Business Cycles

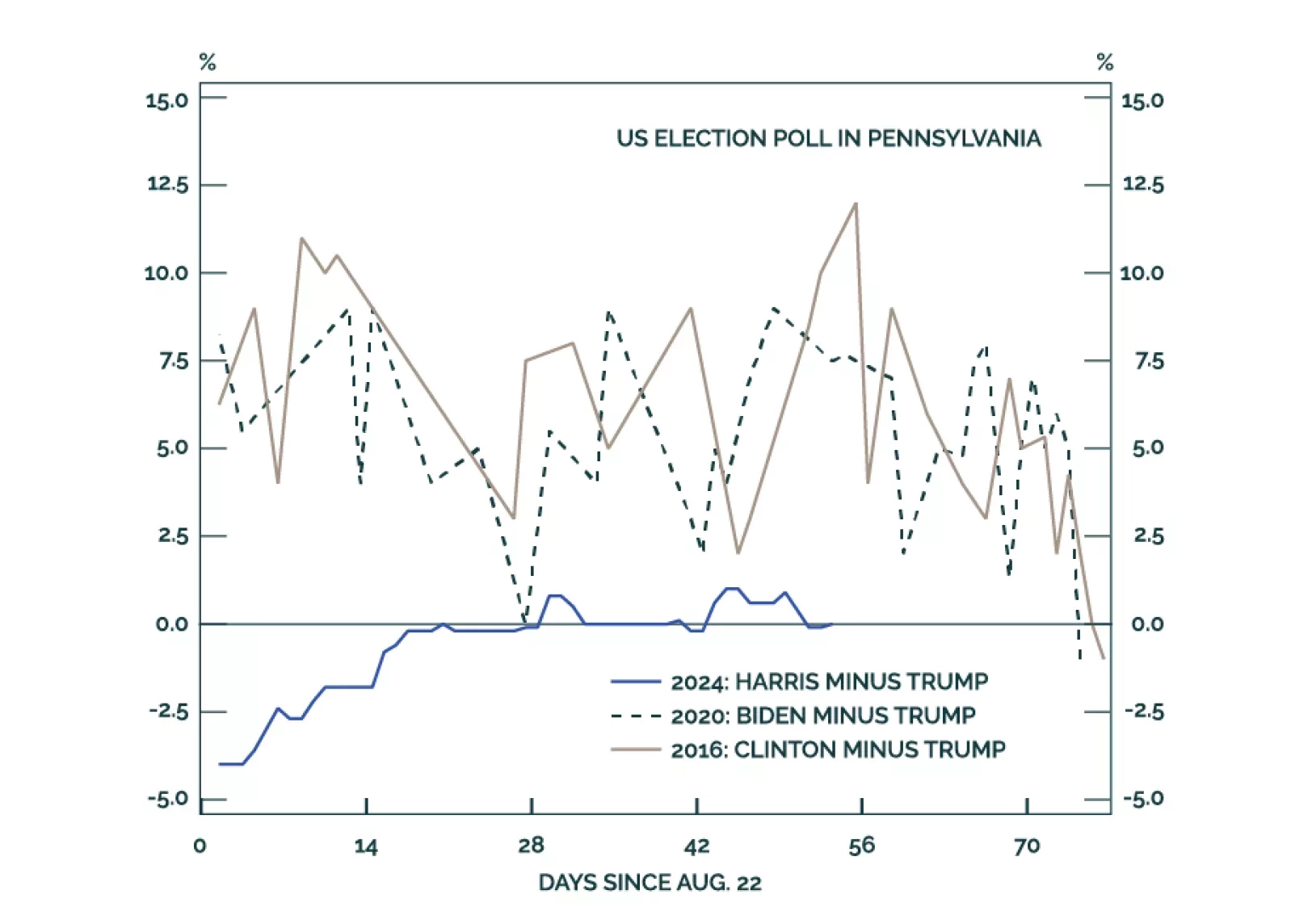

The month of October ahead of a US general election tends to be a volatile month with negative outcome for equities. As such, it is prudent to remain on the sidelines until after the election.

The US election underscores three long-term trends of Generational Change, Peak Polarization, and Limited Big Government. Investors should expect more volatility around the election and should assess the results before adding more risk. While we predicted the October surprise from the Middle East, more surprises are coming before the final vote is cast.

October seasonality tends to be negative for stocks in an election year. That is the only thing that has stayed our hand from shifting out of our tactical underweight on US equities, initiated – poorly – in July.

But the big macro news from September has not been bearish. The Fed has signaled jumbo cuts. Within seven weeks, the US central bank intends to cut by 100bps! Meanwhile, China appears to have reached a “policy bottom,” with its September 26 Politburo meeting signaling an extraordinary rhetorical shift towards fiscal policy. As such, we are starting to sniff out global reflation, akin to the 2015-2016 mid-cycle slowdown.

The labor market data still worries us. It is clearly deteriorating, on paper. Is it because of an imminent recession or “normalization?” It is difficult to say. We are open minded.

Finally, the Middle East tensions are again on the horizon. If Iran stays its hand against Saudi energy facilities – which we expect it to continue to do – the Iran-Israel conflict is a sideshow. Nonetheless, with global reflation afoot, we went long oil last week, on September 26. As such, geopolitics is a neat tailwind to that call.

The market got excited by the 50 bps Fed cut and China stimulus. But these are a recognition that economies are slowing significantly. Stocks often rally after the first Fed cut, before falling sharply. Investors should stay defensive.