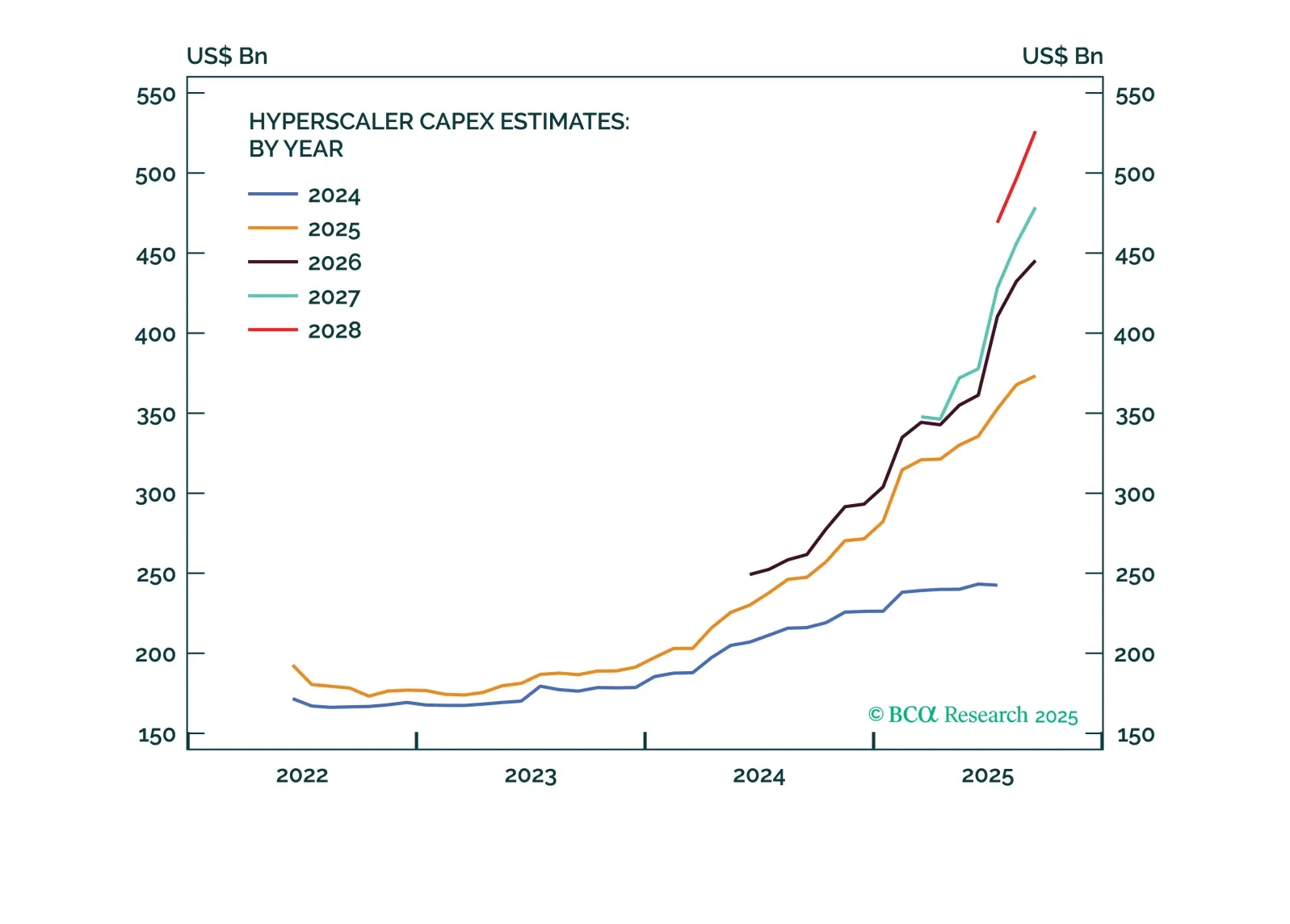

Capex

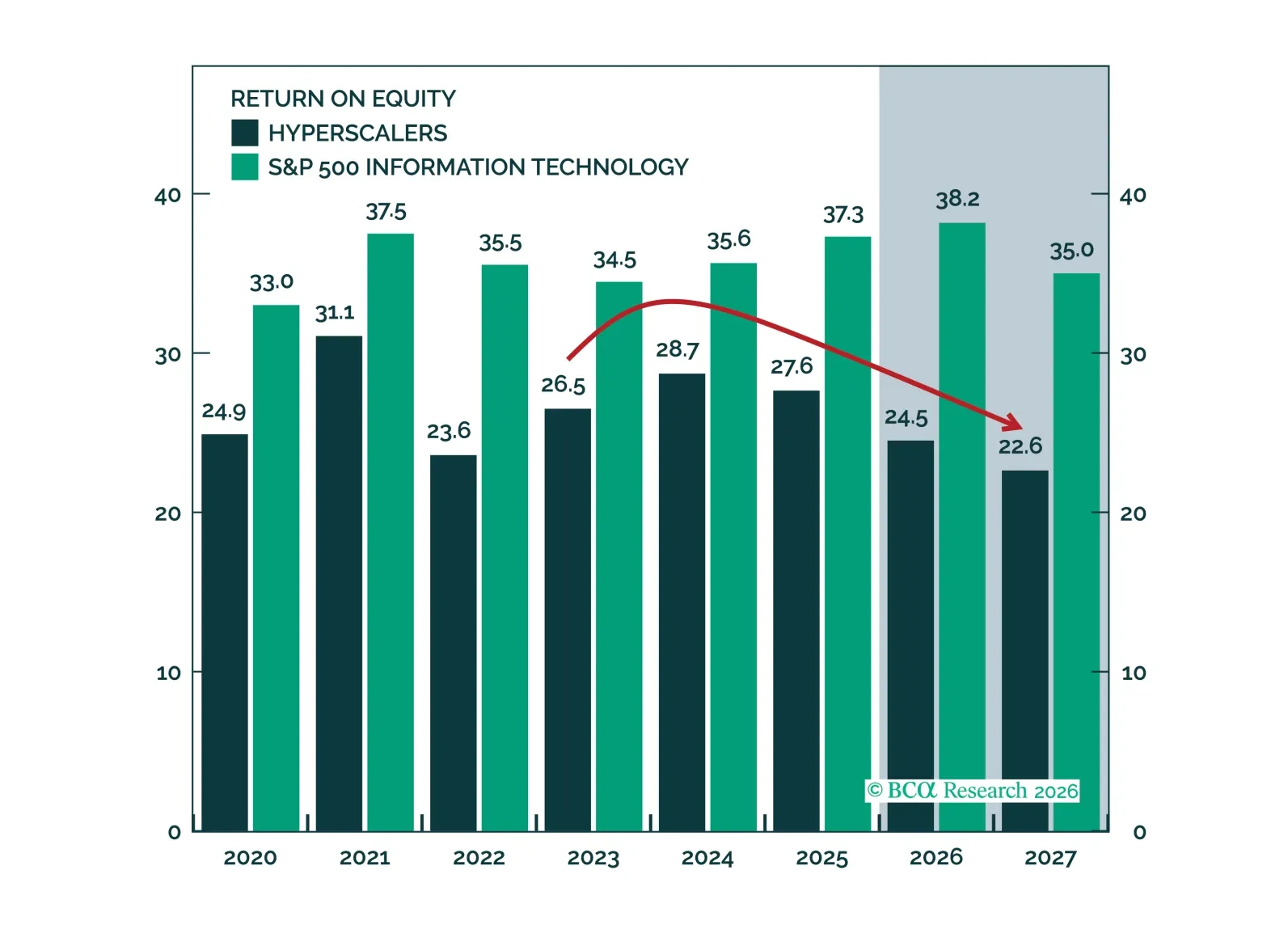

The capex debate is better framed not as boom versus bubble, but as around capacity, leverage, and cash conversion. ROEs have compressed, but revenue growth and margin expansion offer a credible path back. Spenders likely have time to make good on their investments, though the market’s leash may be shorter than anticipated.

The US residential real estate market remains soft. While the decline in mortgage rates is a positive, it is too early to bet on housing becoming the engine of growth for the US economy this year.

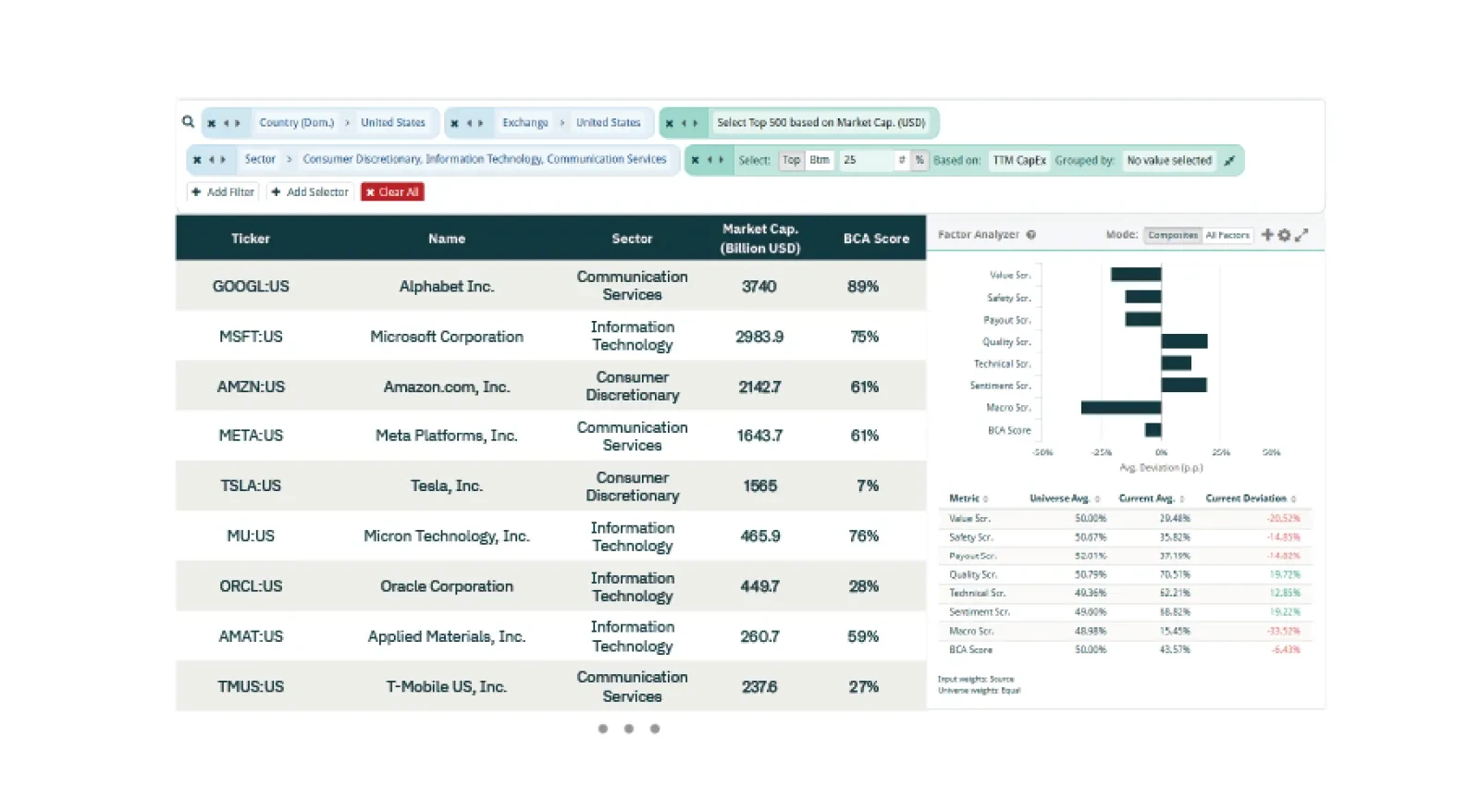

For this screener report, we explore opportunities in a CapEx premium divergence trade, a valuation convergence trade, and European Defense Stocks.

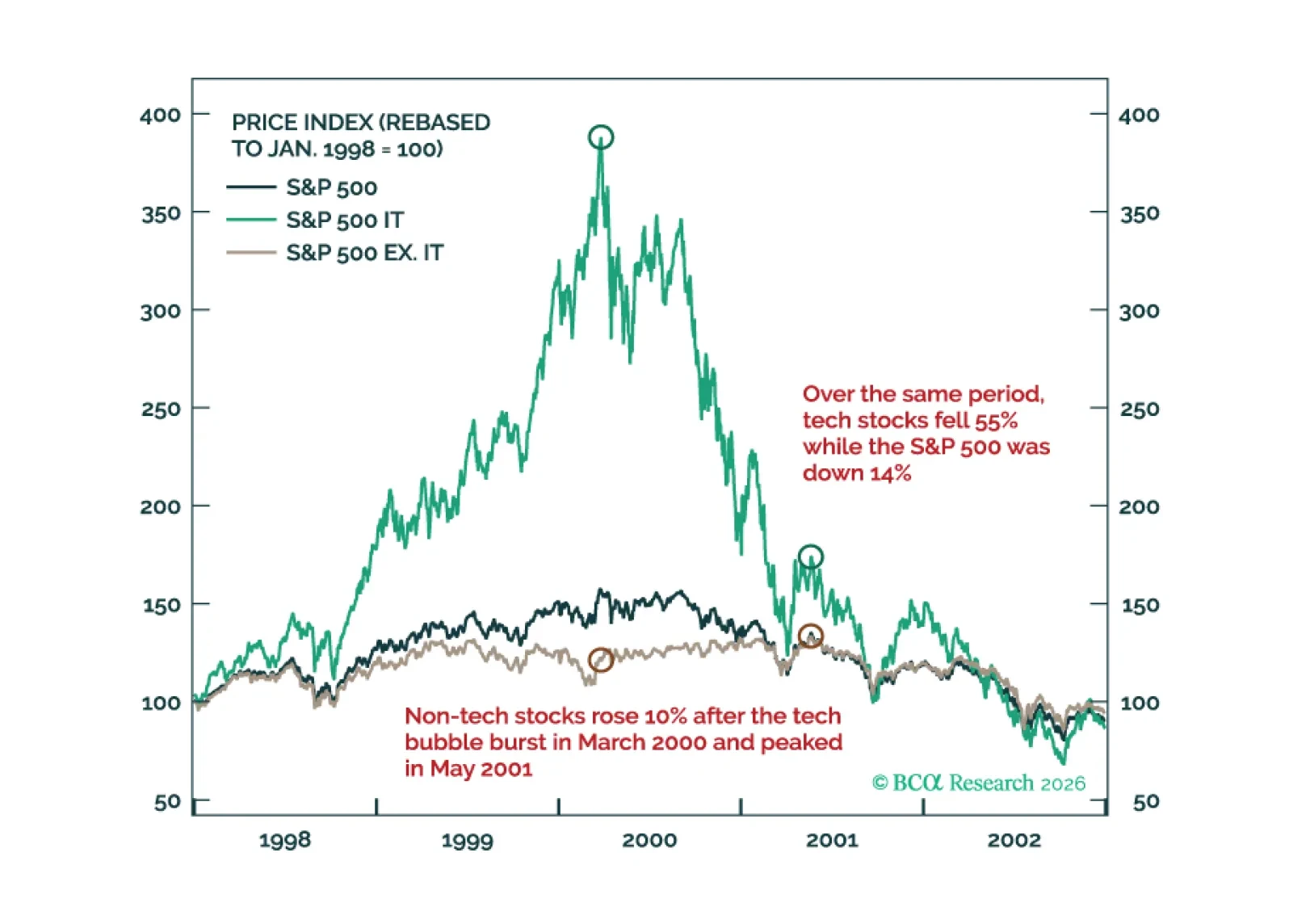

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.

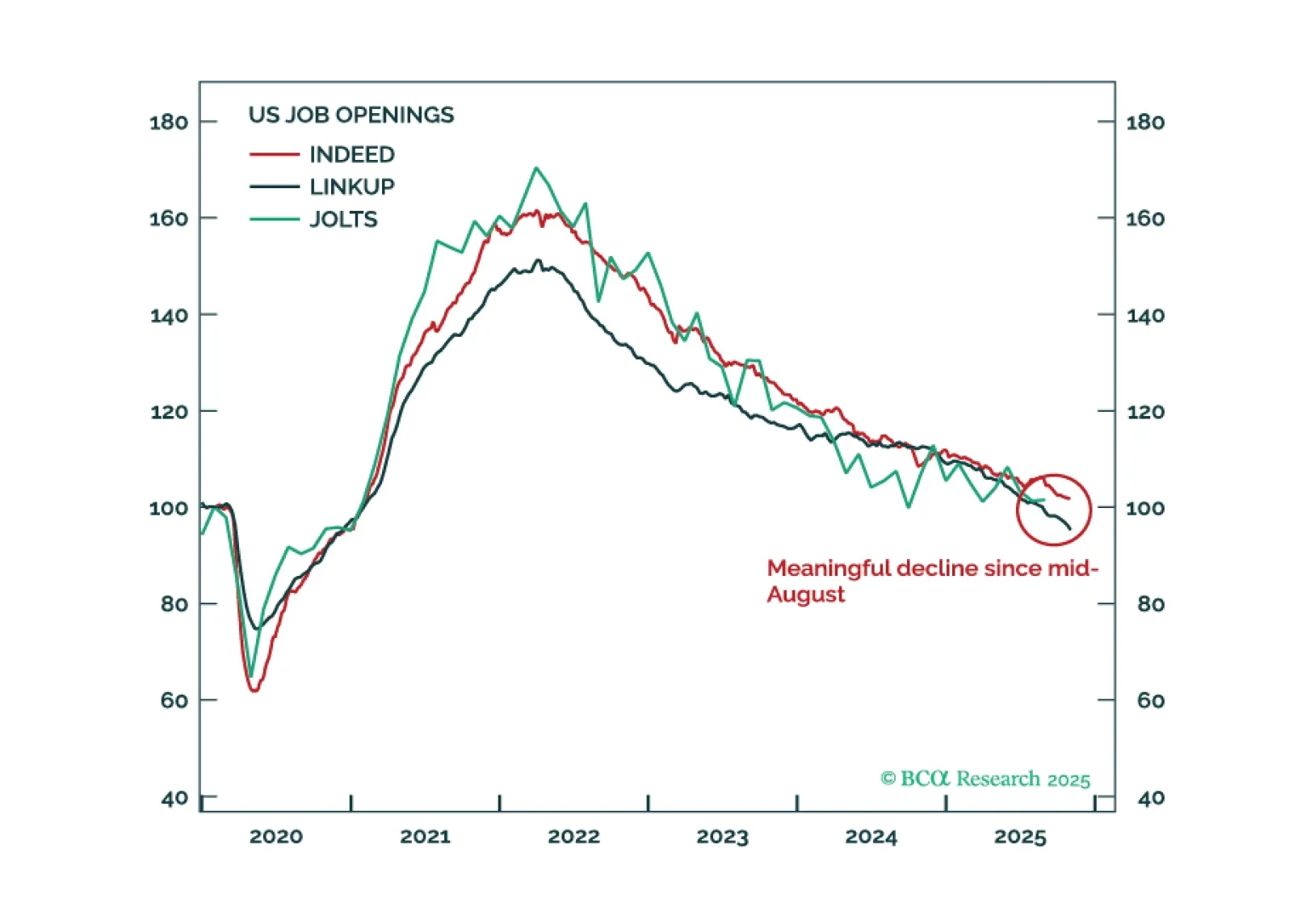

In the absence of official government data, investors are turning to alternative sources to gauge the direction of the US economy. Our analysis of this data suggests that the economy has continued to expand at a moderate pace over the past two months. If the Supreme Court were to strike down the tariffs, this would reduce the near-term odds of a recession while raising the odds of overheating.

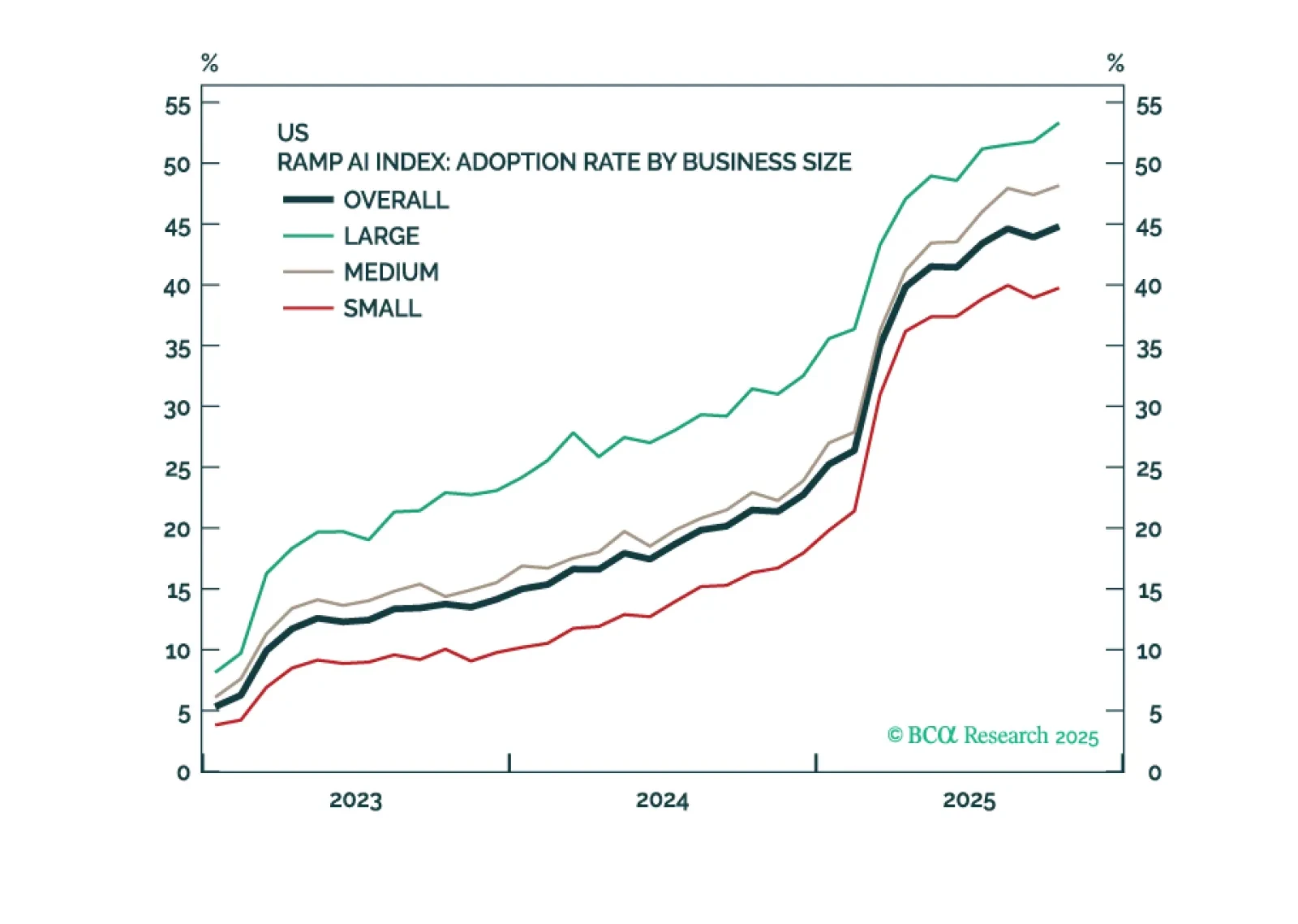

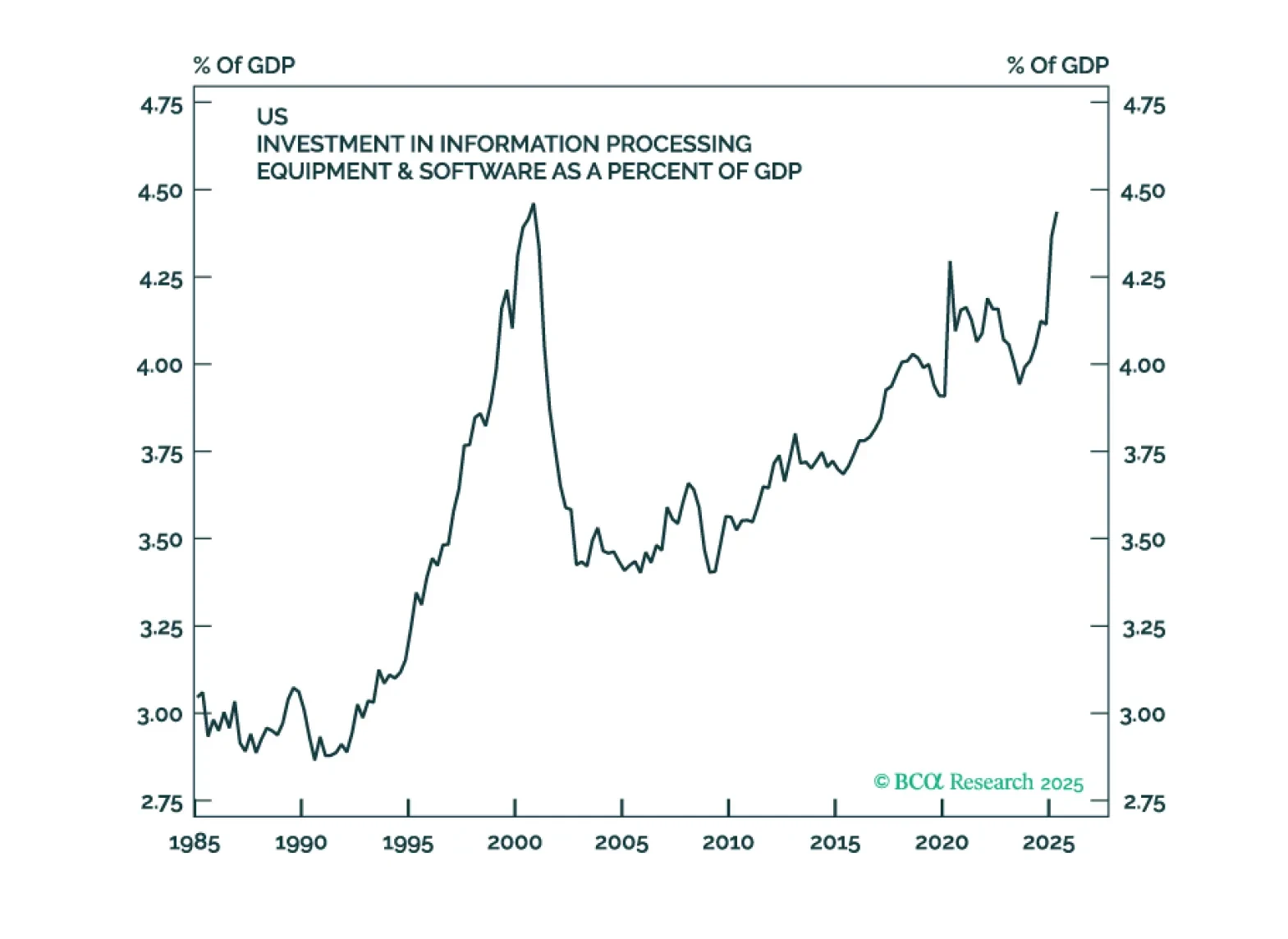

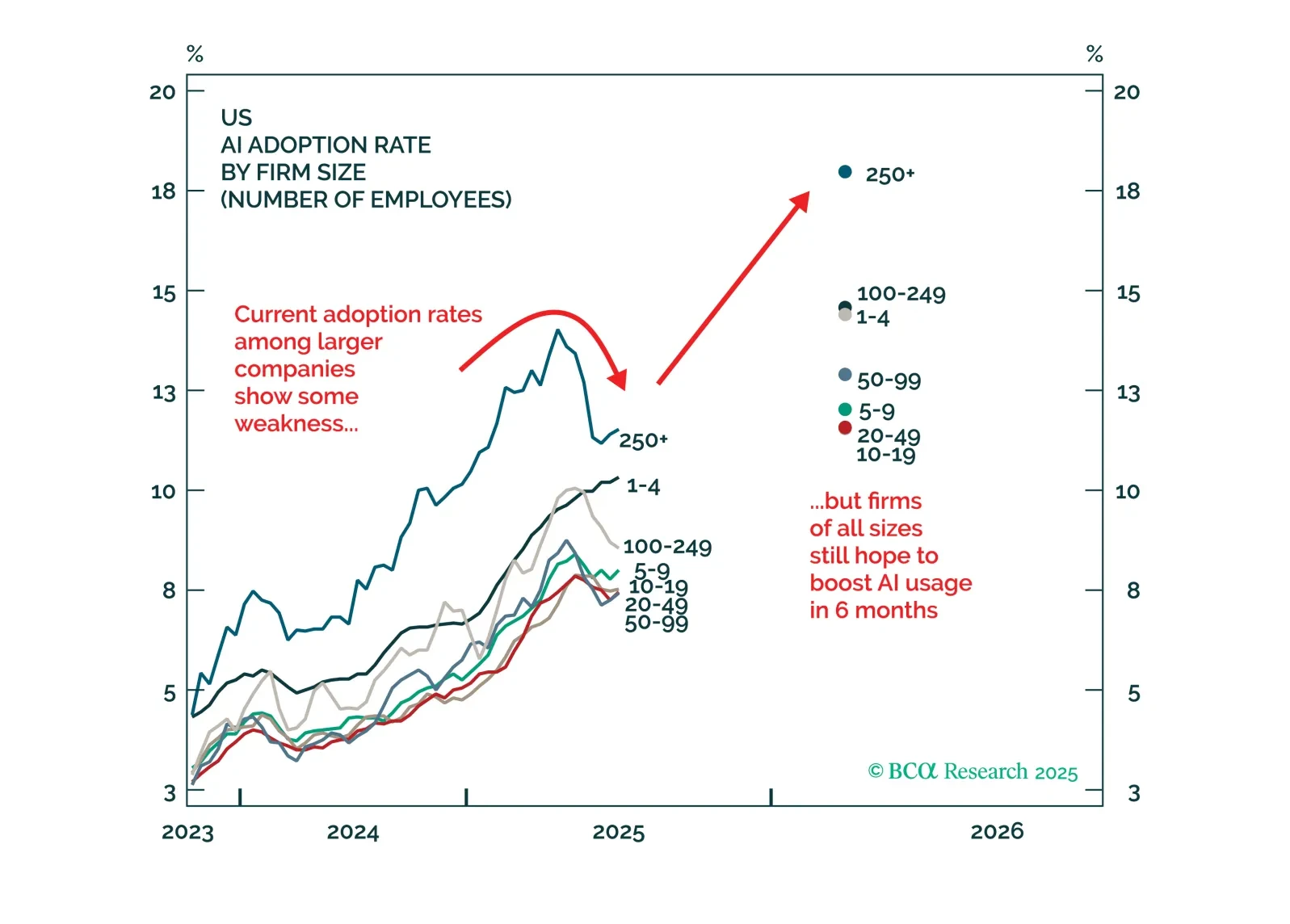

Fresh off a month of boning up on all things AI, we walk through a high-level Q&A discussing AI capex and how much the AI investing boom is really contributing to US growth.

The rush to build AI infrastructure is based on a false premise: that there are significant advantages to being the first to come to market.