Business Cycles

In this Insight, we revisit our "higher for longer" theme for the Reserve Bank of New Zealand, in light of the latest central bank meeting. In conclusion, we are inching towards a more dovish RBNZ ahead. Ergo, we recommend some fixed income and currency trades.

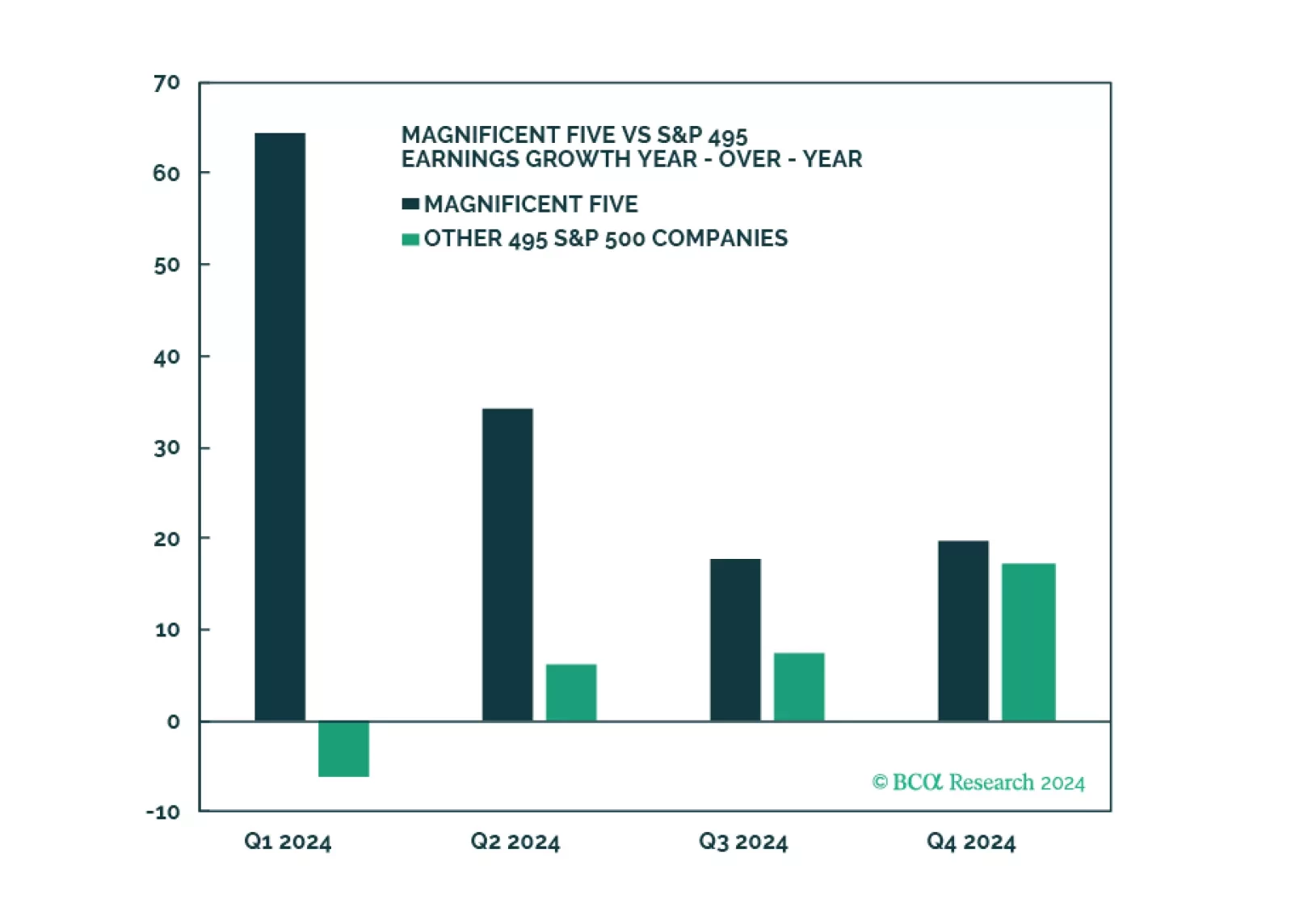

Q1 Earnings and sales growth were strong, but the devil is in the details: Without the Magnificent Five, earnings growth for the index would have been negative. On a positive note, margins have stabilized, and earnings growth is expected to broaden into yearend. Companies are optimistic about the economy. Development of AI applications is in full swing, but few companies are monetizing them yet. Consumer spending is strong but is slowing. We reiterate our underweight of consumer sectors, and overweight of Software and Services as the “don’t fight AI” adage holds.