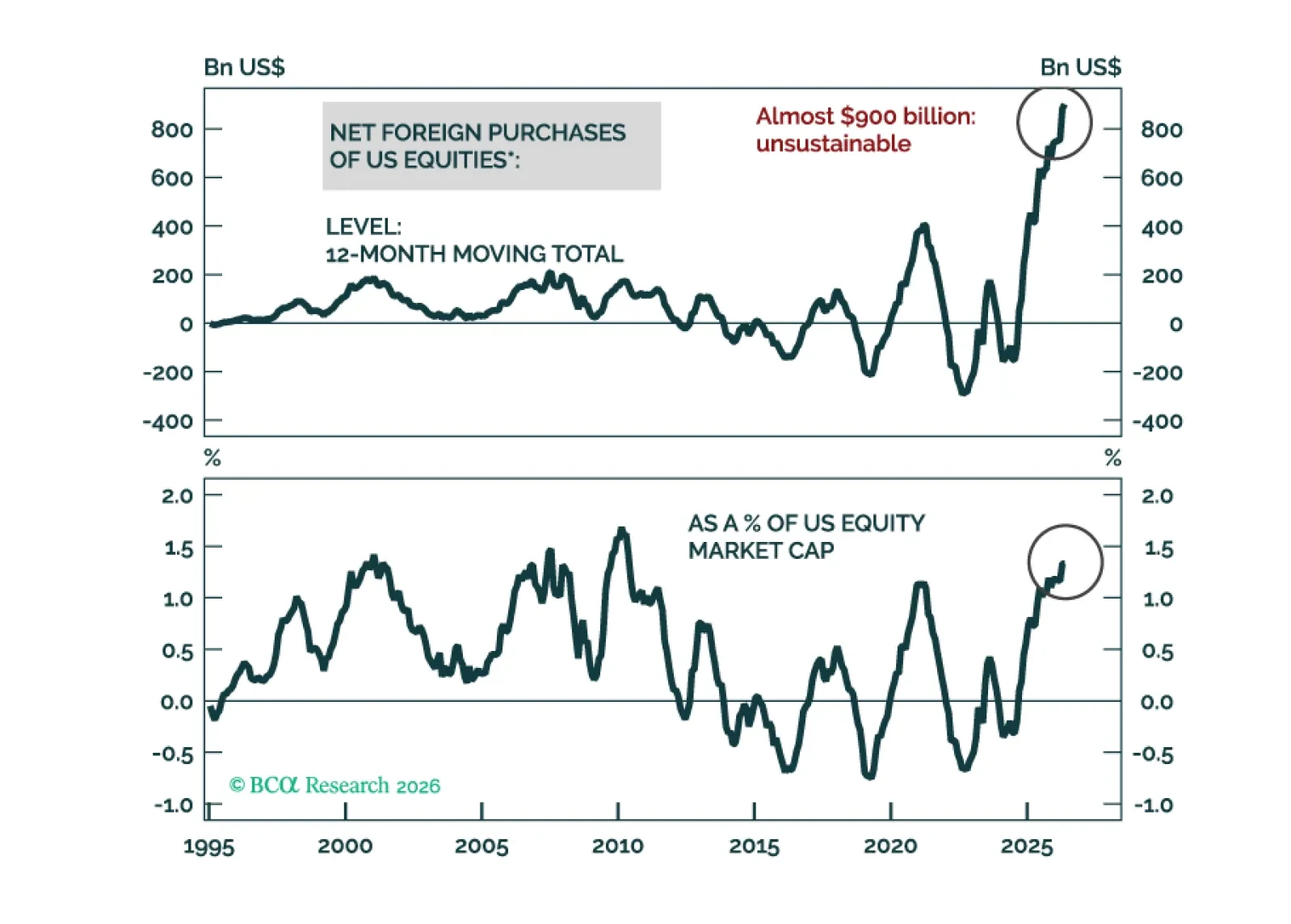

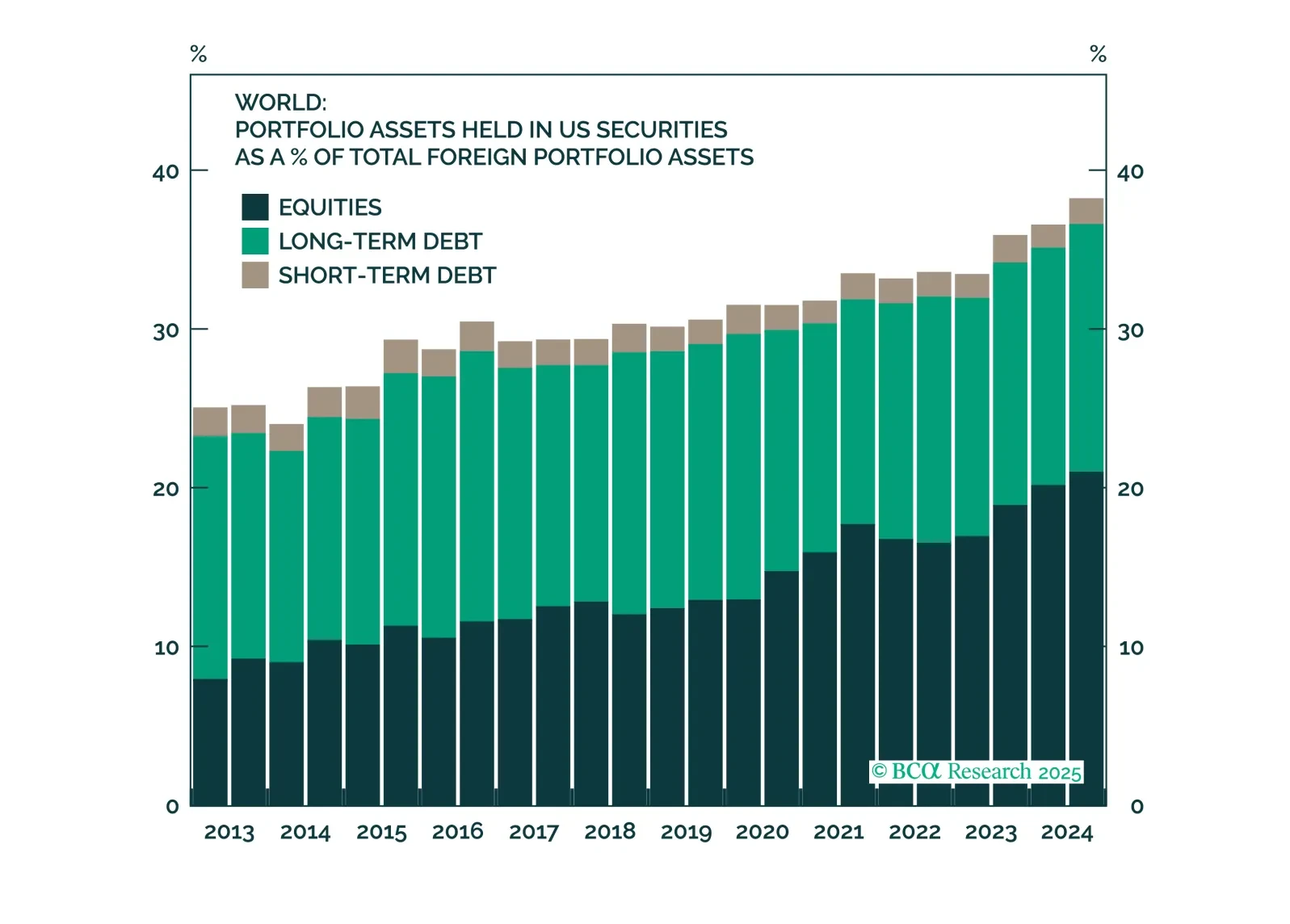

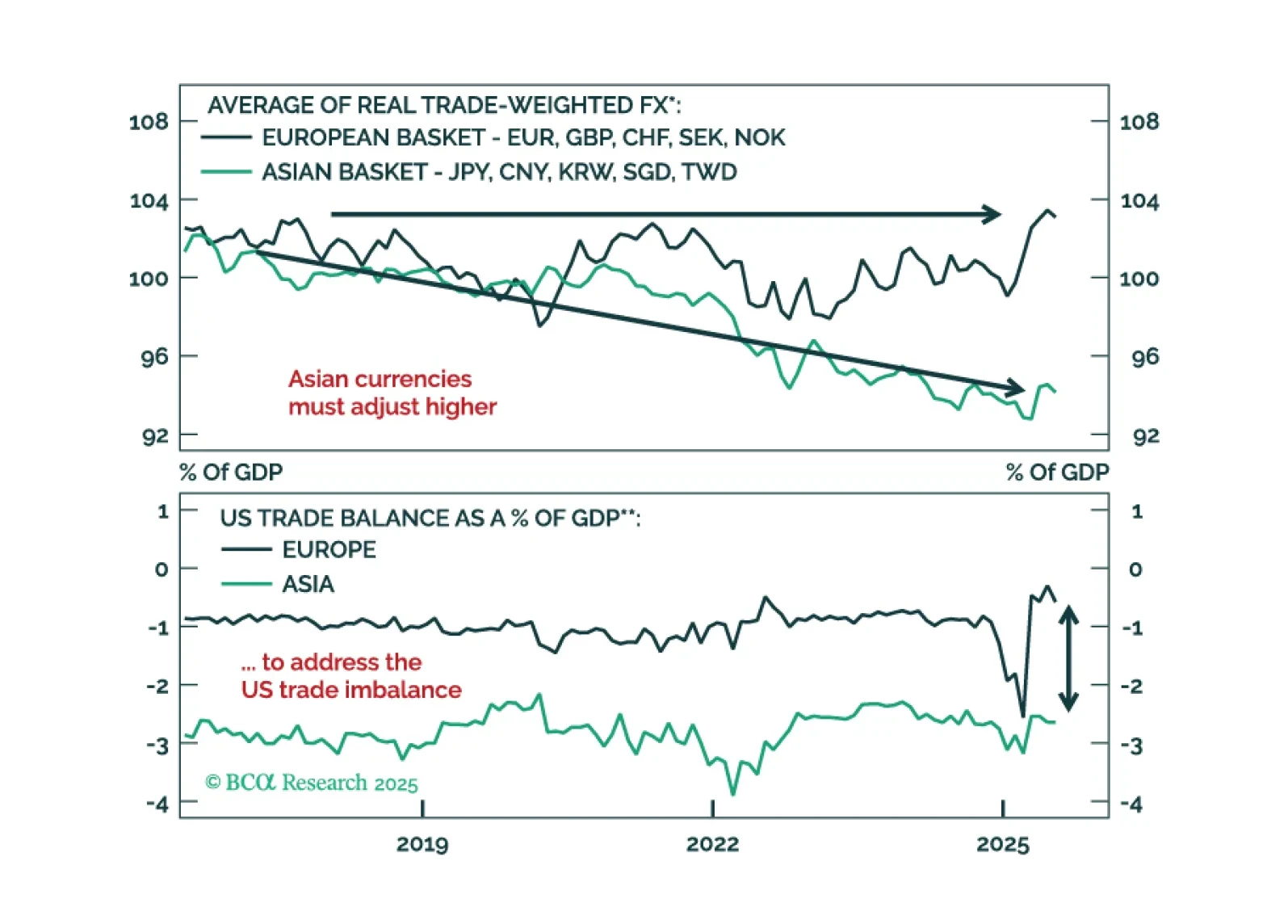

Capital Flows

The US dollar will become a pro-cyclical currency going forward. This regime shift would upend financial market correlations, and most investment portfolios are not positioned for it. A great deal of money is made or lost during regime changes - and one is coming soon. That is why our message remains loud and clear: Get Out of the Dollar (G.O.D.).

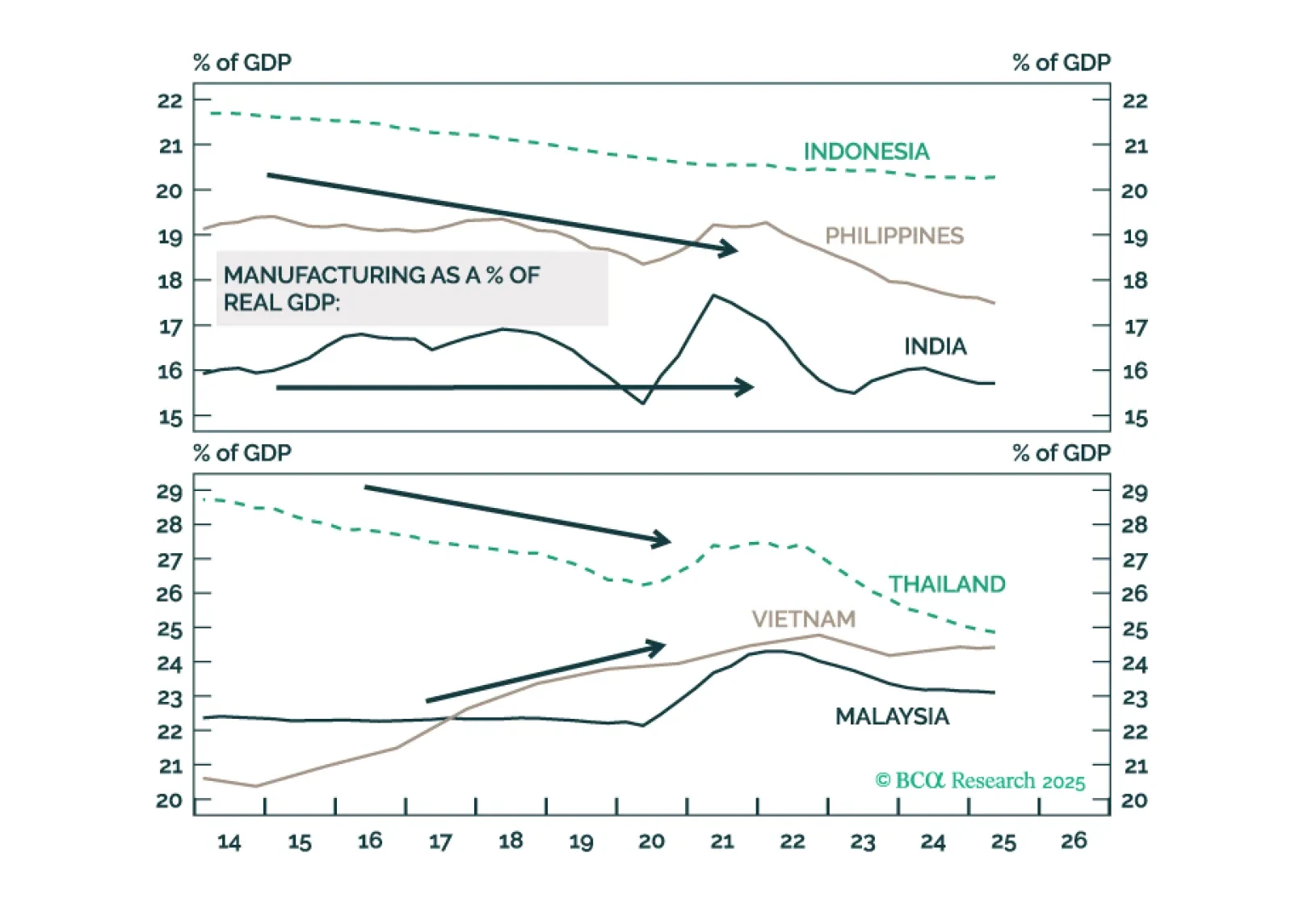

Investors should not count on buoyant growth in the ASEAN and Indian economies because of manufacturing relocation away from China in the next couple of years.

The dollar’s early 2025 decline was a reflection of a global rush to hedge accumulated USD exposure, not a mass exodus from US assets. With most hedging now complete, currency moves should again follow fundamentals, setting the stage for a tactical USD rebound in the months ahead.

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

Despite widespread investor optimism Brazil’s currency outlook is challenged by a toxic mix of poor external, fiscal, and macro fundamentals. Expect BRL to underperform most EM peers.

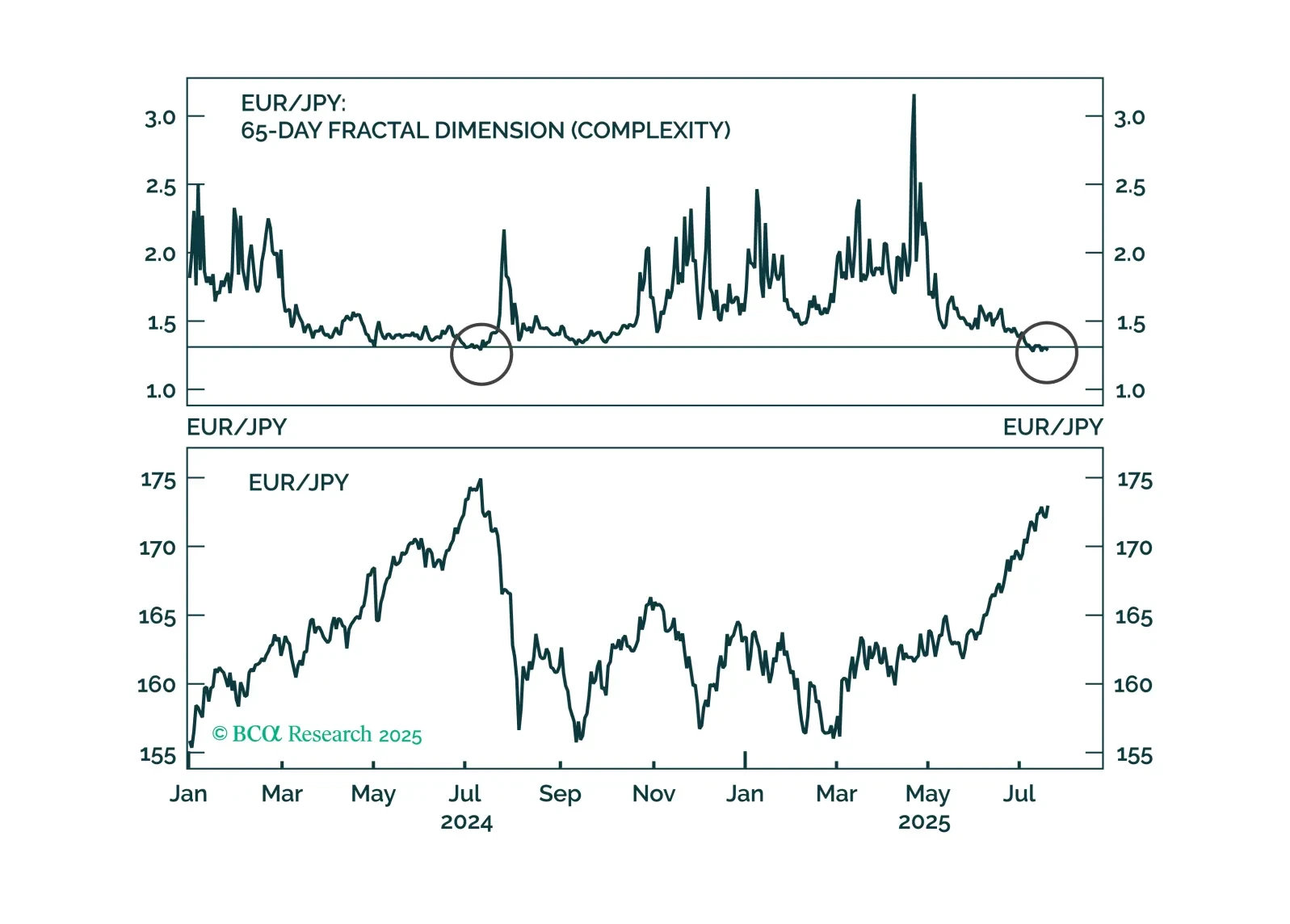

The yen’s discount, surplus, and rising real rates line up for a multi-quarter surge. Find out why EUR/JPY is the first short and when USD/JPY follows.

EUR/JPY has reached stretched levels, prompting new short trade recommendations across BCA Strategies. The calls are underpinned by compelling valuation, macro, and technical signals.

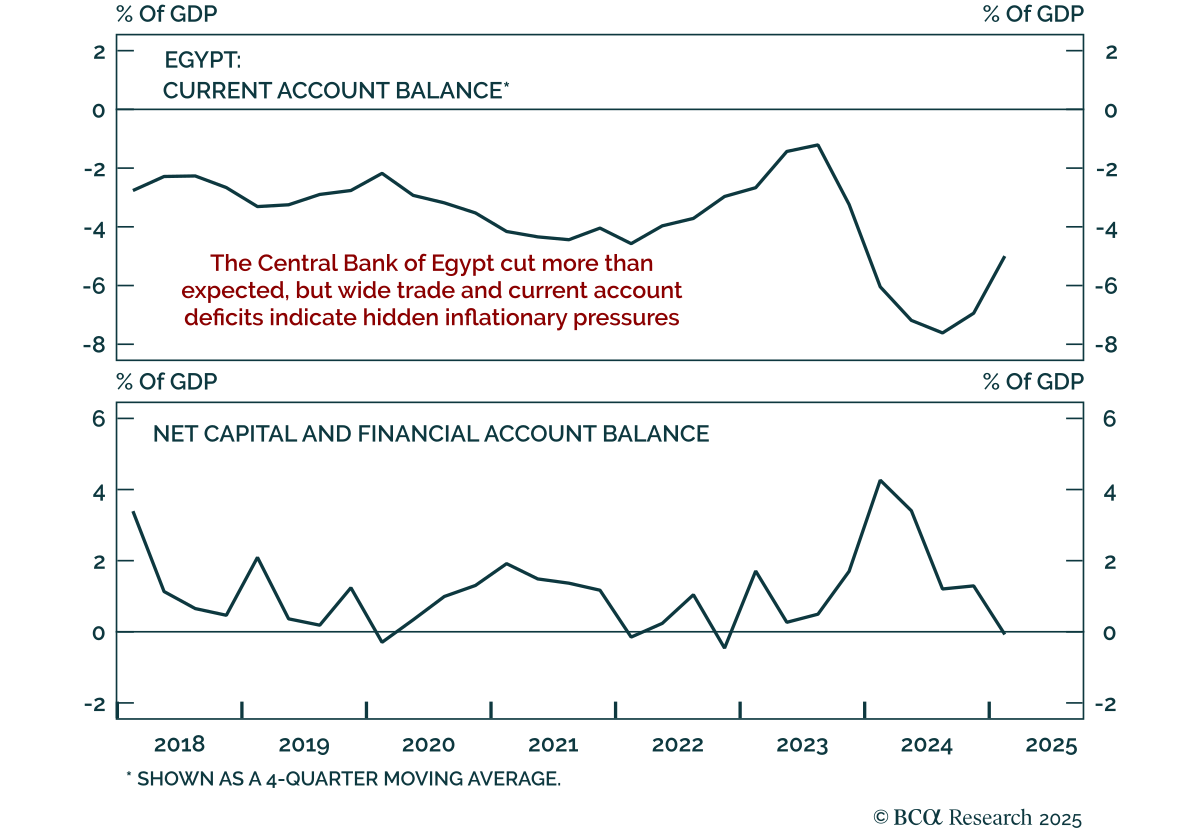

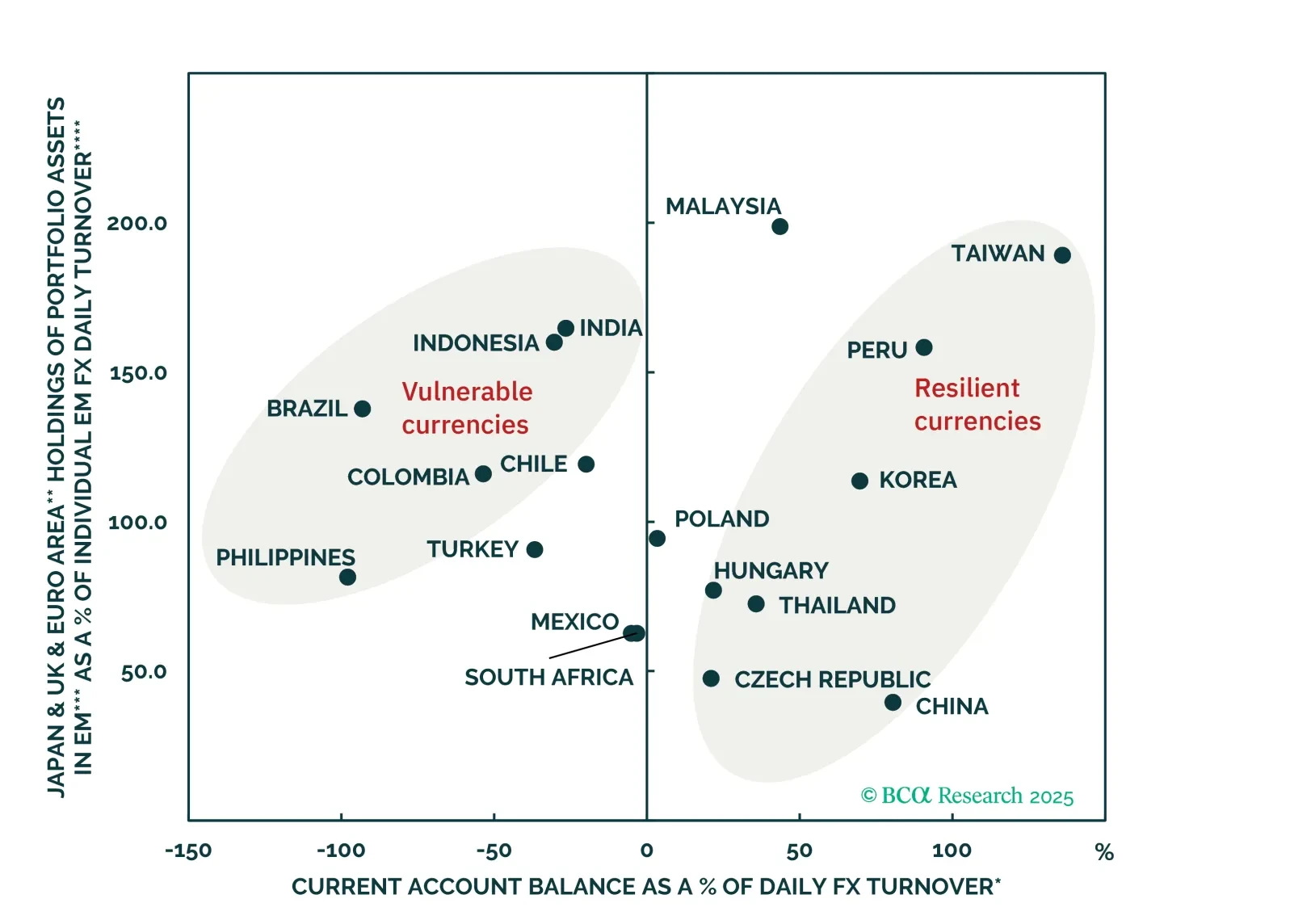

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.