Business Cycles

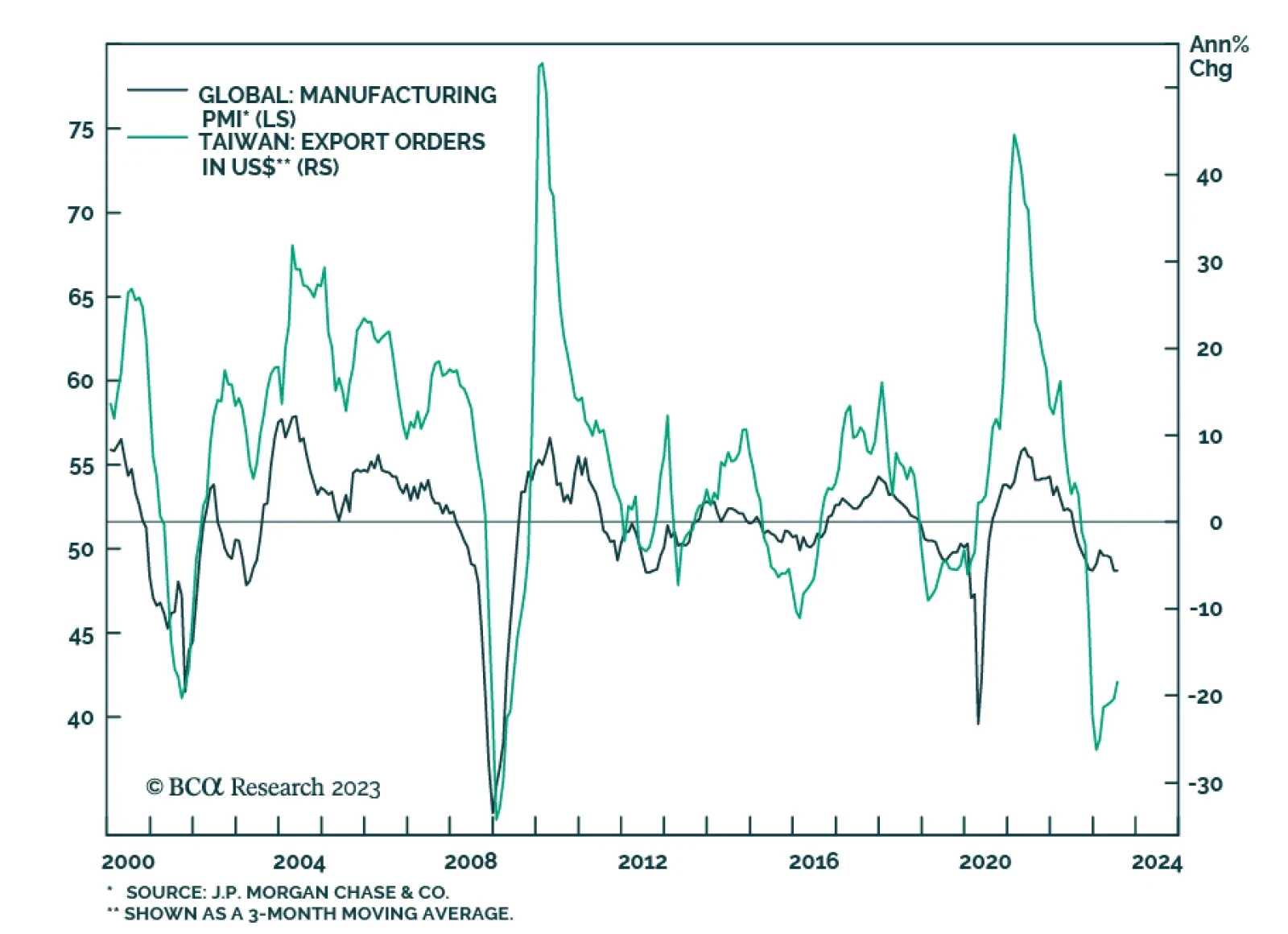

To the extent that Taiwanese export orders are a bellwether for global trade dynamics, the latest update for July provides a less pessimistic signal about the manufacturing cycle. It shows the pace of decline slowed sharply from 24.9% y/y in June to 12.0% y/y…

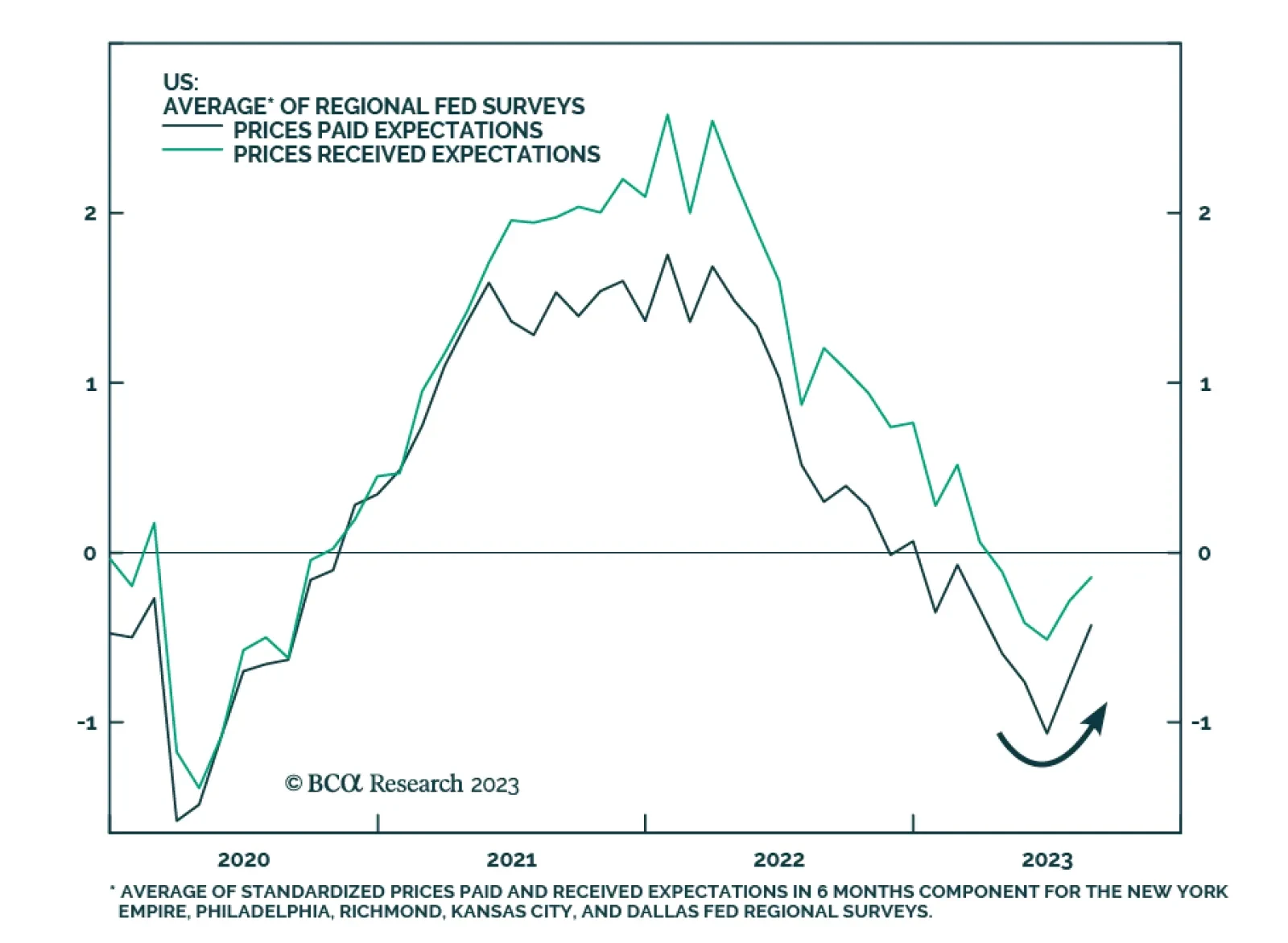

In an Insight last month, we noted that the Global Investment Strategy service increased its subjective odds for the resurgence of US inflation later this year or early next year from 20% to 30%. Here are some of the data points that they track and that point…

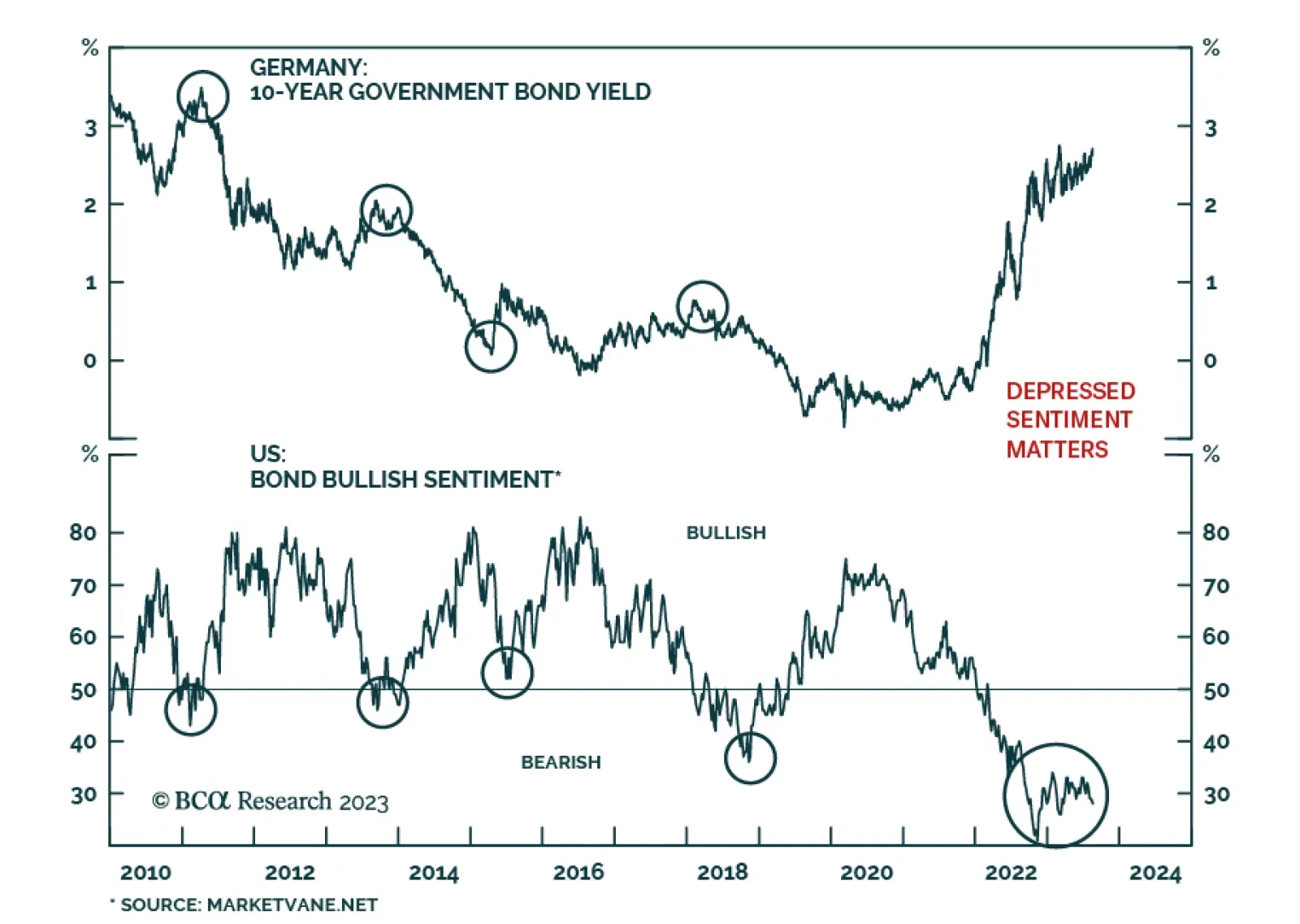

According to BCA Research’s European Investment Strategy service, German yields are unlikely to experience a decisive break out that would carry them to 3%. Five economic forces suggest that German yields are unlikely to move meaningfully higher in the…

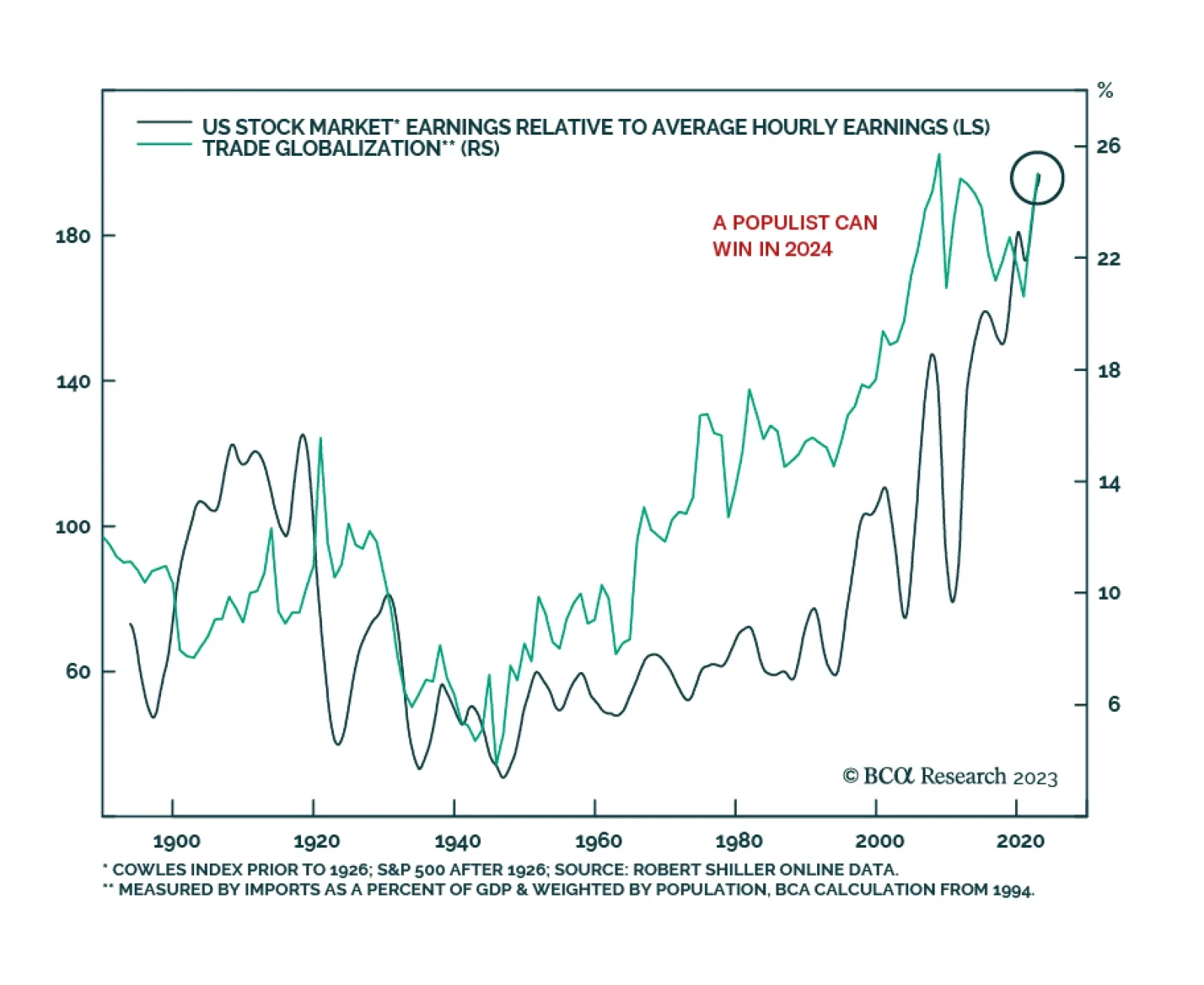

The chief question of the 2024 election is whether US anti-establishment or populist politics is a viable electoral strategy, according to BCA’s US Political Strategy. That will have domestic and global effects not only in 2024-28 but potentially…

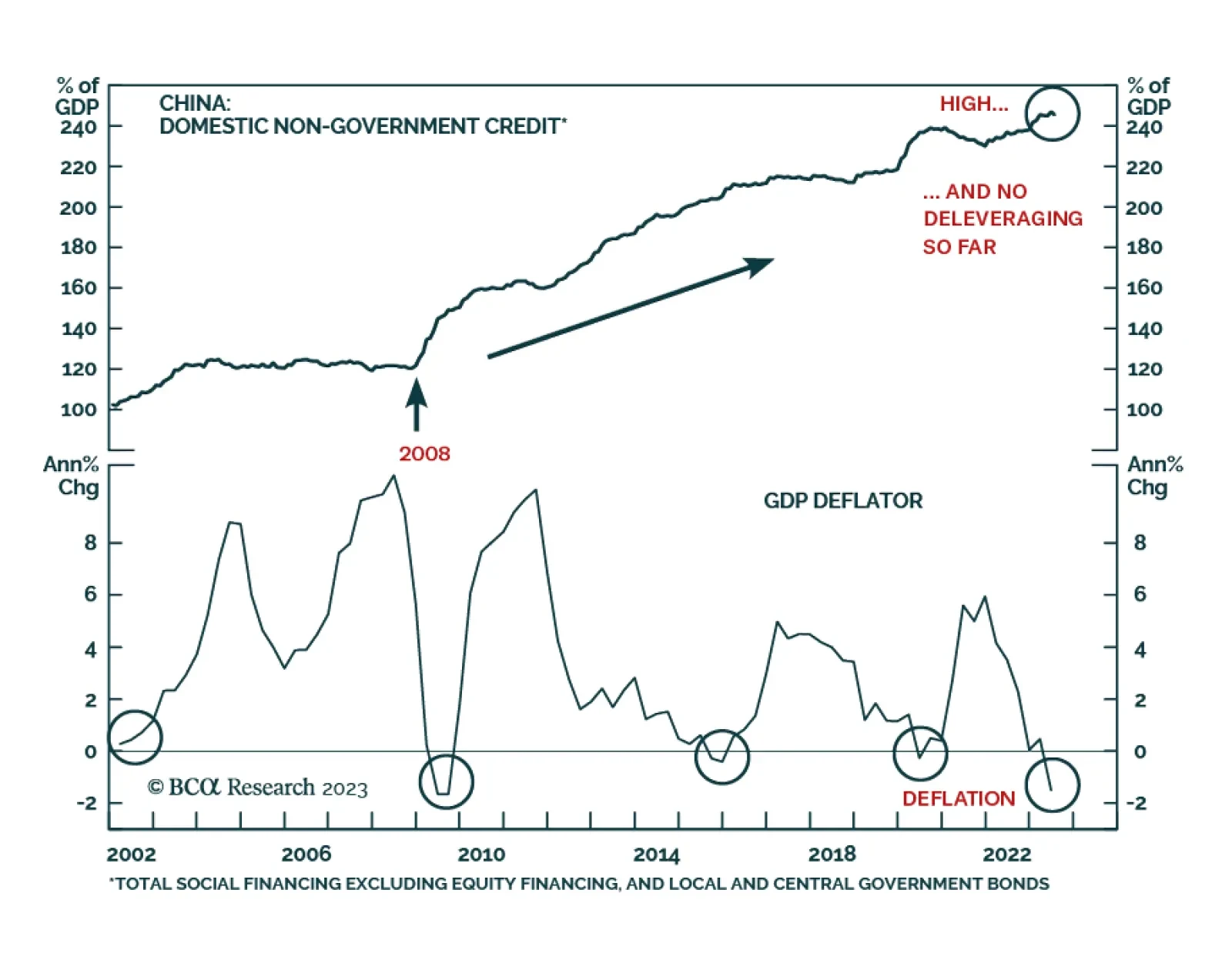

Before doctors prescribe treatments to a patient, they first make a diagnosis. The success of the treatment is contingent upon the accuracy of the diagnosis. The same is true for a country’s economy. Many commentators use notions like debt deflation,…

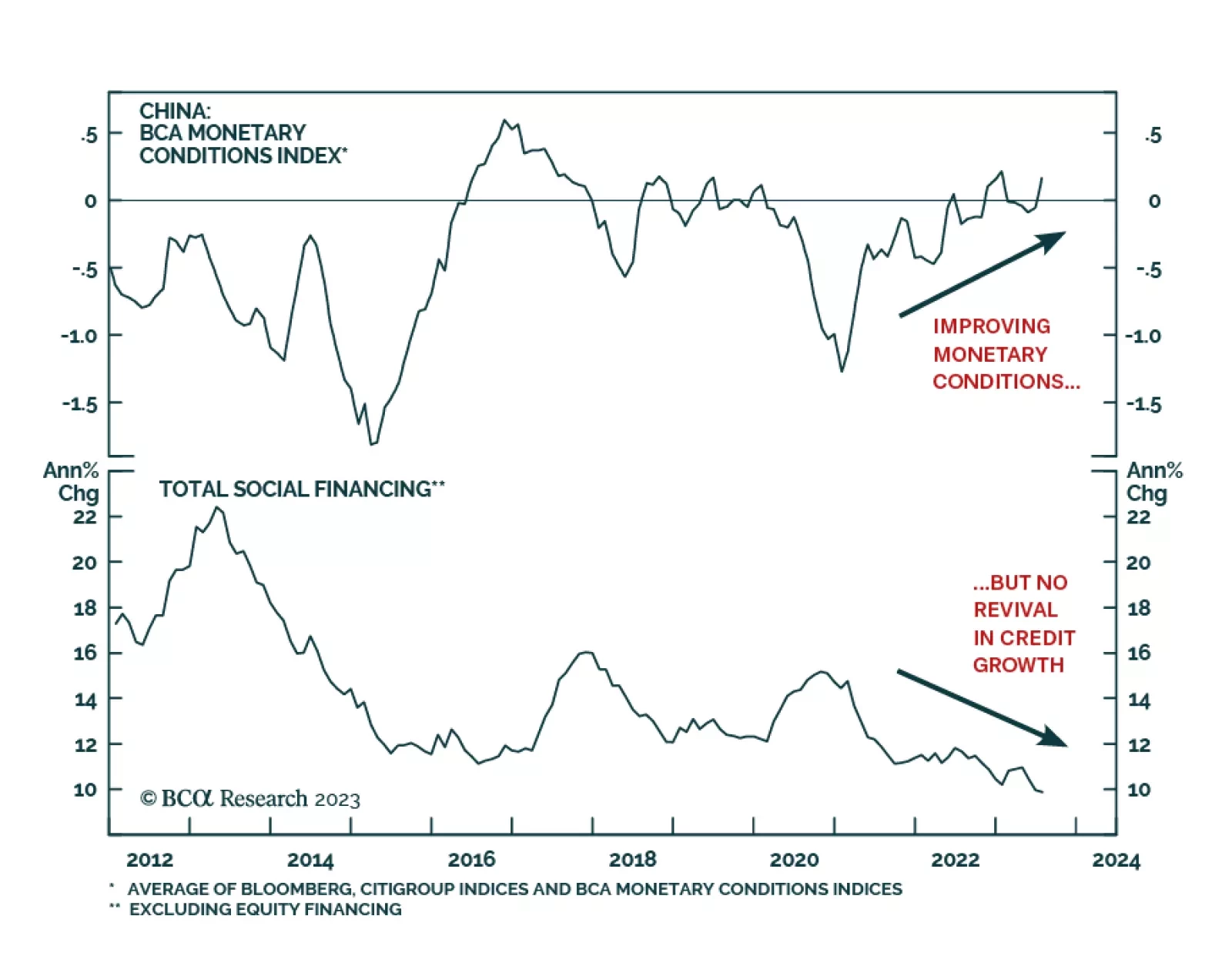

Despite the underwhelming economic recovery, Chinese authorities remain reluctant to open wide stimulus taps as much as they have in past economic downturns. This is corroborated by the PBoC’s marginal interest rate cut last Tuesday. The one-year medium-term…

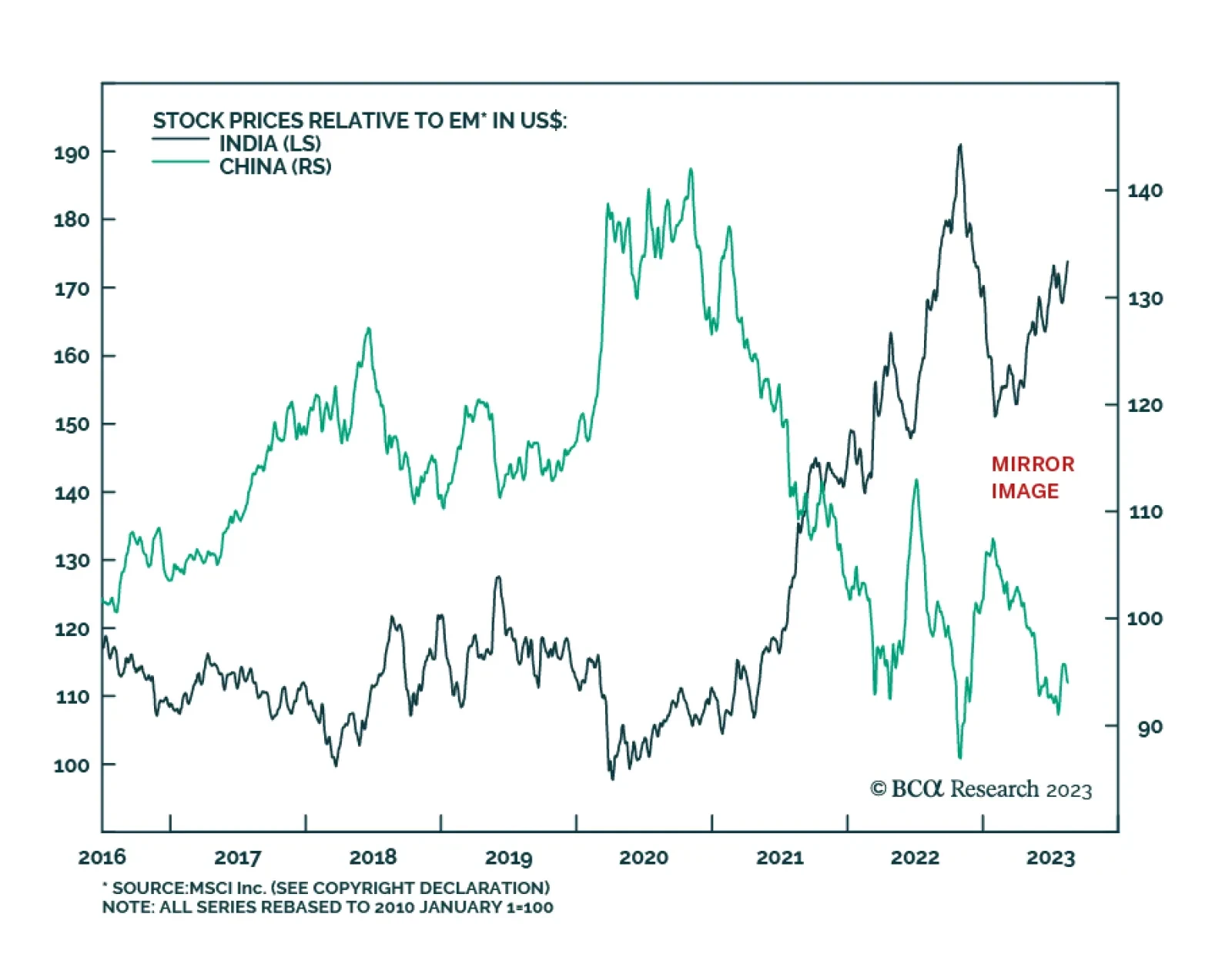

Our Emerging Markets Strategy team expects a further decline in Indian stocks. Foreign equity inflows have been instrumental in the recent rally, but they will likely reverse in the coming months as risk-off sentiments pervade global financial markets. Indian…

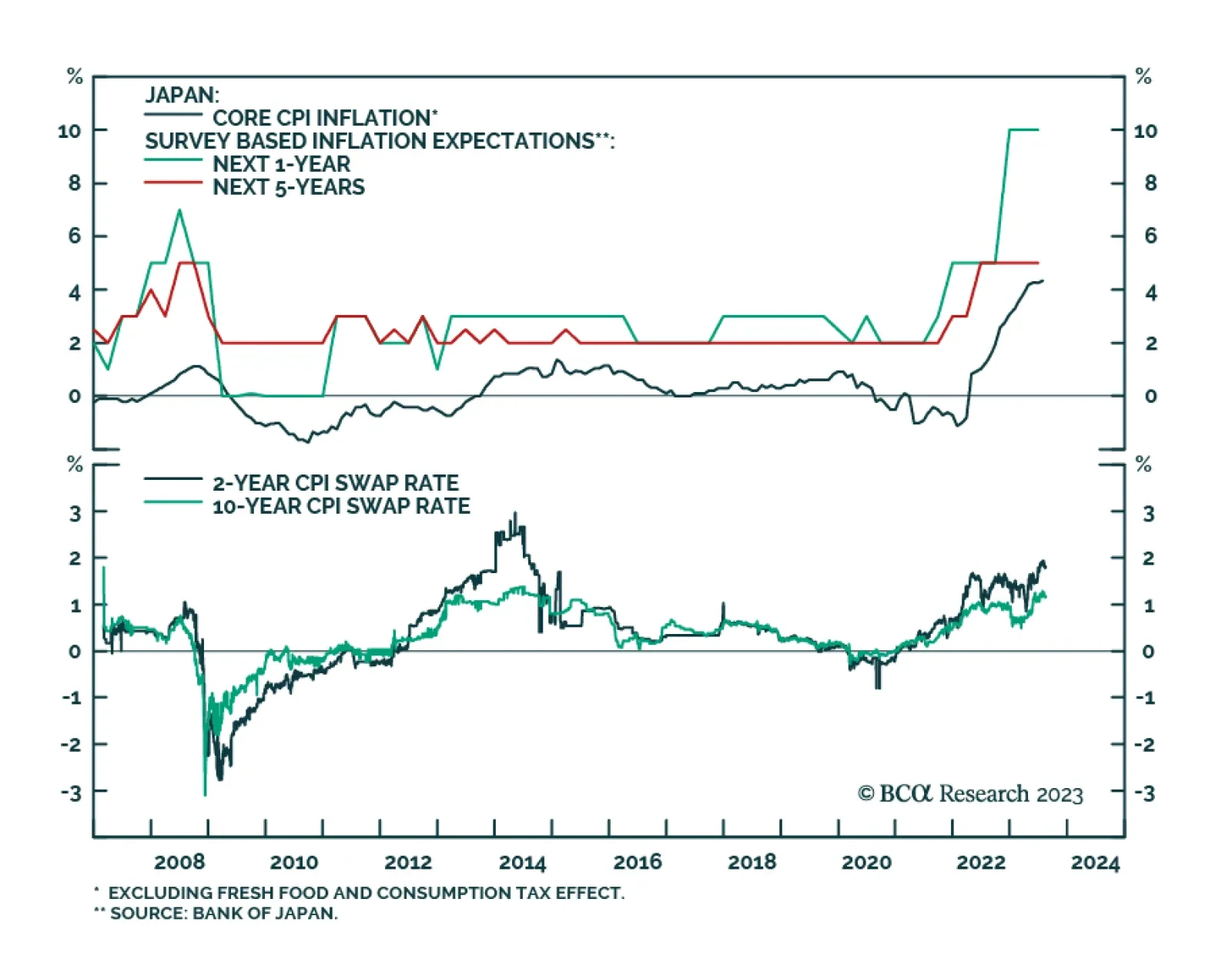

According to BCA Research’s Foreign Exchange Strategy and Global Investment Strategy services, most indications of Japanese inflation are pointing to upside surprises. This will boost interest-rate differentials in favor of the yen. Core-core CPI came…

In this special report, we discuss whether the economic conditions necessary for a stronger yen (and higher JGB yields) will materialize over the next 12-to-18 months.

Commentators often use notions like debt deflation, balance sheet recession, and liquidity trap interchangeably. Yet, these are different concepts. This report develops a framework and provides a diagnosis of China’s economic malaise. A follow-up report will deal with what kind of treatment is needed for a recovery. As a trade, we recommend shorting the EM equity index.