Business Cycles

The 303-thousand increase in nonfarm payrolls in March came in well above consensus expectations of a moderation from 270 thousand to 214 thousand. Healthcare, the public sector and construction were the top contributors to employment growth. Moreover, the…

The past week brought a slew of positive US economic data, all suggesting that conditions remain robust and a recession is not imminent. The ISM Manufacturing PMI crossed into expansion for the first time since September 2022, the number of job openings…

BCA Research’s Foreign Exchange Strategy service maintains a neutral view on the dollar for the next three months. The team continues to believe that the dollar is due for a long-term bear market, but momentum is in favor of the DXY in the near term. …

As a small open economy, Sweden’s economic performance is a good barometer of global growth developments. Swedish PMIs for March were overall positive. The Manufacturing PMI rose to the 50 boom-bust line following 19 consecutive months of contraction and…

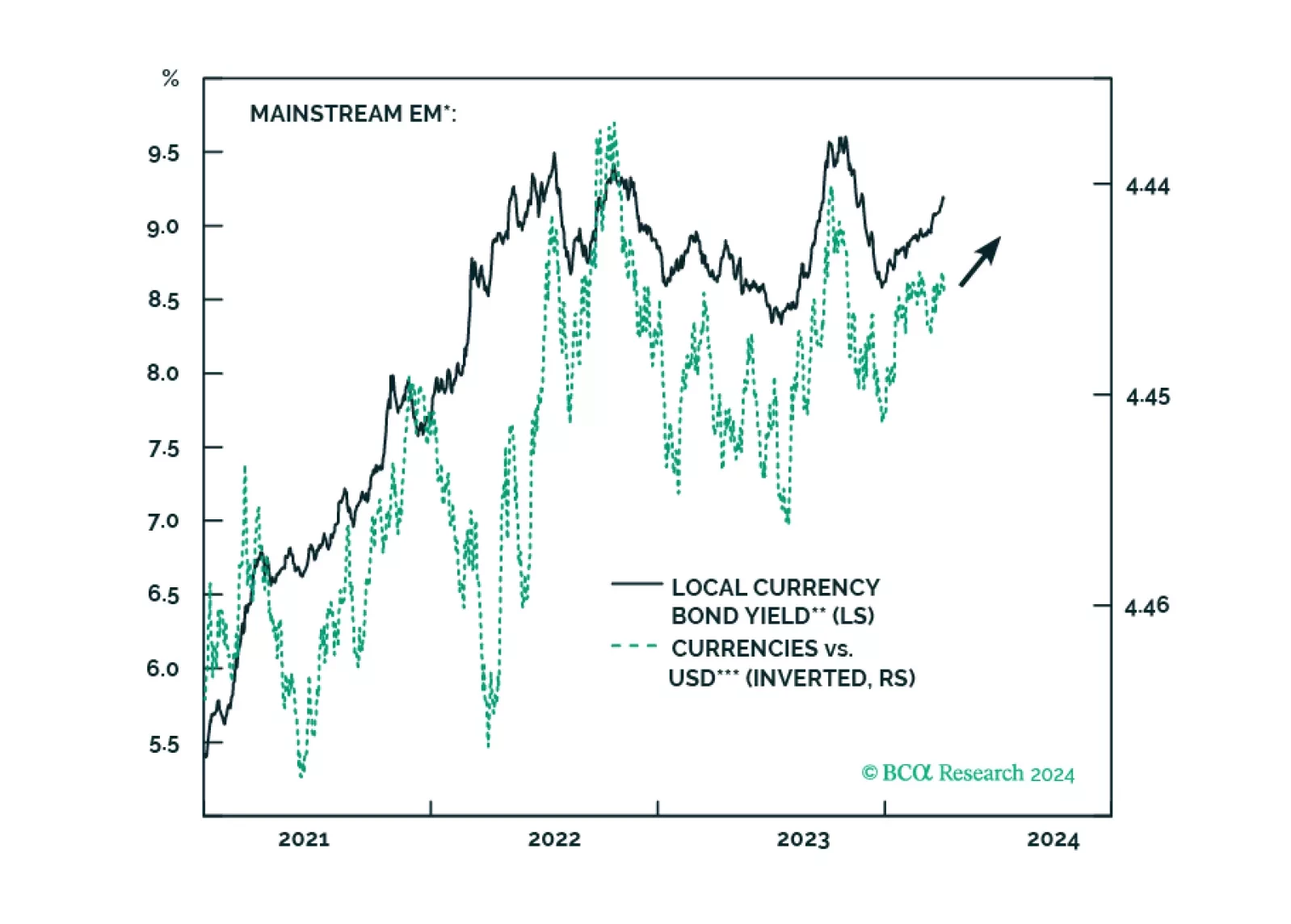

Climbing US bond yields, alongside higher oil prices, might spoil the party for global risk assets. There are budding cracks in EM domestic bonds, and even though we like this asset class in the long run, investors exposed to it should reduce their positions for now.

The extraordinary performance of AI companies has pushed US growth stocks to new highs. So far, the MSCI US Growth Index has returned almost 11% since the start of the year, outperforming global stocks by over 3%. No growth index from the rest of the world…

According to BCA Research’s China Investment Strategy service, the growth rate of China’s infrastructure investment will likely slow from a nominal 9% last year to about 6% this year. Funding constraints will limit local government capability to invest in…

The ISM Manufacturing PMI came in at 50.3 in March, better than expectations of 48.4 and breaking above the 50 boom-bust line for the first time since September 2022. Notably the new orders component rebounded to 51.4, marking the second expansionary reading…

BCA Research’s US Investment Strategy service is watching households, the labor market and consumer credit for signs of a business cycle inflection and the all-clear signal to underweight equities. Equity bear markets and recessions tend to…

The equity rally extended into March as hard landing outcome was priced out. It has broadened, as money flowed into less over-loved pockets of the market. Our models signal that margins are about to stabilize, and earnings growth will accelerate as the year progresses. However, companies are raising prices again and the no-landing outcome and fewer than three rate cuts this year are increasingly likely.