Business Cycles

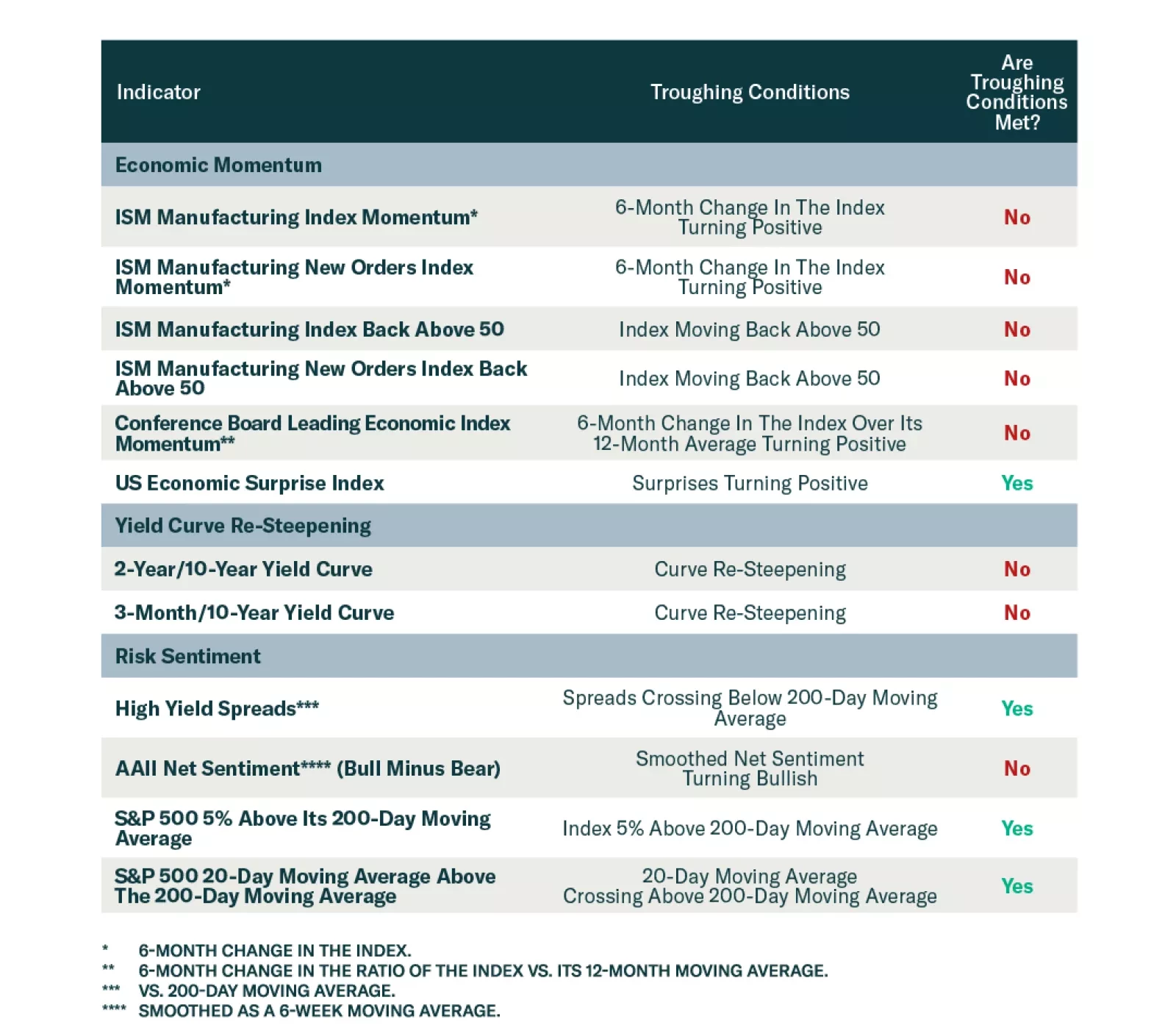

According to BCA Research’s US Investment Strategy service, the near-term consensus outlook has grudgingly improved but is still excessively bearish. Economic surprises will continue to boost stocks until a 2023 recession is fully priced out. On May 4th,…

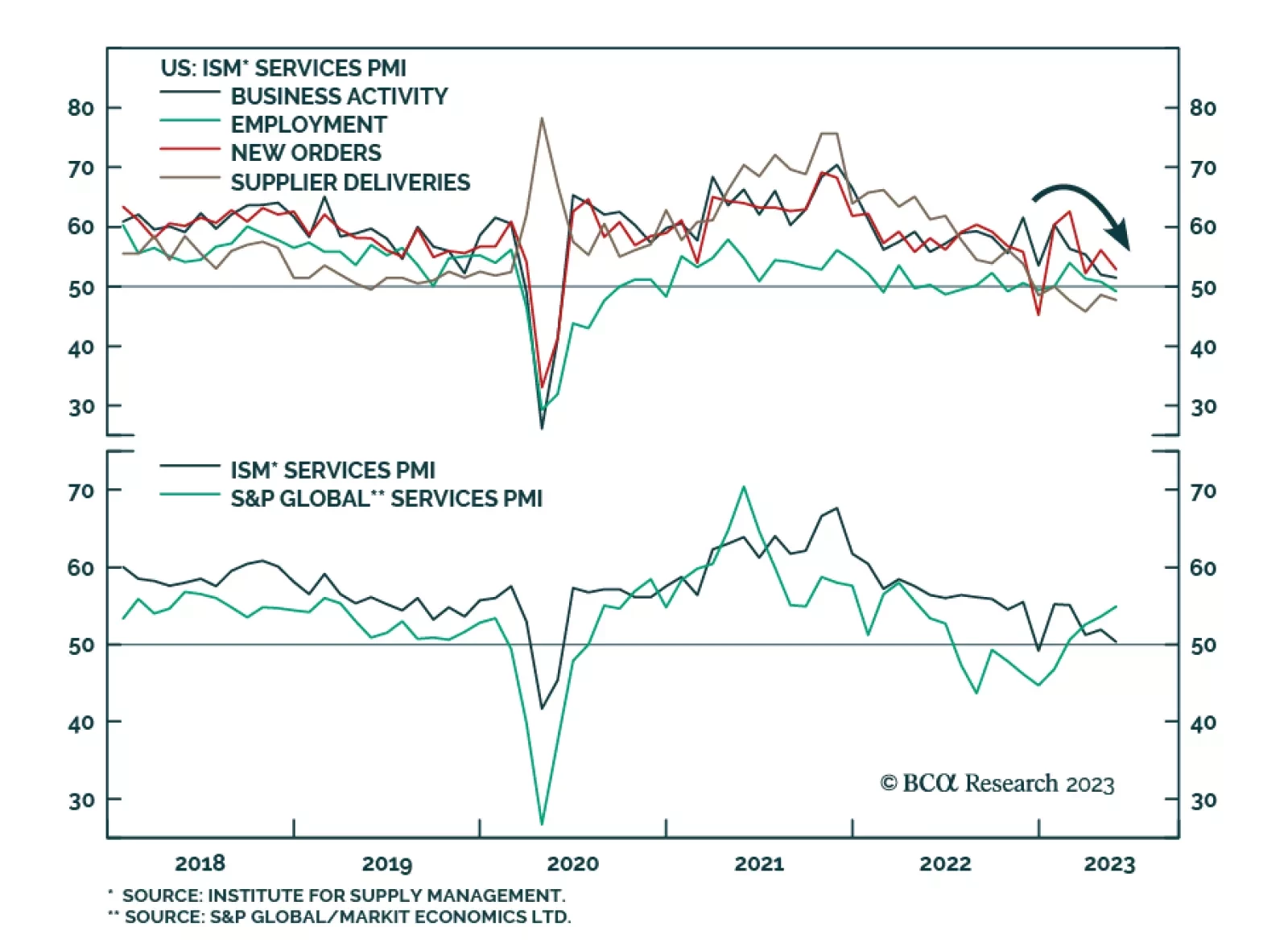

The ISM PMI sent a disappointing signal about US service sector activity in May. The headline index unexpectedly fell from 51.9 to 50.3 – the weakest level since December and surprising expectations of an improvement to 52.4. The details of the release were…

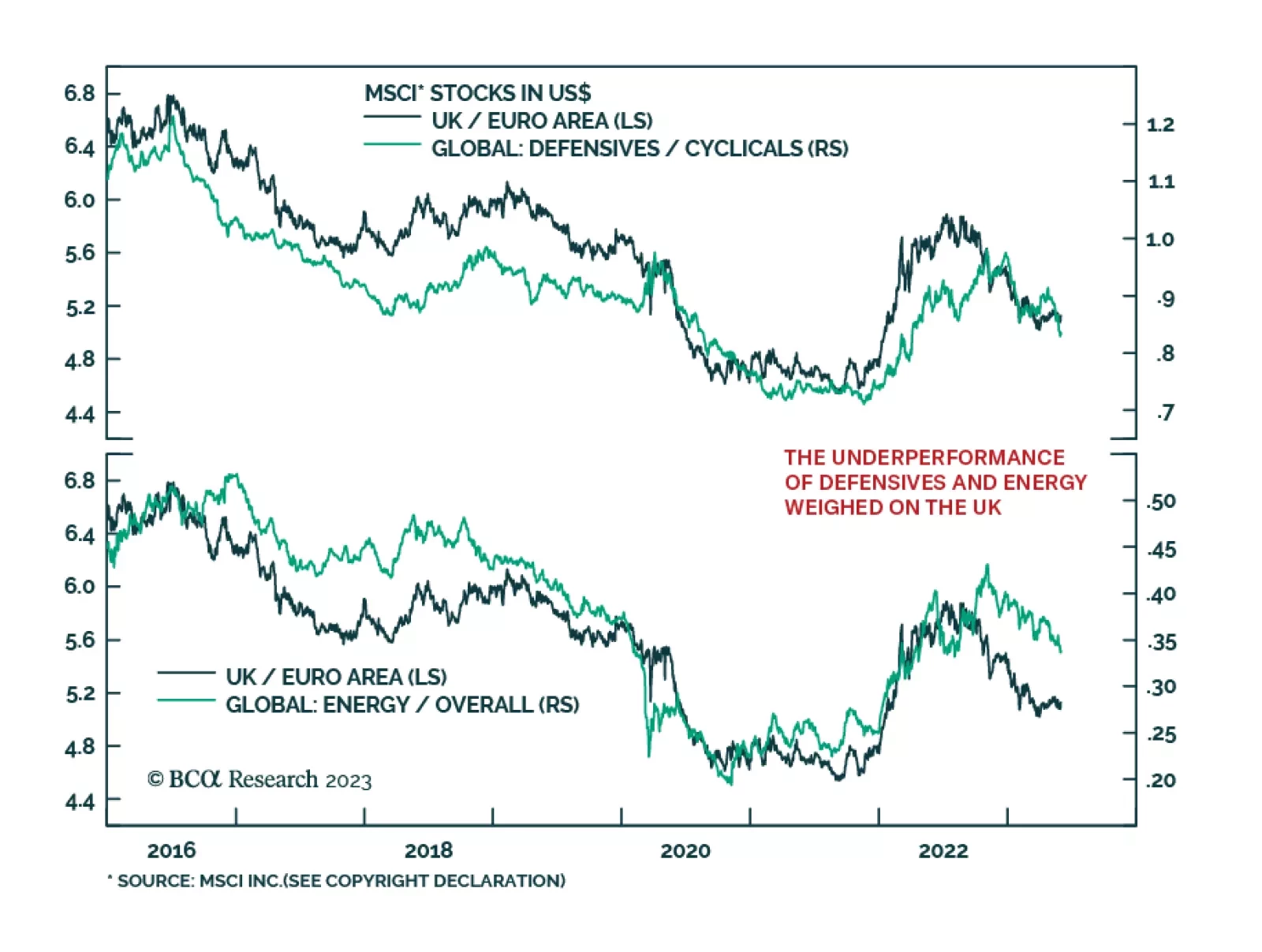

In our May In Review Insight, we showed that last month, UK stocks posted the lowest z-score among all major global equity markets, underperforming their Eurozone peers. What explains this relative weakness? The chart above reveals that the performance of…

In this short weekly report, we review some of our favorite FX trades.

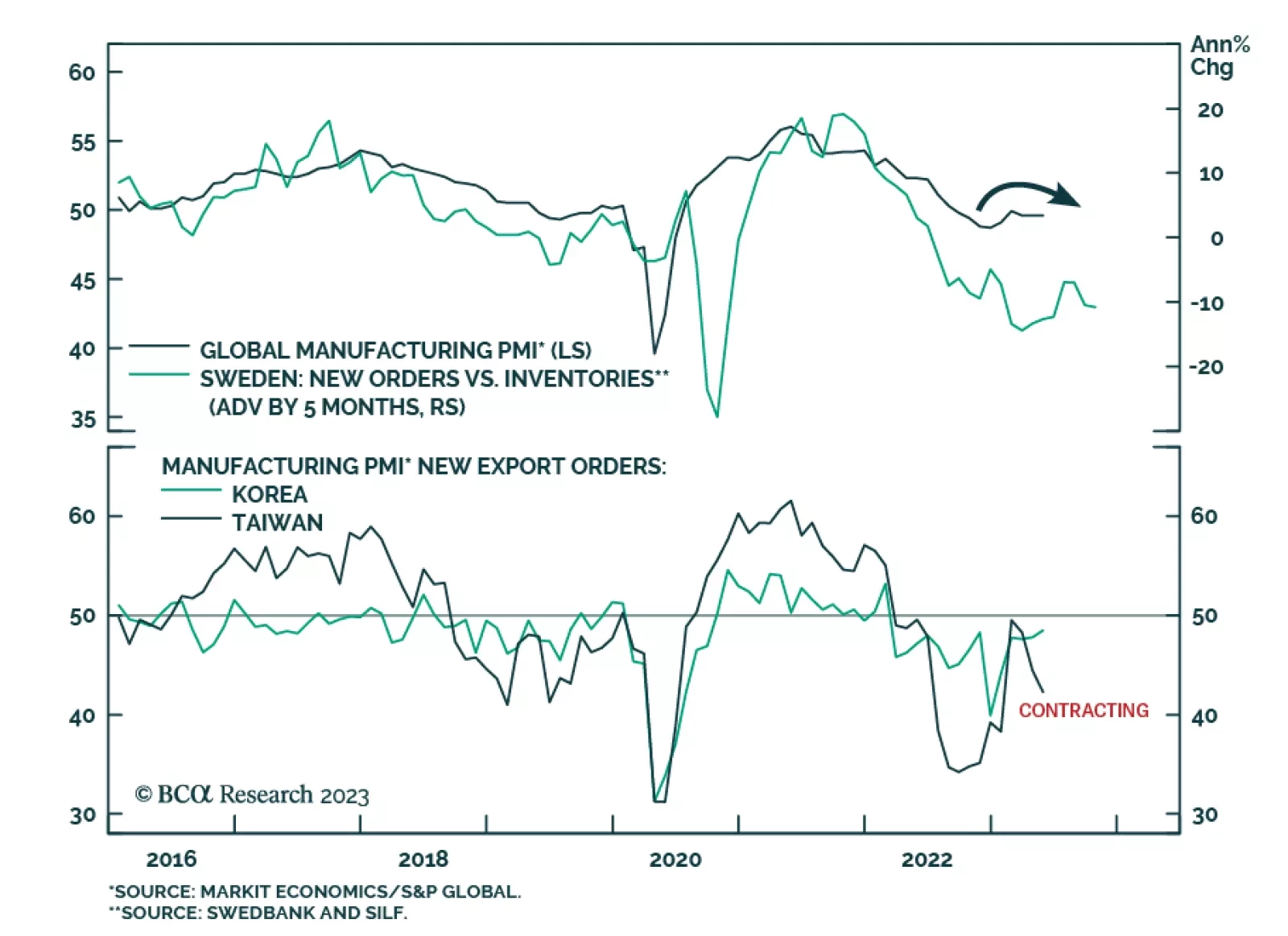

The Global Manufacturing PMI was unchanged at 49.6 in May – below the 50 boom-bust line for the ninth consecutive month. The details of the release were mixed. On the one hand, the Production sub-component rose to an 11-month high of 51.5. On the other hand,…

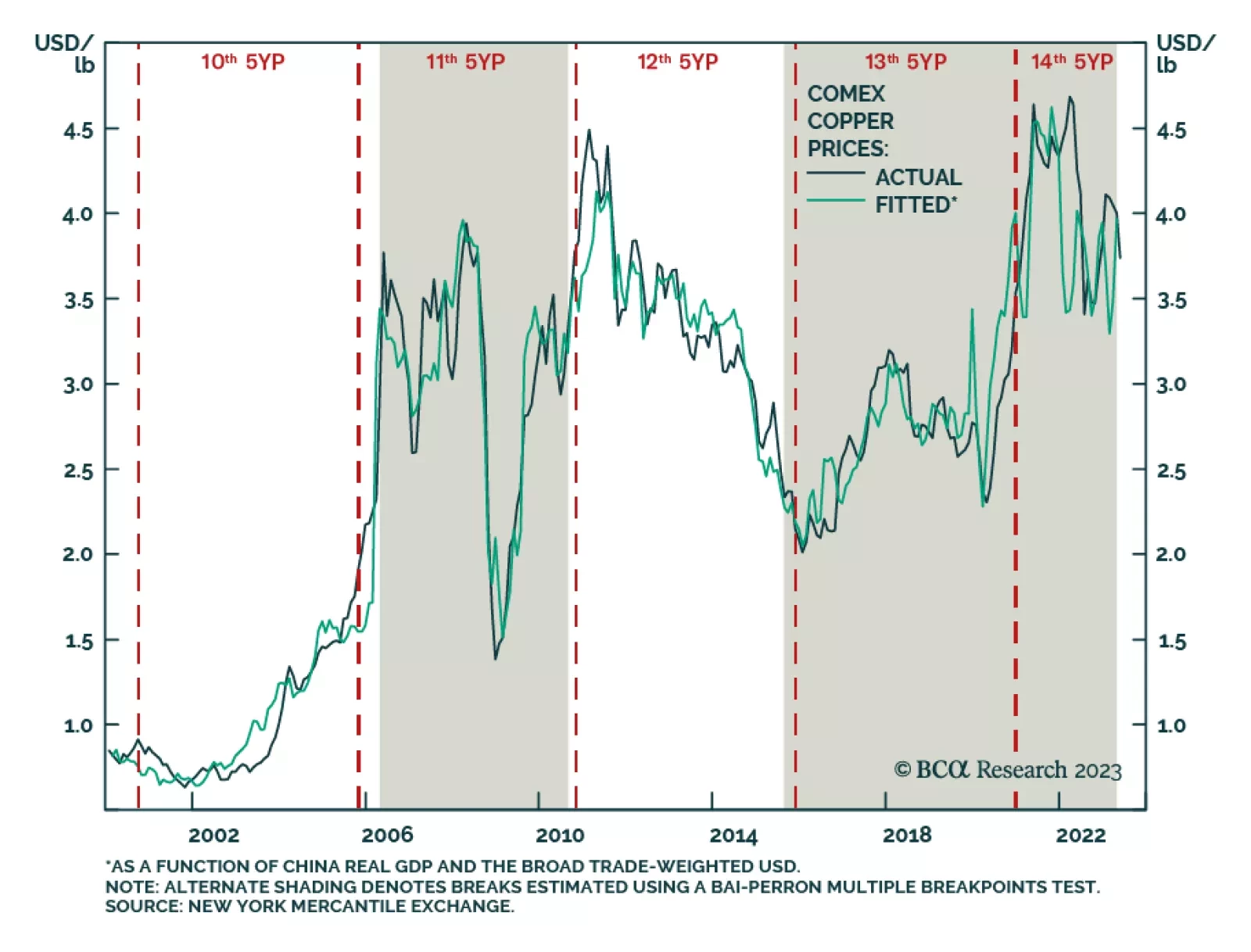

Our colleagues in BCA's Commodity & Energy Strategy (CES) service expect the Chinese Communist Party (CCP) to announce a new round of policy stimulus to re-boot the economy, in an effort to escape a prolonged liquidity trap and address continued…

BCA Research’s Global Asset Allocation service continues to recommend an overweight on government bonds, neutral on cash, and underweight on equities and credit. Market technicals do not suggest this is a robust broad-based equity rally. The US stock…

Symptoms of a liquidity trap for Chinese households are appearing. Our proprietary indicators for the marginal propensity to spend among households and enterprises continue falling. There has been a paradigm shift in Beijing’s approach to policy stimulus. Authorities will be slow to introduce large stimulus. Hence, China-related financial markets are set to fall further.

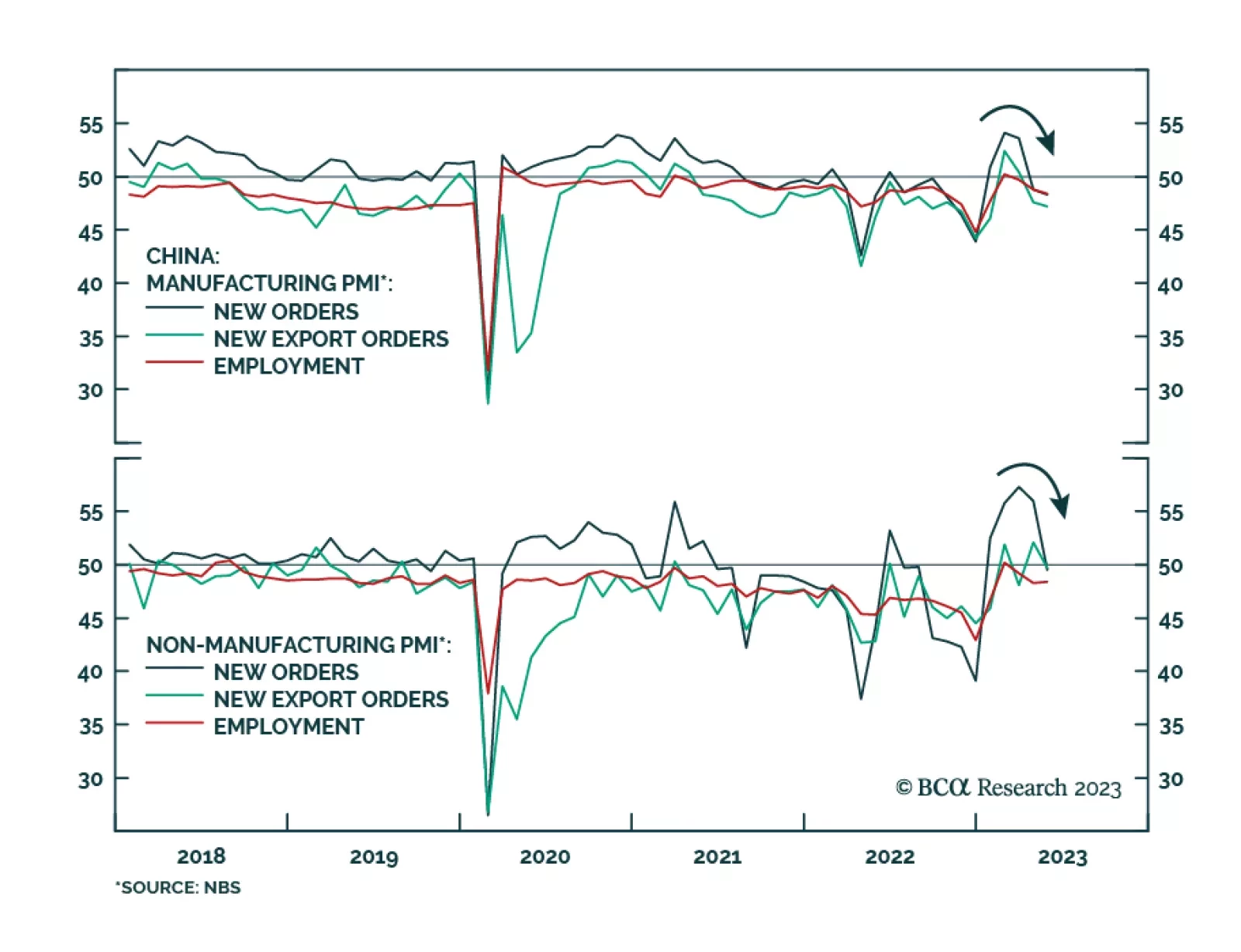

Chinese economic data releases continue to disappoint. Wednesday’s NBS PMI release showed the composite PMI dropped from 54.4 to 52.9 in May – the lowest since January. Importantly, the Manufacturing PMI unexpectedly fell deeper in contraction territory from…

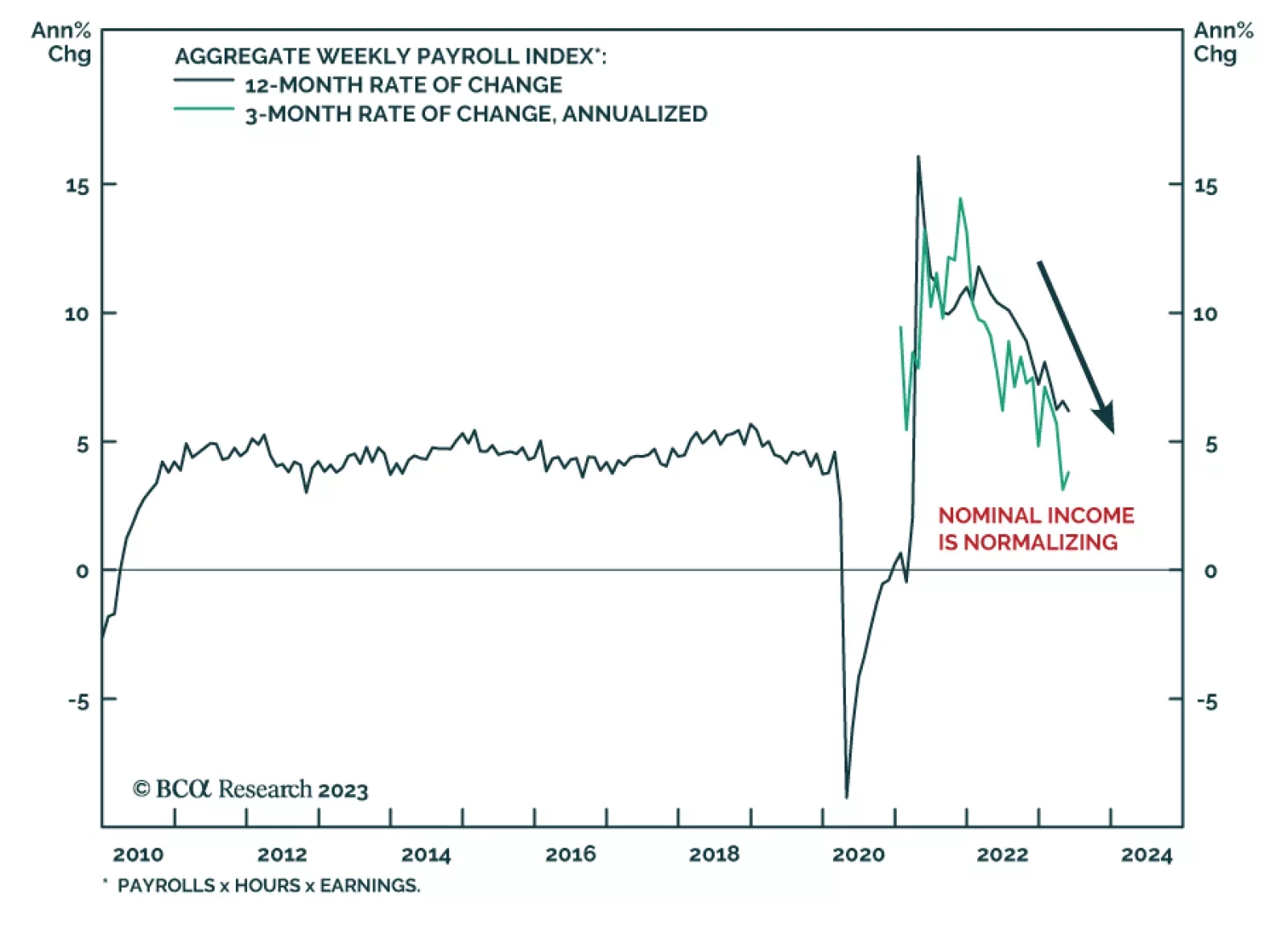

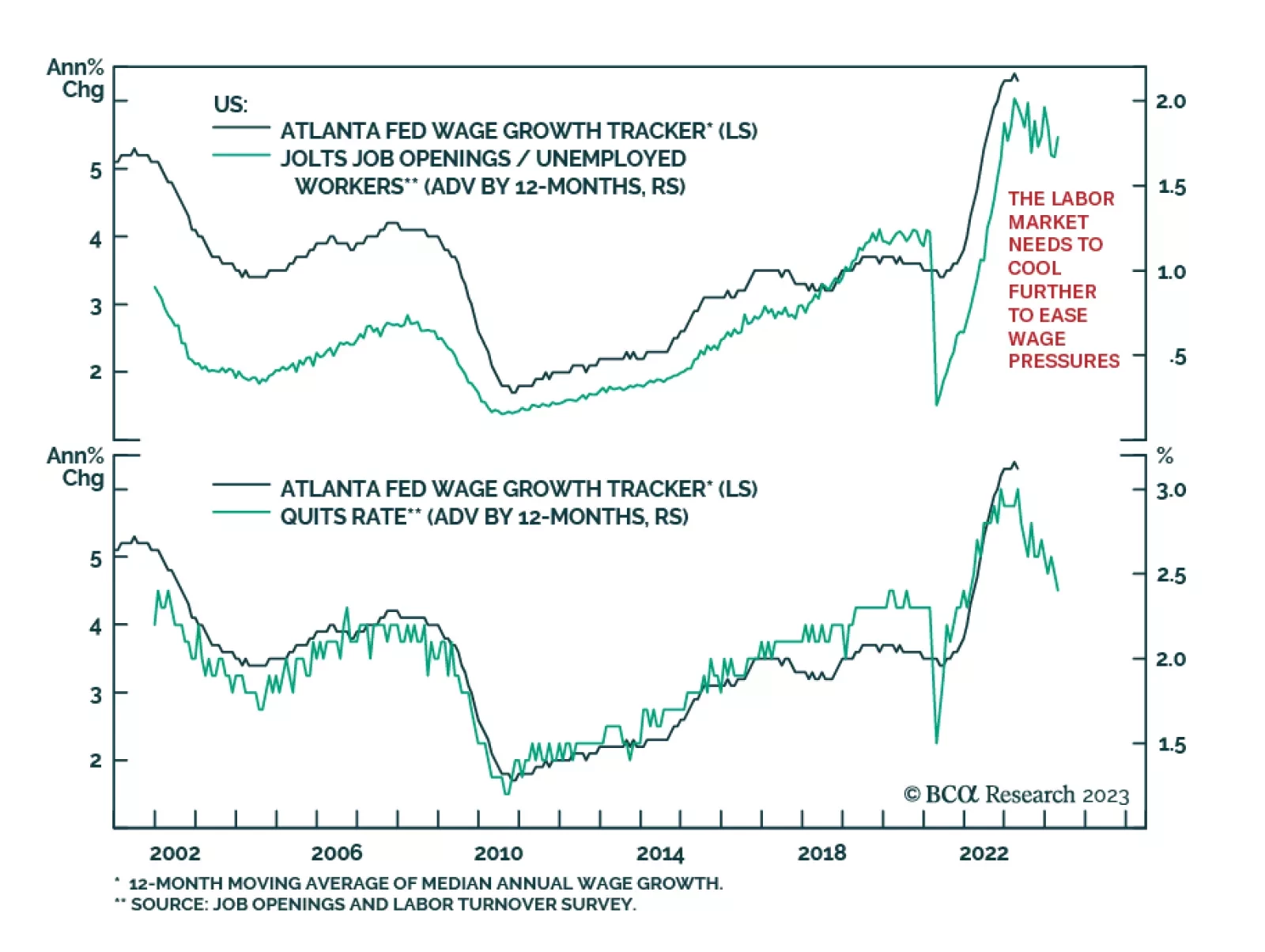

The JOLTS survey for April shows job openings unexpectedly rising from an upwardly revised 9.7 million to 10.1 million – above expectations of a decline to 9.4 million. The job openings rate inched up to 6.1% from 5.9% while the ratio of job openings to…