Business Cycles

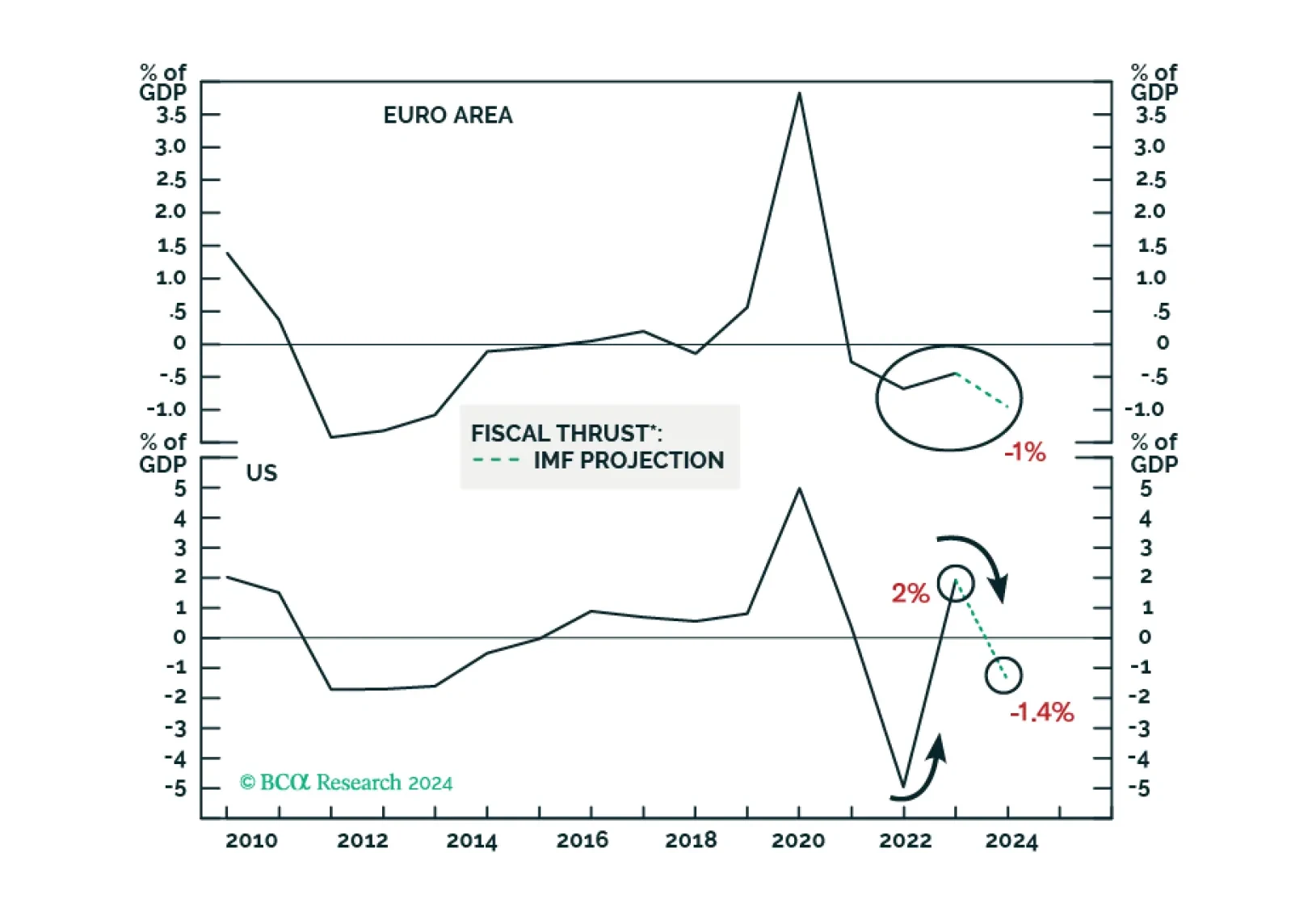

Despite a couple of rate cuts in H2 2024, borrowing costs will remain elevated in real terms amid lower inflation in the US and Europe. This and tightening fiscal policy will hinder domestic demand in advanced economies. Domestic demand in China and EM ex-China will remain very tepid, with risks skewed to the downside.

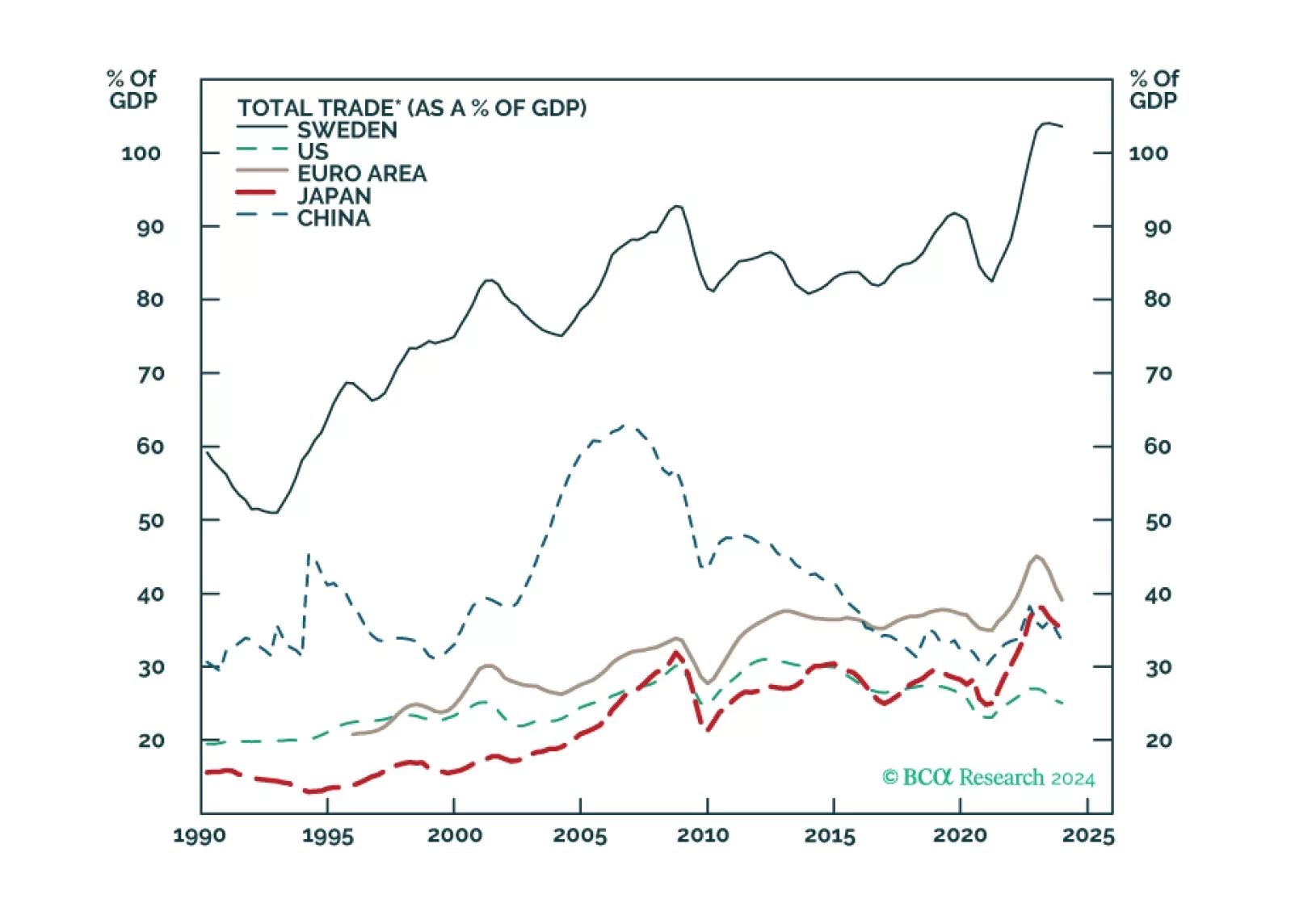

In this joint Foreign Exchange Strategy and Global Investment Strategy Special Report, we assess economic activity in Sweden, a highly cyclical and trade-oriented economy, and its implications for the global growth outlook.

The 10.4% contraction in Taiwanese export orders for February delivered a negative surprise to expectations that the pace of expansion would slow from 1.9% y/y to 1.2% y/y. However, investors should not read too deeply into this weaker-than-anticipated…

Citigroup’s economic surprise index for the Euro Area has been on a steady ascent since mid-2023. Its continued increase after breaking into positive territory at the start of February indicates that the region’s economic data are generating positive…

According to BCA Research’s China Investment Strategy service, the adjustment in China’s real estate sector is not over. Odds are that the property market will contract for the fourth year in a row. The property market indicators continue to paint a grim…

Canada’s CPI release for February shows price pressures continue to ebb with the various measures of inflation all falling below consensus estimates. In particular, headline inflation decelerated from 2.9% y/y to 2.8% y/y – its lowest since March 2021 and…

Various indicators of Eurozone wage growth have cooled off in recent months. Notably, the labor costs index eased sharply from a downwardly revised 5.2% y/y to 3.4% y/y in 2023Q4 – the slowest pace of increase since Q3 2022. Alternative measures such as…

Indicators continue to point to resilient US housing market dynamics. The NAHB Housing Market Index increased for the fourth consecutive month to an 8-month high of 51 in March, beating expectations it would remain unchanged at 48. Increases across all three…

Singapore non-oil exports (NODX) largely disappointed in February, contracting by 4.8% m/m following a 2.3% m/m expansion in January, and falling below expectations of a milder 0.5% m/m decline. In a similar vein, the 0.1% y/y decline in February fell below…

In a recent Insight we highlighted that the selloff in the price of iron ore – which is down 25.4% year-to-date – is sending a pessimistic signal on China’s economy, suggesting that the current rally in Chinese stocks is unlikely to persist over a cyclical…