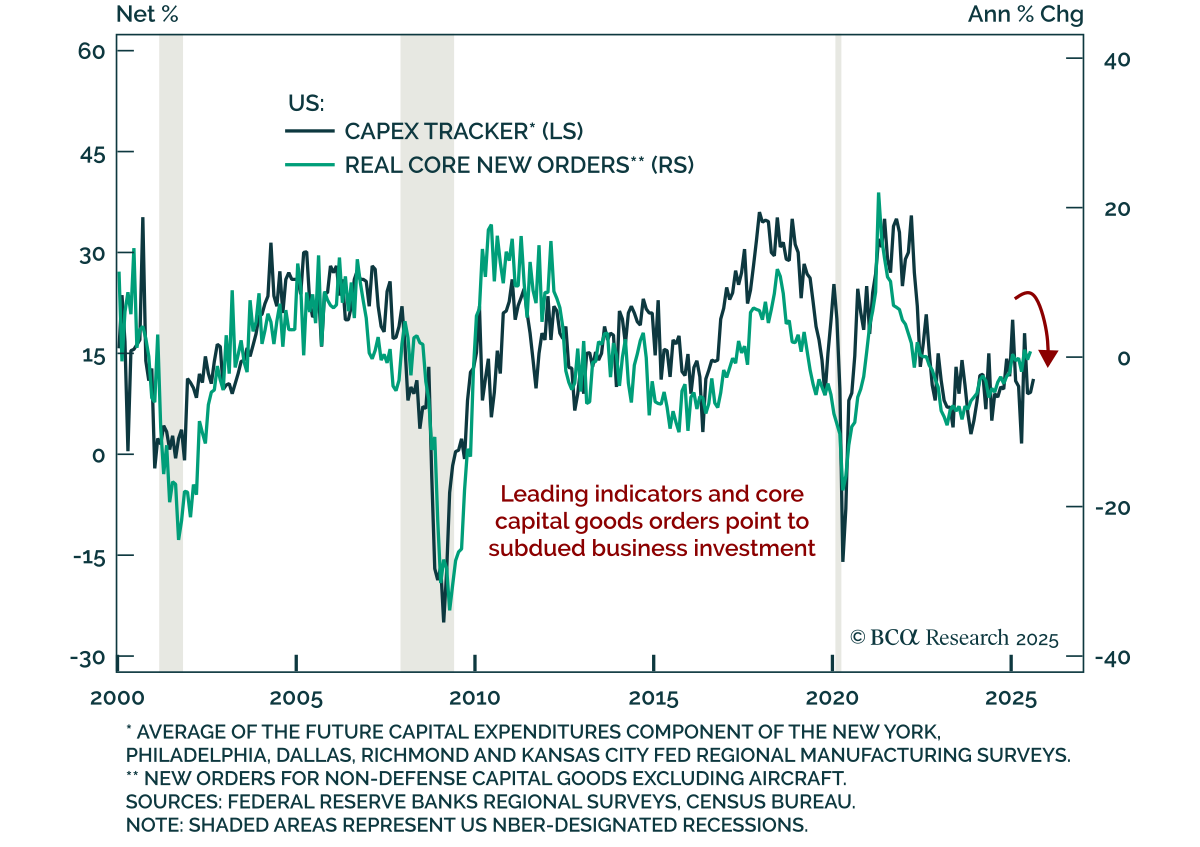

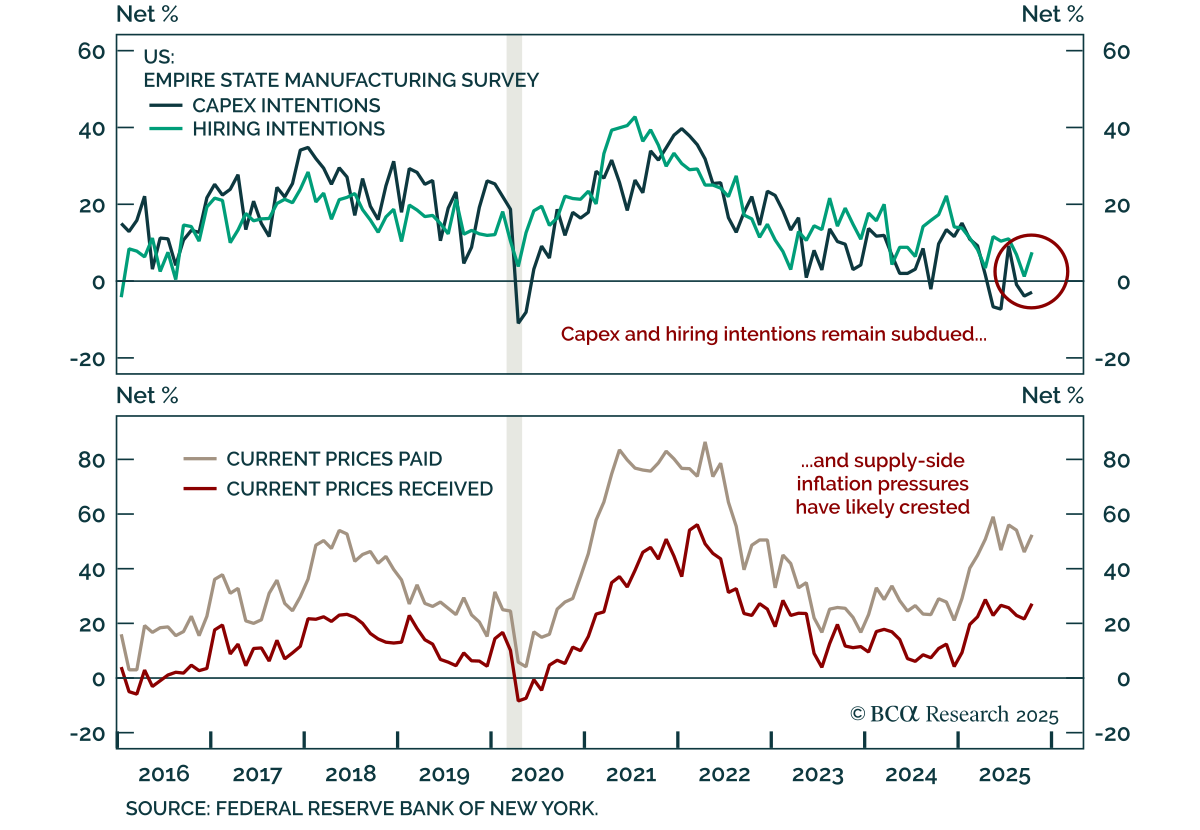

Capex

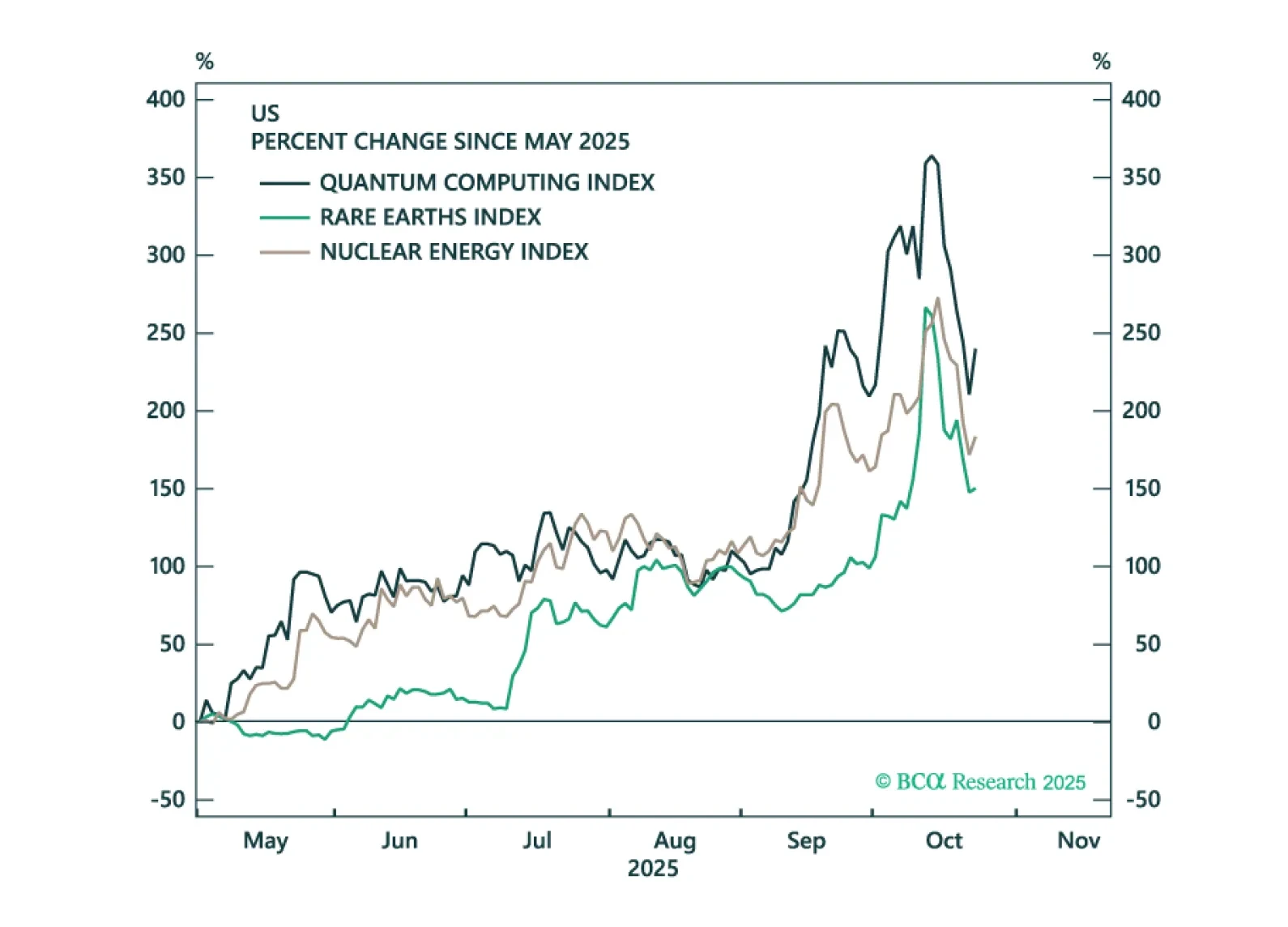

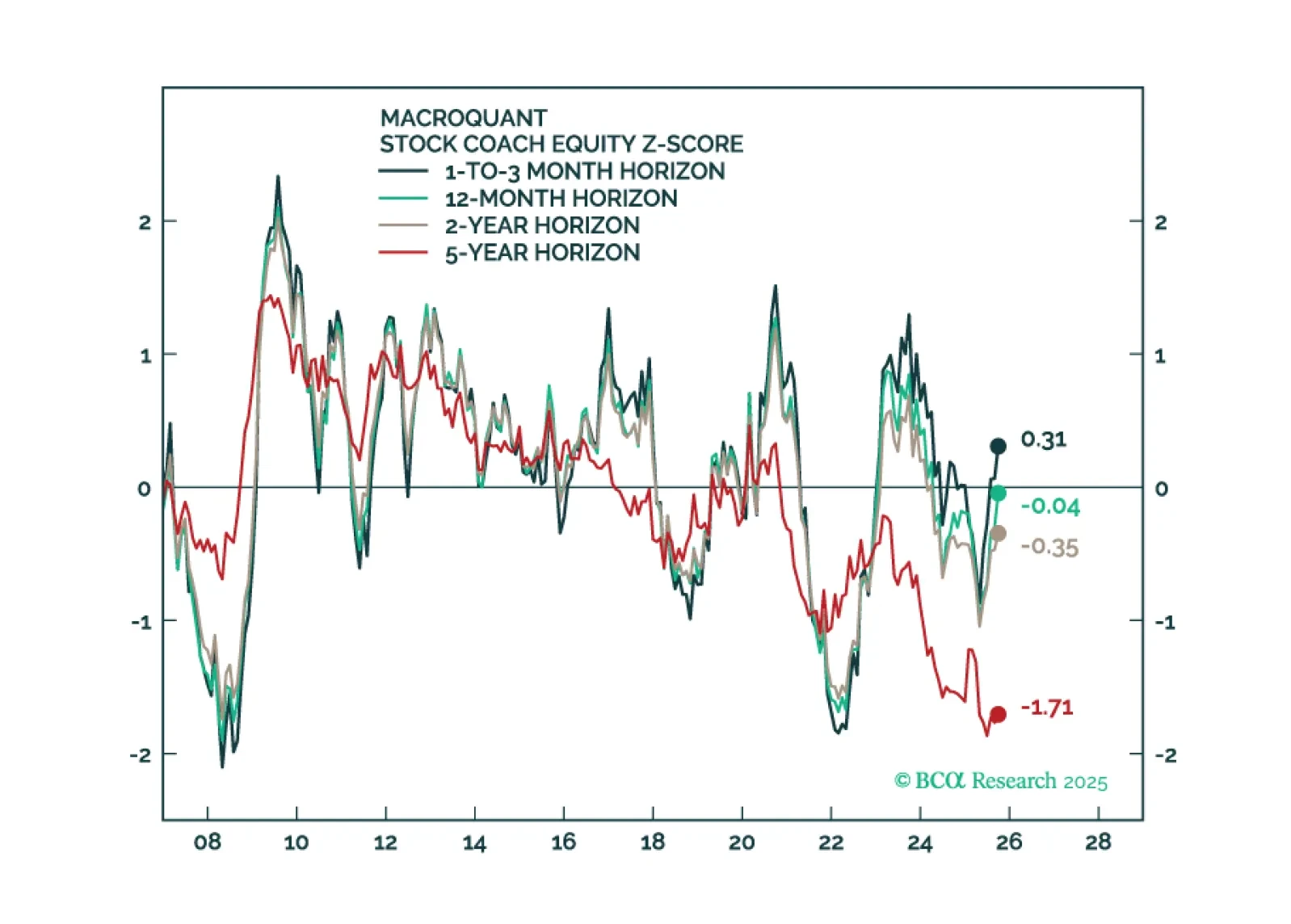

Precious metals, corporate credit, and tech stocks are all showing signs of late-cycle euphoria. We identify various trigger points that investors should monitor to turn more bearish.

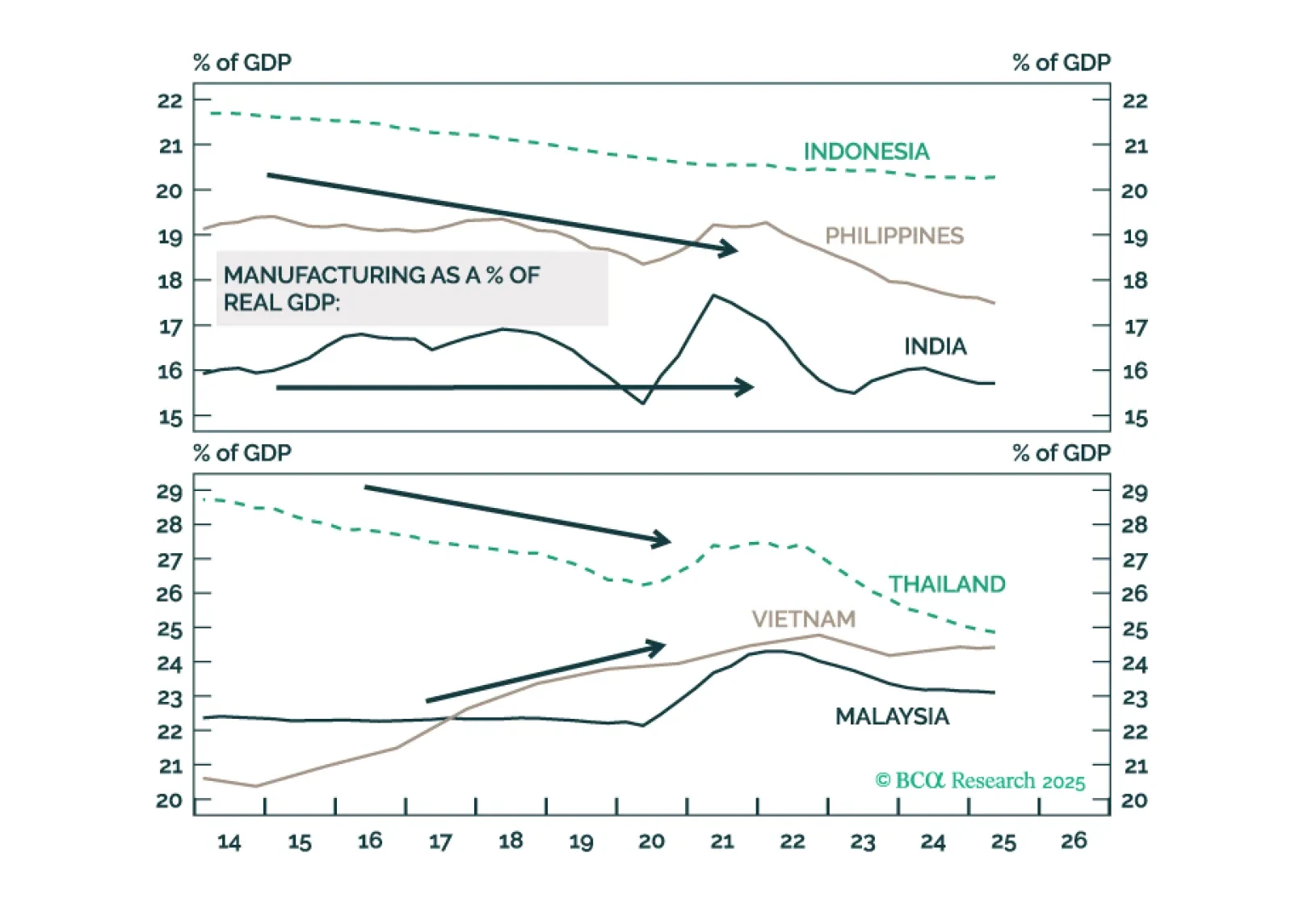

Investors should not count on buoyant growth in the ASEAN and Indian economies because of manufacturing relocation away from China in the next couple of years.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

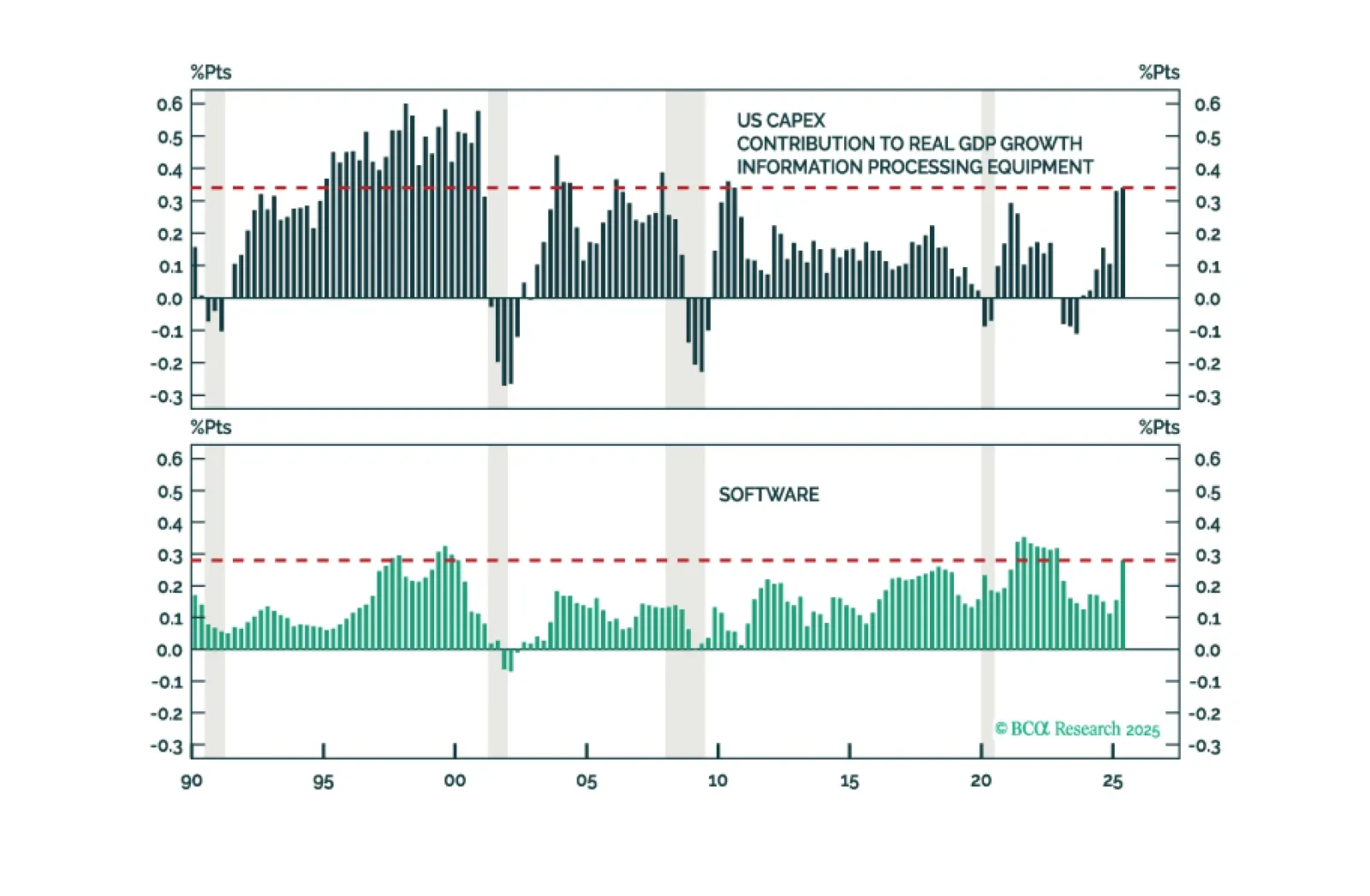

The AI capex boom is having a measurable impact on the economy but, so far, it is more muted than often cited.

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.

Although our recession conviction has risen, we conclude our strategy review by closing our equity underweight and our fixed income and cash overweights. AI momentum is too strong to have anything more than modest exposure to an equity decline via a small SPY put position.

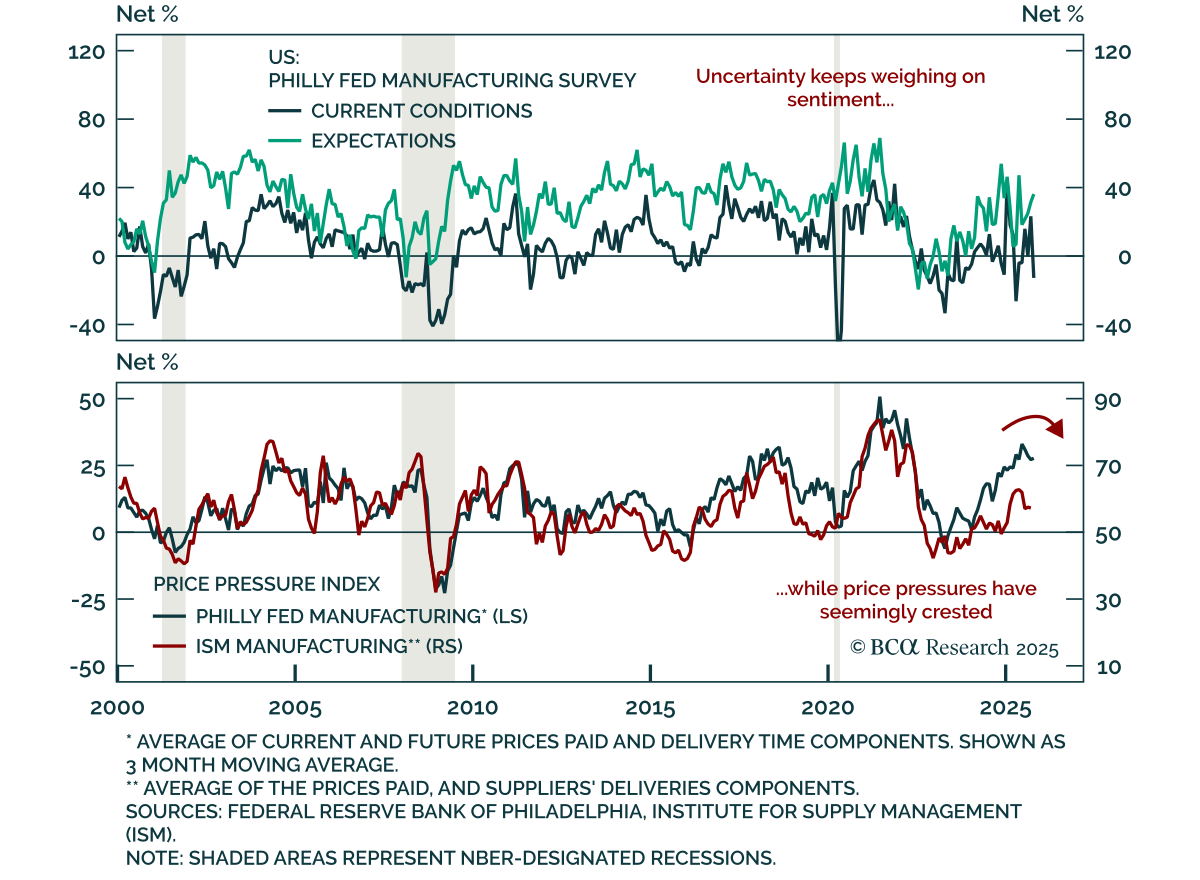

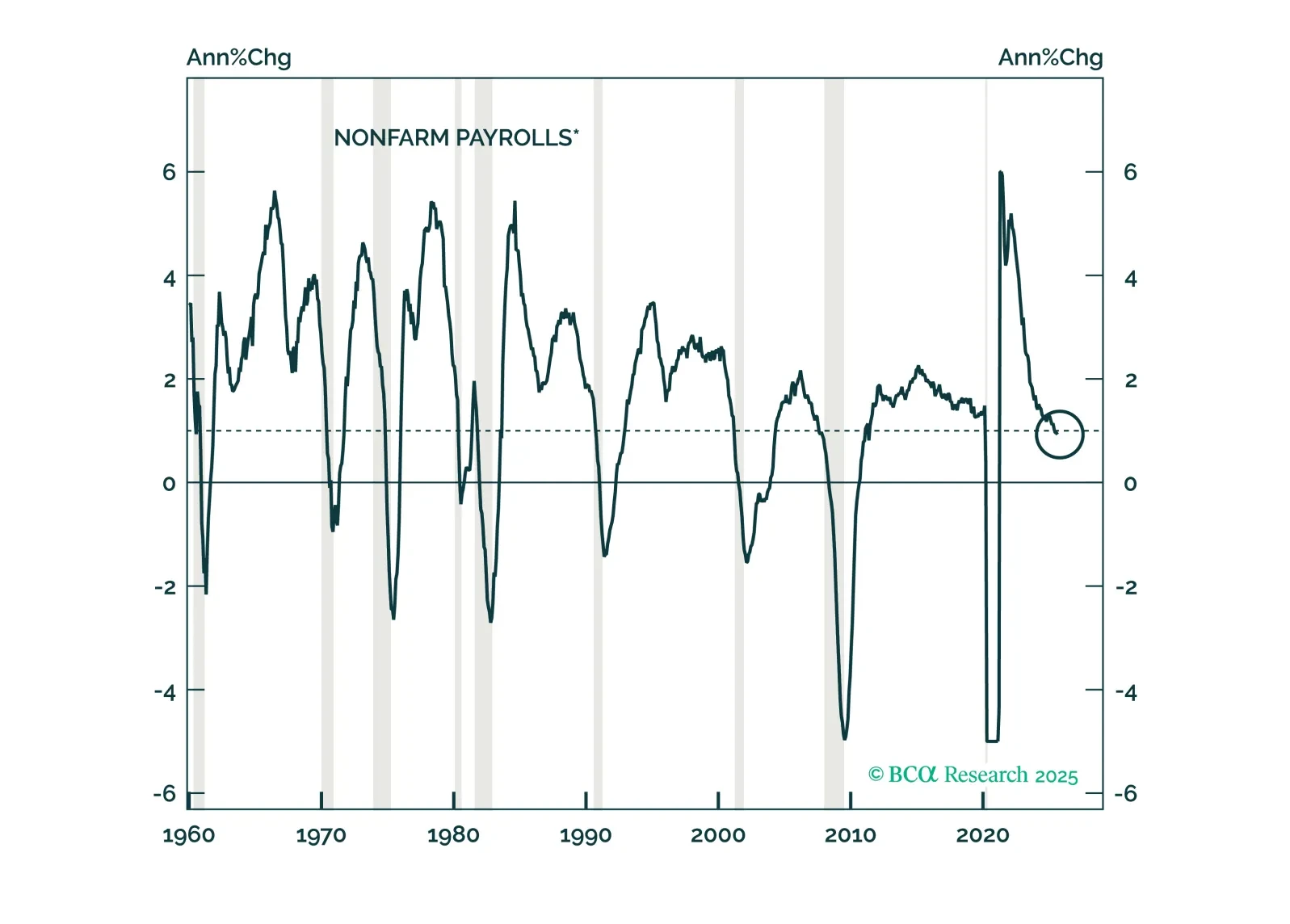

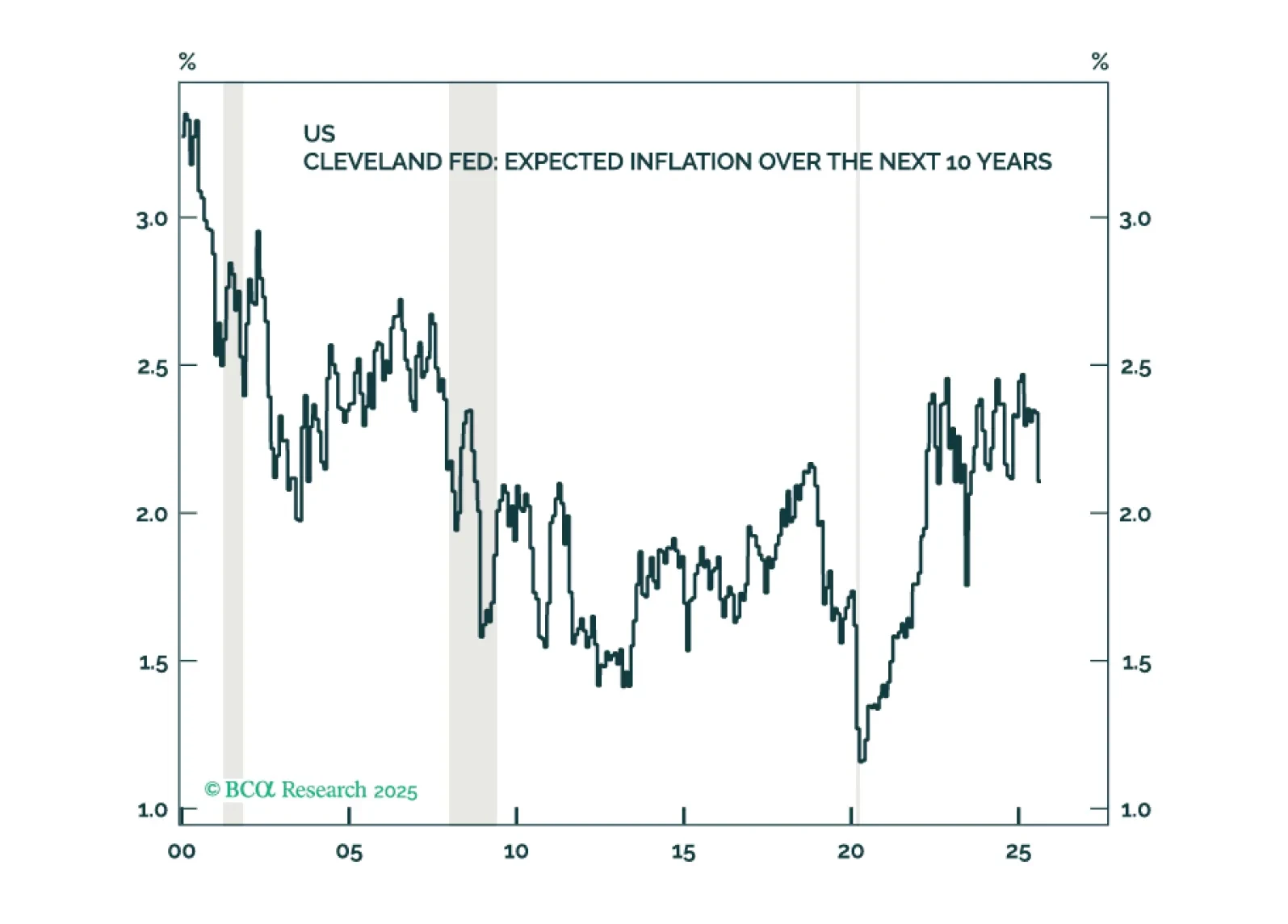

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.