Canada

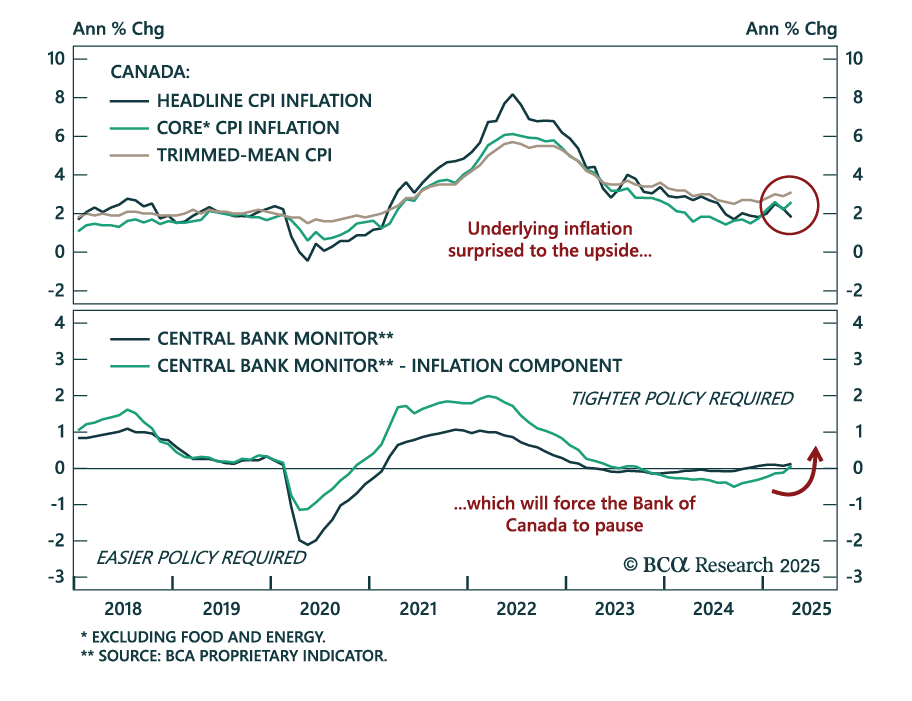

The Bank of Canada may be on hold for now, but deflationary risks are rising fast. Find out why rate cuts may come sooner than markets expect.

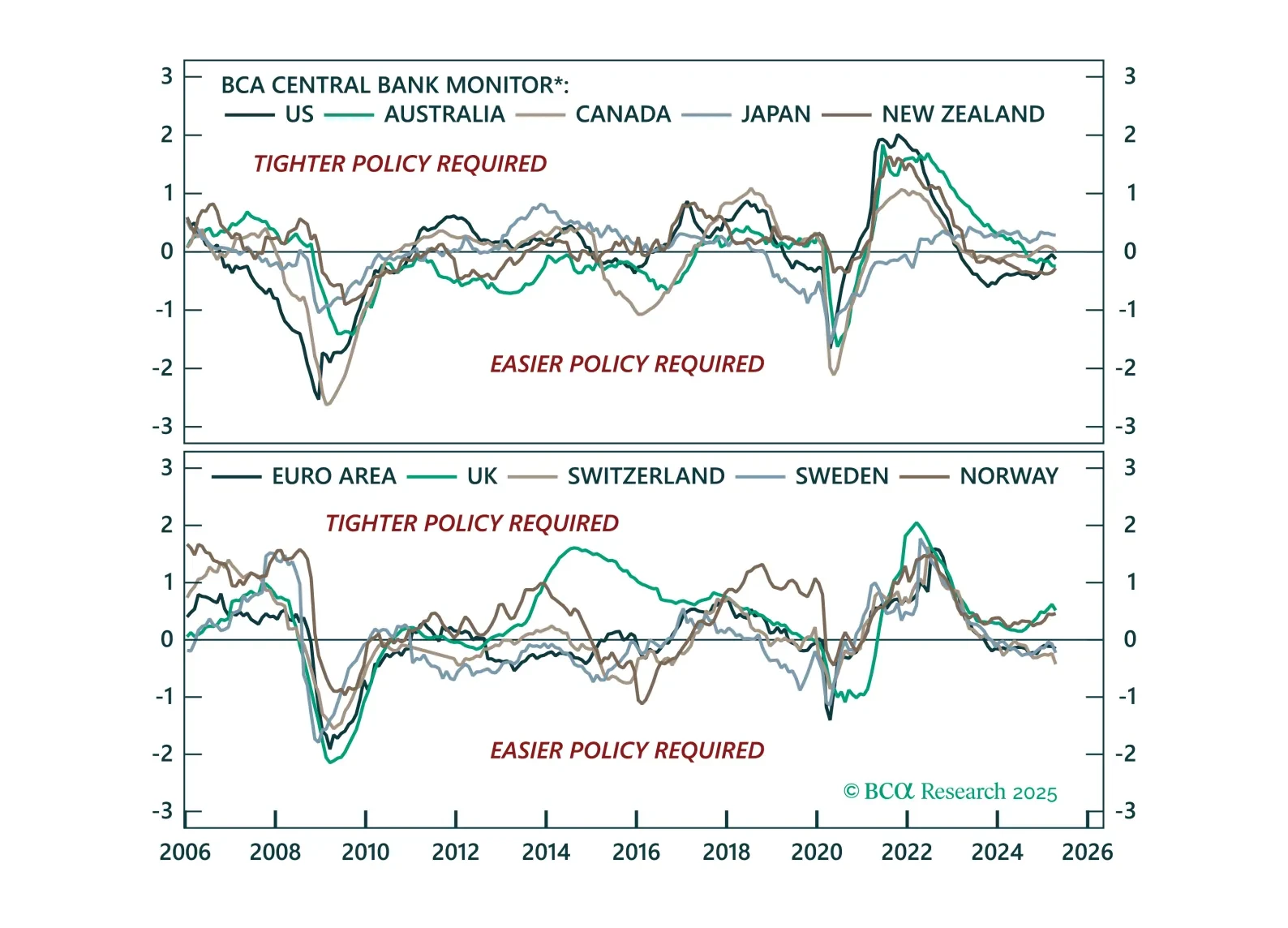

The easing bias remains, but not all central banks are equal. This Central Bank Monitor update reveals who is ready to cut more and who is still pretending not to.

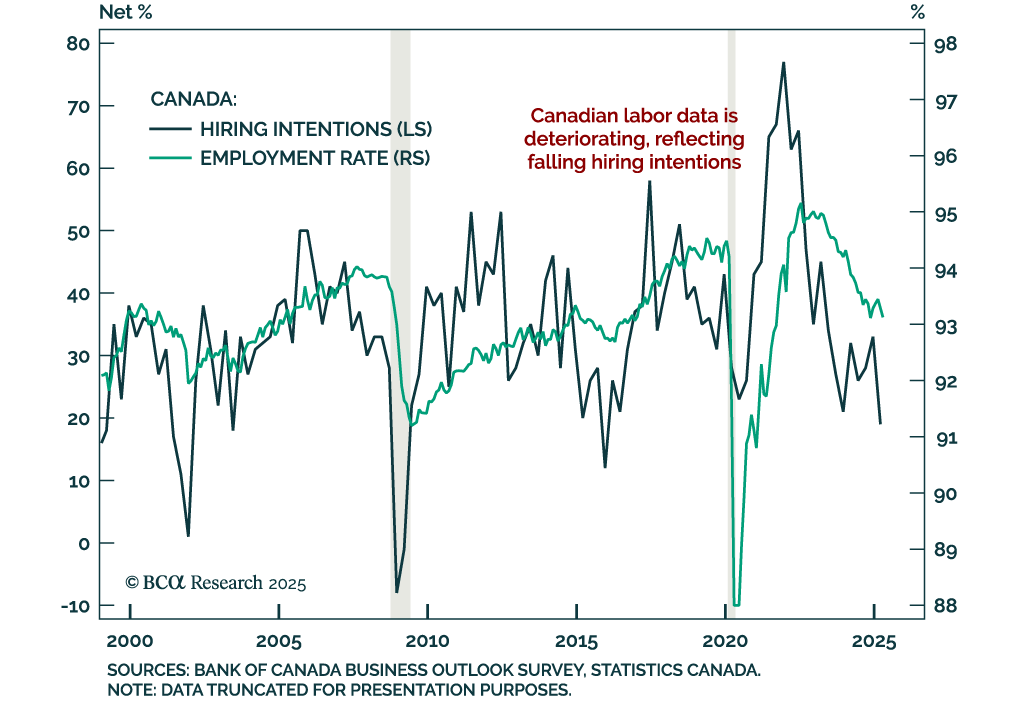

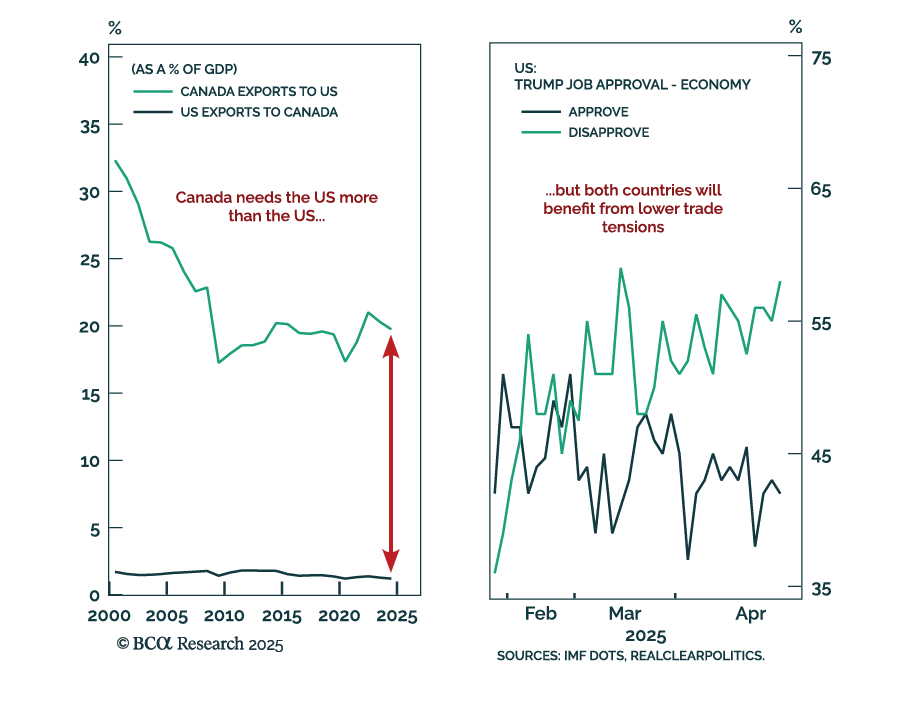

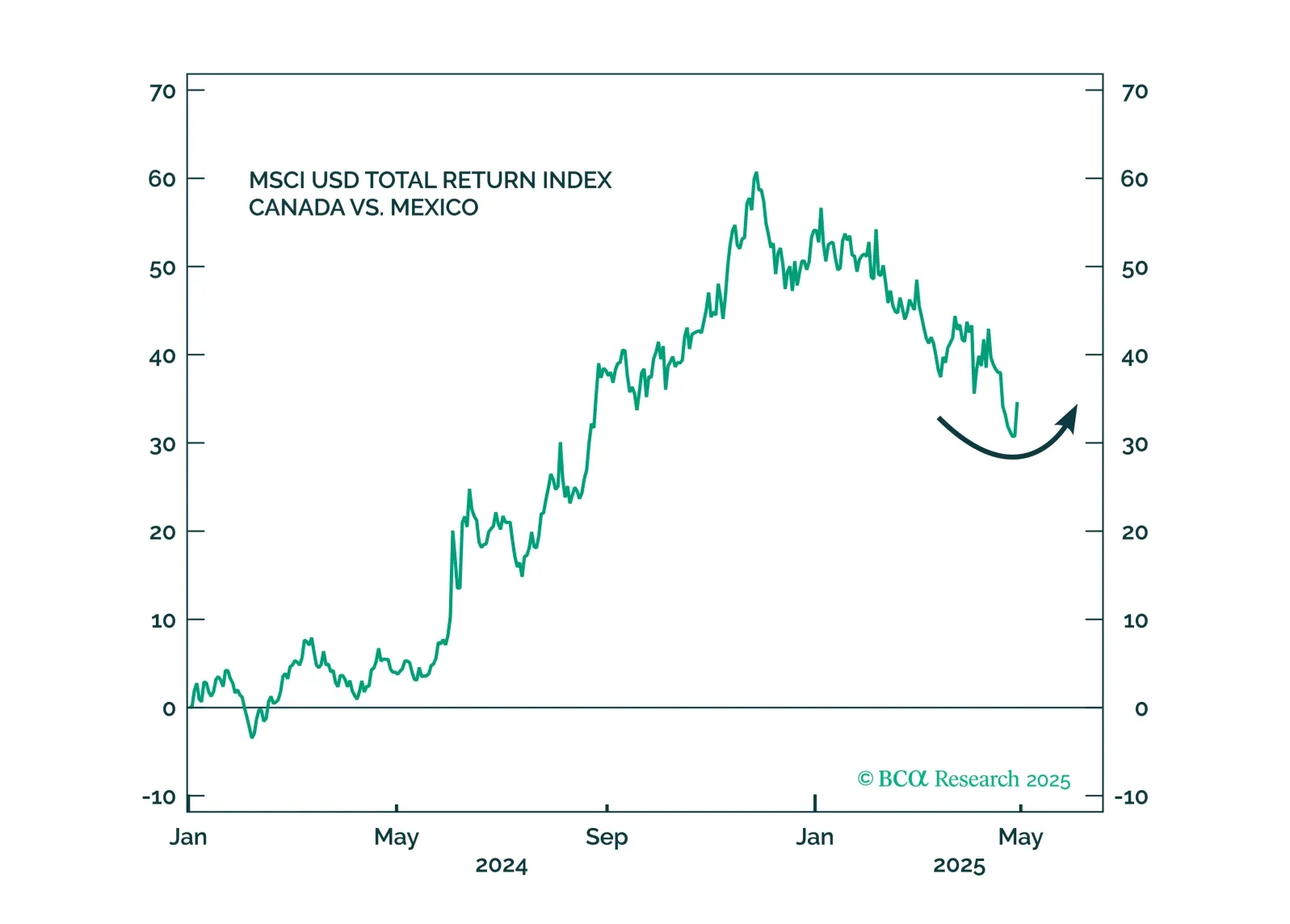

The US and Canada will resolve their trade dispute quickly, leading to a North American deal and better prospects for future relations, as well as for other US trade deals around the world. But even as tariff threats decline, the US economy will slow, weighing on its neighbors. Canada will fare better than Mexico.

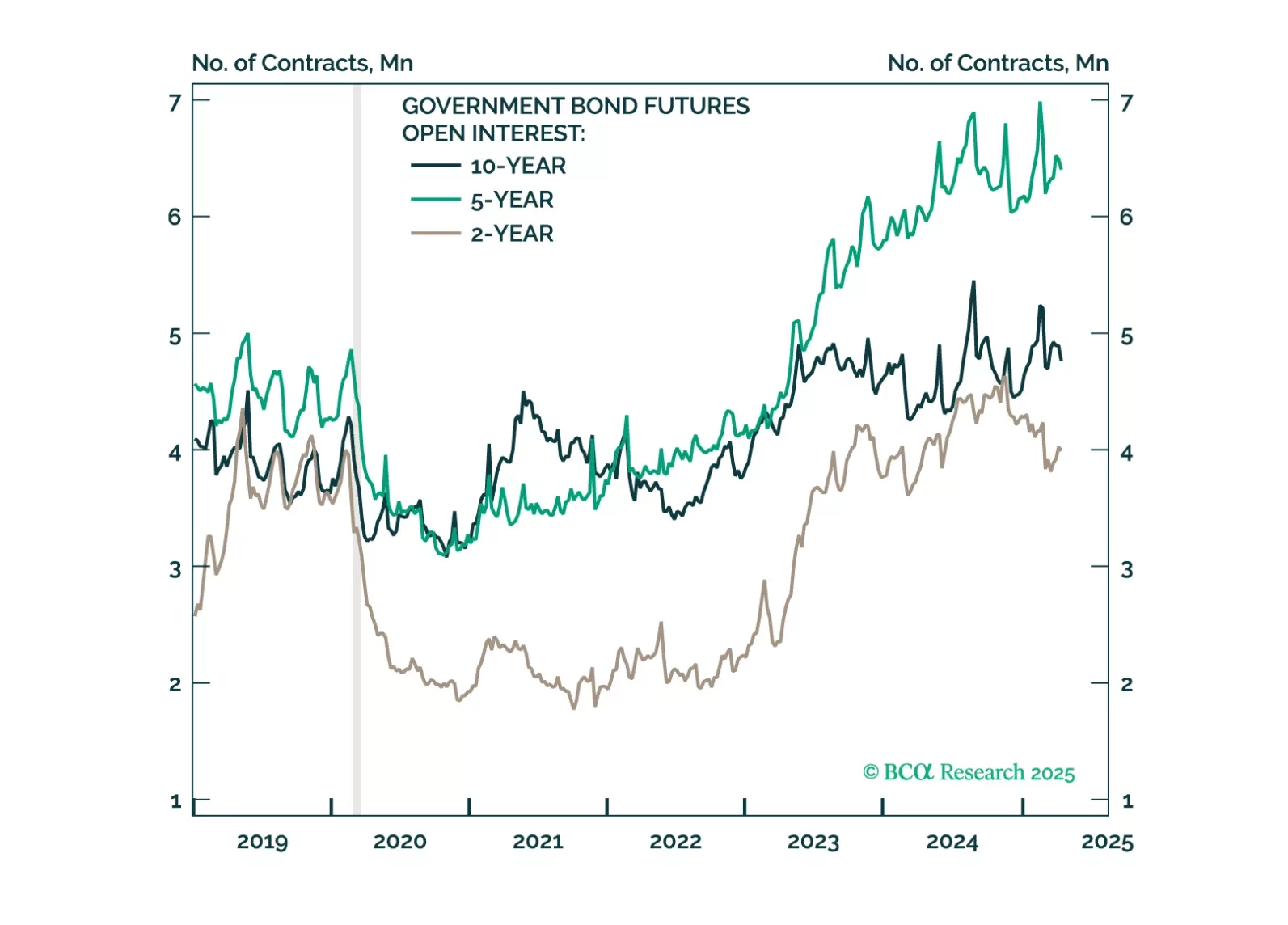

US Treasuries typically outperform both equities and global government bonds during downturns. Recent political shifts could lessen that outperformance this cycle, but we doubt it will disappear completely.

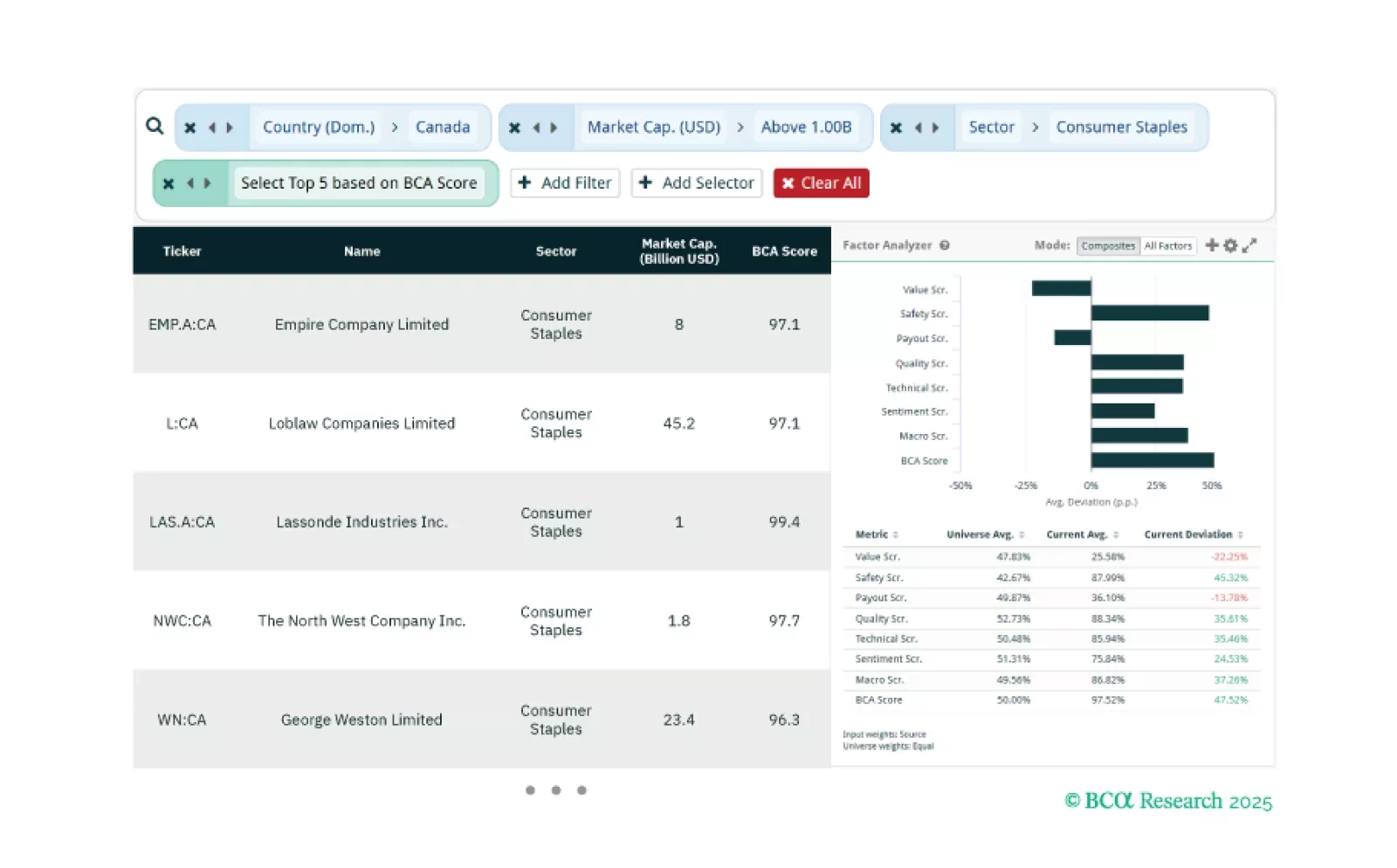

This week, our three screeners cover equity plays in: Canadian Consumer Staples, high-beta Swedish equities, and factor plays across global equities.