Business Cycles

US Treasury yields fell sharply following yesterday’s soft October CPI report, and investors have now officially priced out all remaining rate hikes from the yield curve. In fact, the fed funds futures curve is priced for a 25 basis point rate cut by next…

To the extent that US small businesses are typically more exposed to domestic economic conditions than larger firms, results of the NFIB Small Business Economic Trends survey are instructive. One important trend is that the October survey results…

The ZEW survey of investor sentiment continues to send an optimistic signal. German sentiment jumped from -1.1 to +9.8 in November – its highest level since March and beating expectations of a smaller improvement to 5.0. Similarly, expectations for the Euro…

The DXY collapsed to a 2 ½ month low on Tuesday following the softer than anticipated CPI inflation release which prompted investors to bring forward their Fed rate cut expectations (see The Numbers). This marks an acceleration of a budding downtrend since…

BCA Research’s Global Fixed Income Strategy service remains long 10-year German bunds vs short 10-year Japanese government bonds (JGBs) as a tactical trade. This trade mirrors the team's two highest conviction strategic views in government bond space,…

China's money and credit data remained weak in October. New total social financing amounted to RMB 1.85 trillion – less than the RMB 1.95 trillion anticipated and below the prior month's increase of RMB 4.12 trillion. Similarly, loans extended by banks fell…

Agriculture commodity prices have been on a steady decline for over a year. Since peaking in mid-May 2022, the GSCI Agriculture index has dropped by 34% -- nearly half of which occurred in 2023. The weakness is generally broad-based. Corn prices are down 32%,…

Our equally weighted global cyclical equity index has outperformed equally weighted defensives for most of this year. By October 17, this outperformance stood at about 12.6%. This outperformance is consistent with US Treasury market dynamics. The relative…

BCA Research's Global Investment Strategy service assigns 25% odds of the recession starting in 2025 or later. Our colleagues continue to think that the US will succumb to a recession in 2024, probably in the second half of the year. They see the…

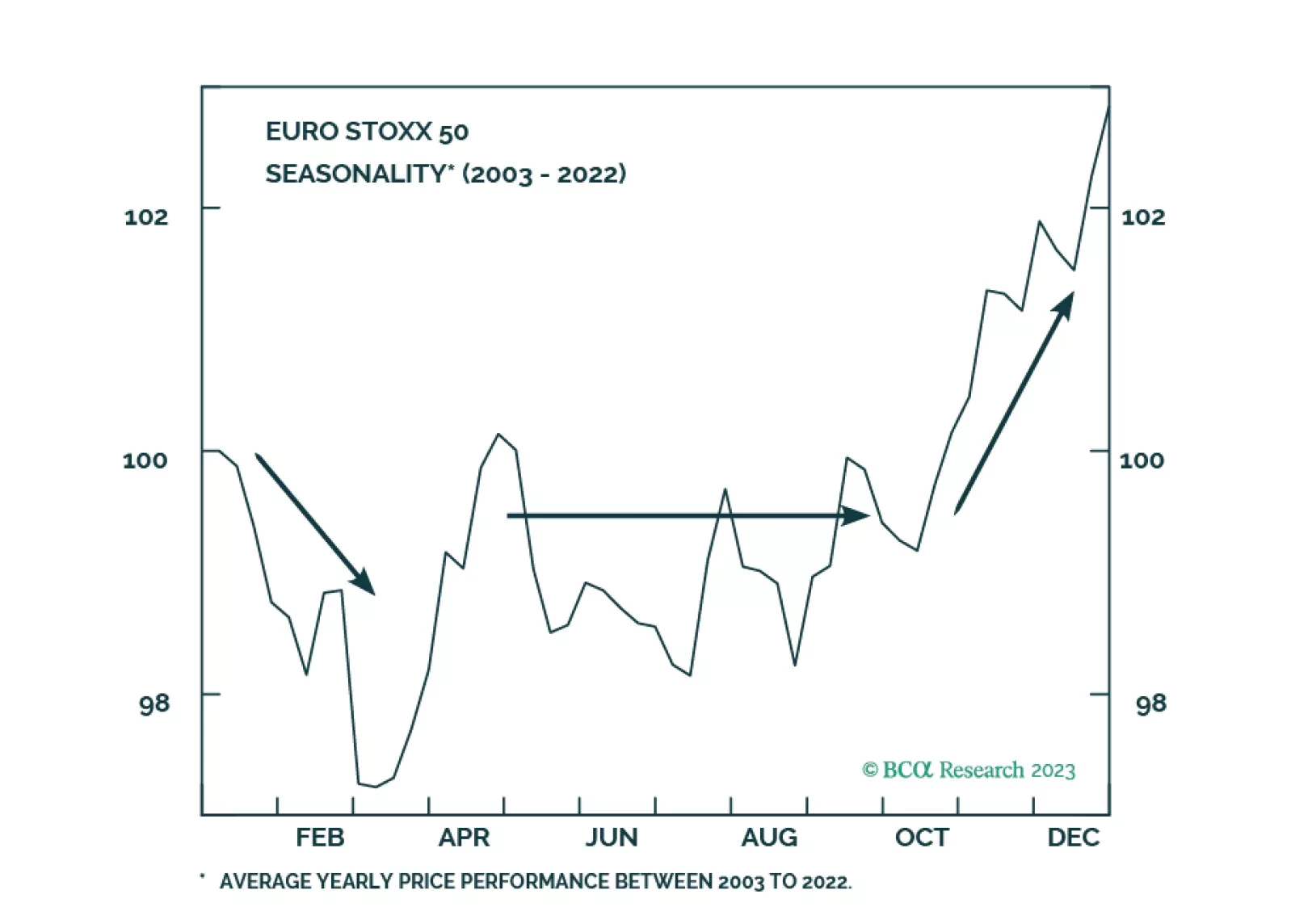

European markets have room to rebound in the coming weeks, however, a recession looms. What are the lessons from history that investors can use to position themselves under these conditions?