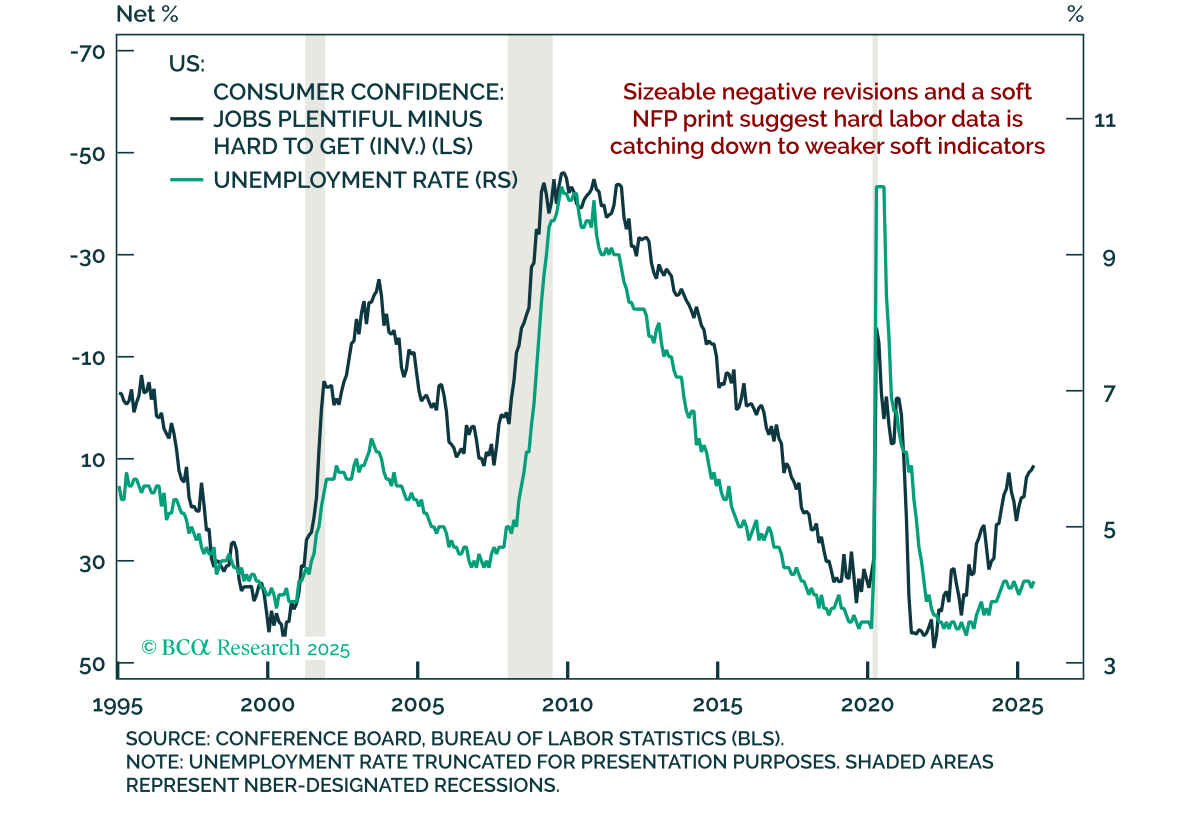

Business Cycles

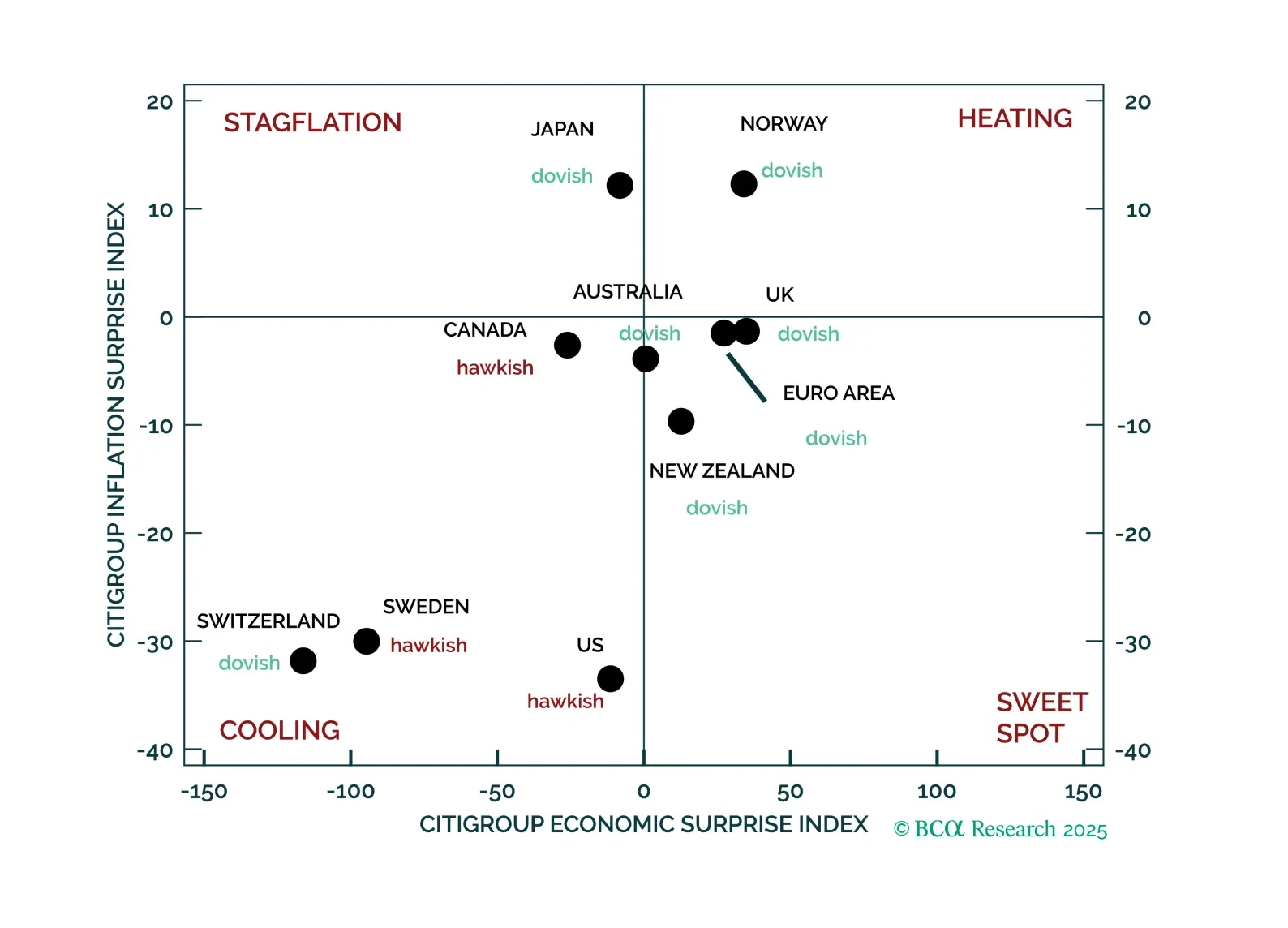

We apply a systematic approach to investing based on economic, inflation, and monetary policy surprises to the foreign exchange market. The signals from this framework are broadly consistent with the tactical views of our FX strategists, which anticipate a pause in the USD’s decline and a partial reversal of the recent euro strength.

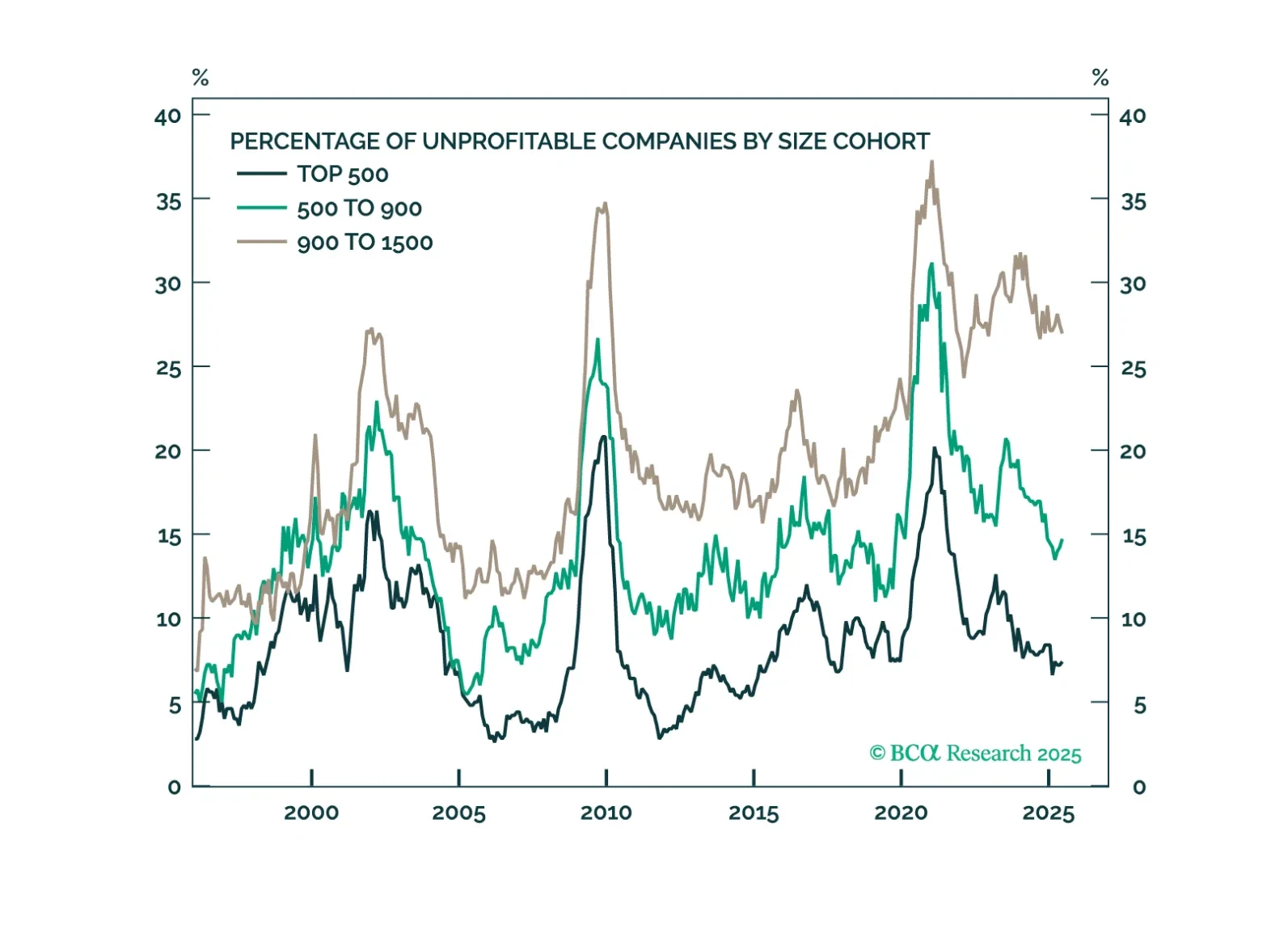

Recently, small-cap stocks have shown signs of outperformance. In this report, we examine whether the rebound is sustainable by analyzing long-term structural trends, the macroeconomic backdrop, the impact of tariffs, and other key factors.

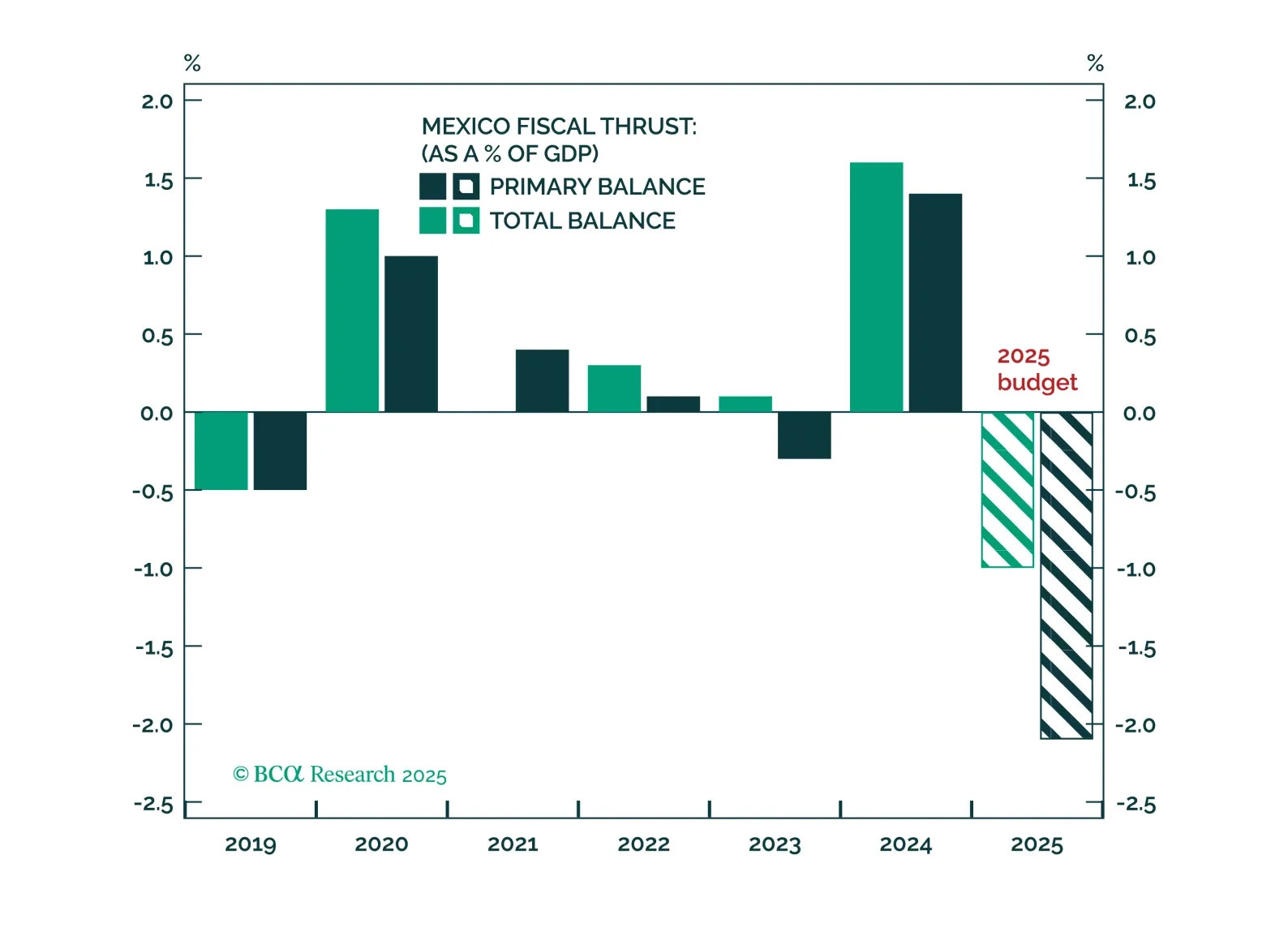

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

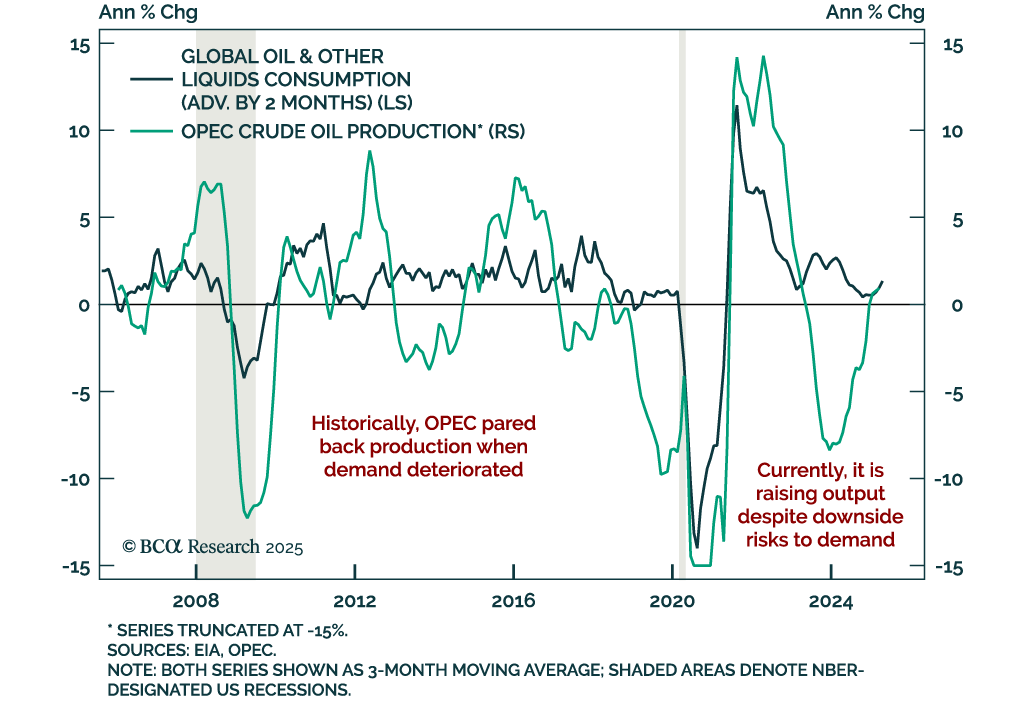

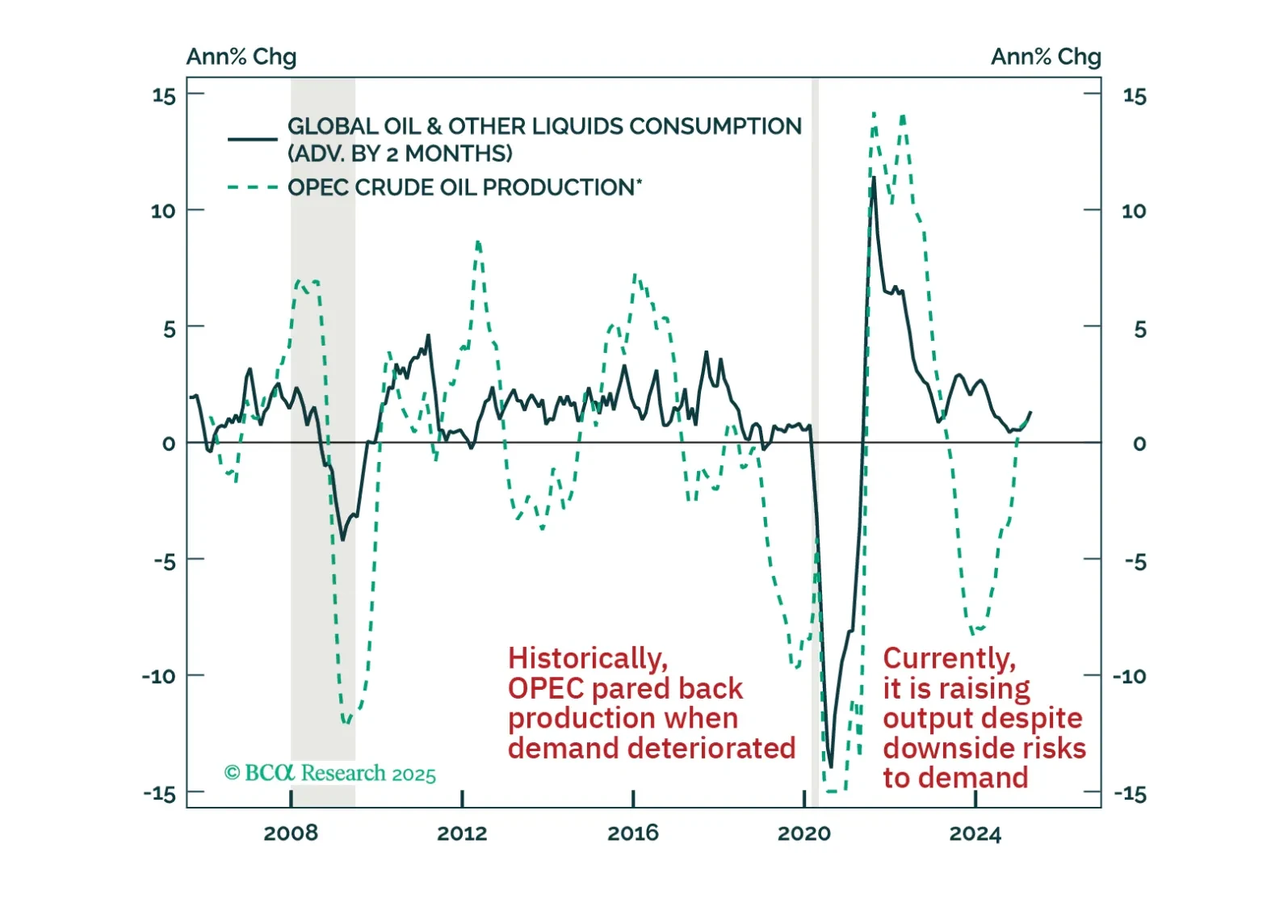

Oil has borne the brunt of the year-to-date deterioration in cyclically sensitive financial assets. It is a key underperformer both within the commodity space and among global risk assets. This underperformance underscores that in addition to the trade war-induced headwind to demand, bearish supply-side developments are also weighing down on crude prices. As we discuss in this report, these dynamics will likely continue exerting downside pressure on oil prices over the coming weeks and months.

Europe’s near-term outlook remains clouded by uncertainty, even after the tariff reprieve. Our latest update breaks down why the risks to growth, profits, and financial conditions are still skewed to the downside — with Sweden standing out as a key bellwether.

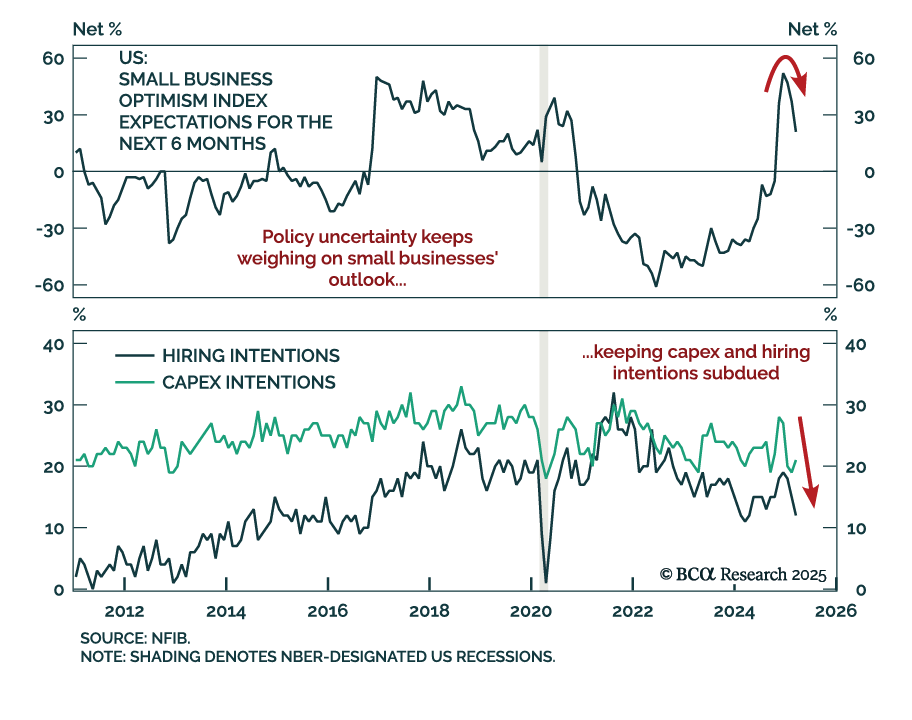

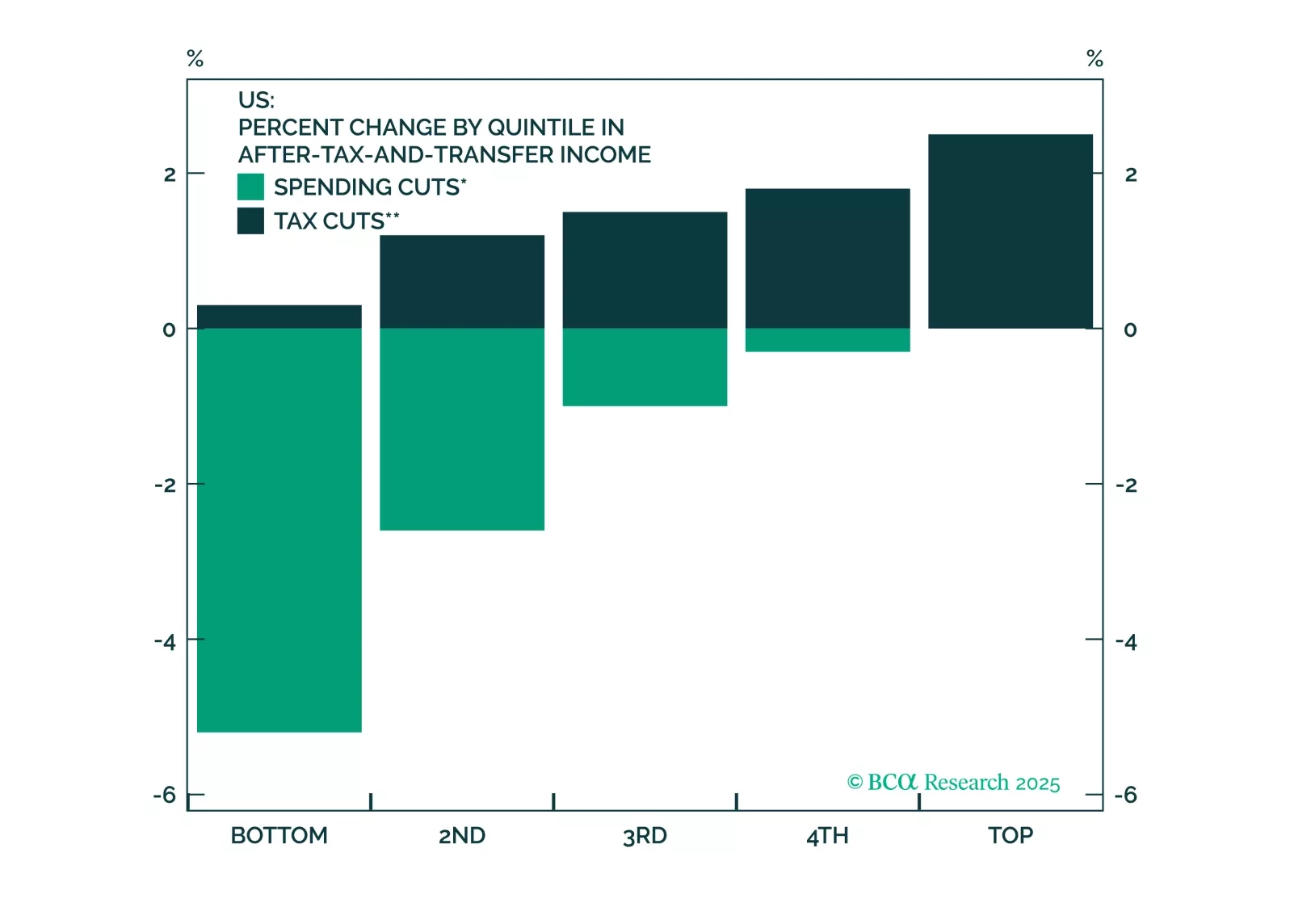

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.