Business Cycles

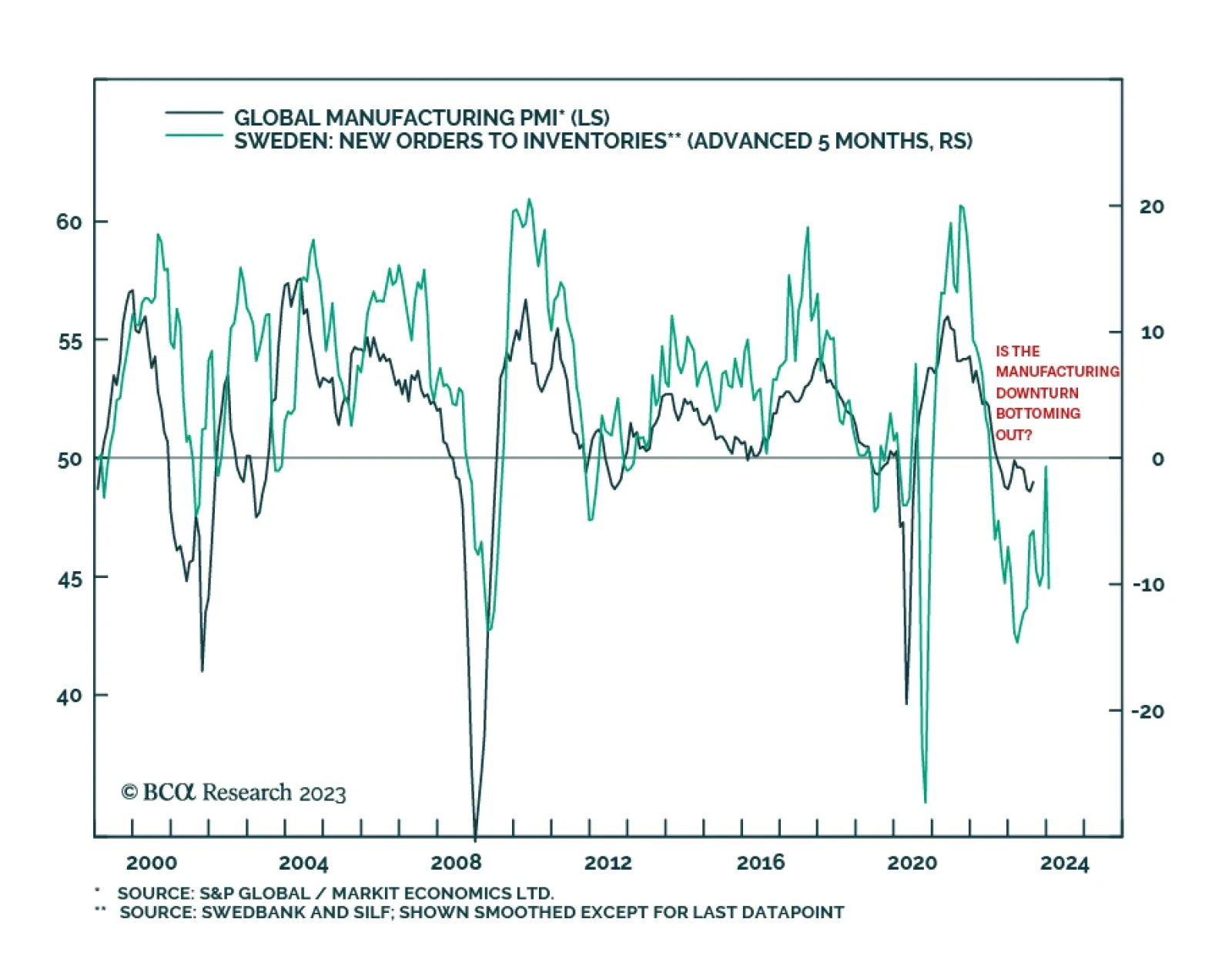

The Global Manufacturing PMI suggests that although the global manufacturing downturn remains intact, the pace of deterioration slowed in August. The headline PMI index ticked up by 0.4 points to 49. In particular, the Output, New Orders, and New Export…

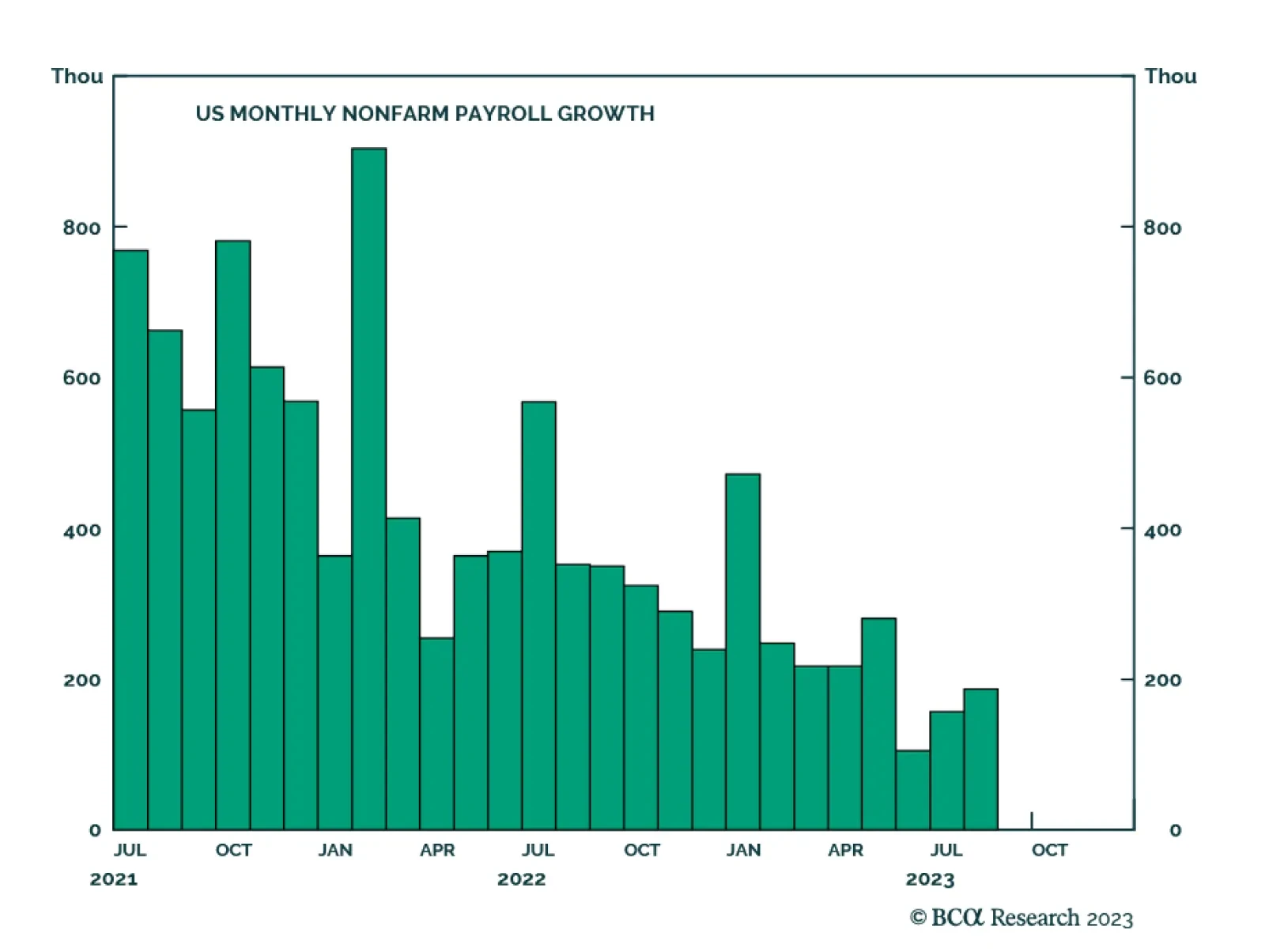

Friday’s US employment report suggests that the softening of the labor market is continuing at a steady pace. Although nonfarm payroll employment in June and July was revised down by 110 thousand, the 187 thousand increase in August came in above expectations…

In Part 2 of this series, we prescribe the treatment needed to produce a recovery for the ailing Chinese economy. Authorities will only panic and unleash “irrigation-style” stimulus if the unemployment rate rises sharply, or a financial crisis unravels in onshore markets. This is not yet the case.

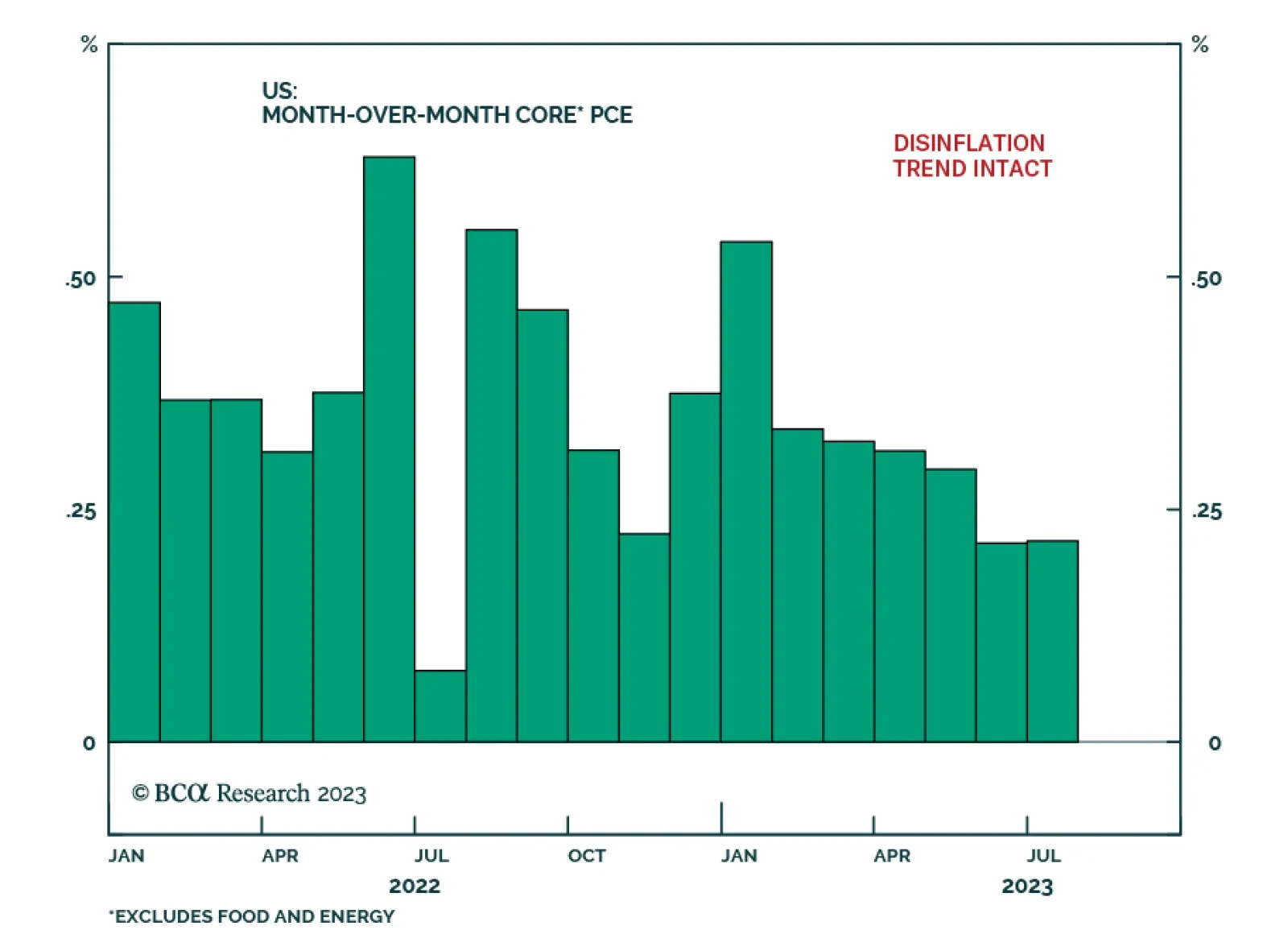

The US Personal Income and Outlays report shows consumption remained resilient in July. Although personal income growth decelerated from 0.3% m/m to 0.2% m/m, spending accelerated from an upwardly revised 0.6% m/m to 0.8% m/m – above expectations of 0.7% m/m.…

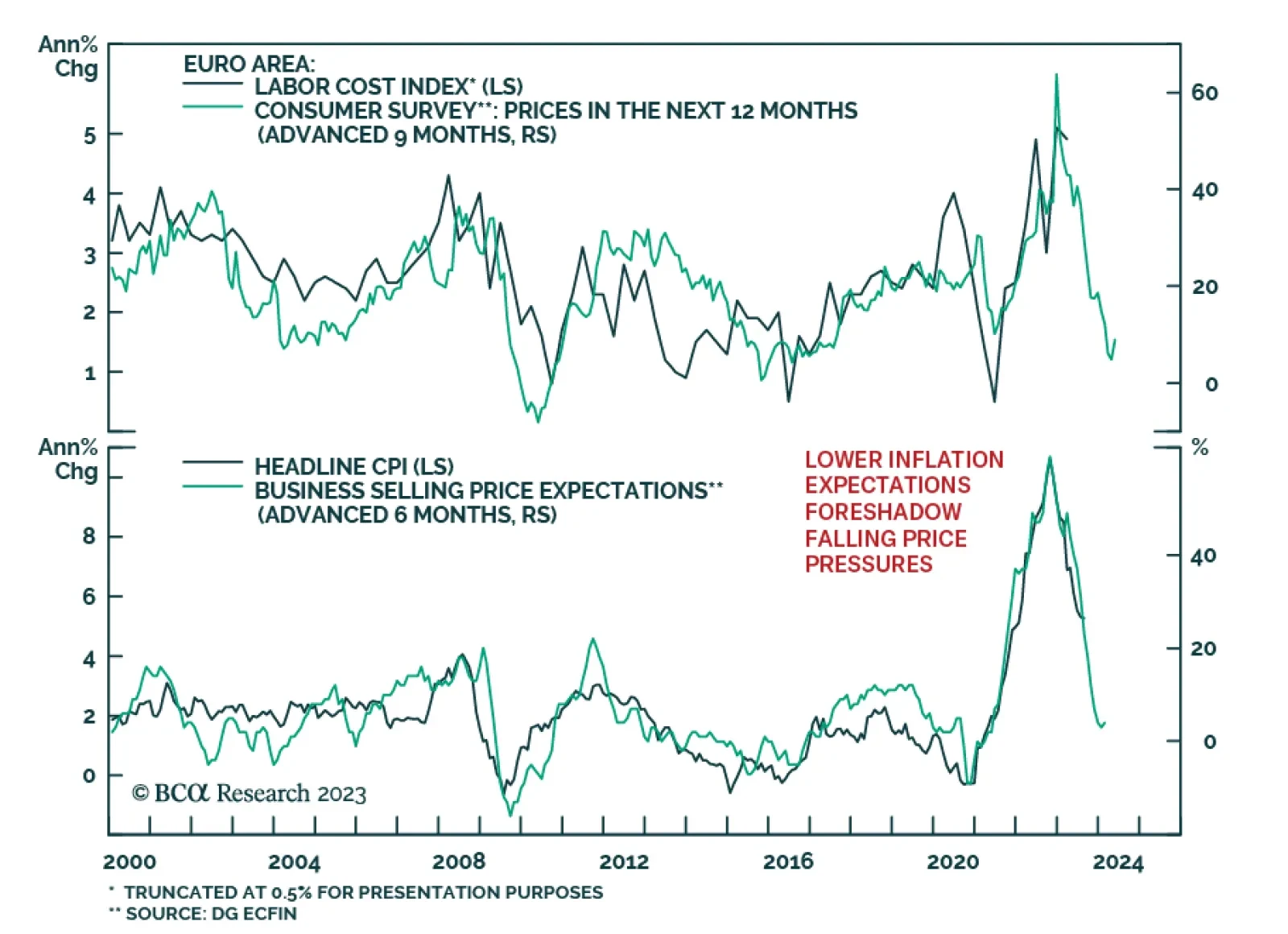

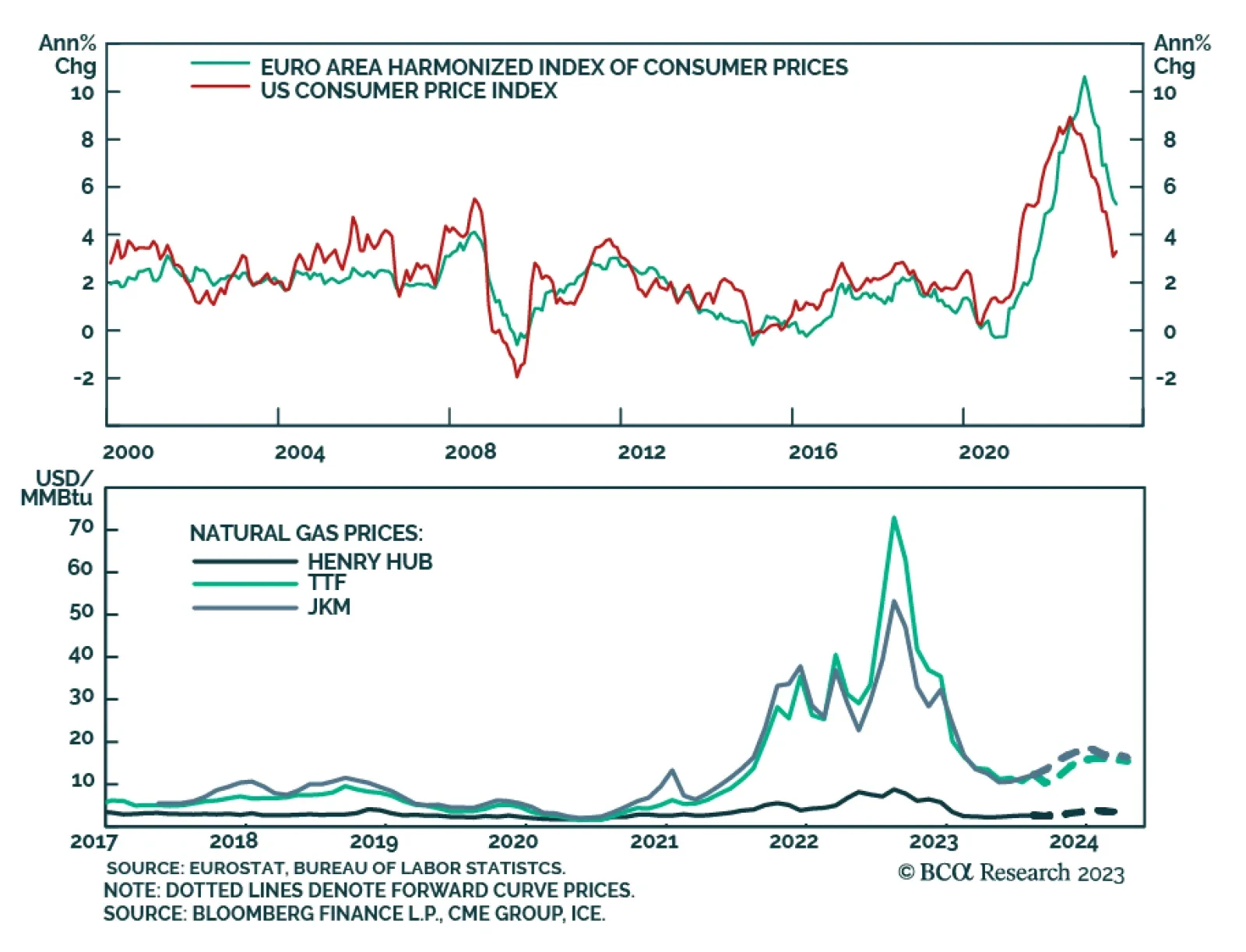

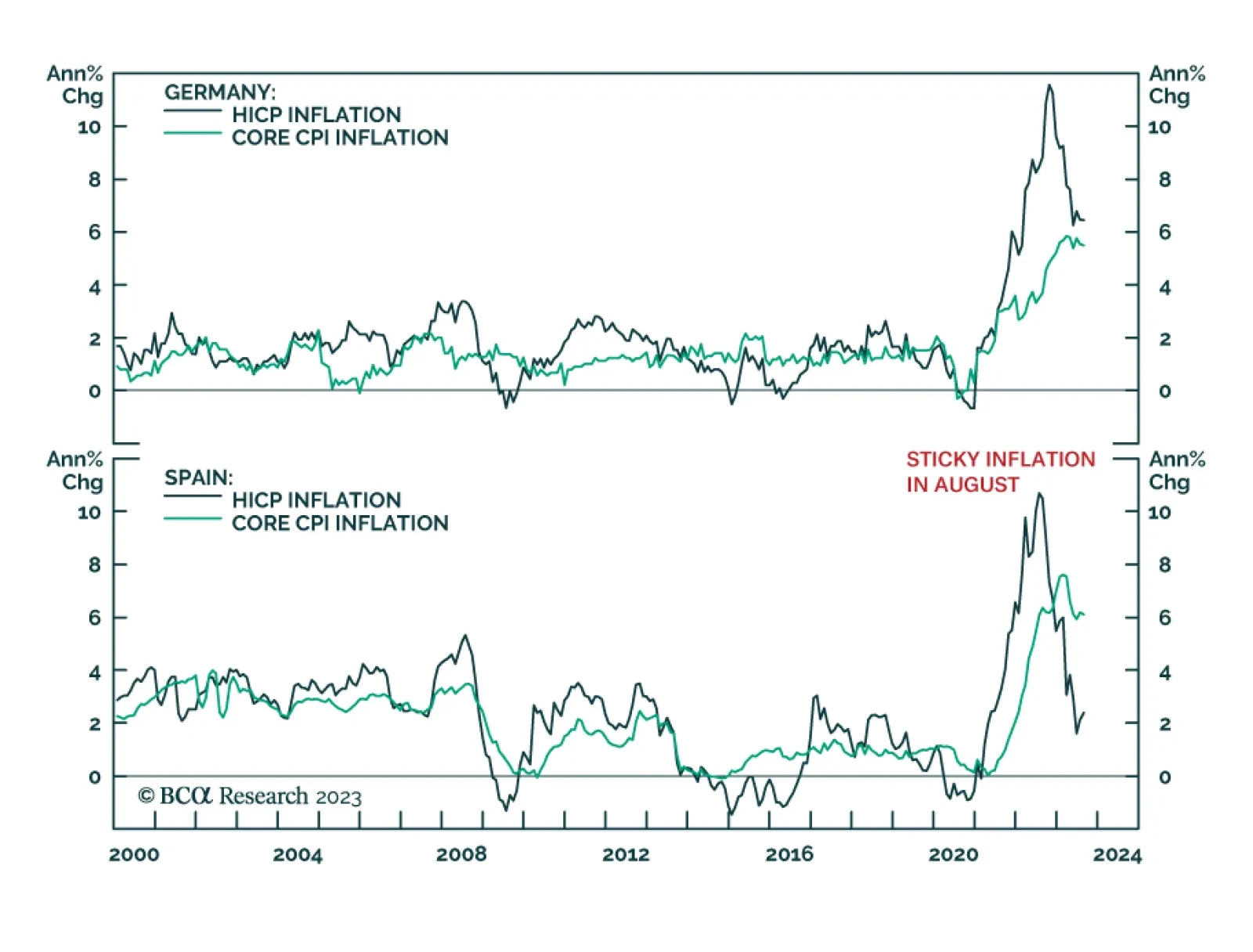

Eurozone headline inflation surprised to the upside in August, confirming the signal from the preliminary German and Spanish releases. The year-on-year gauge was unchanged at 5.3% – surprising expectations of a deceleration to 5.1%. Similarly, the 0.6%…

According to BCA Research’s Commodity & Energy Strategy service, current monetary policy settings at the Fed and ECB risk pushing commodity and energy prices lower. Lower prices and higher rates will suppress capex and set the stage for higher inflation…

Euro Area inflation data surprised to the upside on Wednesday. According to preliminary data, although Germany’s harmonized headline CPI inflation rate fell from 6.5% y/y to 6.4% y/y in August, it nevertheless came in above consensus estimates calling for…

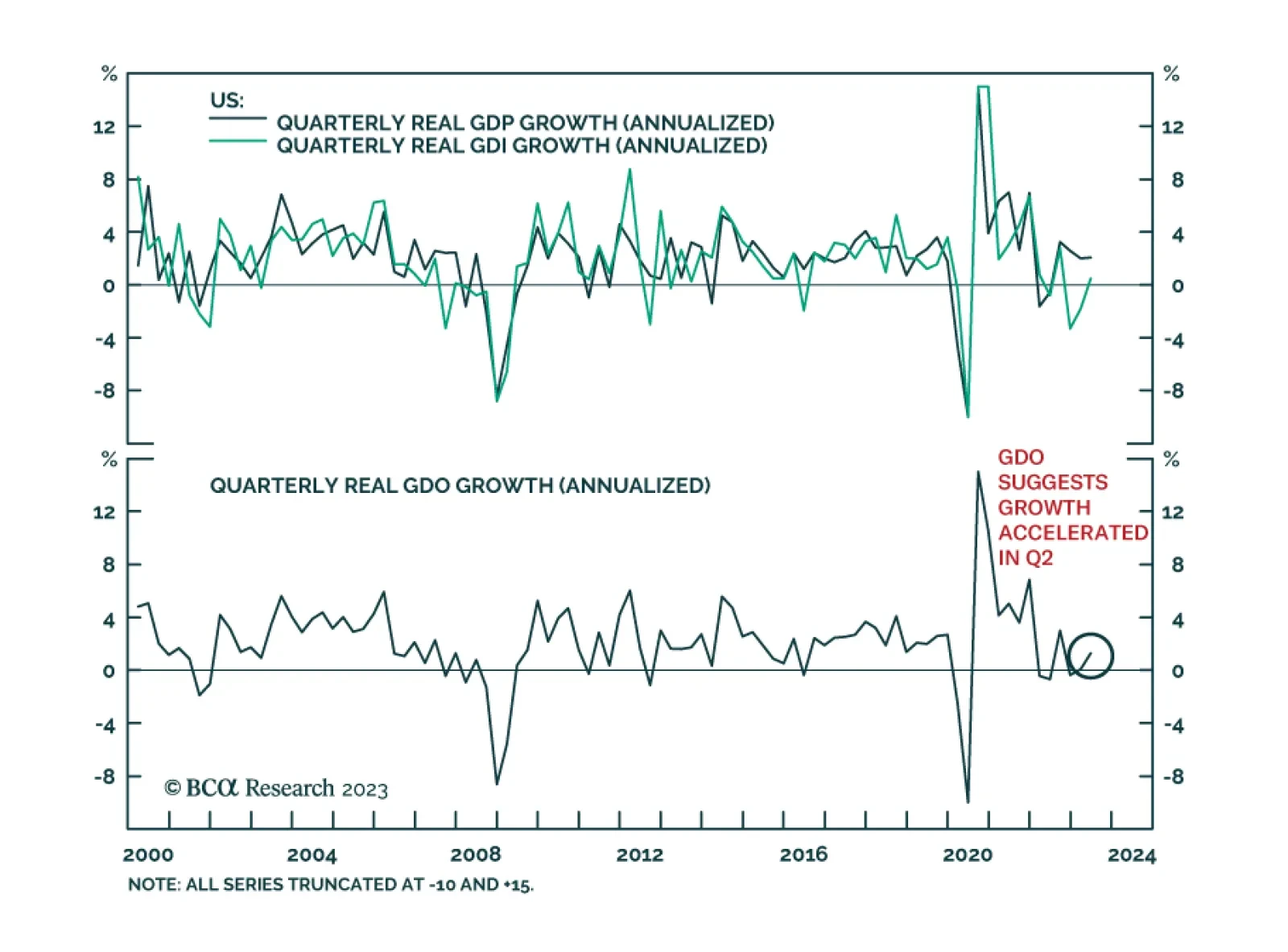

US Q2 GDP growth was revised down from 2.4% to 2.1% on a quarterly annualized basis, only slightly above Q1 growth of 2.0%. Although consumption was revised up by 0.1 percentage points to 1.7%, business spending grew at a slower pace than initially reported…

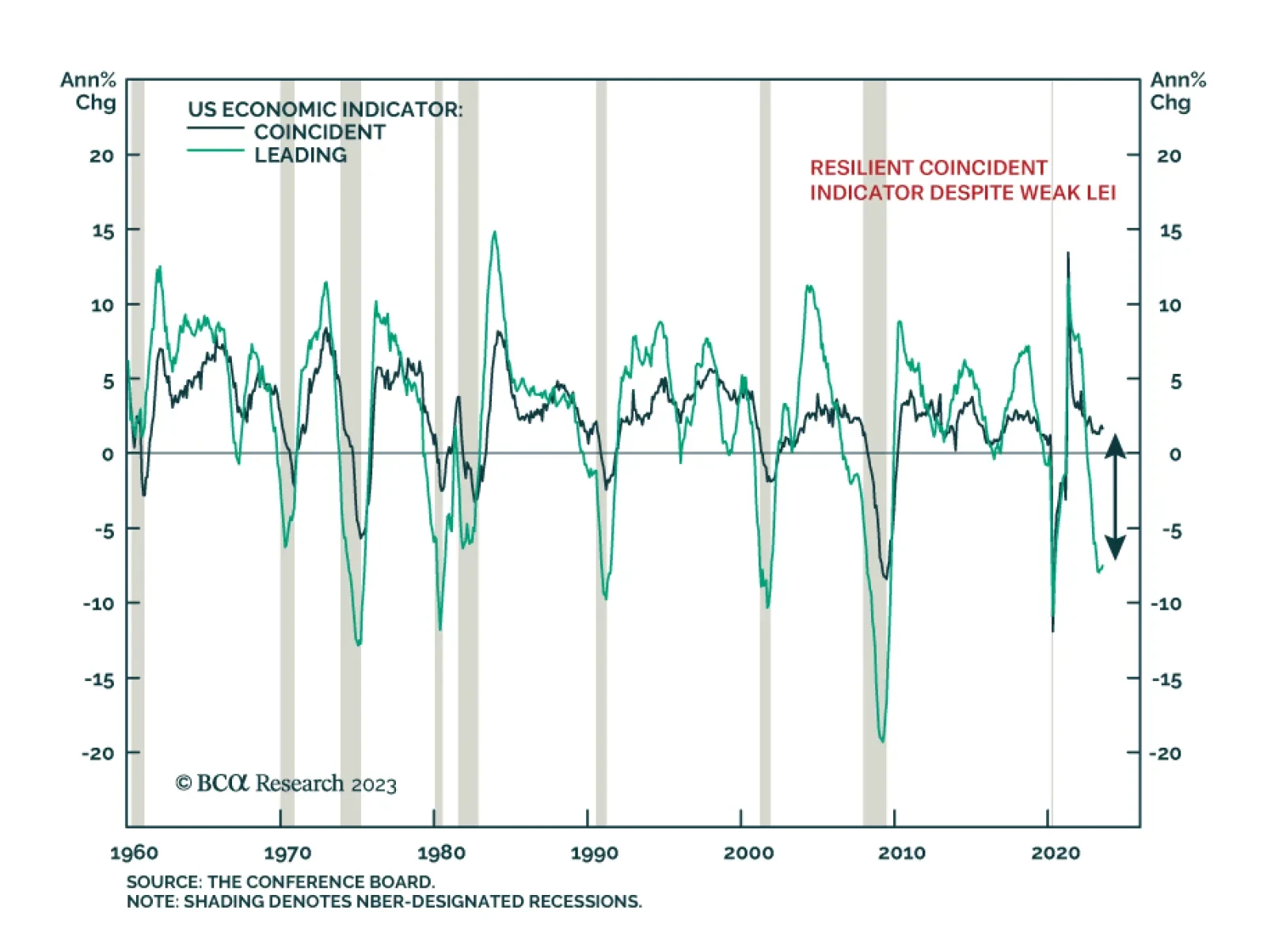

Consensus expectations for the US economy were bleak at the start of the year. In hindsight, this pessimism was excessive: real GDP expanded in the first two quarters of the year (see Country Focus). Similarly, the US Conference Board’s Coincident Economic…

BCA Research’s US Bond Strategy service’s base case outlook calls for a modest curve steepening as wage growth and inflation fall. Odds are that the next big yield curve move will be a bull-steepening that coincides with the onset of the next recession and…