Business Cycles

2023 was an unexpectedly good year for global financial markets. Most of the major financial assets we track generated positive abnormal gains. Although US stocks outperformed their global counterparts, Eurozone, Japanese, and EM ex-China equities led in…

Economists have been consistently revising up their 2024 US GDP forecasts over the past 4 months. The consensus now anticipates US growth to clock in at 1.3% this year. According to the latest estimate from the Atlanta Fed’s GDPNow model, this will follow…

December PMIs indicate that the global manufacturing sector is not experiencing a meaningful rebound. The Global Manufacturing PMI declined from 49.3 to 49.0 in December, marking the sixteenth consecutive month of a sub-50 reading. The output, new orders,…

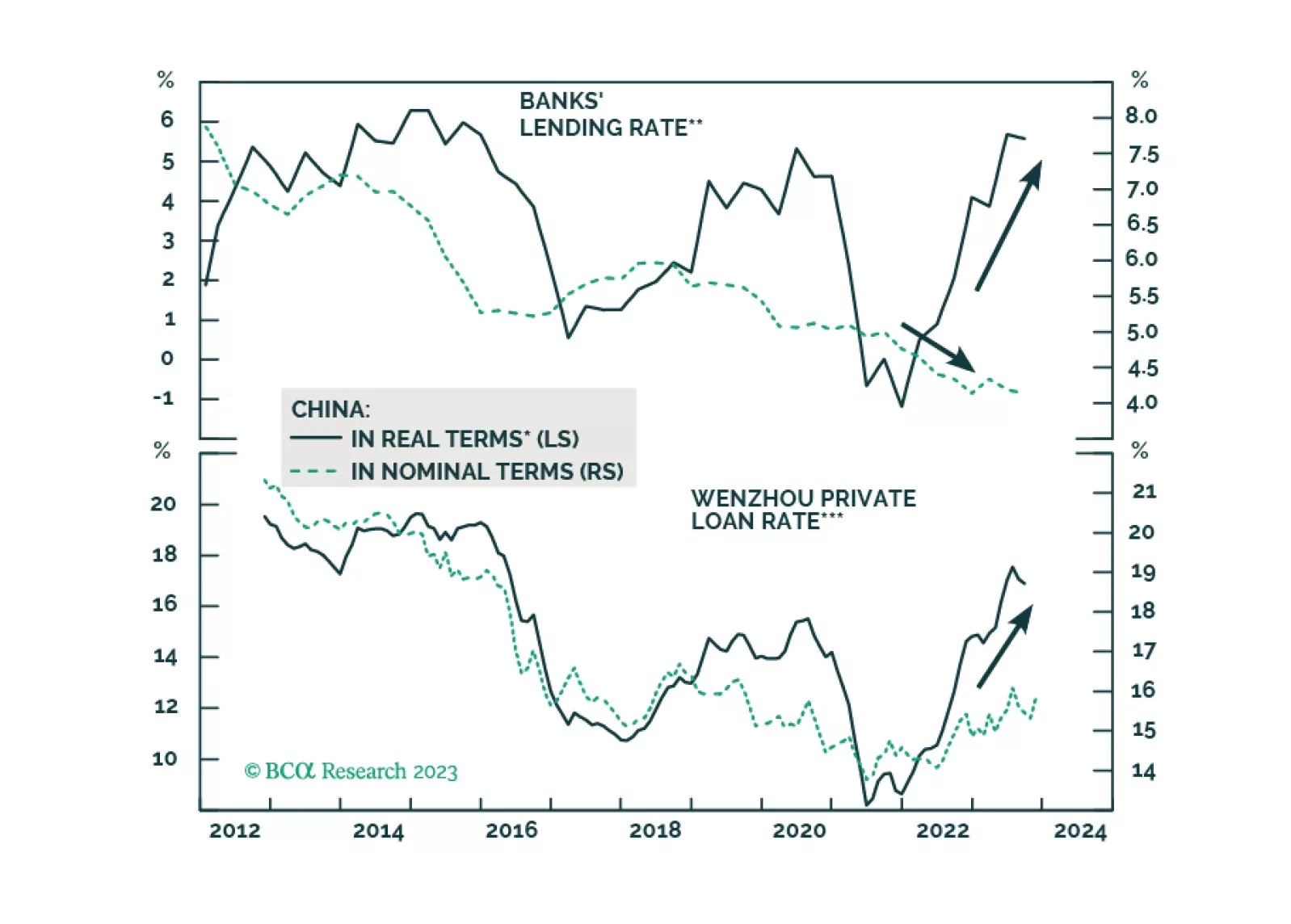

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

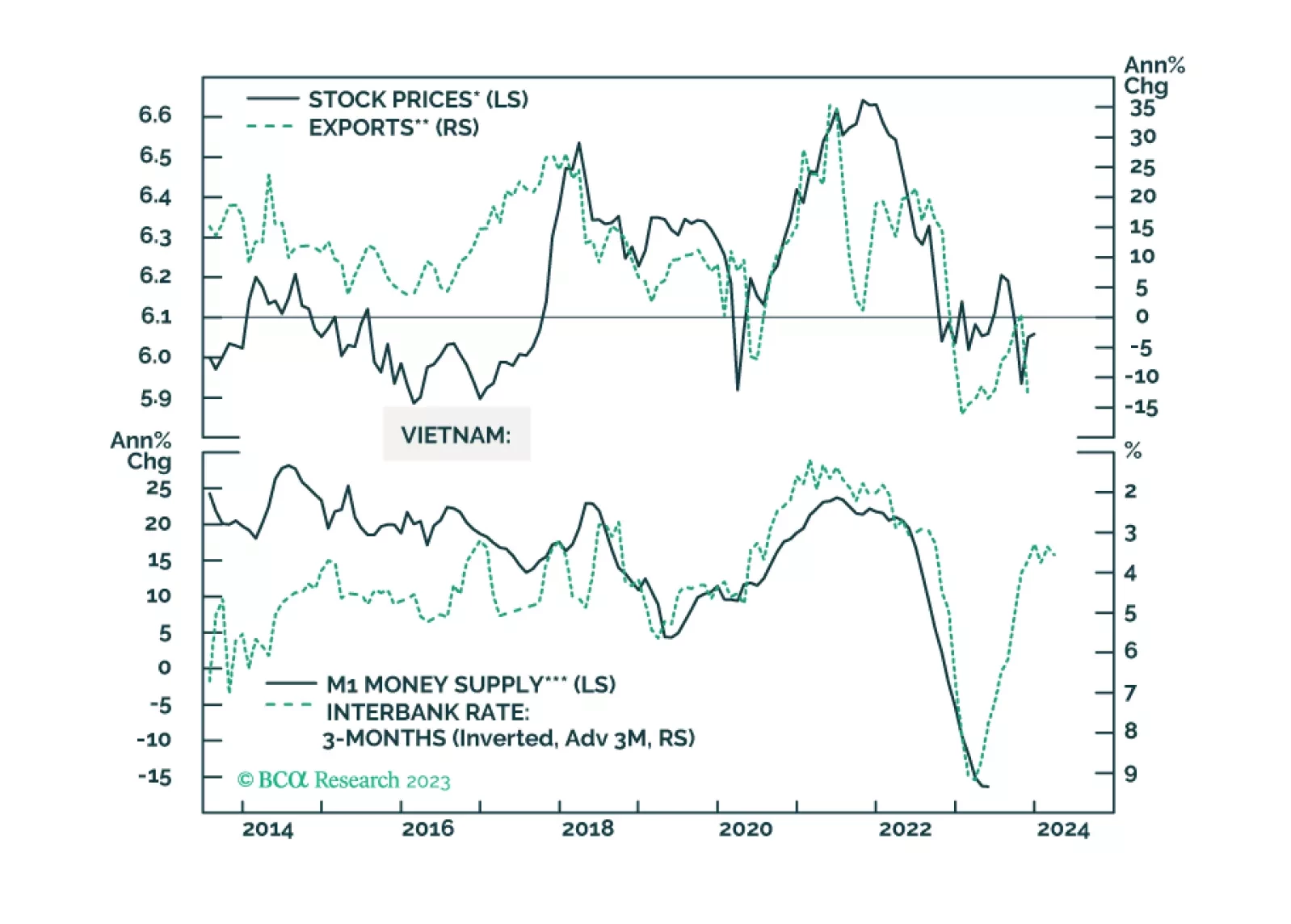

Vietnamese stocks may not see an immediate rally as global manufacturing and exports remain weak. But investors with longer-term horizons should stay overweight this market.

Explore the eight main themes that will drive the returns of European assets in 2024.

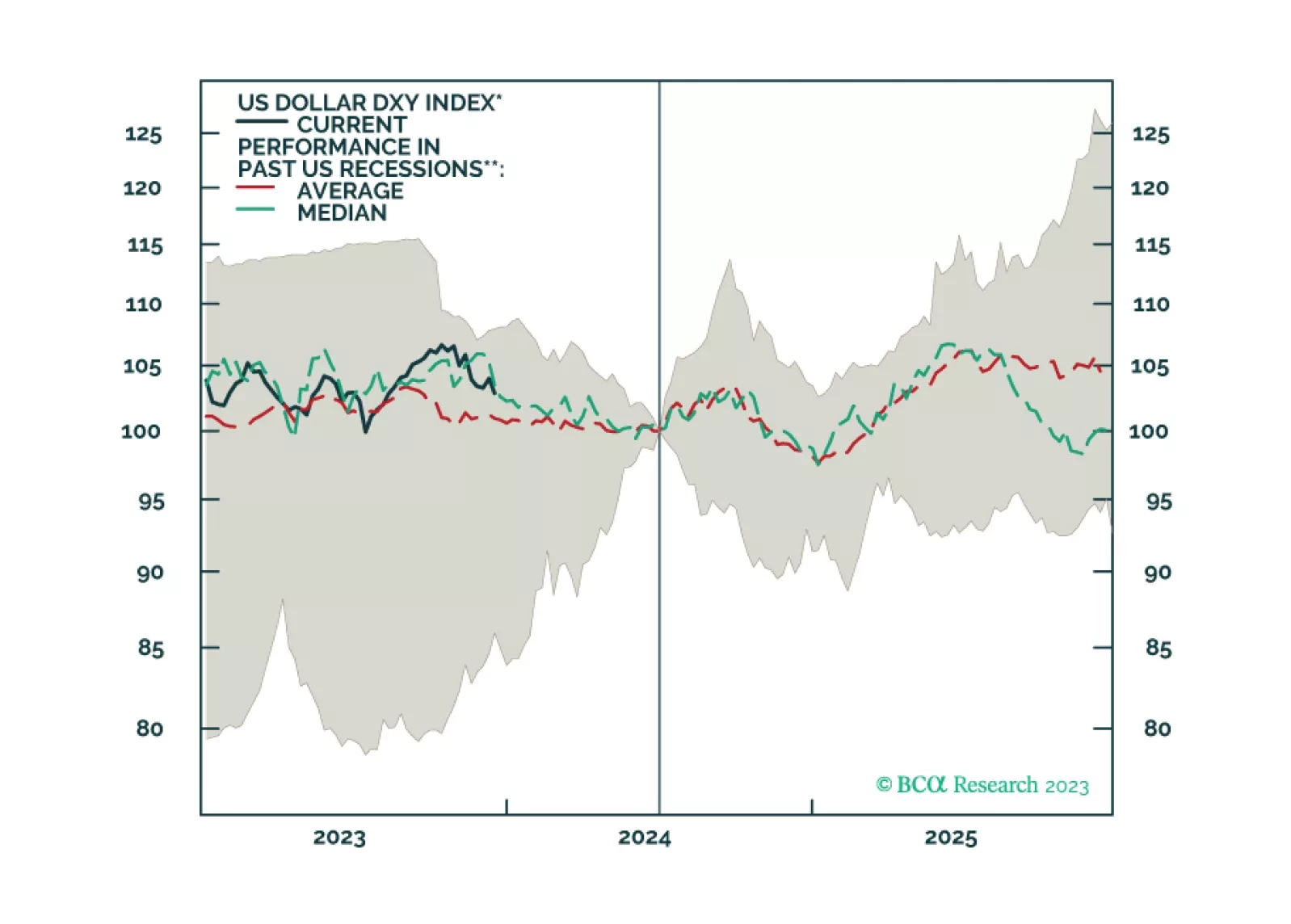

In this week’s report, we present our dollar view for 2024 and beyond, with a few trade ideas.

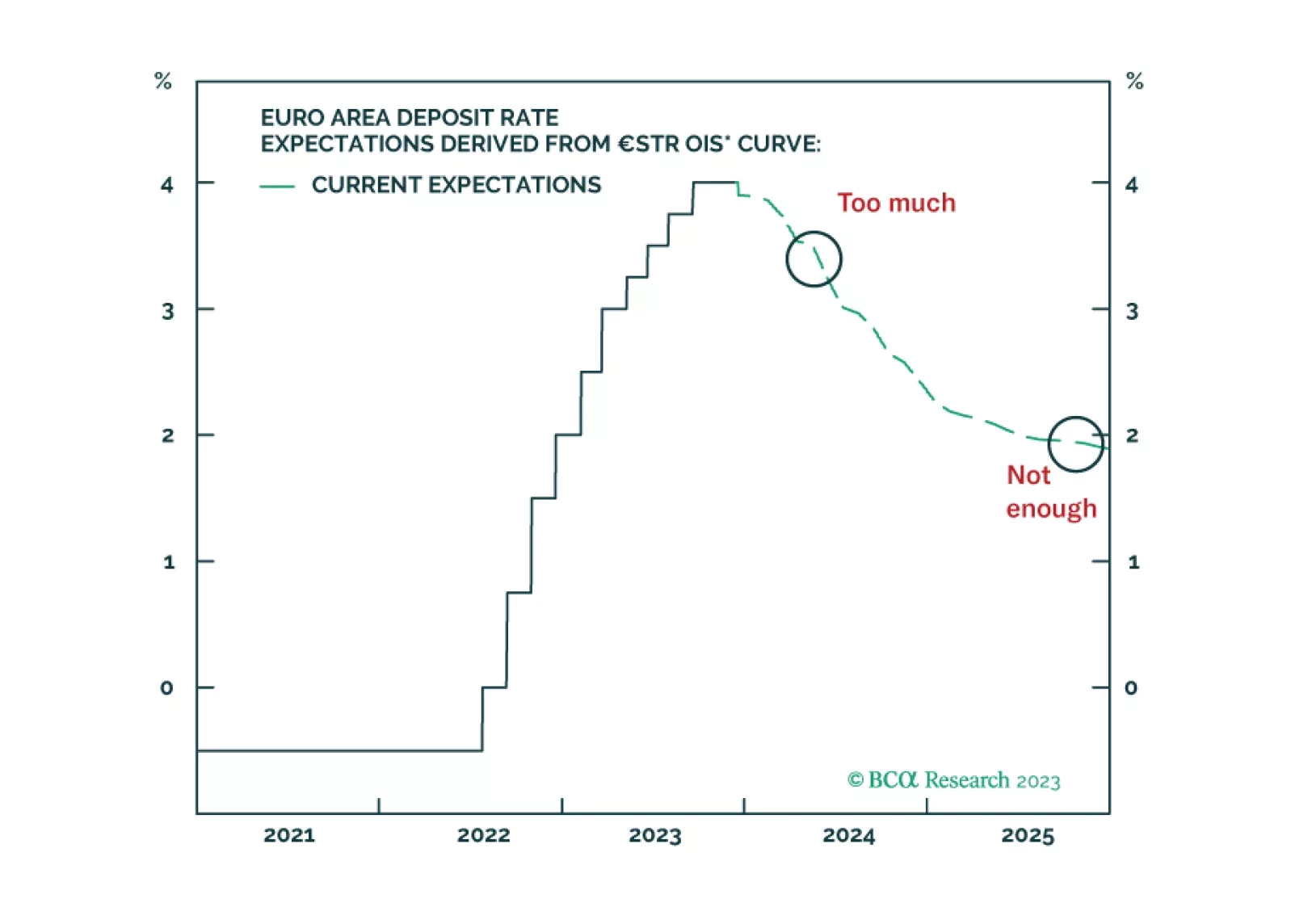

As expected, the ECB kept its policy rate unchanged on Thursday. In the updated macroeconomic projections, the central bank revised down its inflation and growth forecasts for next year. It now expects inflation to ease to 2.7% in 2024 – 0.5 percentage…

The November US retail sales release for November delivered a positive signal about consumer spending. Overall retail sales unexpectedly increased by 0.3% m/m, surprising expectations of a 0.1% m/m decline. The details of the report were also favorable. Eight…

The short answer, according to our colleagues at BCA’s Commodity & Energy Strategy (CES) is straightforward, but not simple: Political economy – i.e., how states organize and operate their economies to support policy and advance their interests. …