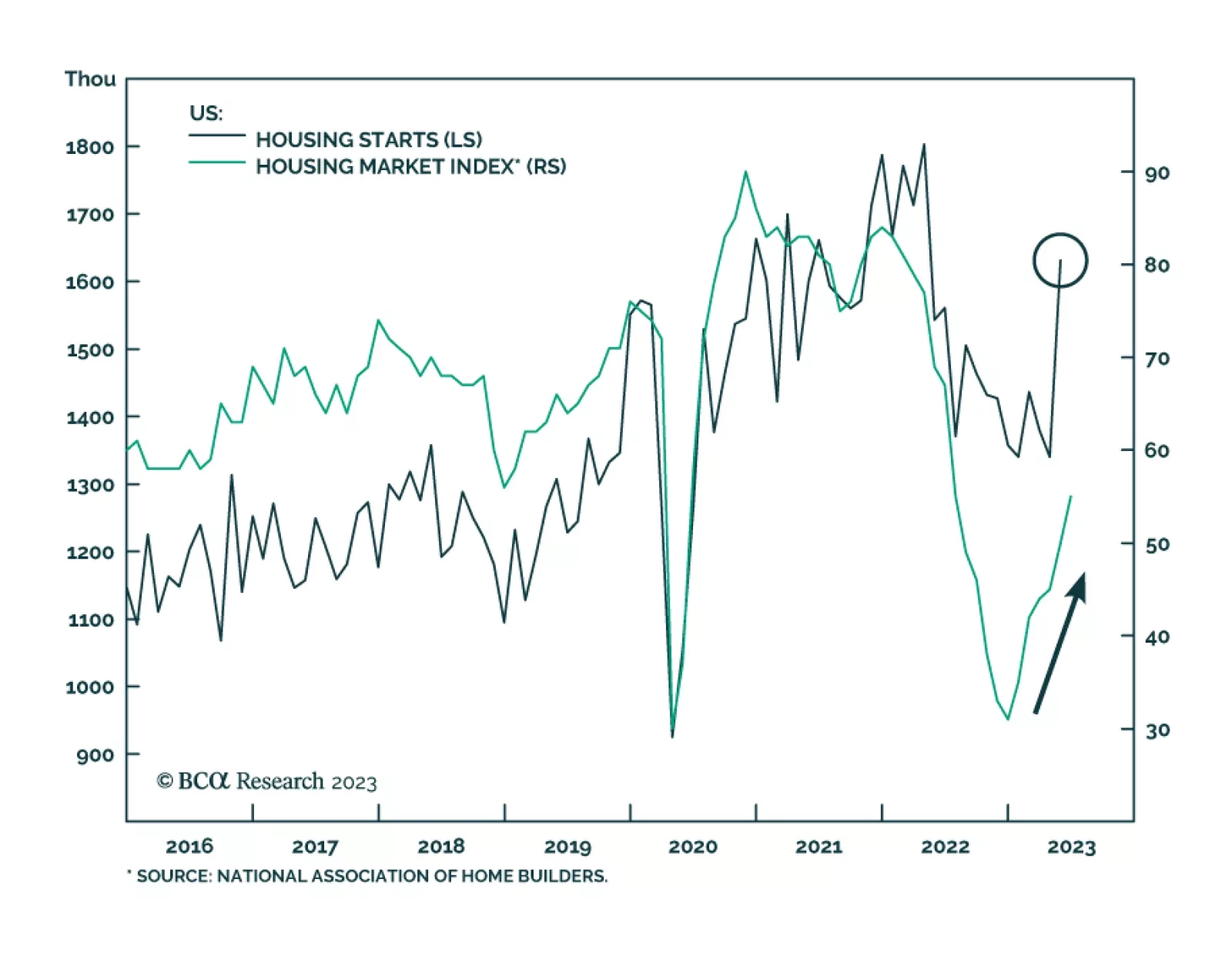

In their just-published update of US housing market conditions, our colleagues at the BCA Bank Credit Analyst focus on whether May’s strong showing in new home starts and sales in May – up 21% and 12%, respectively – is a head fake or the beginning of a…

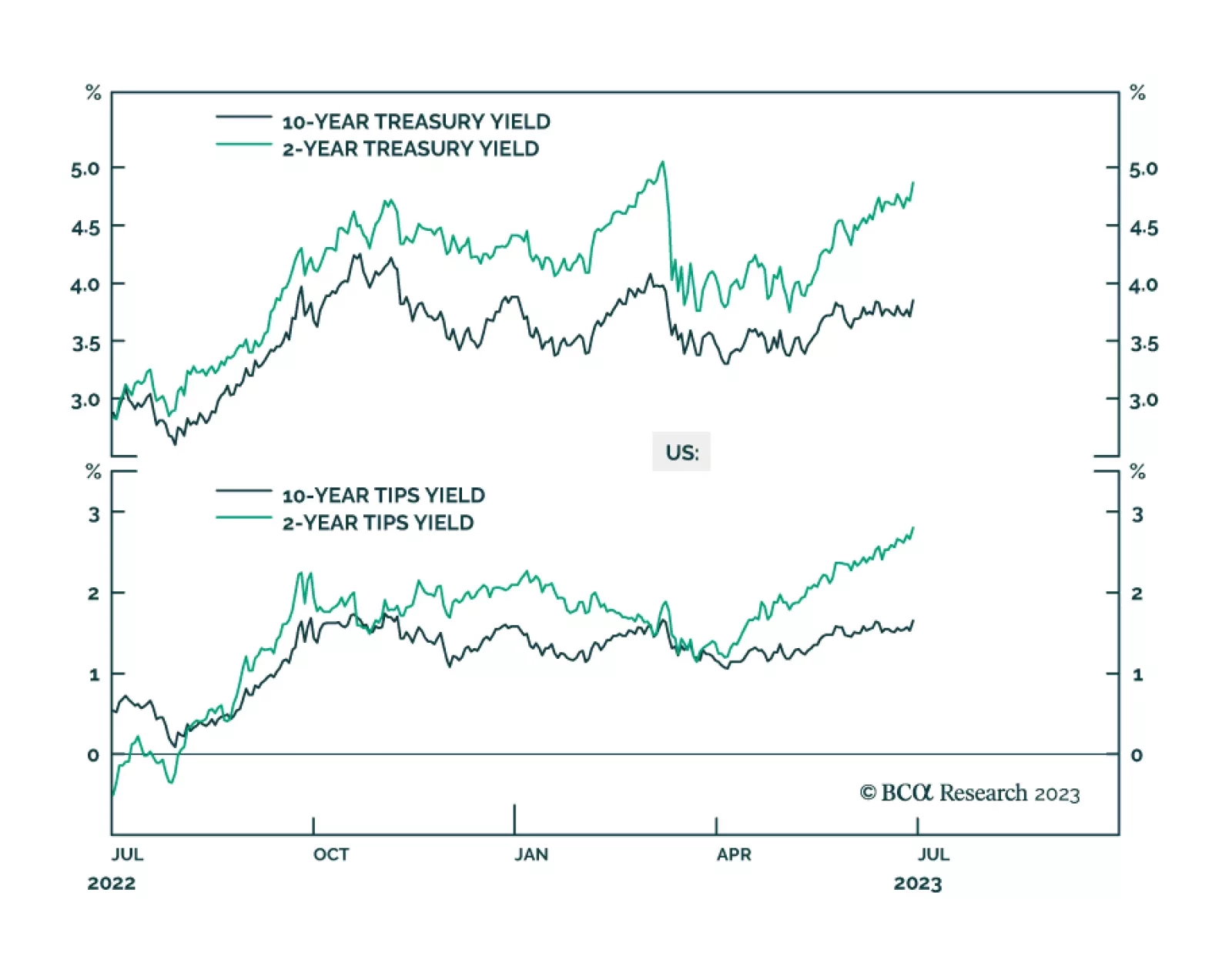

Our US Bond Strategy service responds to recent data releases which showed that real economic growth and the labor market are surprisingly resilient, while inflation pressures continued to decline. The 10-year Treasury yield broke above its top-end trading…

We build a four-stage business cycle framework based on economic growth and capacity utilization, and then analyze historical returns for most major asset allocation decisions for each stage. Given that we are in the early recession stage (negative growth coupled and an overheated economy), our framework recommends a defensive positioning across all asset classes.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.