Business Cycles

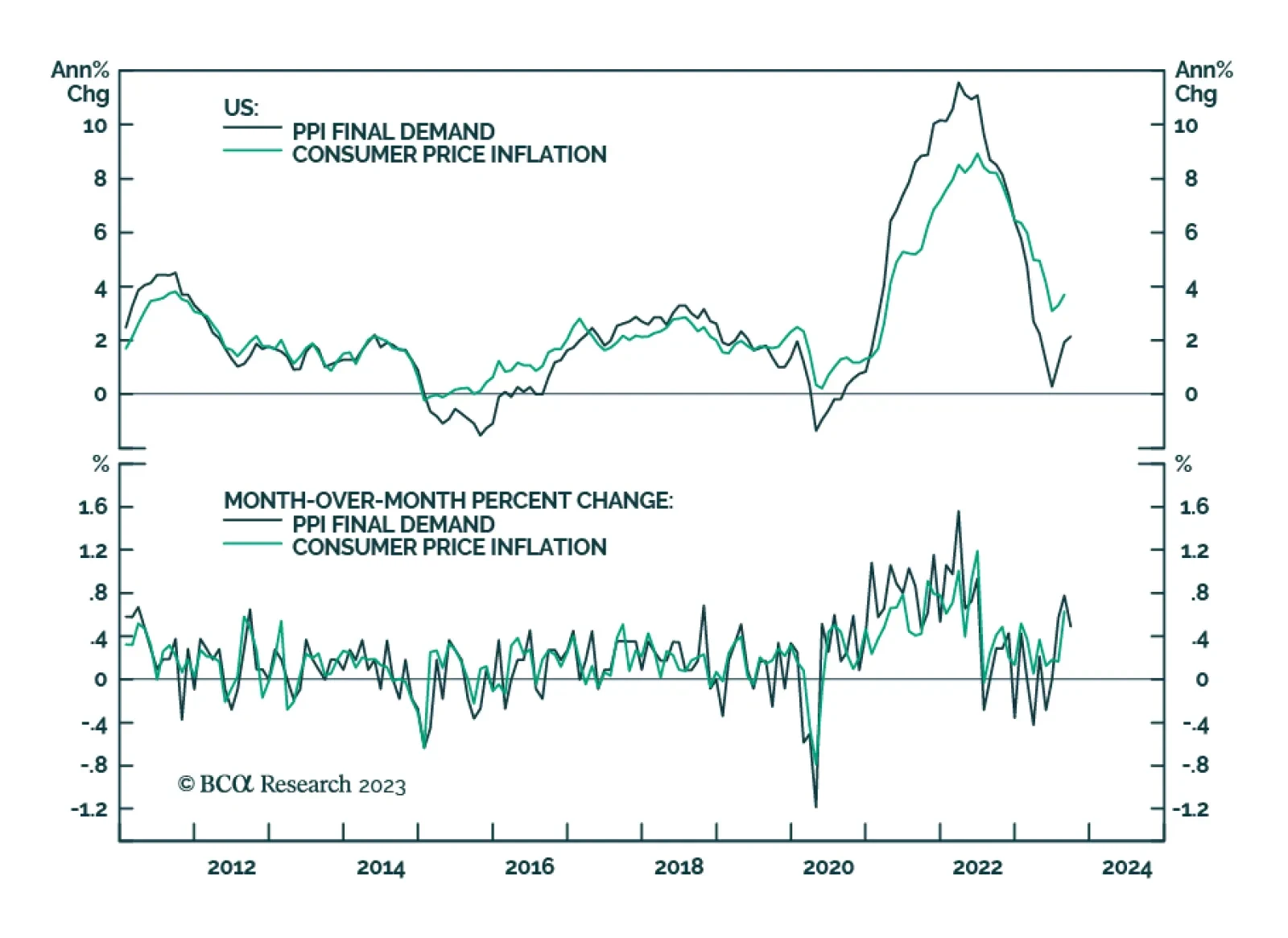

The US PPI report came in hotter-than-anticipated in September. Although the headline index decelerated from 0.7% m/m to 0.5% m/m, it remains above expectations of a more pronounced moderation to 0.3% m/m. In particular, a 3.3% m/m increase in energy prices…

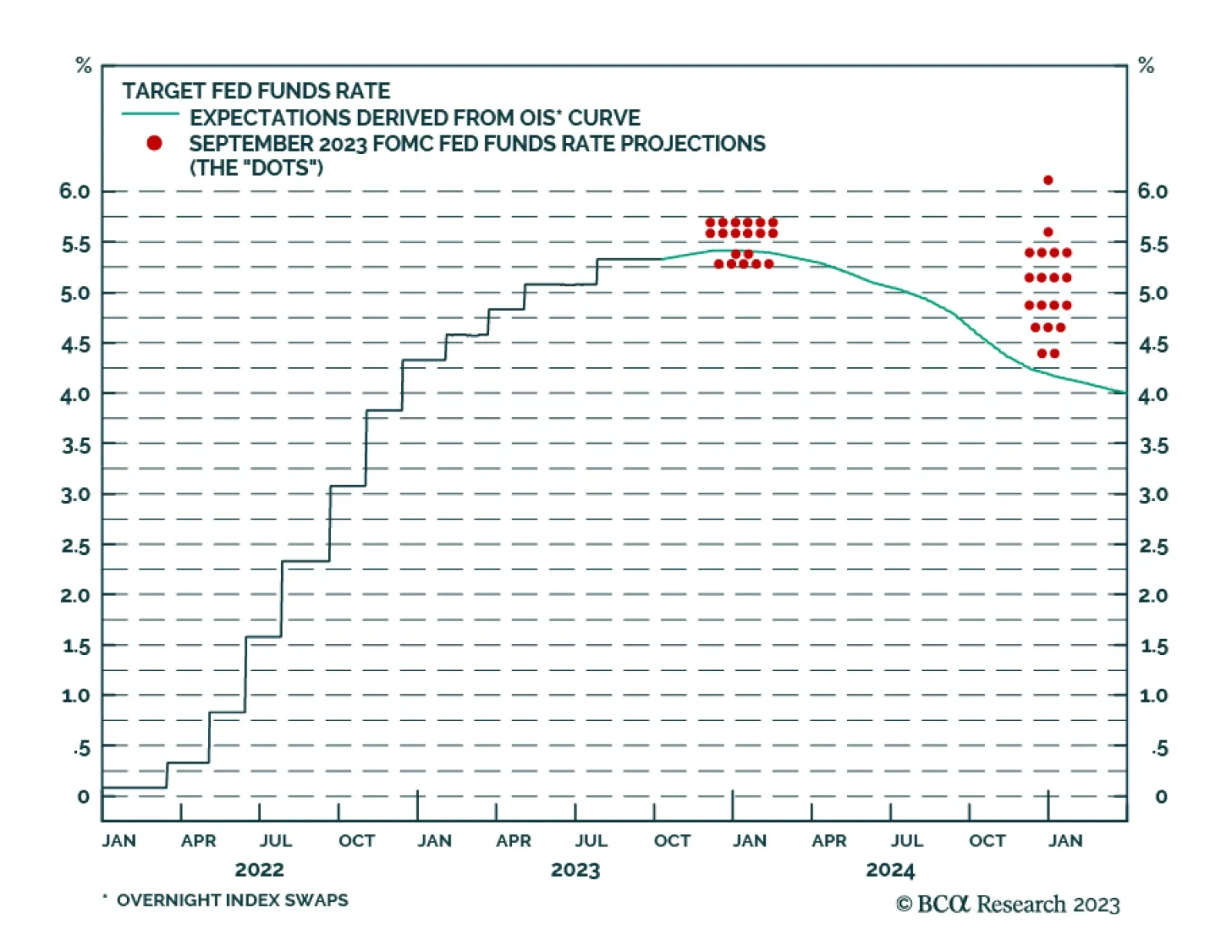

The minutes of the September FOMC meeting confirmed that the Fed intends to maintain restrictive monetary policy for longer. Although inflation has been moderating, participants continue to view it as unacceptably high and emphasized that they remain…

Taiwanese exports unexpectedly grew for the first time in just over a year in September – sending a positive signal about the global manufacturing cycle. The 3.4% y/y increase surprised anticipations of a moderation in the rate of decline from -7.3% y/y to…

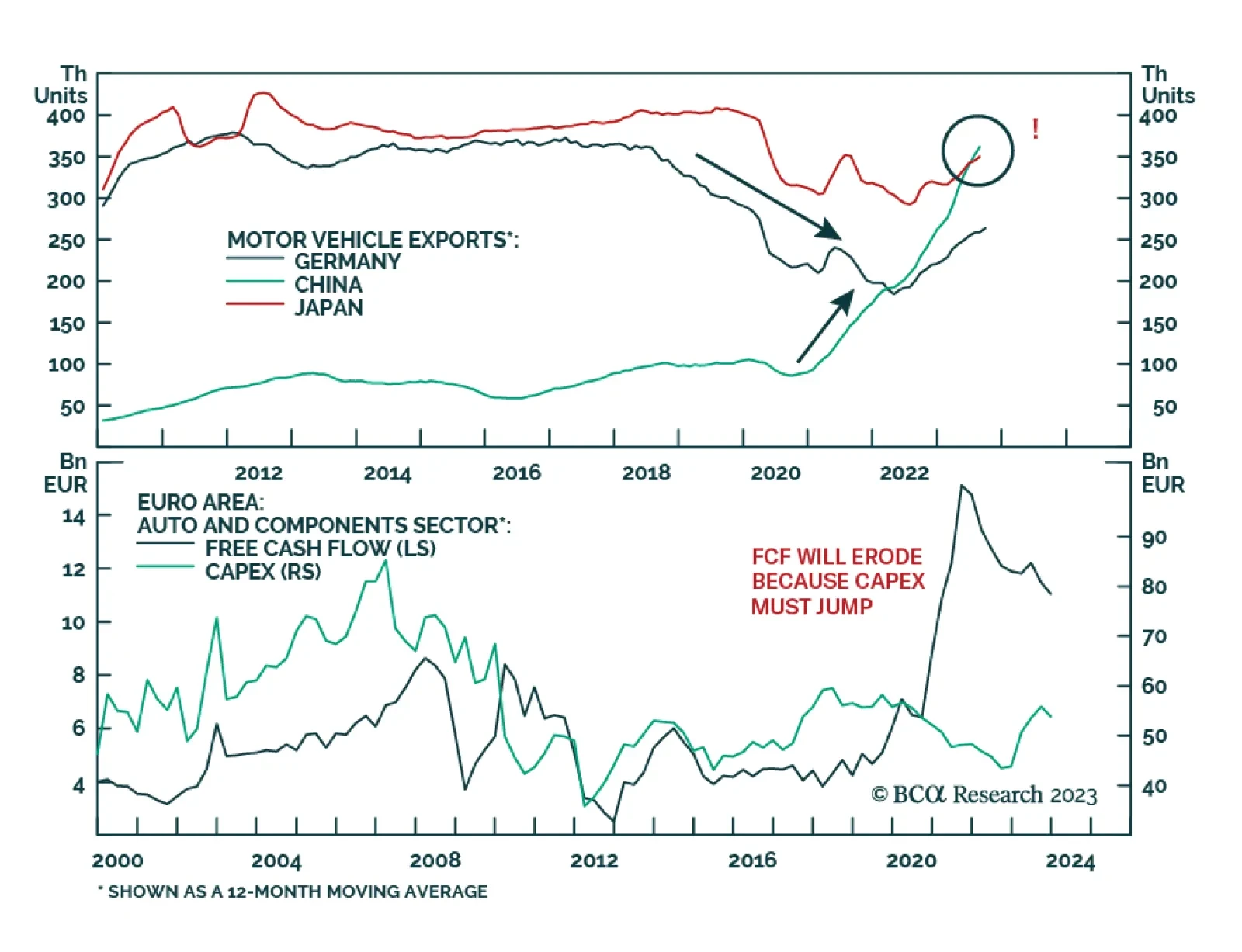

According to BCA Research’s European Investment Strategy service, European automobile and components stocks will suffer over the coming years. The European automobile and components equity sector is cheap, trading at a modest 5.4 times forward earnings or…

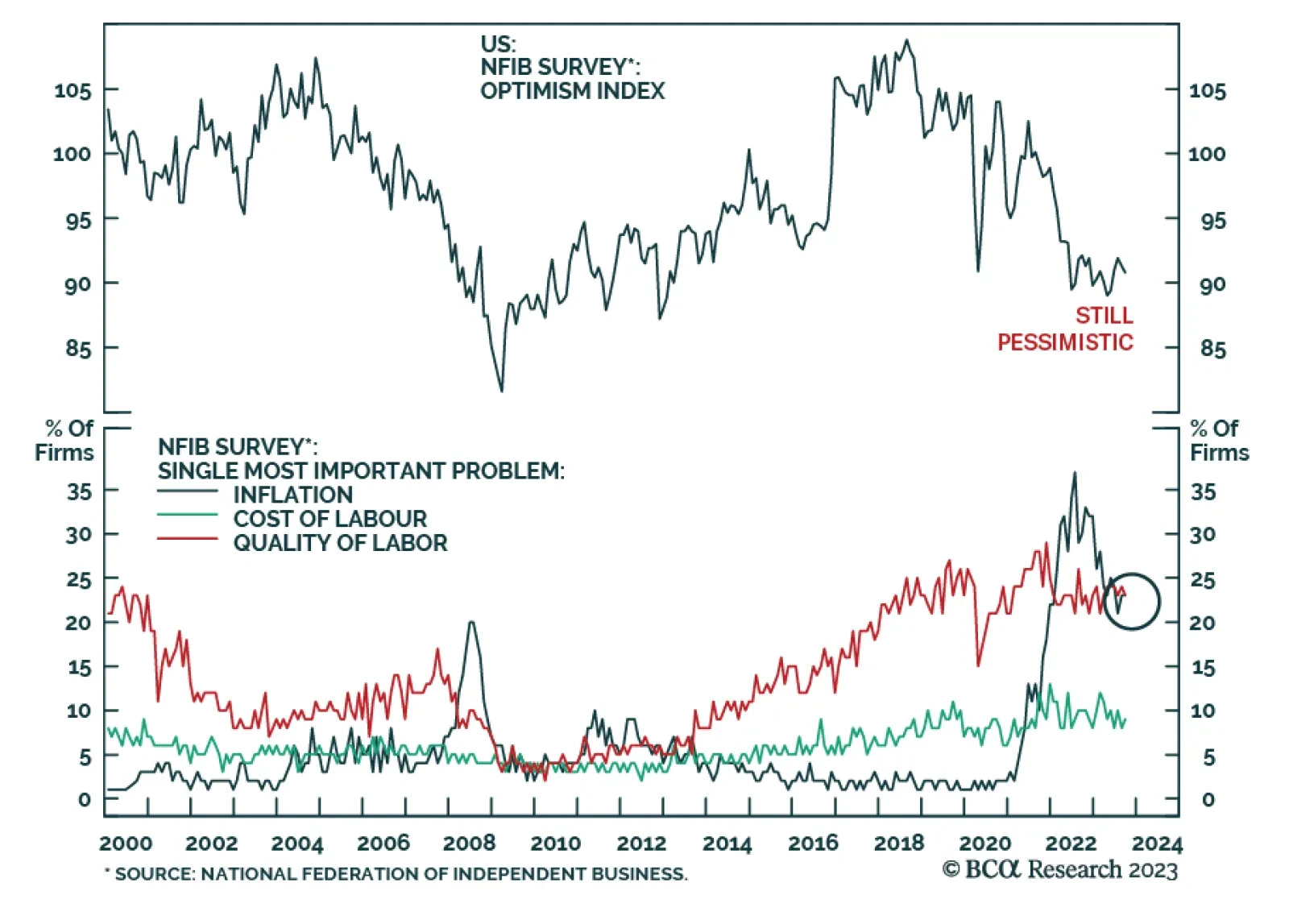

US small business optimism deteriorated for the second consecutive month in September. The NFIB index weakened by 0.5 points to 90.8, slightly below expectations of a more muted decline to 91.0. The latest move brings the index further below the 49-year…

Dovish comments by several Fed officials contributed to a Treasury rally and improvement in sentiment towards risk assets on Tuesday. Globally, rumors that Beijing is planning to unleash more stimulus supported Chinese financial assets and global China plays.…

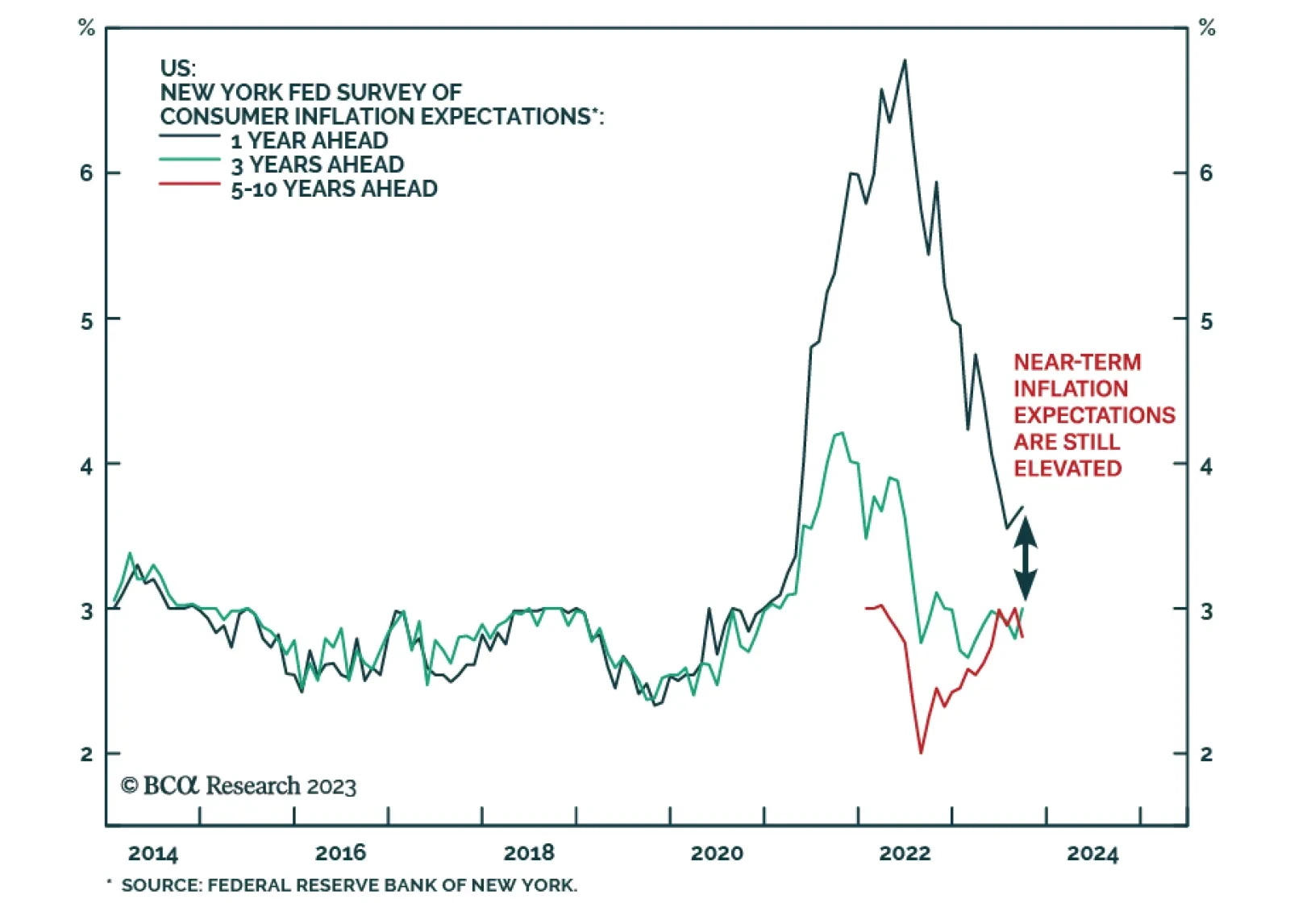

Results of the New York Fed’s survey show American consumers’ near-term inflation outlook ticked up in September. Respondents’ one-year ahead inflation expectations rose from 3.6% to 3.7%, and the three-year ahead expectations increased from 2.8% to 3.0%.…

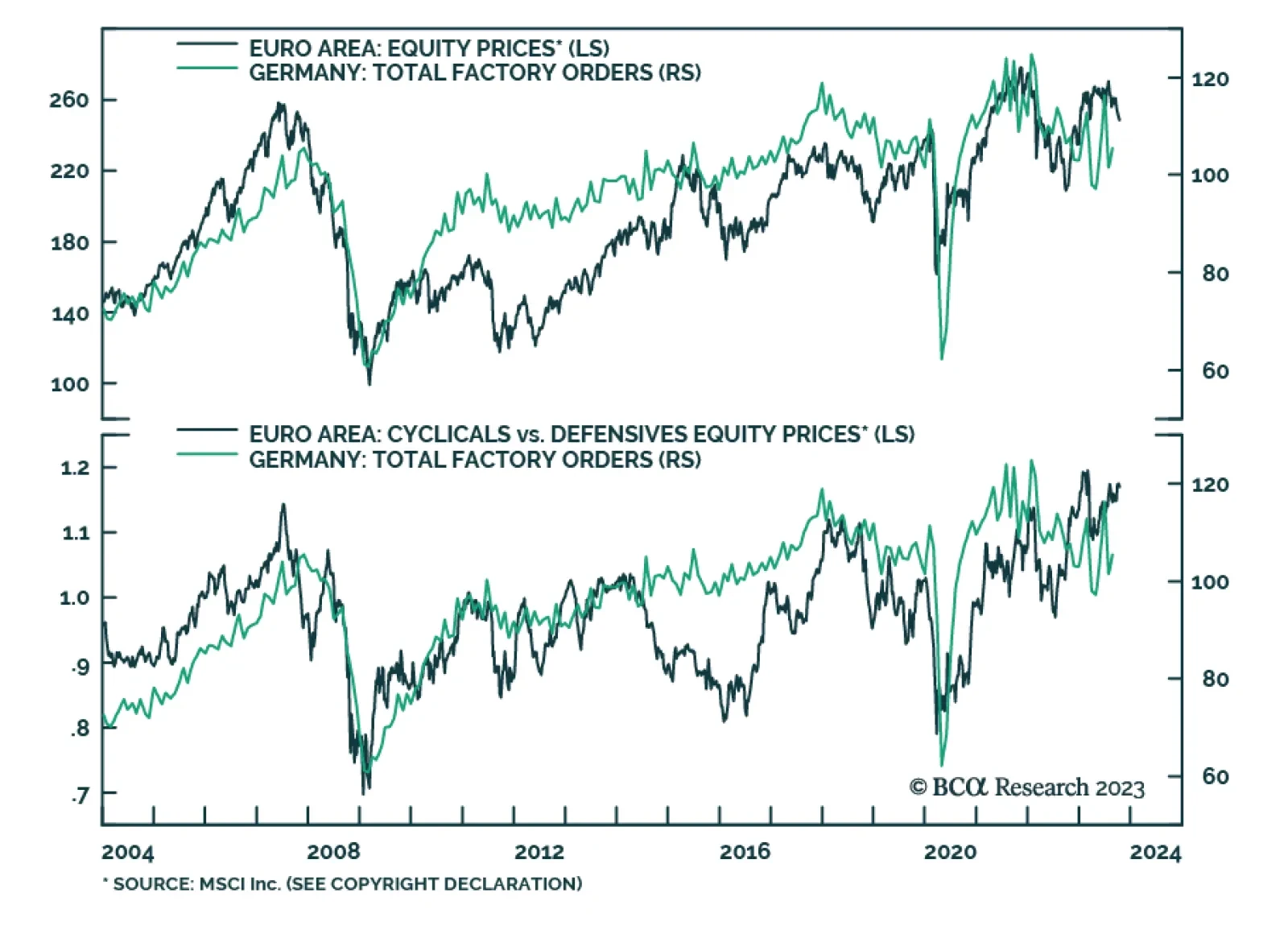

As we highlighted in a recent Insight, the stronger-than-anticipated improvement in German factory orders should be viewed with some degree of caution. Germany is the European economy most exposed to the global manufacturing sector. Several leading indicators…

The market has been held hostage by surging rates. Zombie companies are “alive” and are multiplying – they are highly sensitive to surging borrowing costs. Underweight Utilities to reduce portfolio duration. Maintain neutral positioning of Basic Materials but take a granular approach to allocations within the sector.

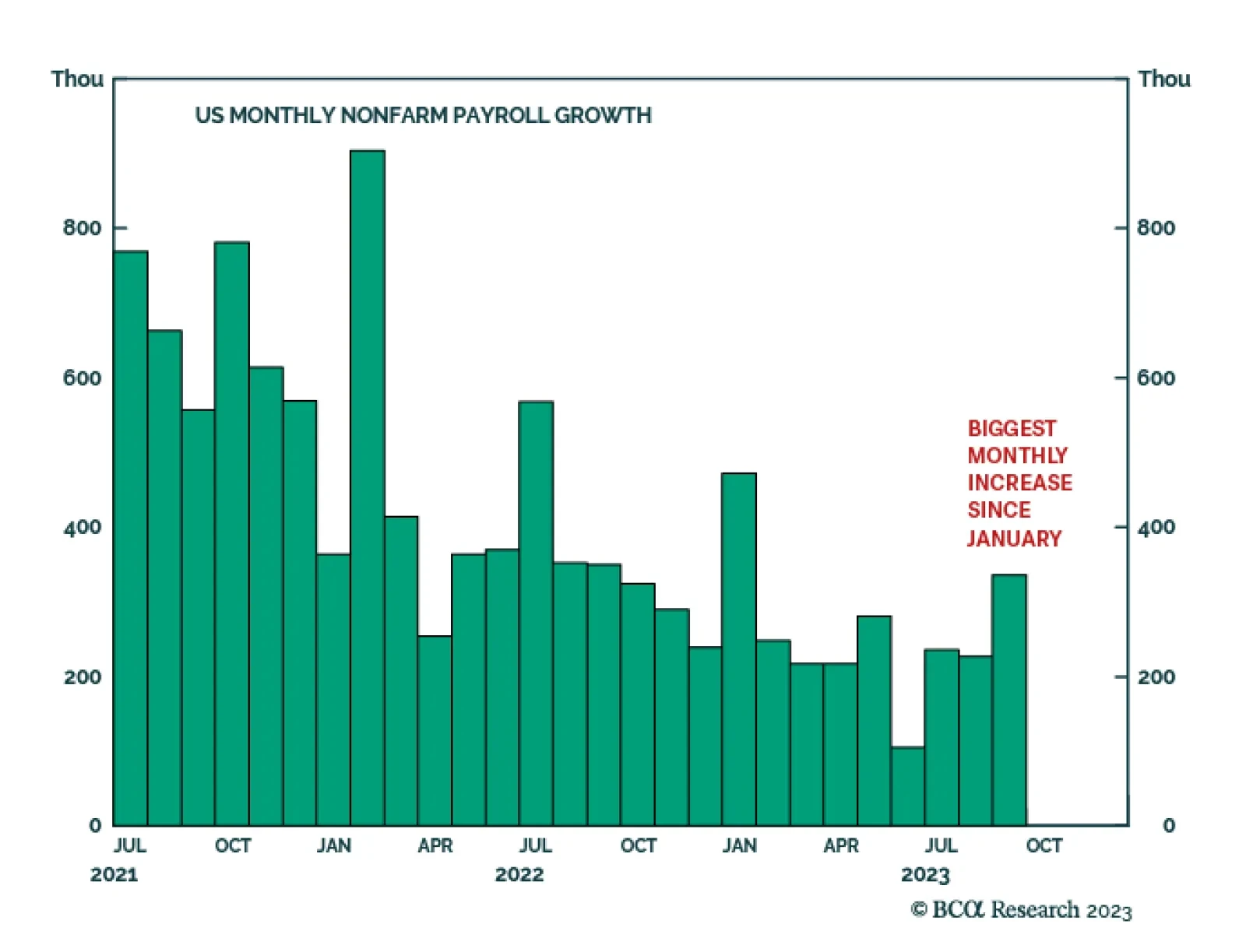

The US Nonfarm Payroll report delivered a strong positive surprise about employment growth in September. Job gains accelerated from 187 thousand to 336 thousand – significantly above expectations of a slight decline to 170 thousand. In addition, the increase…