Business Cycles

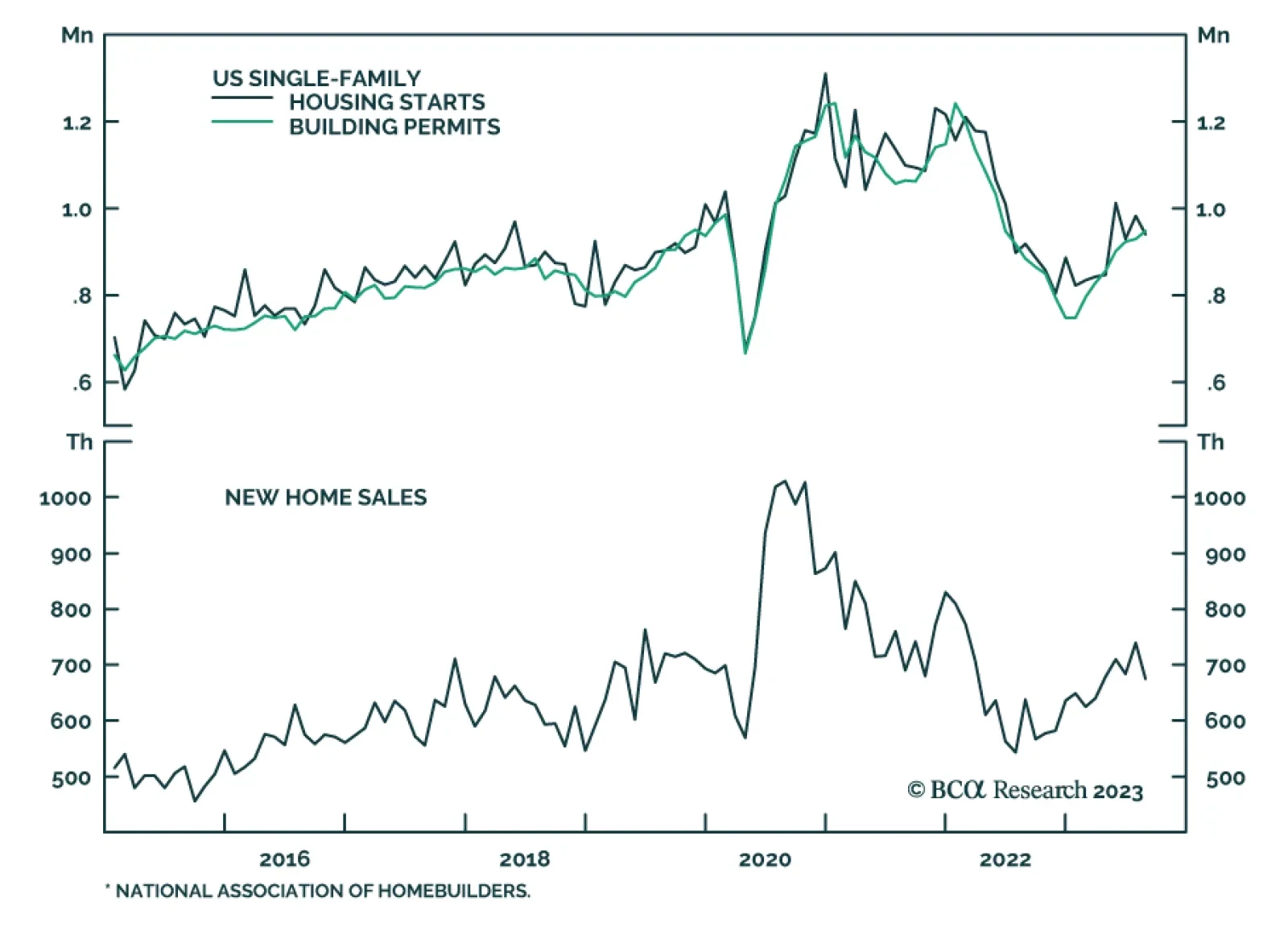

On the surface, US housing market data is sending conflicting signals. On the one hand, both the FHFA as well as the S&P CoreLogic gauges of US house prices surprised to the upside in July and are now expanding on both a month-over-month and…

The year-to-date rally in US cyclical stocks has fizzled. After climbing 29% in the first seven months of the year, cyclical equities are down 6.0% since the beginning of August. This drop is happening in the context of a general equity selloff. However, the…

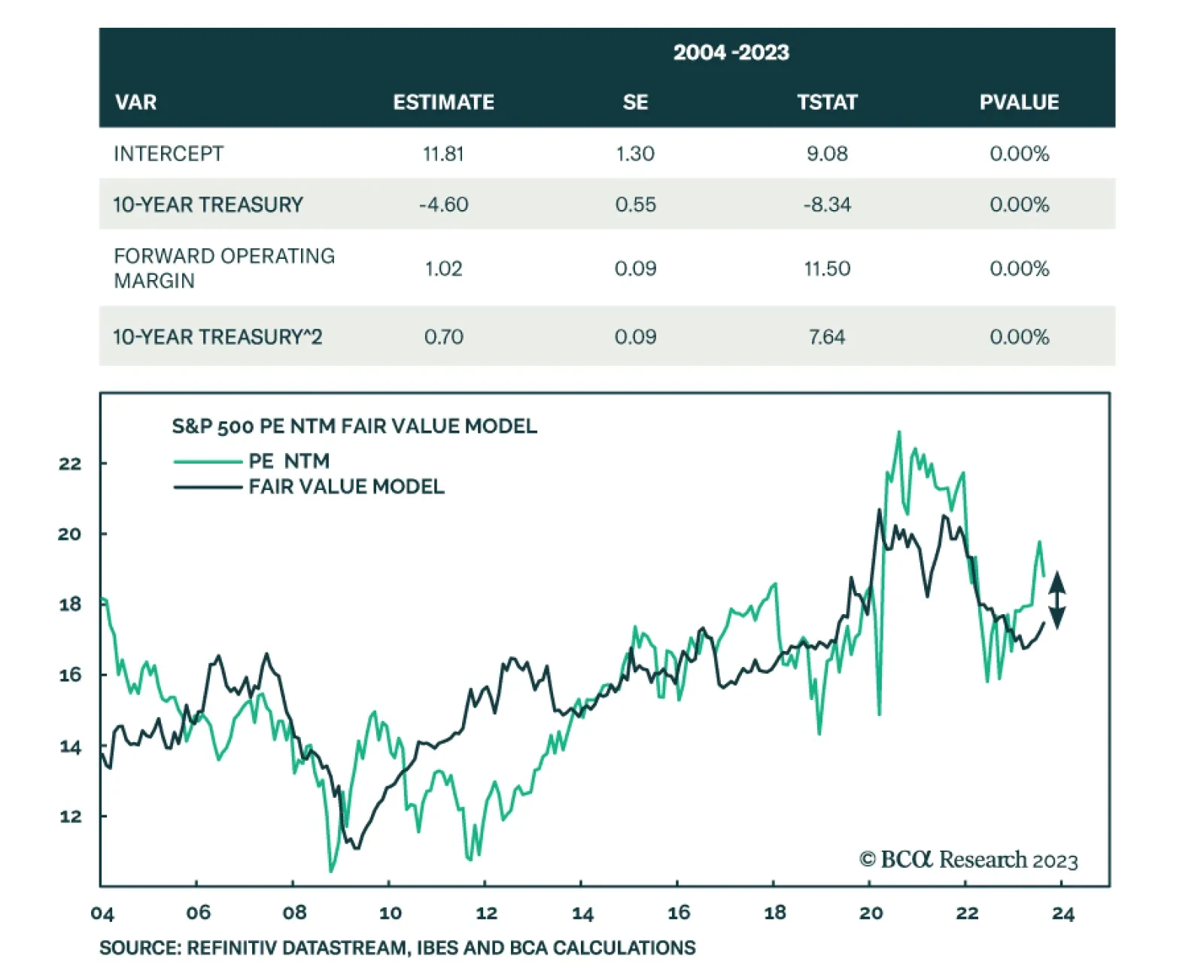

One of the few things US equity investors agree upon these days is that the S&P 500 is expensive whether it is relative to history, other asset classes, or the level of interest rates. But how overvalued is the market? To this end, BCA’s US equity…

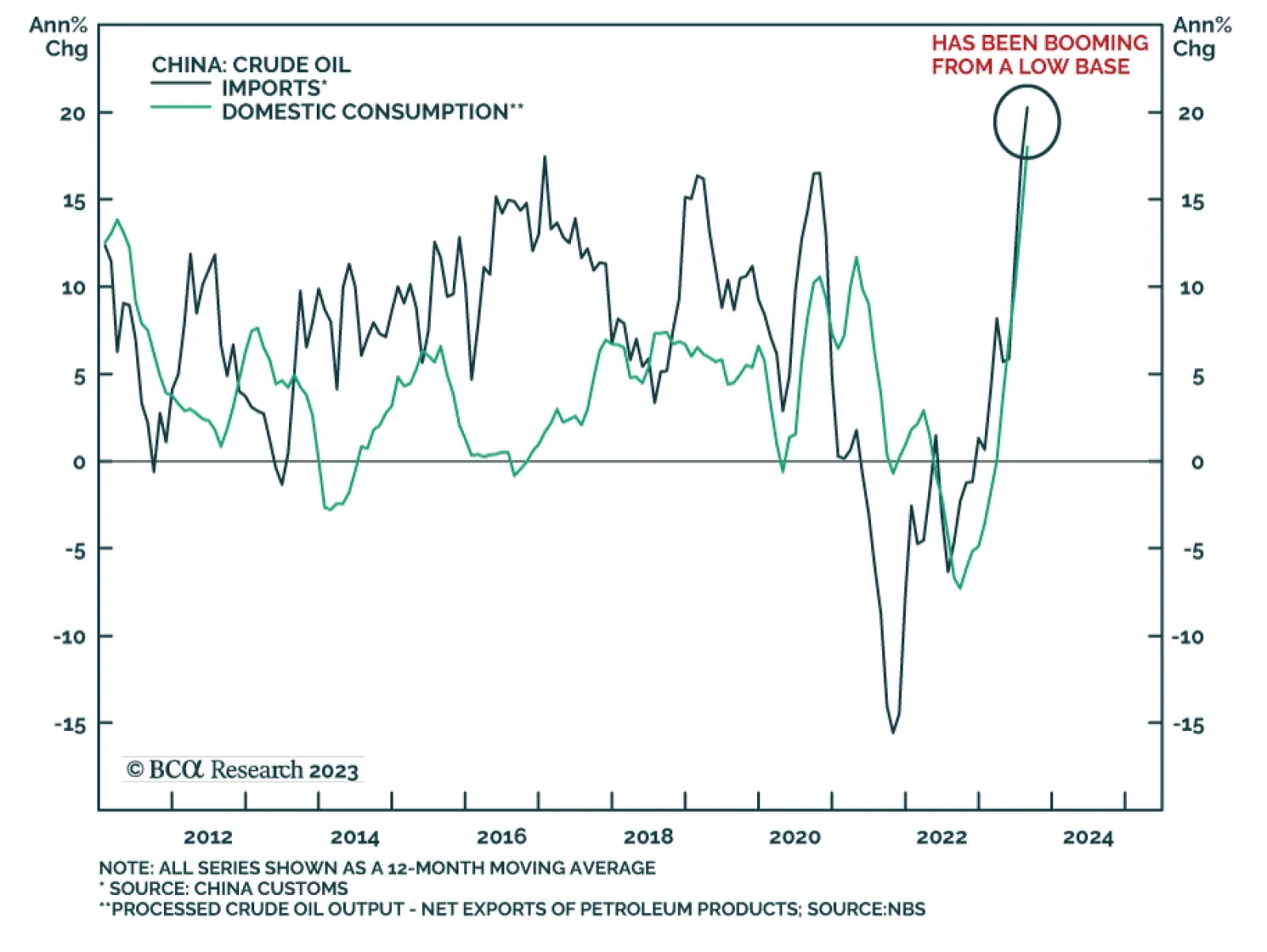

BCA Research’s China Investment Strategy service estimates that China’s oil demand growth will decline from 12% year-on-year in the past eight months to a still robust 4%-6% in the next six-to-nine months. China’s crude oil imports and domestic consumption…

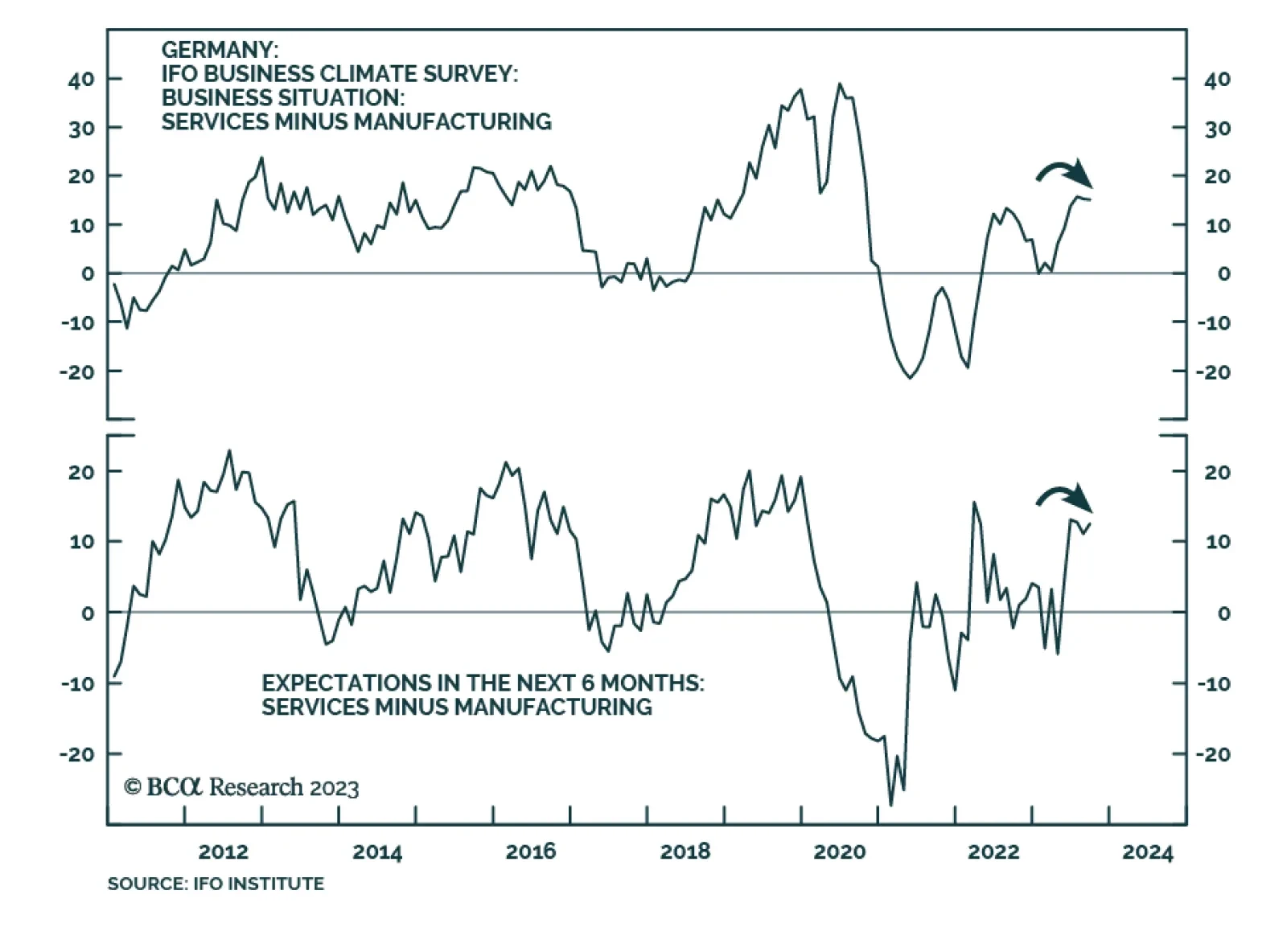

The message from the German Ifo is that although business sentiment continues to weaken, the pace of deterioration slowed in September and appears to be in the process of bottoming. The Business Climate Index’s marginal 0.1-point decline to 85.7 delivered…

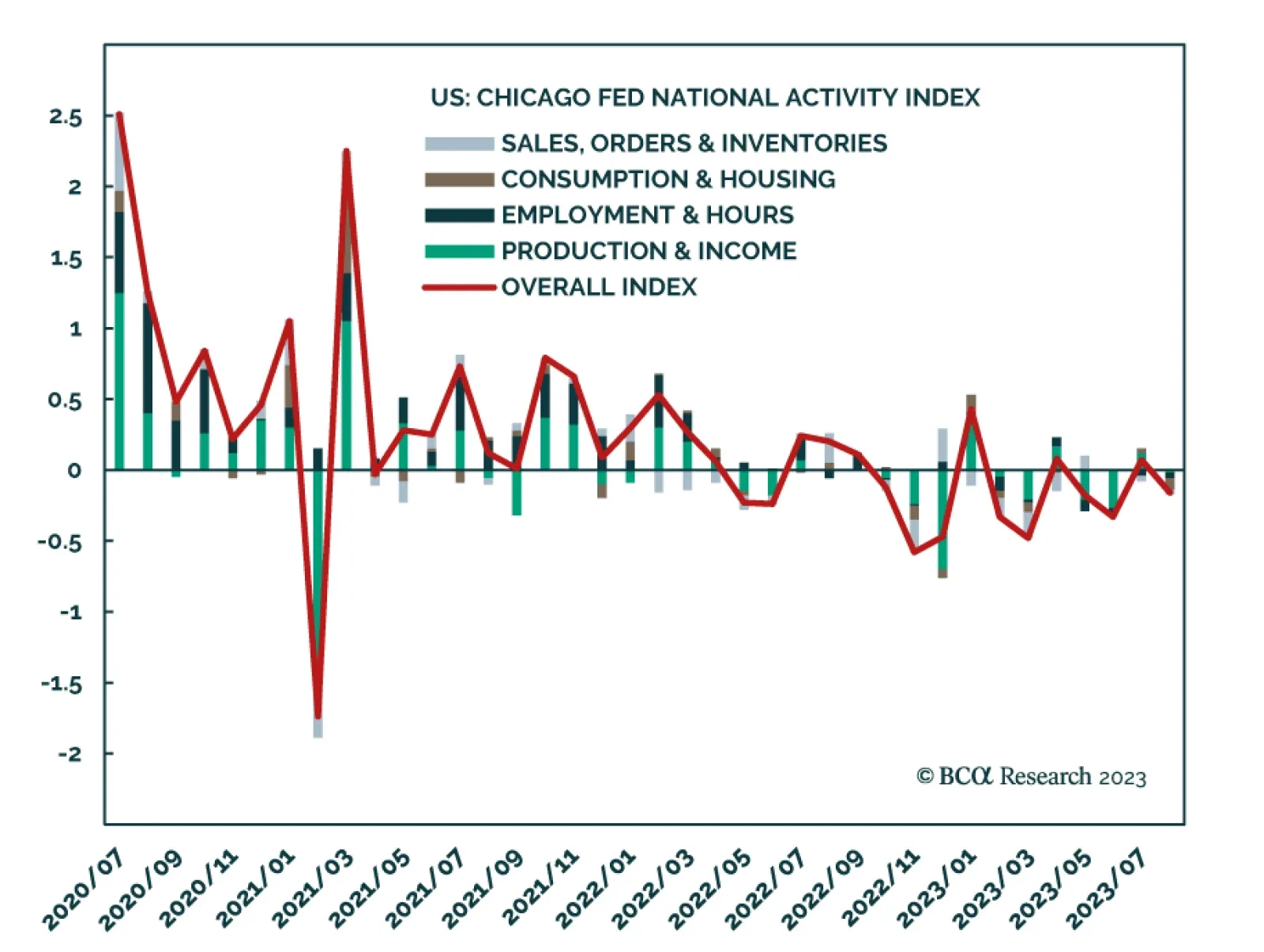

In a recent Insight we highlighted that the GDP tracking indicators produced by regional Fed banks are sending different signals about economic conditions in the US. While the Atlanta Fed’s GDPNow model suggests Q3 growth is around 4.9%, the New York Fed and…

Last week, the Federal Reserve signaled that it expects to deliver one last rate hike this year. Similarly, some of its European counterparts signaled that they are at or close to the end of their hiking cycles. Where does this leave the outlook for USD…

Bulls and bears have capitulated, and the majority of the clients surveyed expect a rangebound market in the near term. Our fair value PE NTM indicates that the S&P 500 is only modestly overvalued. The continued outperformance of the Magnificent Seven faces multiple hurdles. Meanwhile, fiscal spending is unlikely to create an impetus for another leg up in equity performance.

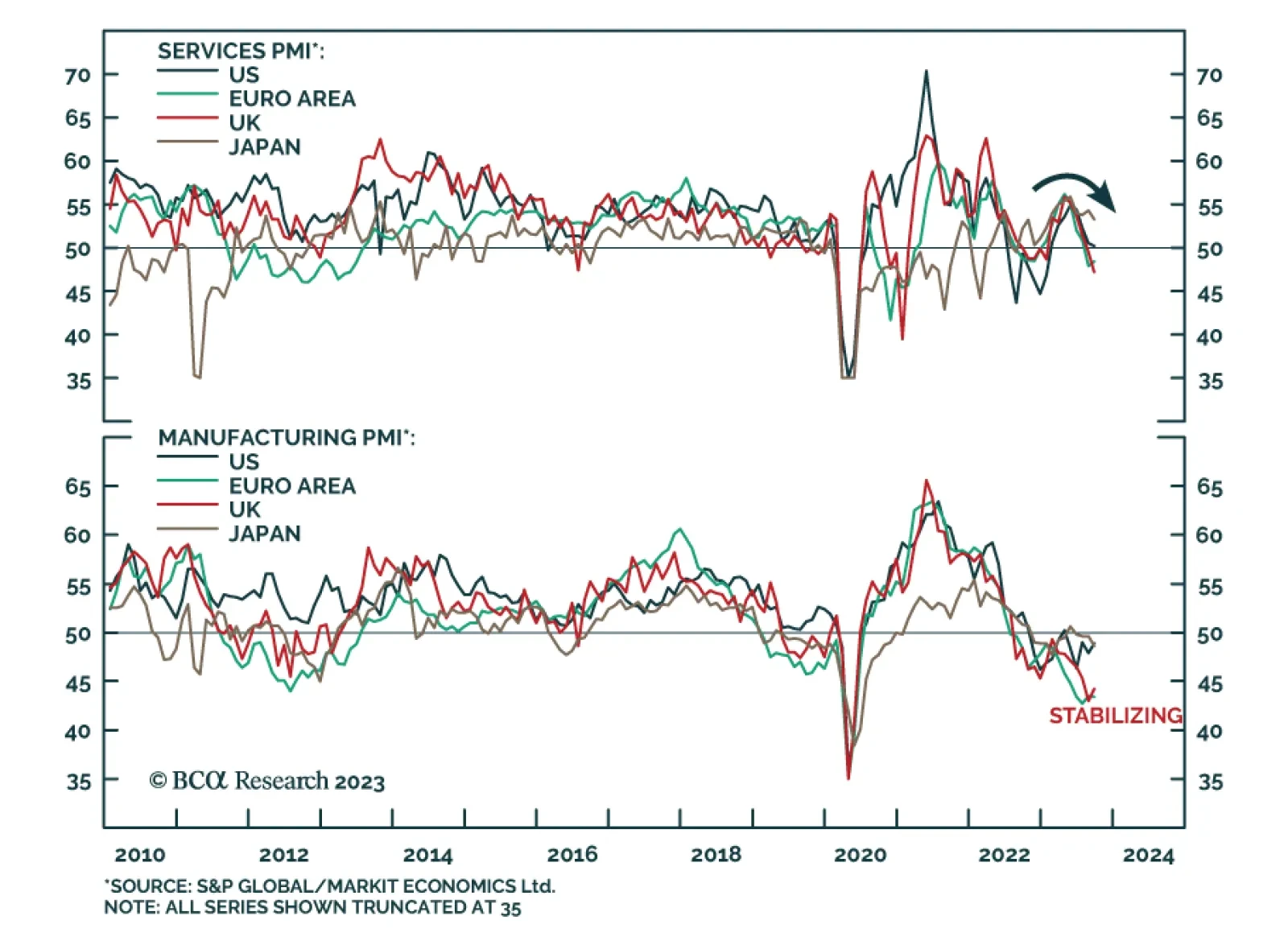

Flash PMIs suggests that the tailwind to services from pent-up demand during the pandemic is easing and that although the global manufacturing downturn is bottoming, it is not meaningfully reaccelerating. In the case of the US, the Services PMI’s…

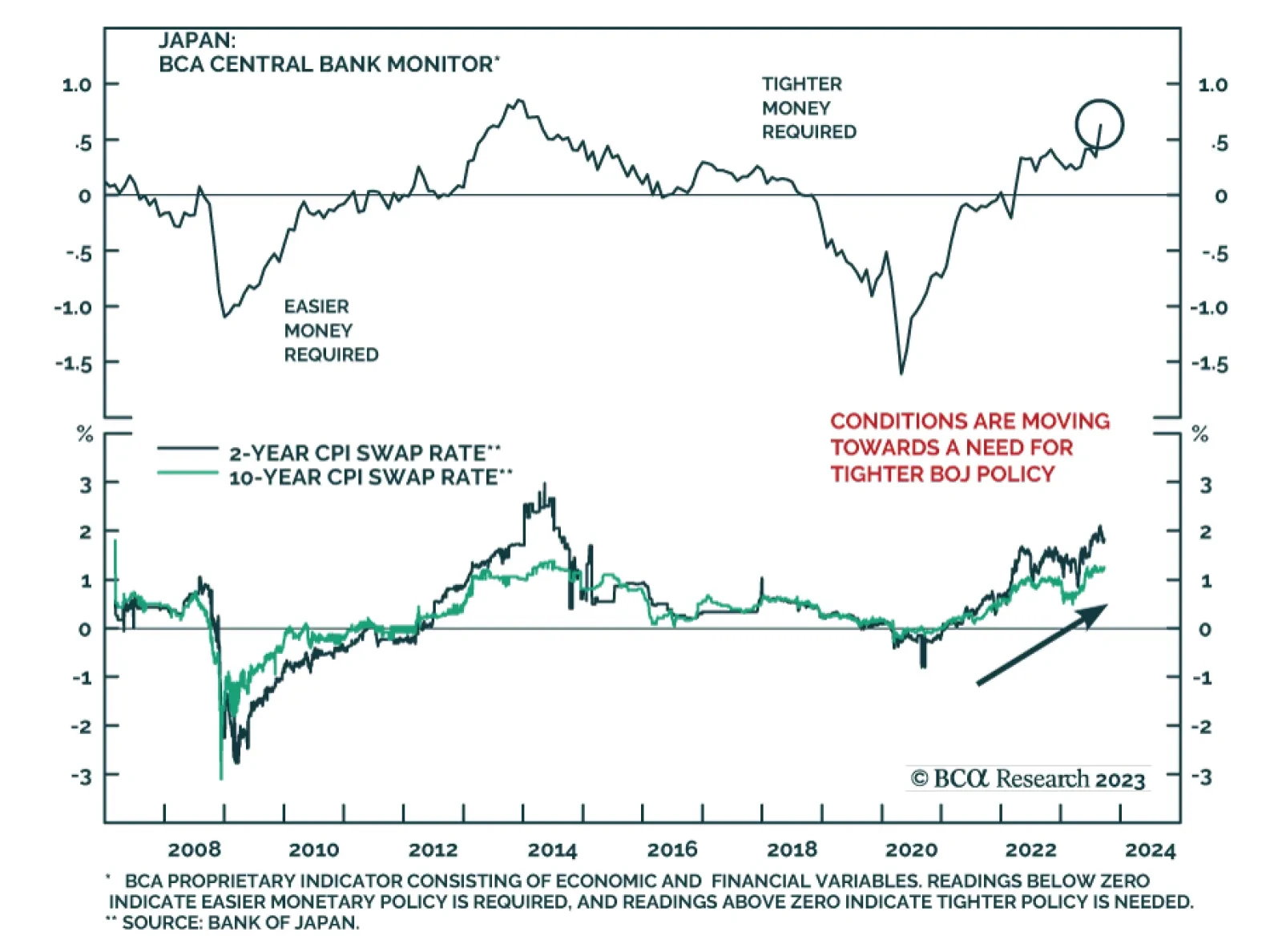

As expected, the Bank of Japan voted unanimously to keep policy unchanged on Friday. The policy rate remains at -0.1% and the central bank maintains Yield Curve Control (YCC) on 10-year JGB yields. To the extent that the BoJ made an important tweak to its…