Business Cycles

The selloff in US Treasuries has accelerated in recent weeks and the 10-year US Treasury yield is quickly approaching the cyclical peak of 4.25% that was set last October. While momentum is certainly on the side of the bond bears, our US Bond team doesn’t see…

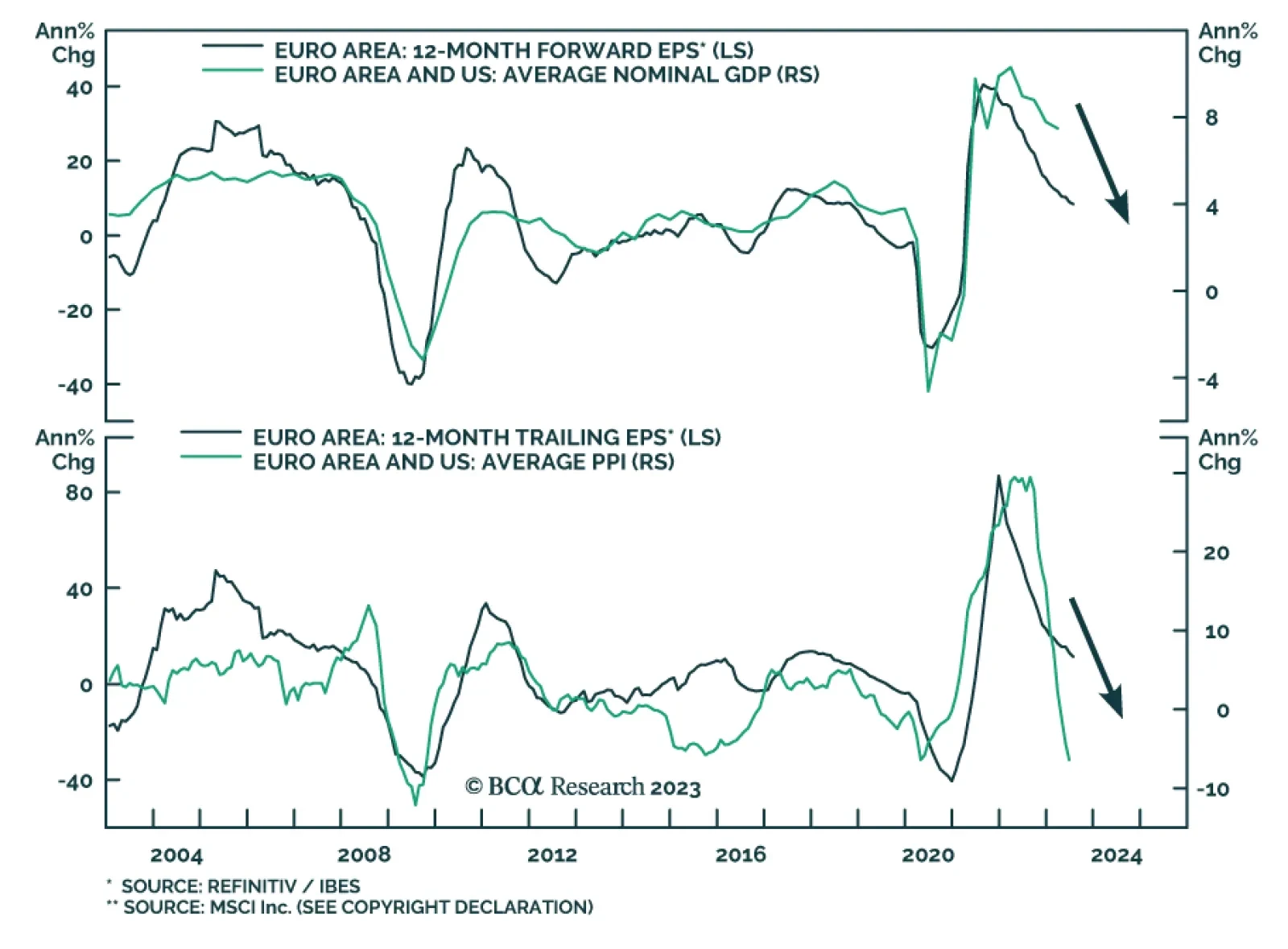

According to BCA Research’s European Investment Strategy service, the earnings outlook of Eurozone equities will continue to deteriorate over the coming two quarters despite the improvement in real economic activity. Earnings and revenue growth are…

Sweden’s preliminary Flash GDP data, which is subject to revisions, points a 1.5% quarter-over-quarter and 2.4% year-over-year contraction. However, this report could potentially constitute the trough in the country’s economic slowdown. Indeed, Sweden’s…

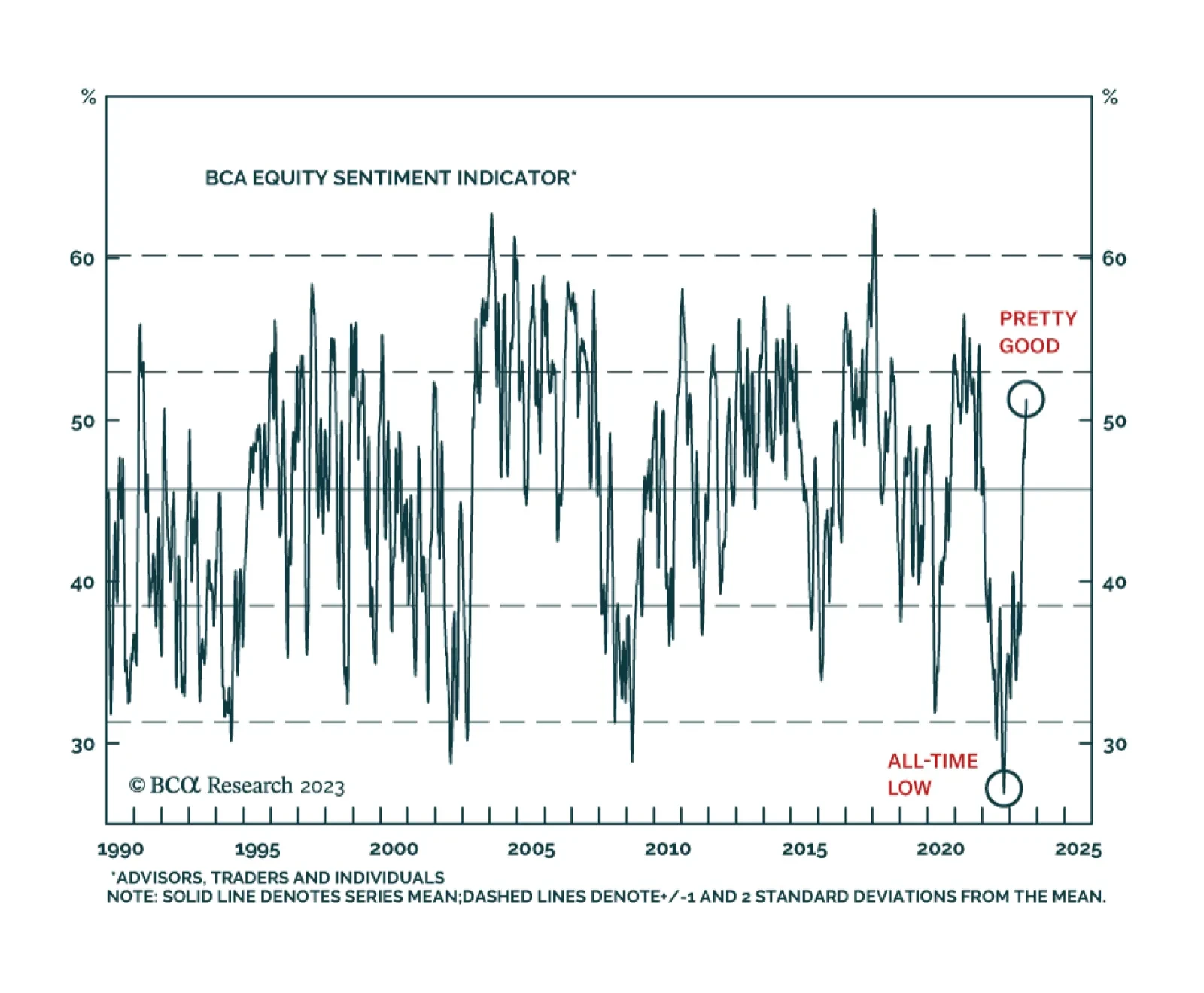

In a recently published report, BCA’s Bank Credit Analyst service reviewed the BCA Valuation Index, alongside three other US equity indicators which are published in Section III of each month’s report. The other indices included in our suite of equity…

BCA Research's US Investment Strategy service’s yearlong recommendation to overweight equities was founded on its high-conviction view that investors were underestimating American consumers’ resources and resolve. The consensus pooh-poohed the mountain of…

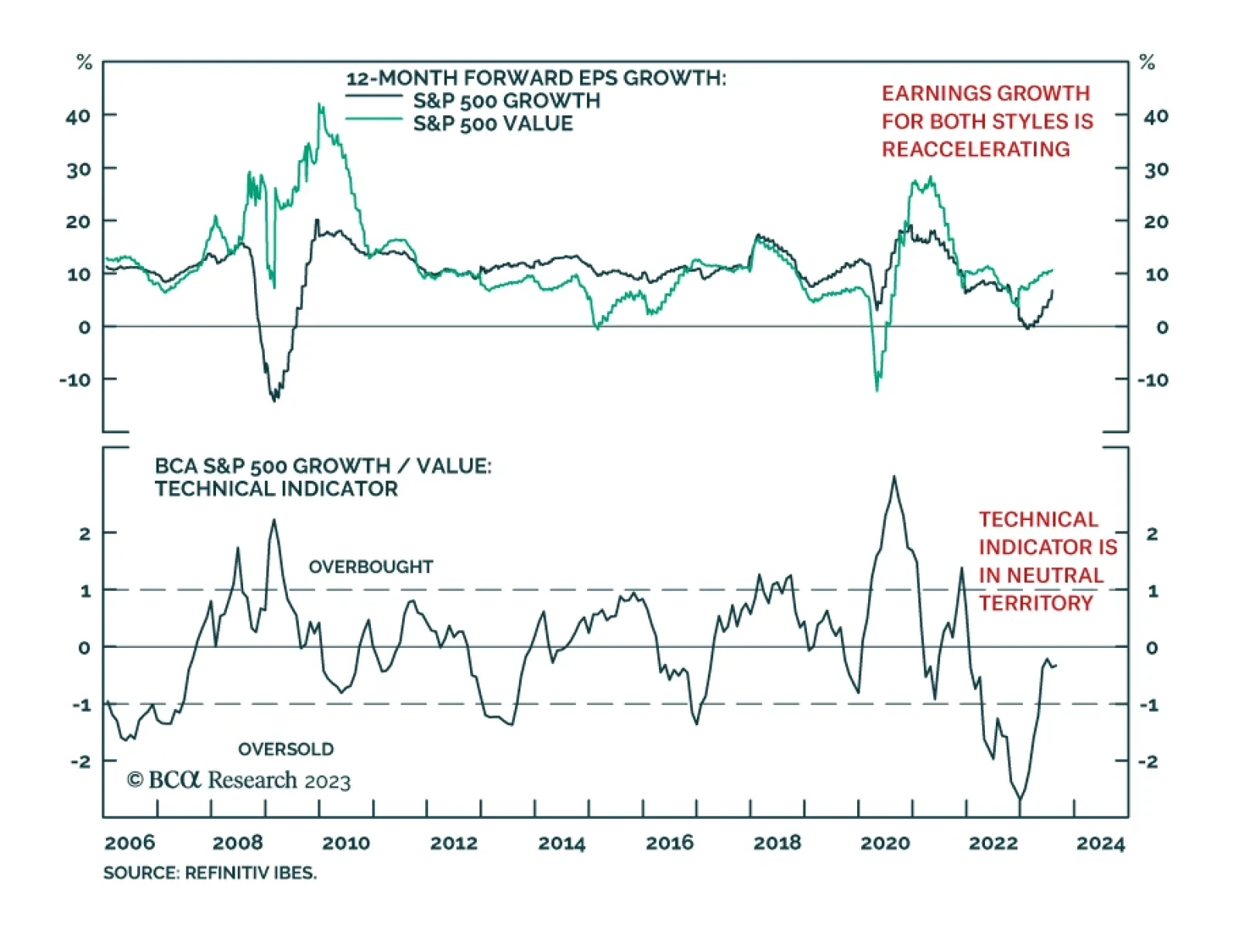

According to BCA Research’s US Equity Strategy service, the outperformance of Growth sectors most likely has run its course. The team has opened an overweight in Growth vs. Value in April. Since then, the trade is up 2.73%. They are now closing this…

Outperformance of Growth sectors most likely has run its course. It is time to shift Growth vs. Value allocation to neutral, downgrade Semis, and upgrade Energy to overweight.

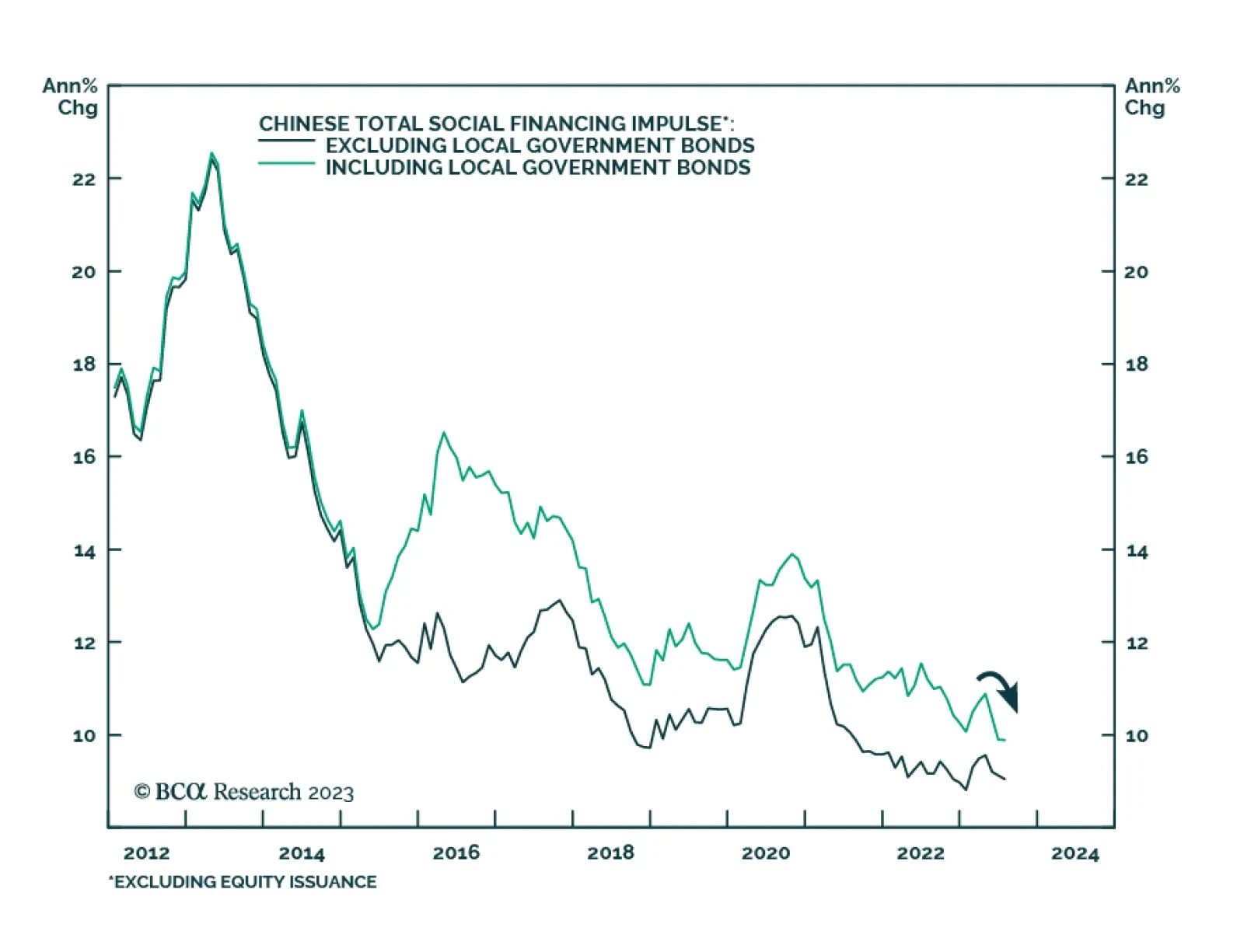

Chinese credit and money data fell significantly below expectations in July. The CNY 0.53 trillion increase in aggregate social financing marks a significant slowdown from CNY 4.22 trillion in June and came in significantly below expectations of CNY 1.10…

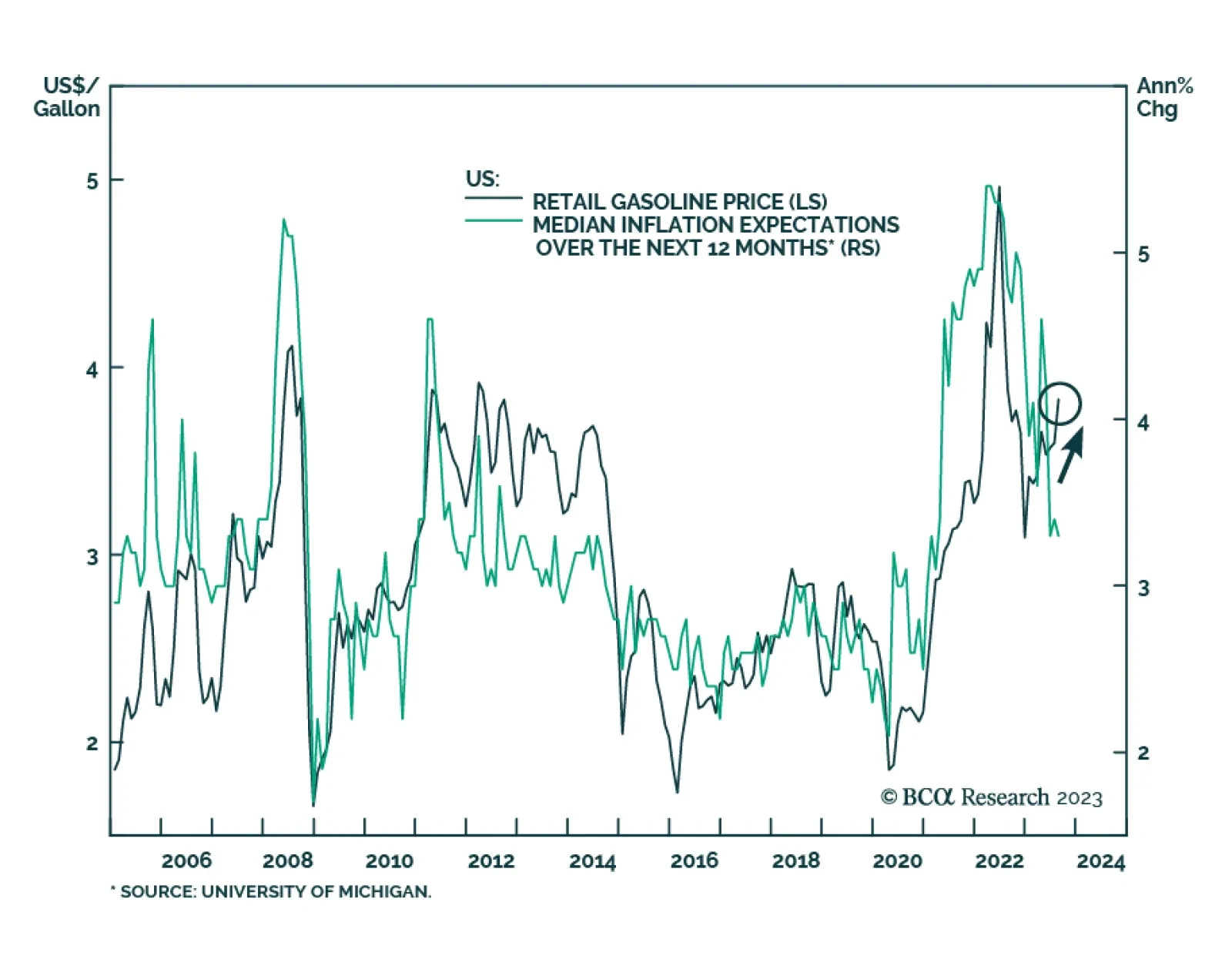

The preliminary release of the University of Michigan’s Consumer Sentiment survey shows US households’ 1-year ahead inflation expectations unexpectedly ticked down from 3.4% to 3.3% in August, surprising consensus estimates of an increase to 3.5%. Similarly,…

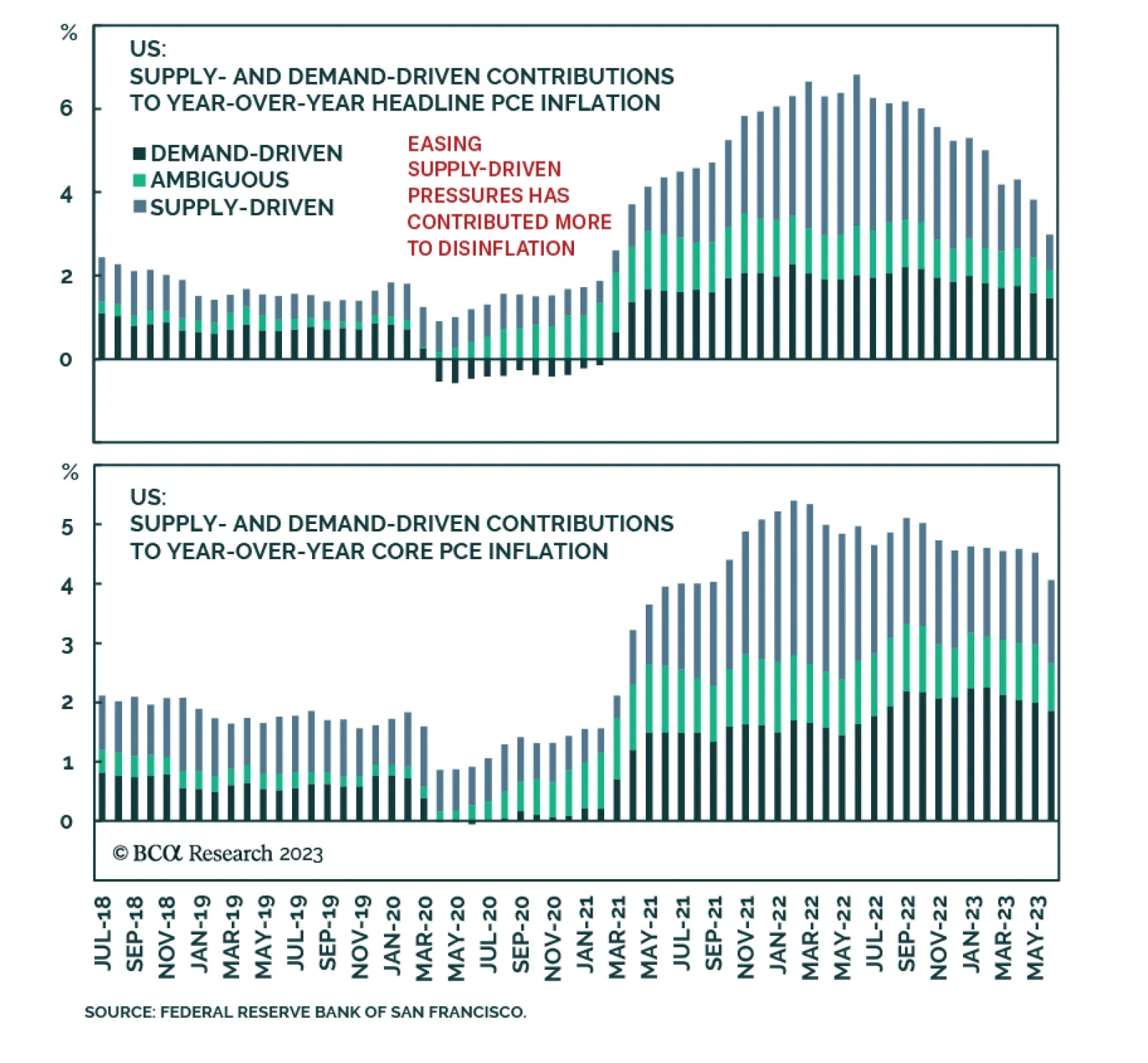

While the July US CPI release provided a positive signal that the disinflationary trend remains intact, a key question going forward is how much more scope is there for this process to run. One way to answer this question is by assessing the progress in…