Business Cycles

This week, we review our currency positions, based on the latest data from G10 economies.

In the past couple of years, Mexico has been among the favorite markets for investors within the EM space. As our Emerging Markets Strategy team argued in a recent report, the cyclical and structural outlook for Mexican risk assets remains brighter than ever.…

Our Emerging Market Strategy (EMS) colleagues recommended booking an 11.4% gain on their Egyptian T-bill trade initiated earlier in the year. Now that currency-devaluation risk has been removed from the picture for the foreseeable future, they are…

A market-cap weighted index of CE3 economies (Poland, Hungary and Czechia) returned a whopping 64% in common currency terms since its 2022 low. Polish and Hungarian equities led the rally, advancing by a respective 86% and 78% in local currency terms…

The US January JOLTS data released yesterday was in line with expectations, with job openings clocking in at 8.86 million versus a downwardly-revised 8.89 million in December. Importantly, US job openings are likely to continue trending lower in February…

The Bank of Canada (BoC) kept its policy rate steady at 5% for the sixth consecutive meeting yesterday, in line with expectations. The BoC, which has changed its communication policy to now provide a press conference after every meeting, reasserted the need…

BCA’s European Investment Strategy team continues to expect the German economy to trail that of the rest of Europe. Since 2020, Germany has fallen behind, with its real GDP lagging that of the broader Eurozone by 5%. The contribution of consumption to GDP…

Data out of Norway is becoming increasingly positive, and there is a strong investment case to be made for the country, with bullish implications for both equities and the currency: Retail sales remain robust and are catching up to the improvement we…

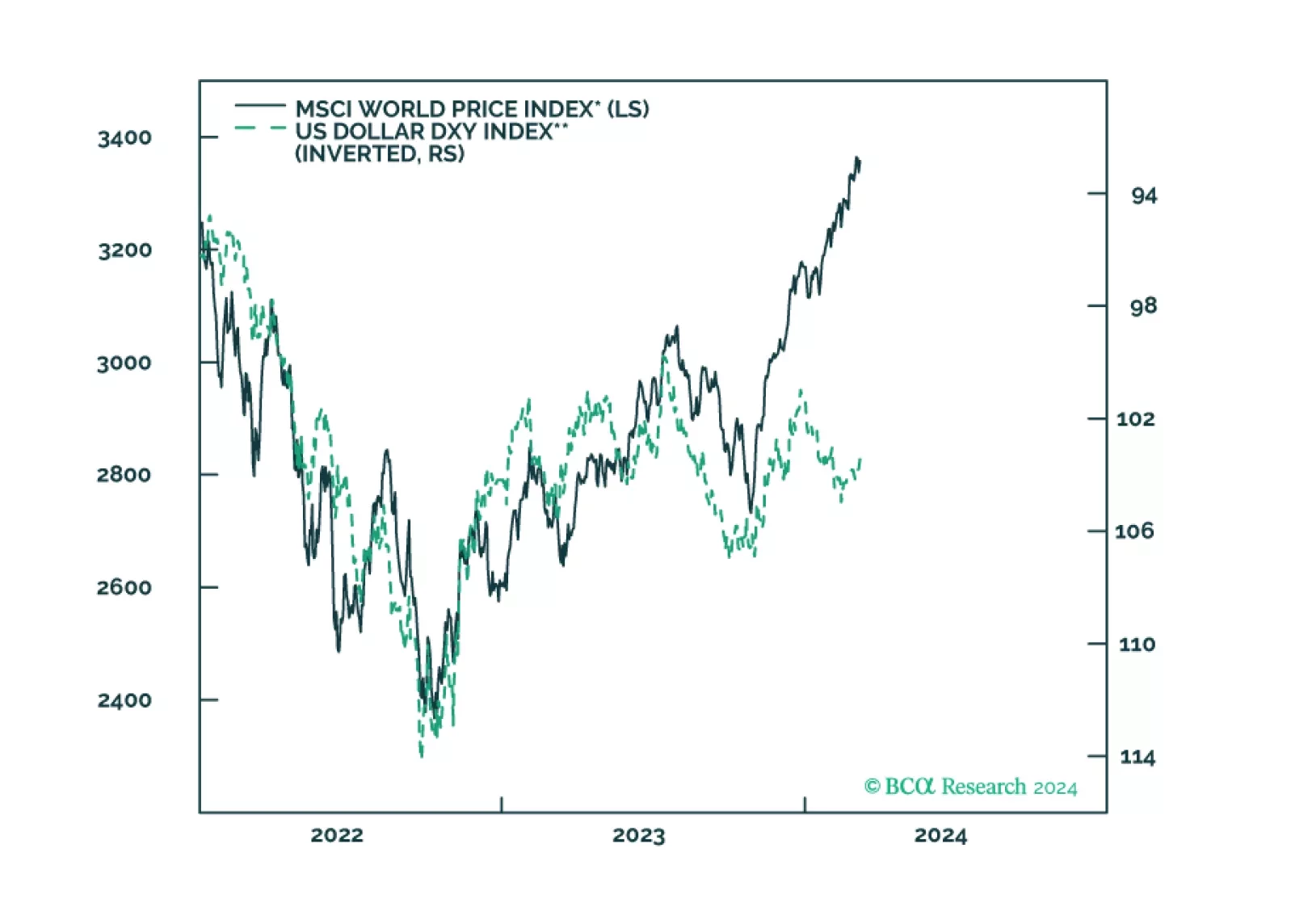

We noted in a previous Insight that recent comments from Raphael Bostic, President of the Federal Reserve Bank of Atlanta, may reflect a growing realization among policymakers that they have inadvertently caused a significant easing in financial…

The stock market of the Eurozone’s largest economy keeps grinding higher with the DAX 40 closing at new highs last week. Since its October low, the index of German blue-chip companies advanced by 20%. Does this rally have legs? On a relative basis,…