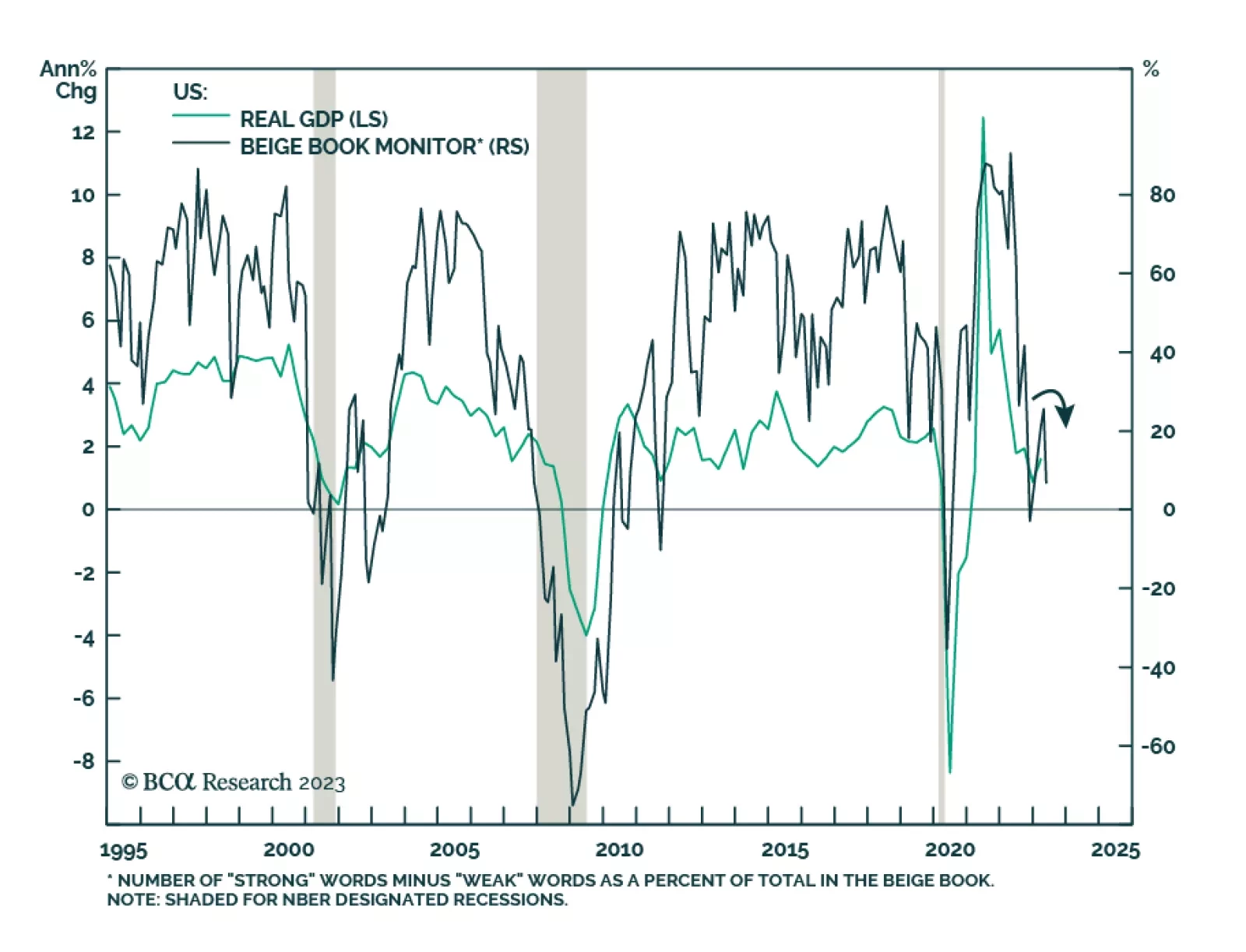

Business Cycles

President Erdogan and the Justice and Development Party emerged as the winner of the Turkish general election which was concluded yesterday. This victory means that their expansive policies of the past decade will continue, and Turkish assets will suffer. Across the Aegean, the Greeks voted to reelect the New Democrats under the leadership of Prime Minister Mitsotakis. Their fiscal prudence and structural reforms will be continued as voters had rewarded them with another term in office. Go long Greek versus Turkish equities.

Global growth will weaken in the coming months, yet monetary authorities worldwide will be reluctant to ease policy. This state of affairs foreshadows a clash between markets and policymakers in the months ahead. China’s recovery is losing steam. The latest divergence between Emerging Asian and LATAM currencies will not last.

The change in the BoE’s tone has likely altered the path for sterling. In this report, we explore if the BoE’s lens for monetary policy is justified, and provide some targets for the pound.

The change in the BoE’s tone has likely altered the path for sterling. In this report, we explore if the BoE’s lens for monetary policy is justified, and provide some targets for the pound.

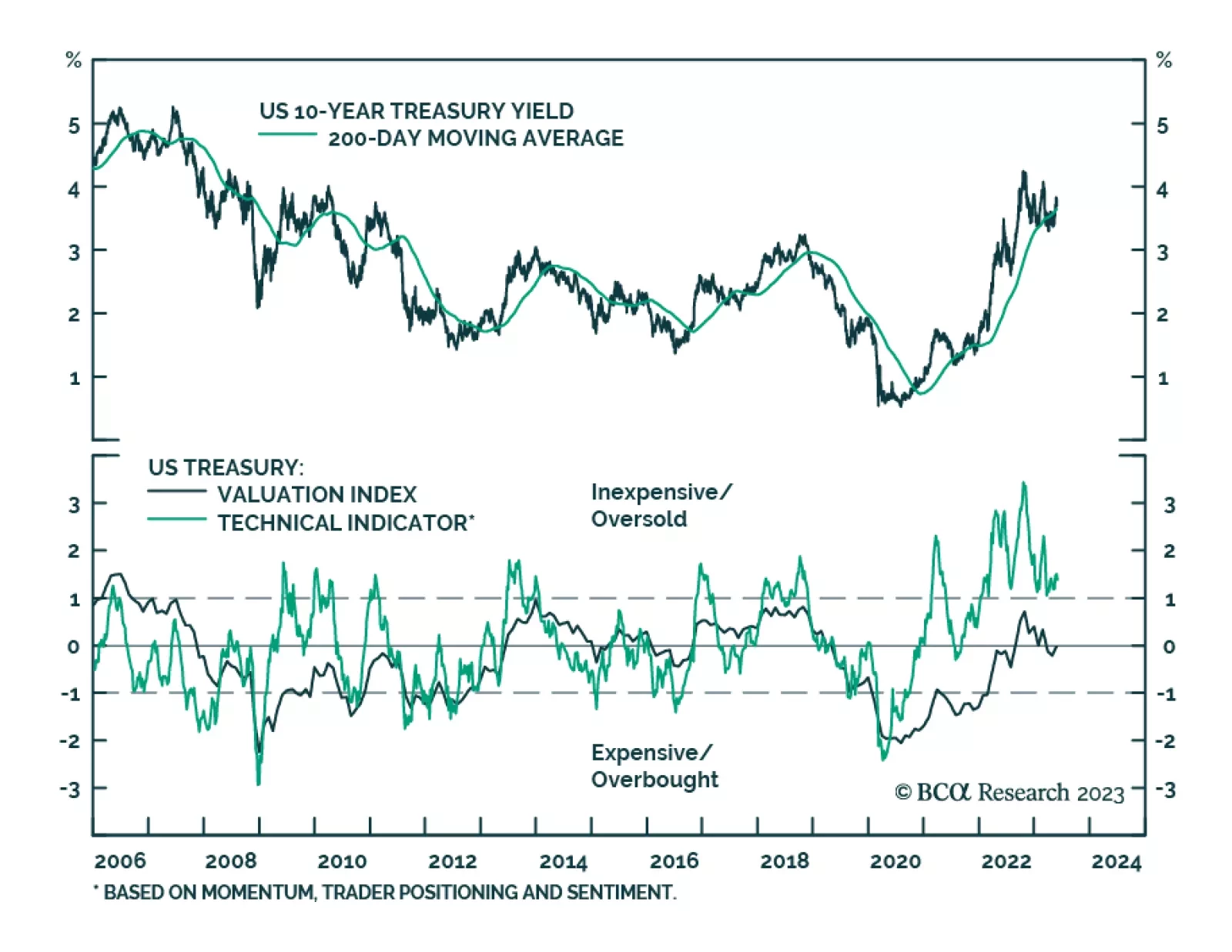

There is a 50:50 chance of experiencing a major deflationary shock in the next two years, and an even greater likelihood on a longer timeframe. The good news is that several assets provide a good insurance against this risk, and that this insurance is now cheap. Plus we highlight a compelling commodity pair-trade.

Indian EPS growth is set for major disappointments vis-à-vis the lofty expectations. Weak domestic demand amid tight fiscal and monetary policy entails more downside in stock prices. Stay underweight.

Macro and geopolitical risks may spoil the narrow window for a stock market rally before recessionary trends rise to the fore.