Business Cycles

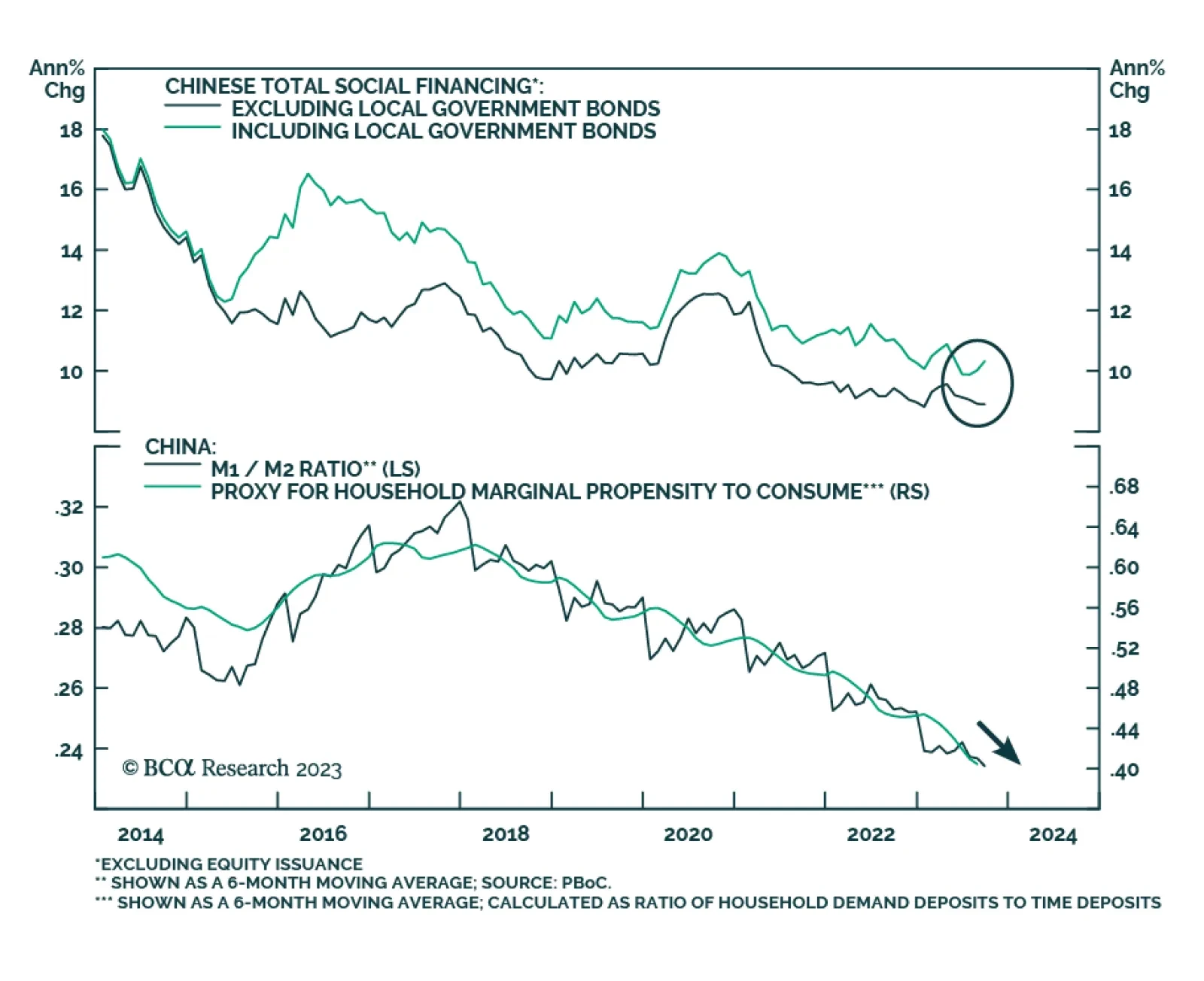

On the surface, Chinese credit data sent a positive signal about the domestic economy. Chinese aggregate social financing totaled CNY 4.1 trillion in September – exceeding both August’s CNY 3.1 trillion and expectations of CNY 3.7 trillion. However,…

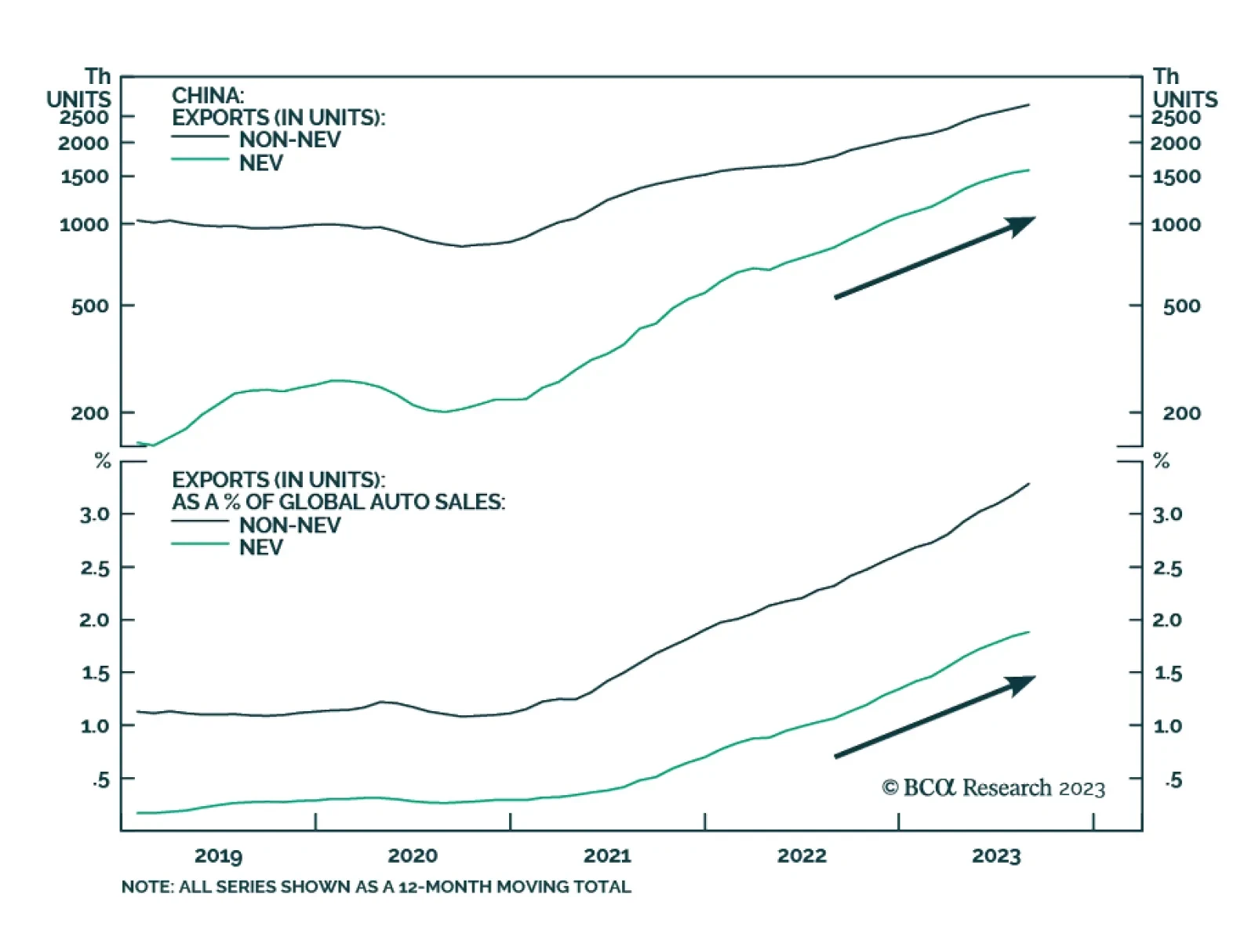

On the surface, the slower pace of contraction in Chinese exports in September is a positive signal for global trade. The 6.2% y/y drop in the dollar value of Chinese exports was not as bad as the 8% y/y decline anticipated or the 8.8% y/y decline in August. …

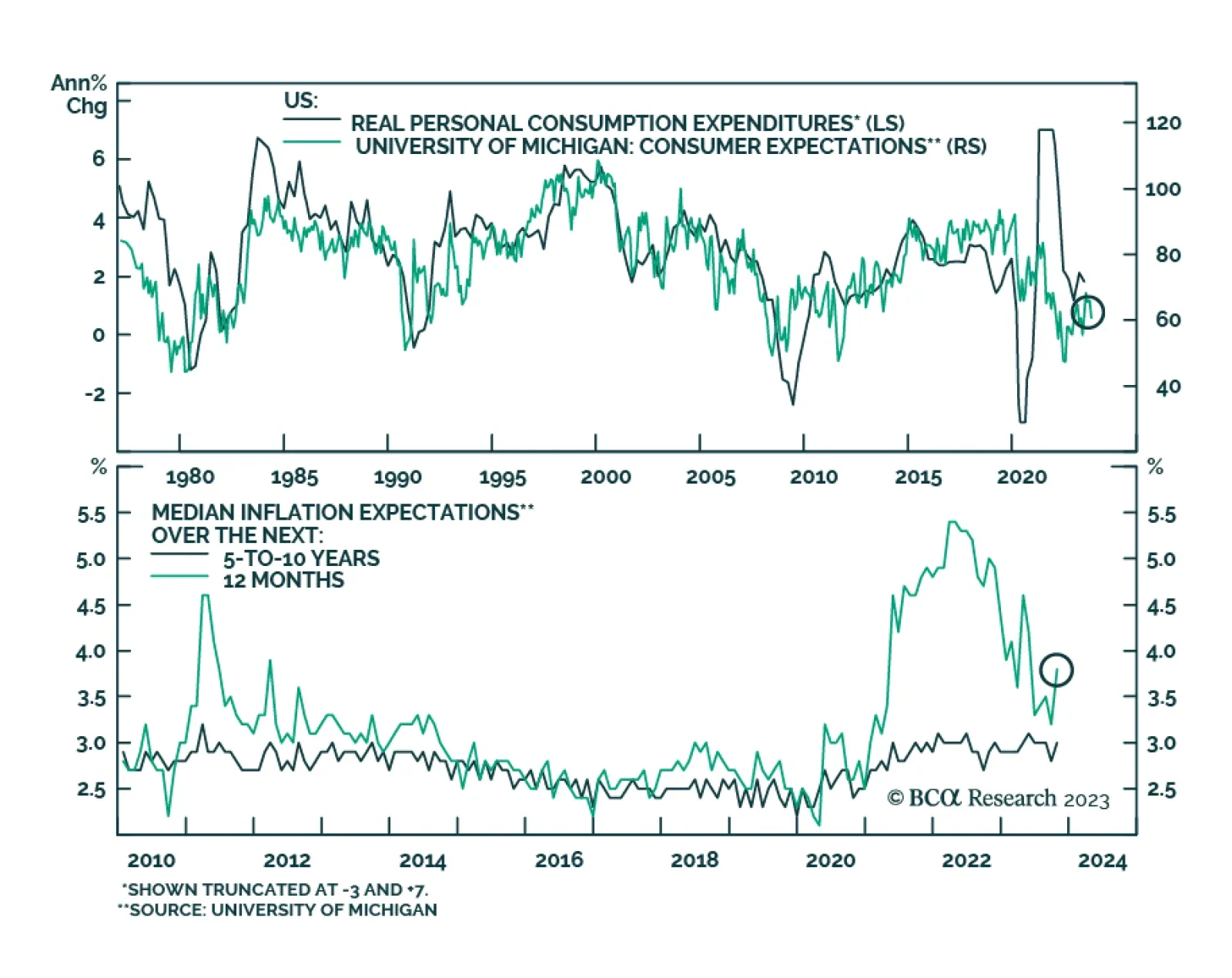

The preliminary release of the University of Michigan’s Consumer Sentiment survey delivered a negative surprise on Friday. A bigger-than-anticipated drop pushed the headline sentiment index down to a five-month low of 63. Weaker-than-expected assessments of…

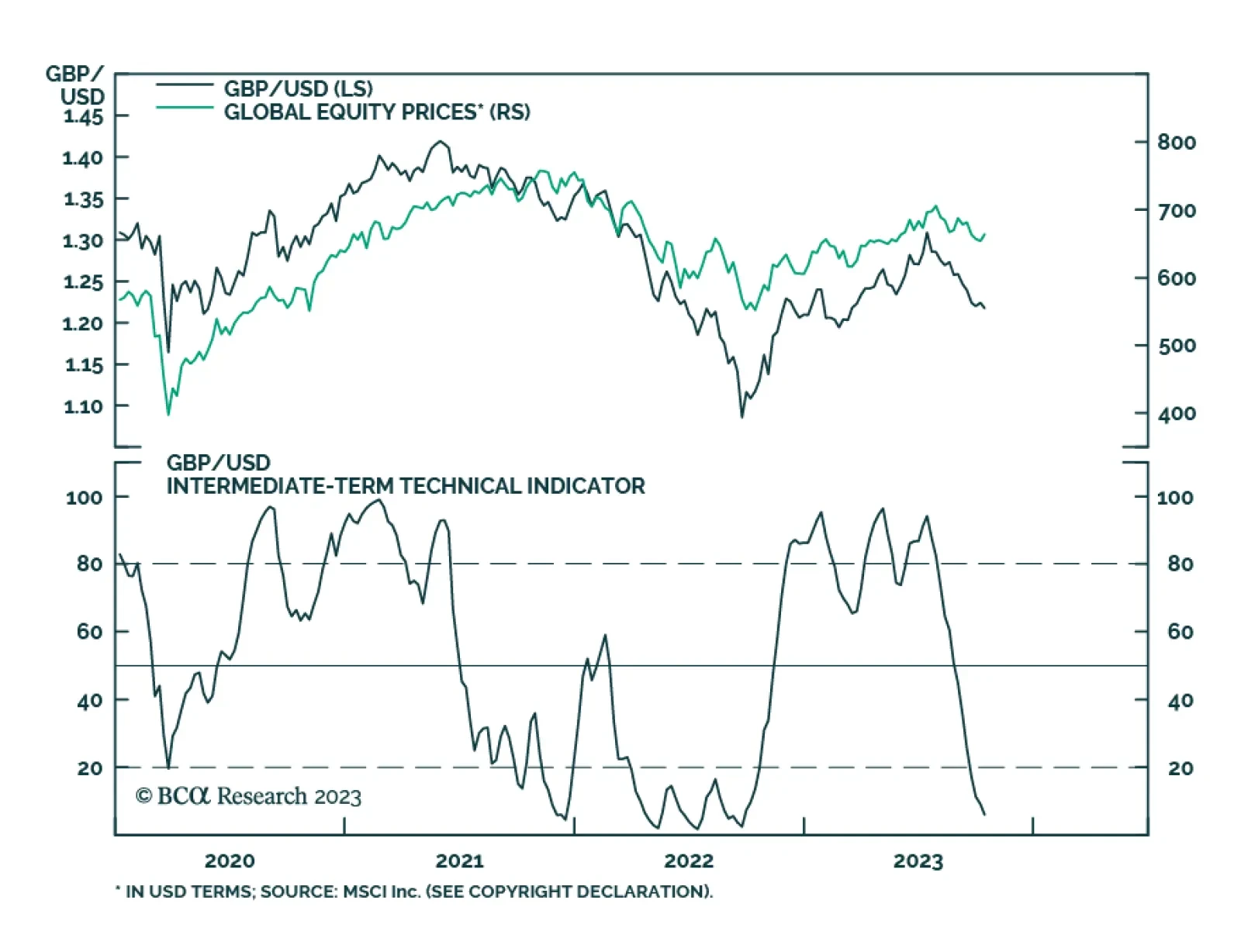

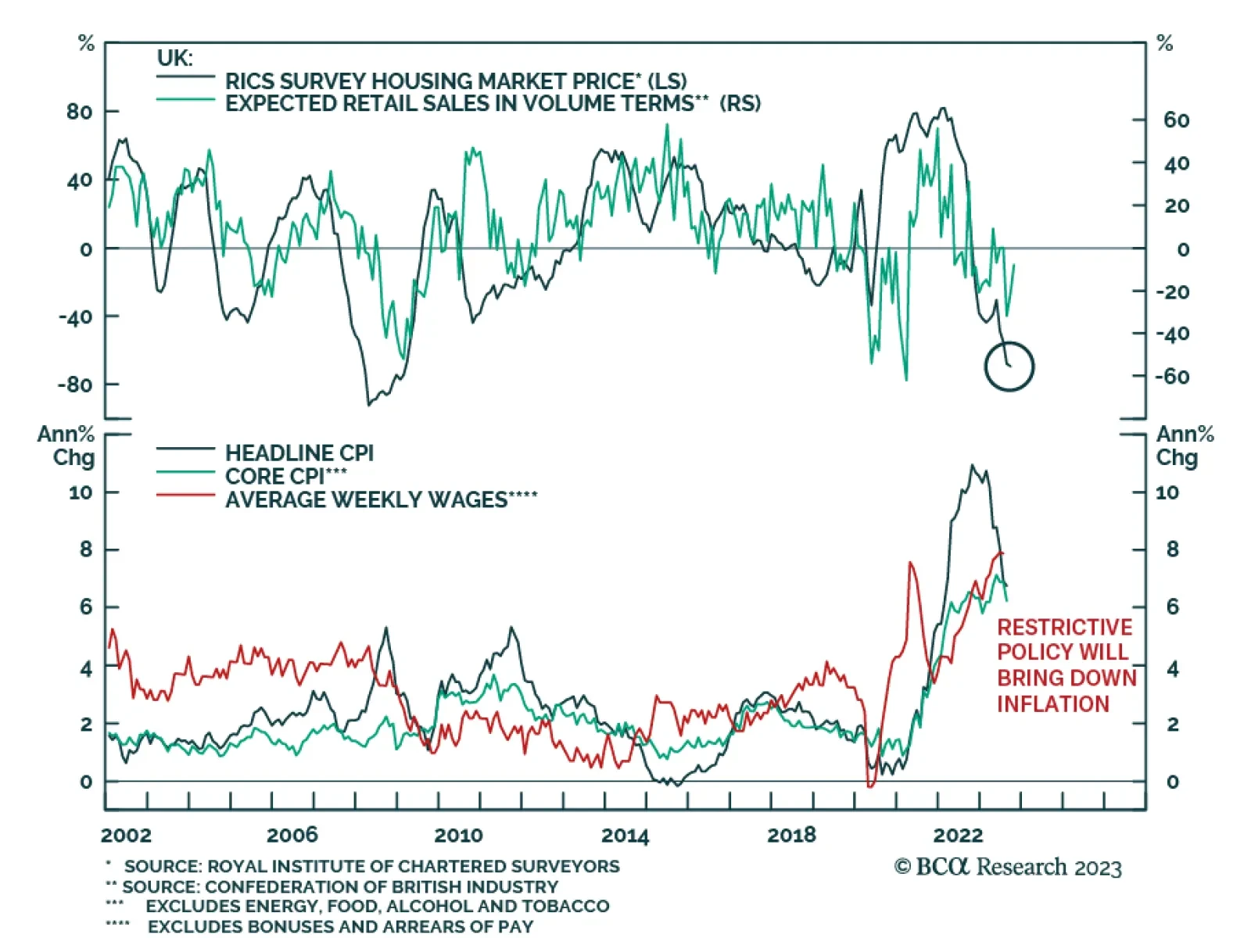

Back in May, our foreign exchange team suggested the risk to sterling was to the downside. Indeed, GBP/USD is down 8% from its recent peak. While dollar strength largely explains this move in GBP/USD, there have been other fundamental factors at play. The…

This week's Insight gauges the potential of a dollar breakout or breakdown and suggests a few trade ideas.

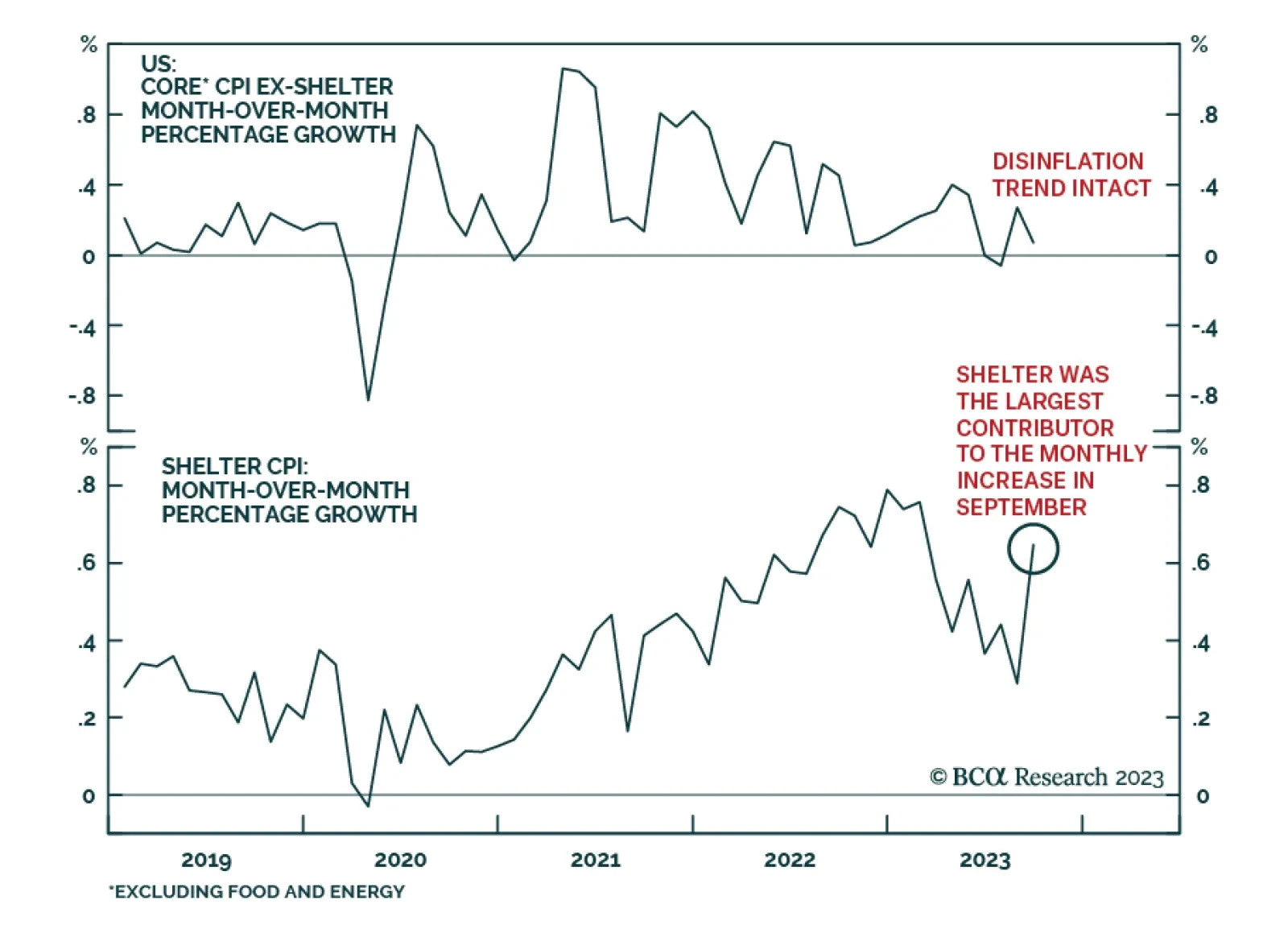

The US CPI report shows inflation was higher than anticipated in September. Although the headline index decelerated from 0.6% m/m to 0.4% m/m, it is above expectations of 0.3% m/m. The annual rate of change remains at 3.7% y/y – also above consensus estimates…

As expected, the UK economy bounced back in August with GDP expanding by 0.2% m/m following a 0.6% m/m decline in July. Yet to the extent that this improvement largely reflects a rebound after strikes weighed down on activity in the prior month, the growth…

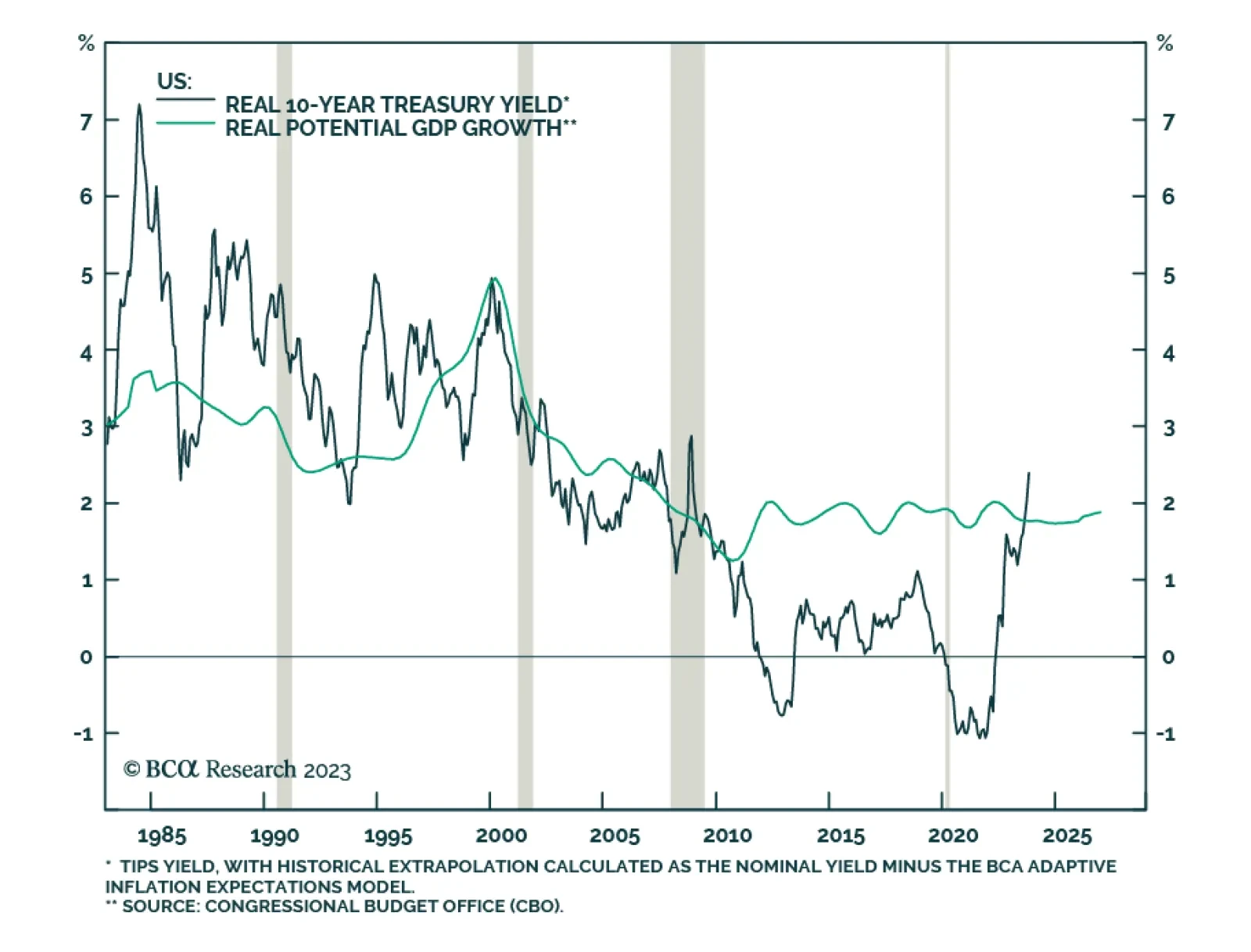

The last few weeks saw a repricing of nominal yields to levels not breached since before the Great Financial Crisis. Breaking down the US 10-year Treasury yield into real and inflation expectations components reveals the selloff was mostly driven by the…

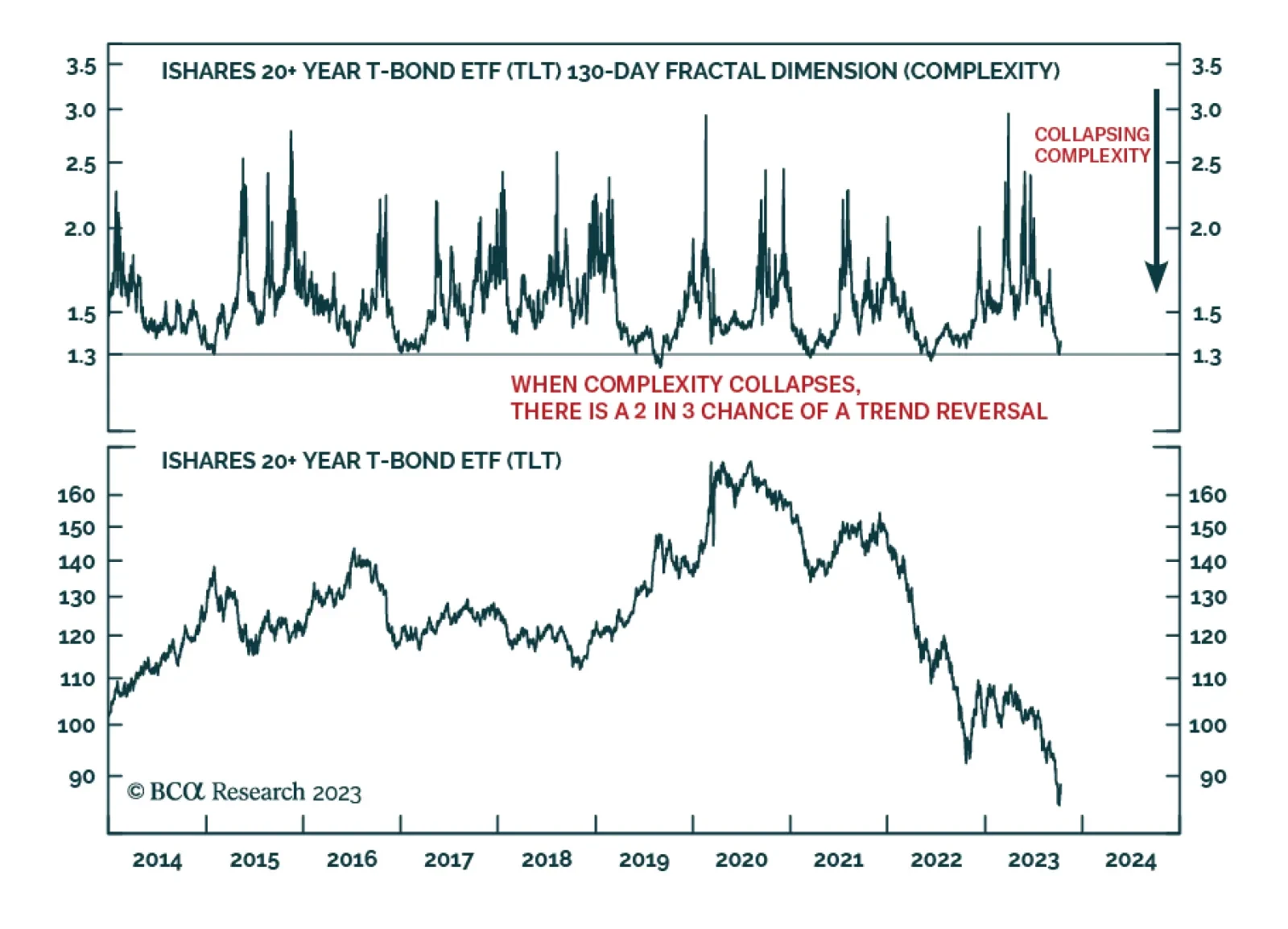

According to BCA Research’s Counterpoint service, the sharp sell-off in long duration bonds (ticker TLT) has reached the collapsed 130-day complexity that has preceded several turning-points in the last few years. This suggests a two-thirds probability of a…

US monetary policy is restrictive, as evidenced by a falling jobs-workers gap. The reason that unemployment has not risen is because labor demand still exceeds supply. That will change in the second half of 2024 when the US economy succumbs to recession. Investors should increasingly favor bonds over stocks.