Business Cycles

The disinflationary trend in US CPI continued in June as headline CPI dipped to 3% year-over-year, down from 3.3% in May, and core CPI declined by a tick to 3.3%. On a month-over-month basis, headline prices fell by 0.1% and core prices rose by 0.1%. One…

The NFIB Small Business Optimism (SBO) index climbed from 90.5 to 91.5 in June, the highest print this year, topping consensus expectations of a softening to 90.2. On the surface, this appears to be good news. Indeed, small businesses are particularly…

As highlighted in Wednesday’s edition of BCA Live & Unfiltered, the Chinese economy and its financial markets face several daunting challenges. Its demographic outlook is unfavorable, with a low birthrate stifling population growth; the grim math of…

Copper has experienced a roller-coaster ride so far this year, with front-month futures on the Chicago Mercantile Exchange gaining nearly 40% from early February to late May, tumbling nearly 15% in just over five weeks, and bouncing around 7% over the last…

Our colleagues from the Emerging Markets Strategy team argue that investors should brace for a significant correction in Indian stocks in the coming months. They posit that the pillar of Indian corporations' sustained profit growth — surging revenues — is…

Participants in the Philly Fed’s Survey of Professional Forecasters (SPF) assign a 26% probability to a contraction in US real GDP four quarters from now, down from their 44% peak probability in 2022. The unwieldy contraction-in-four-quarters wording makes…

We expect continued softening in the US economy will lead to decelerating wage growth, muffling the principal consumption driver. Because the US has been the foremost catalyst for global growth in this cycle, a US recession will eventually morph into a global…

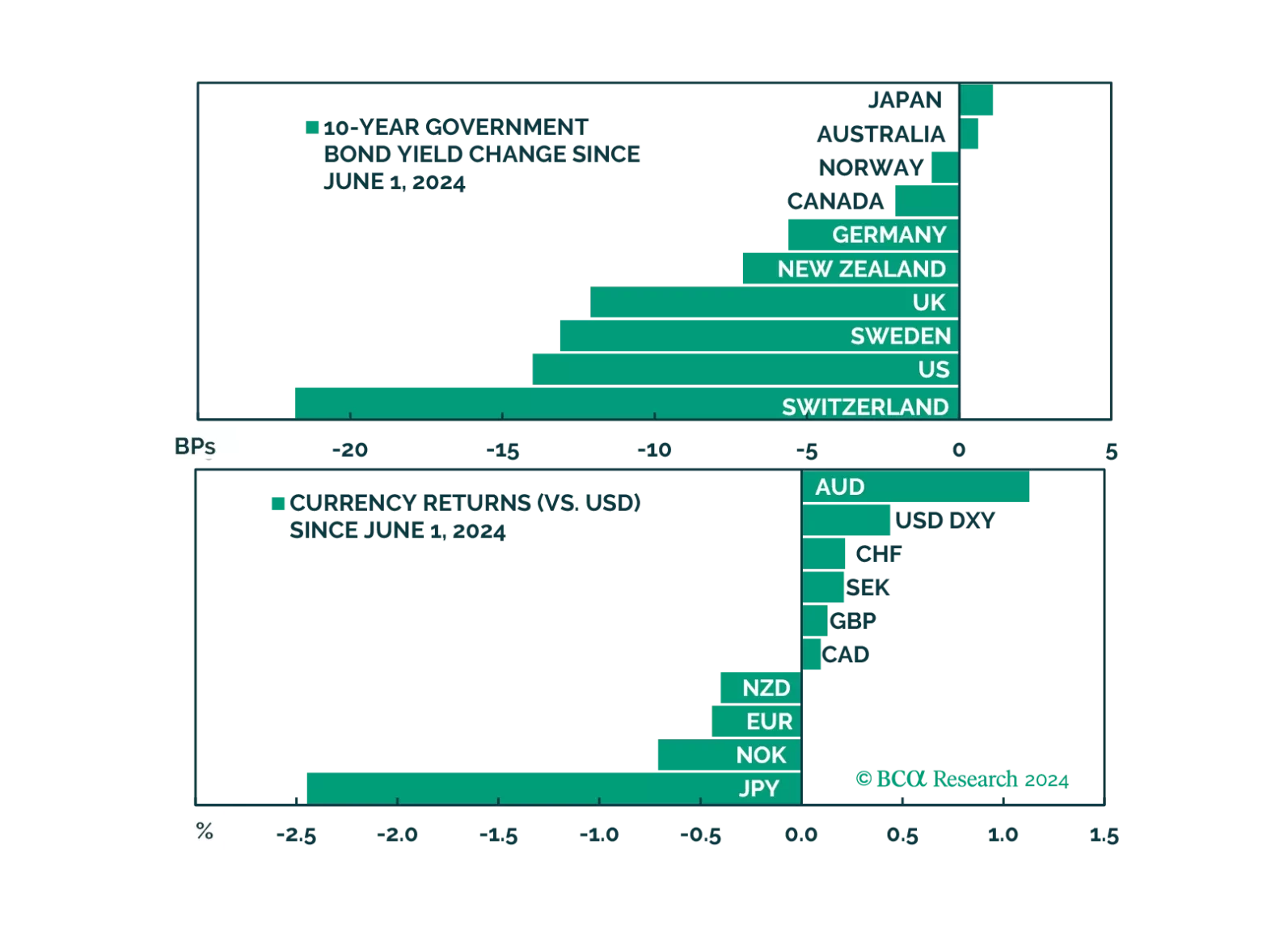

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.

The stabilization in global growth continued in June. The JPM Global Manufacturing PMI came in at 50.9, nearly in line with May’s 22-month high. However, international trade flows deteriorated notably. The new export orders component started contracting in…

The US unemployment rate stands at just 4.0% today following 27 consecutive sub-4% readings. Does this low unemployment rate guarantee a soft landing in the US economy? Our Global Investment Strategy (GIS) team’s base case is that the US economy will fall…