Canada

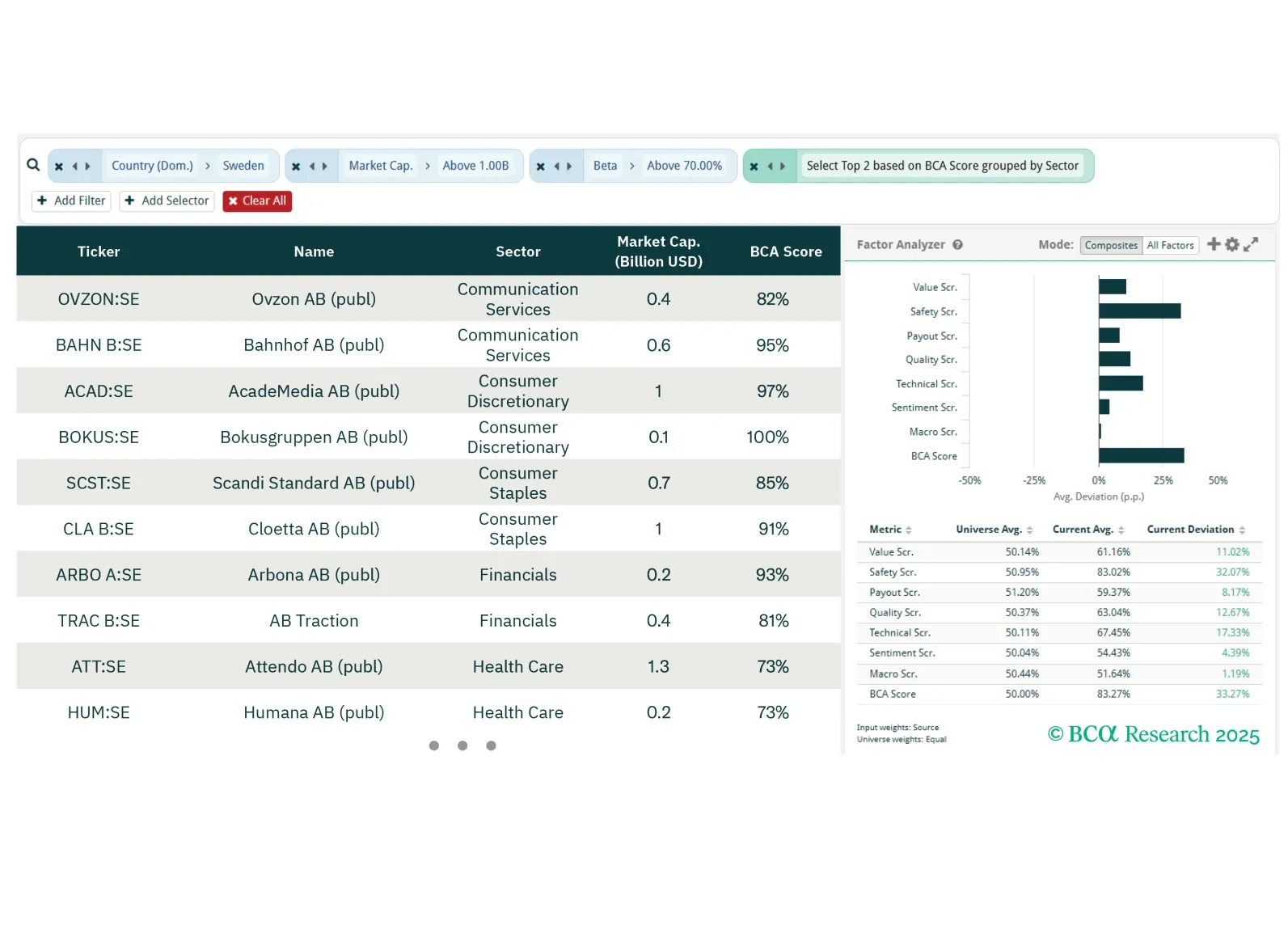

This week, our screeners explore opportunities in the Swedish stock market, Canadian gold-exposed and domestic-focused sectors, and ex-tech GenAI names.

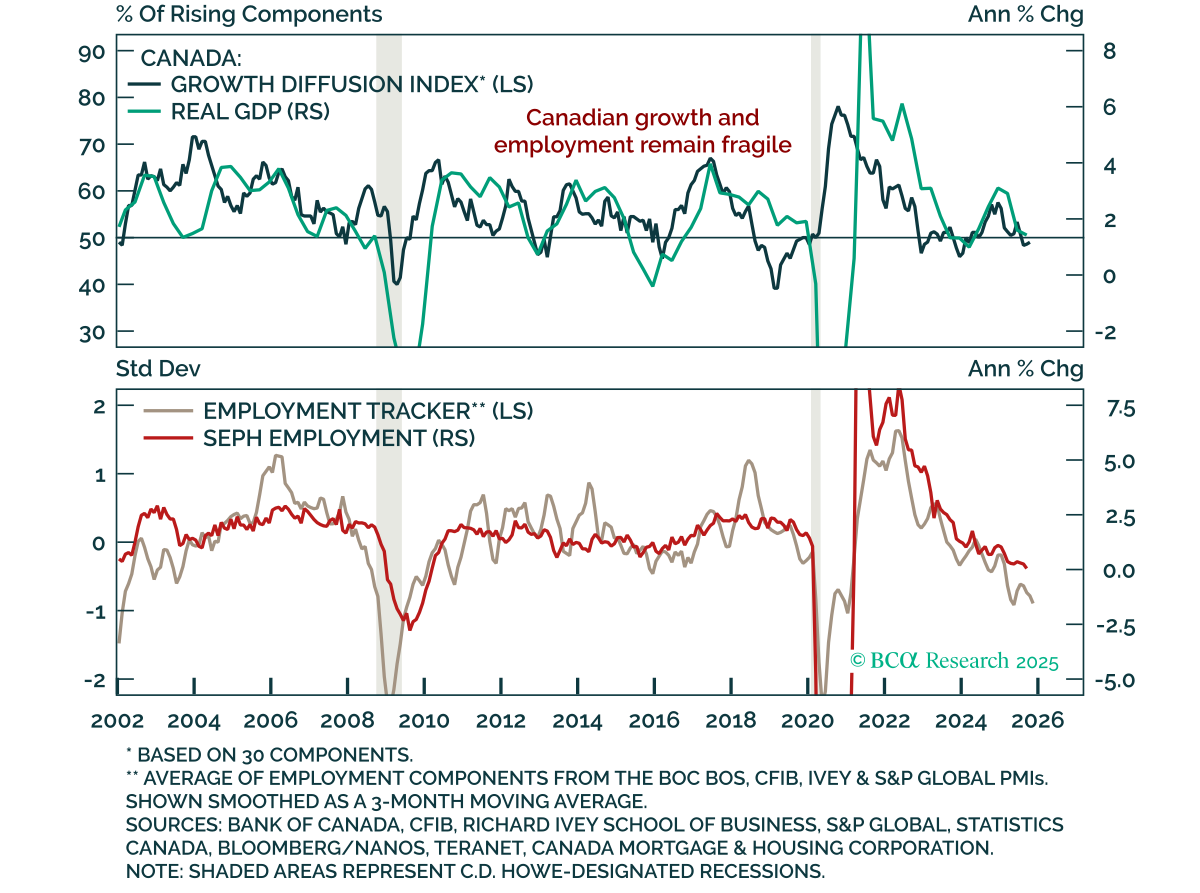

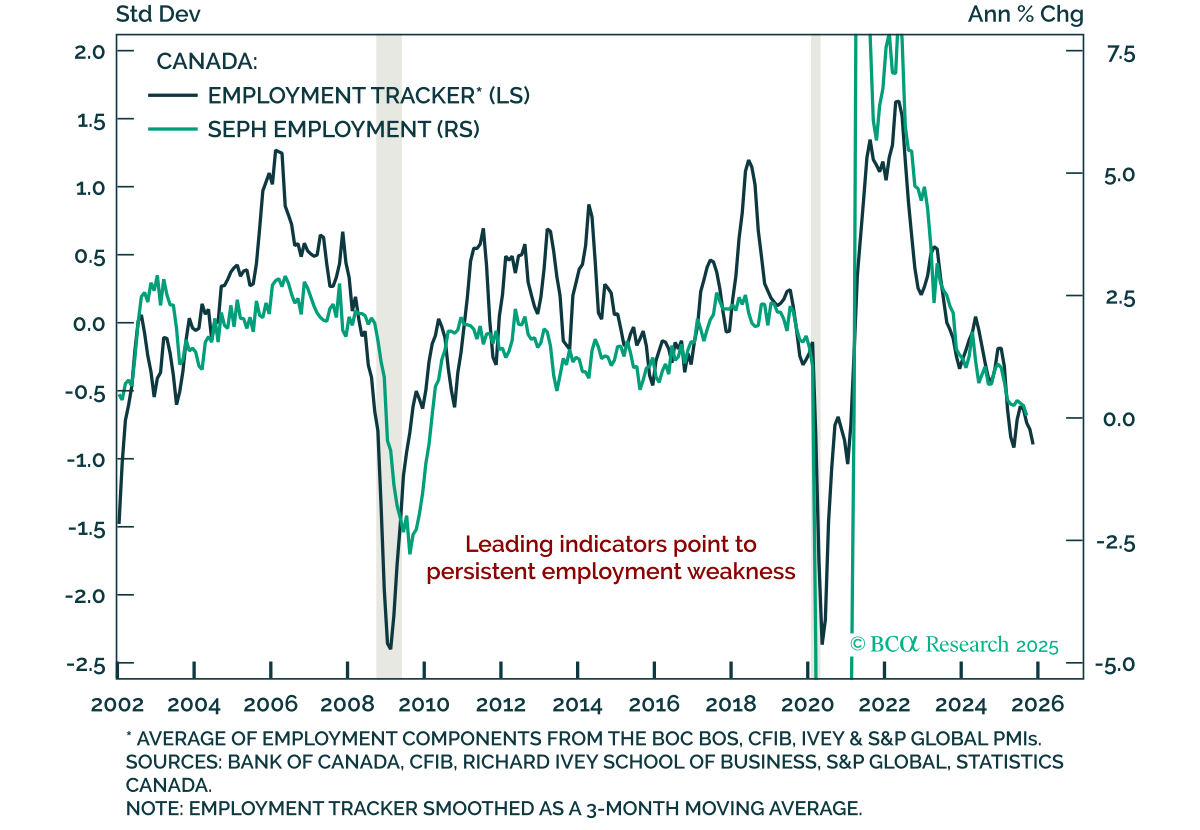

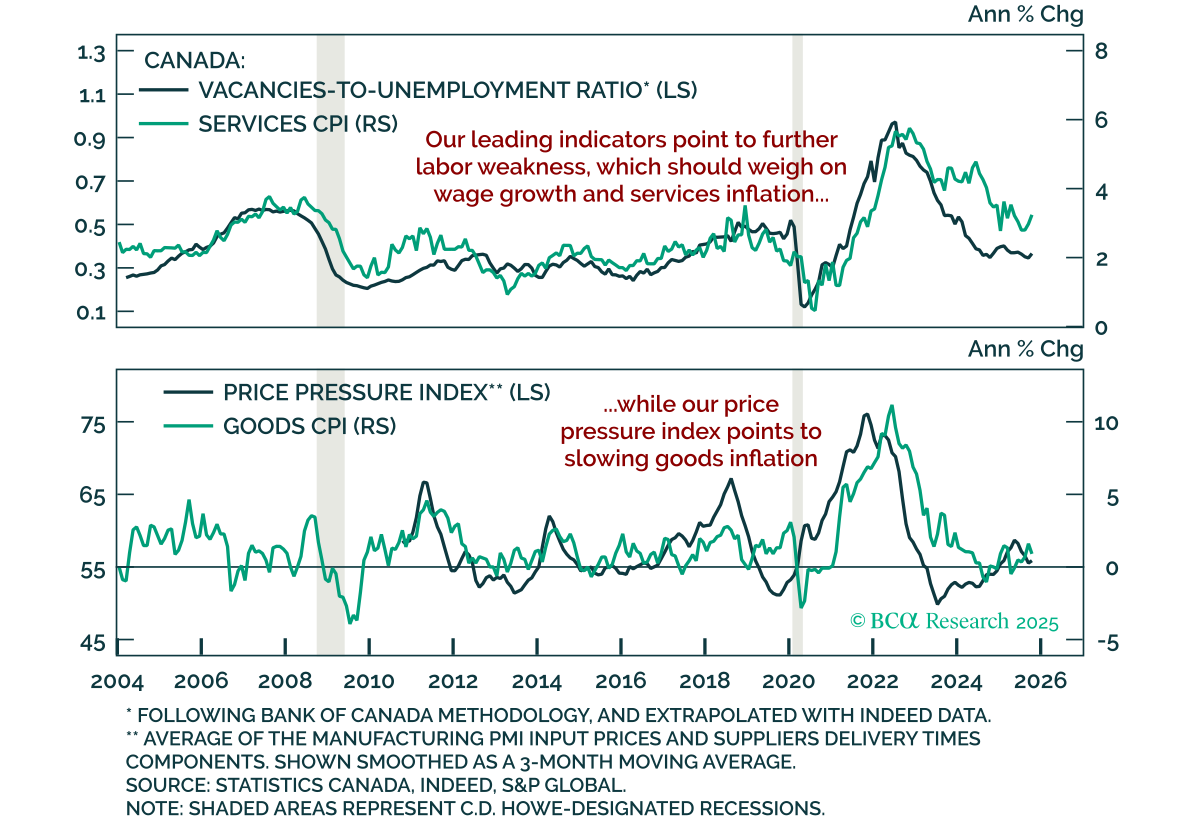

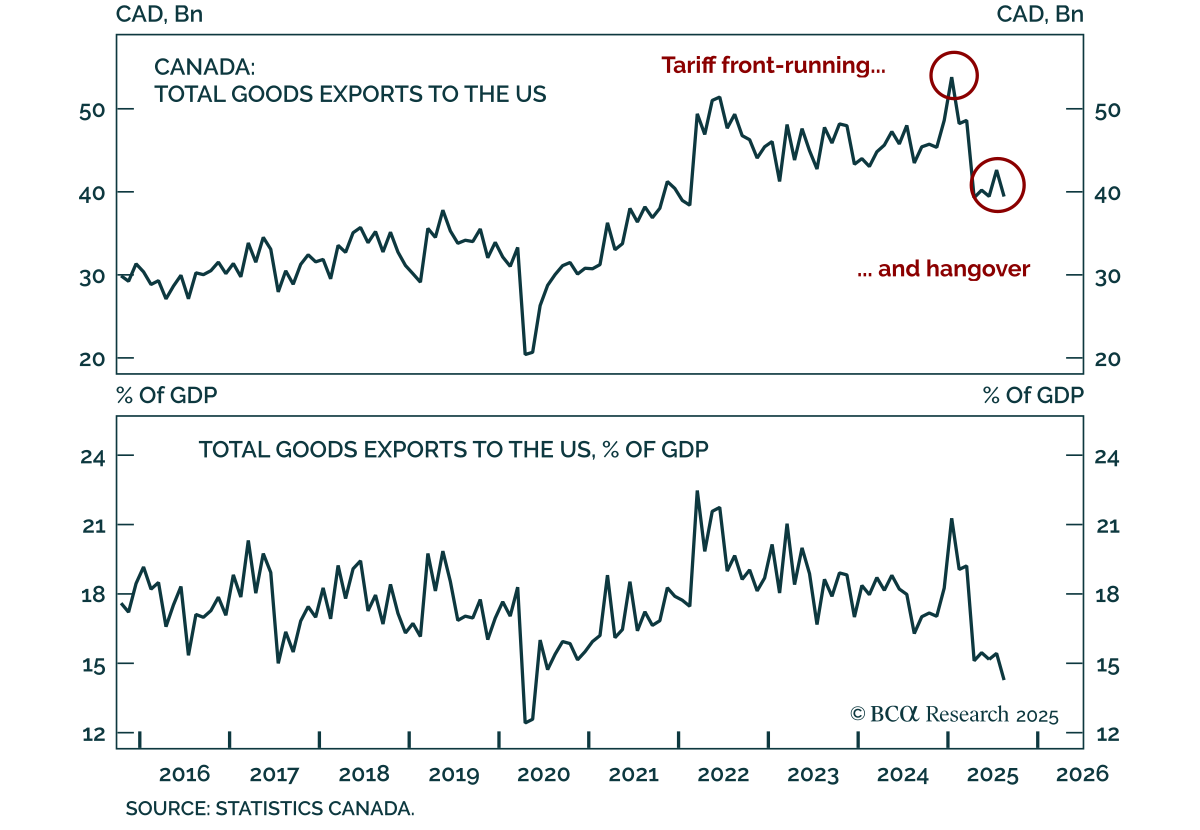

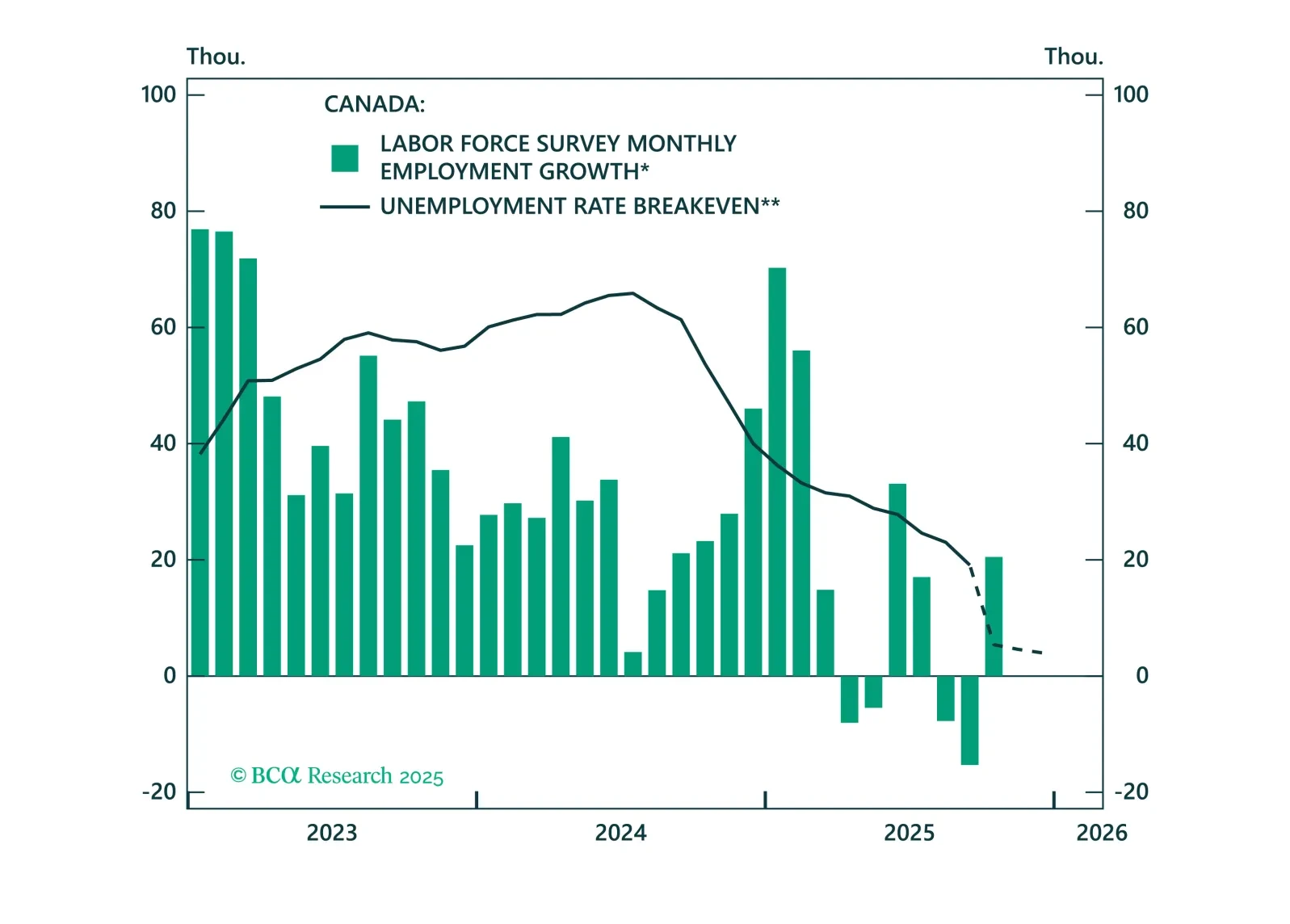

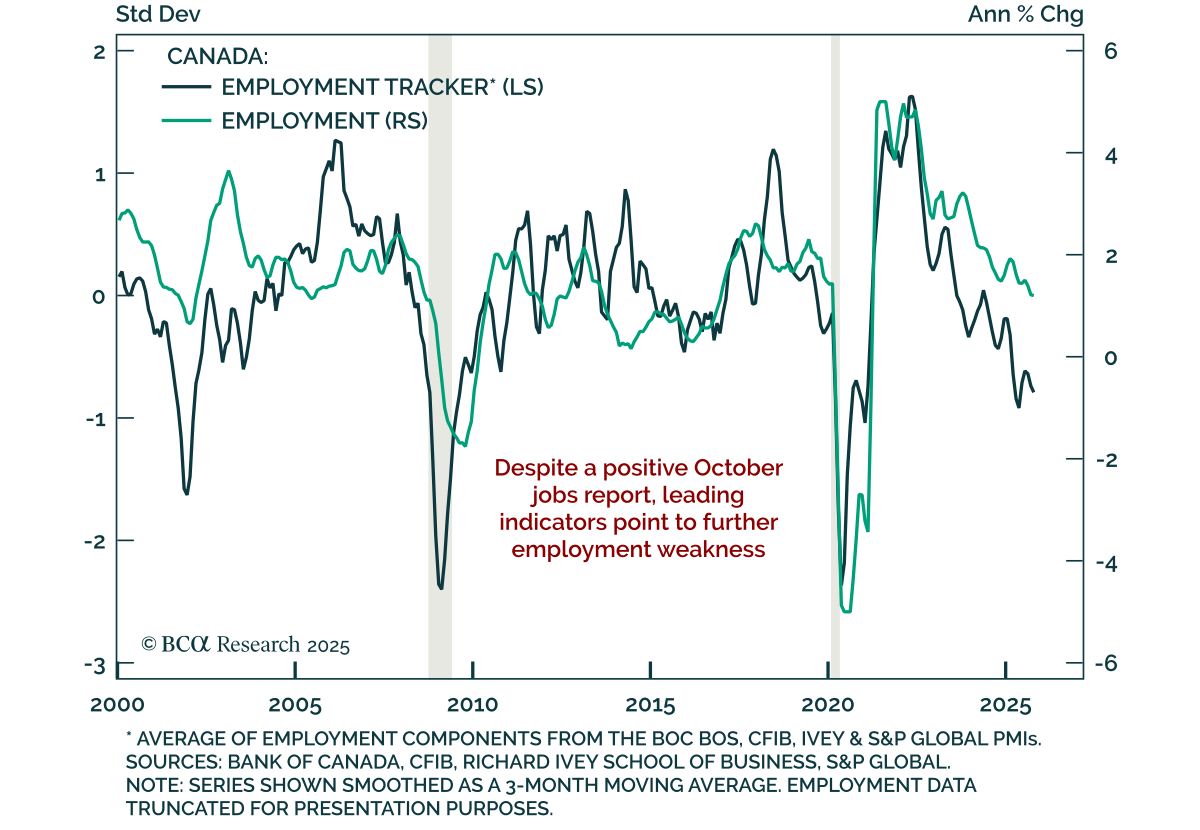

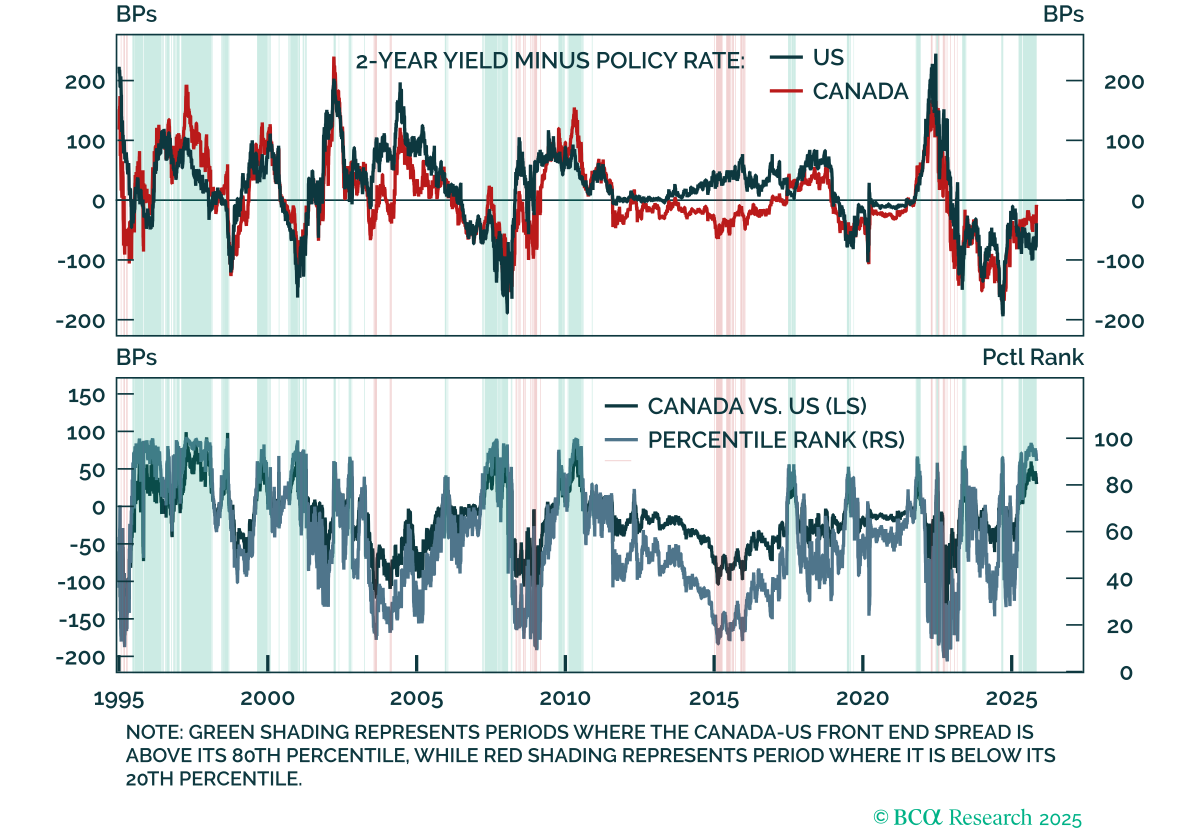

The trade war hit Canada’s economy hard, but the worst is over. In our latest update on Canada, we assess the aftermath of the trade shock, the new budget, and the effects of BoC easing. We outline what this means for duration, the Loonie, and Canadian stocks heading into 2026.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.