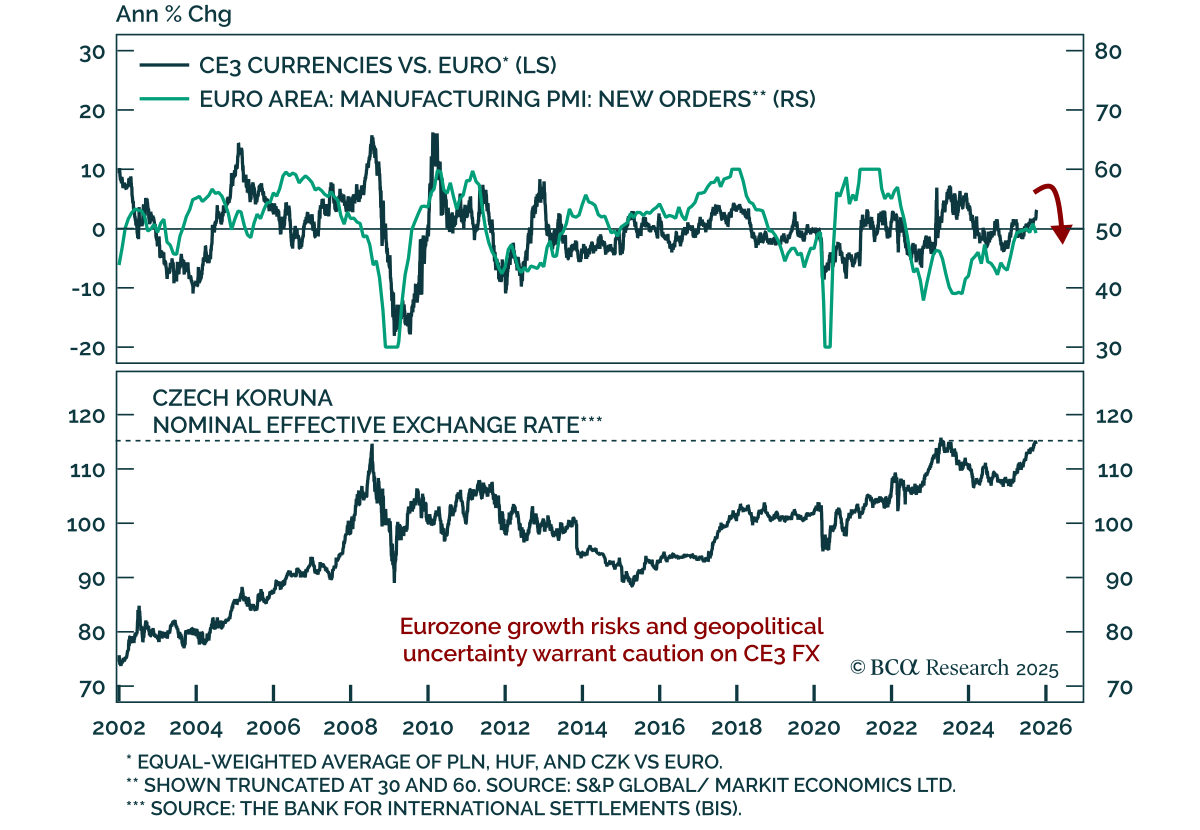

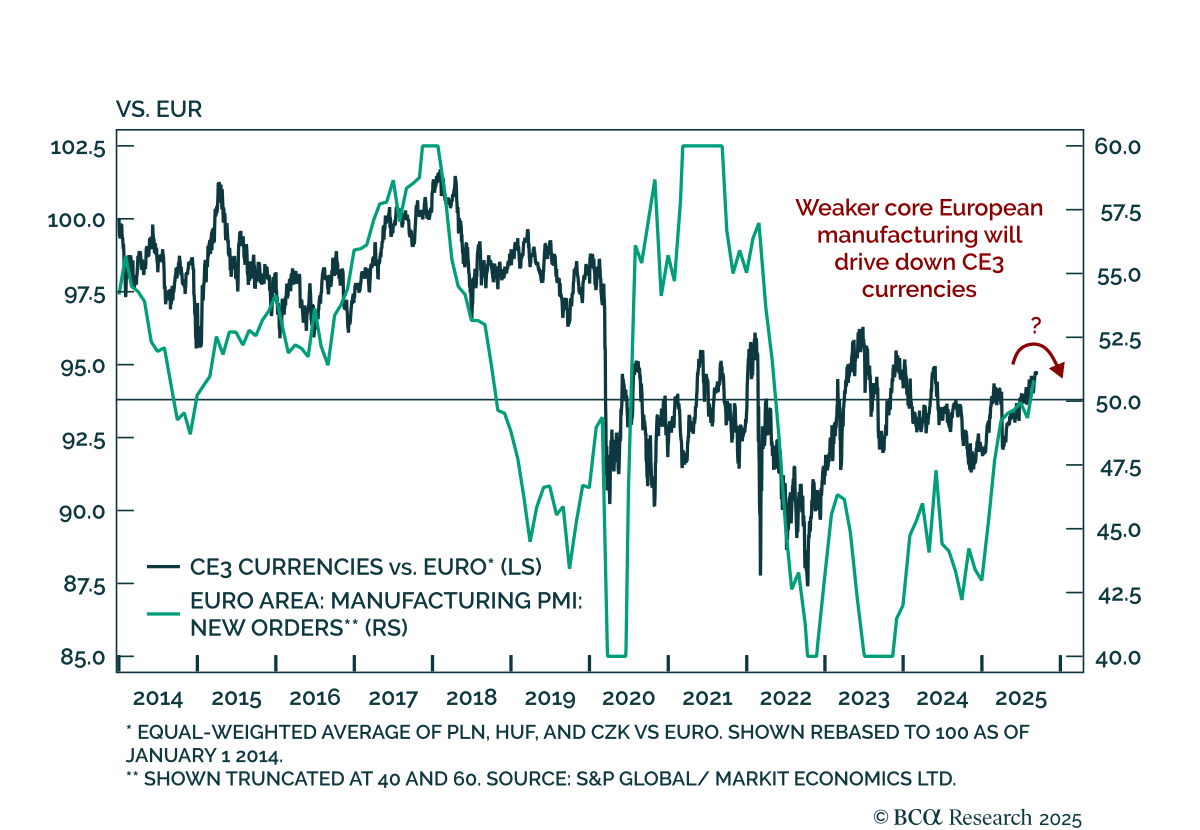

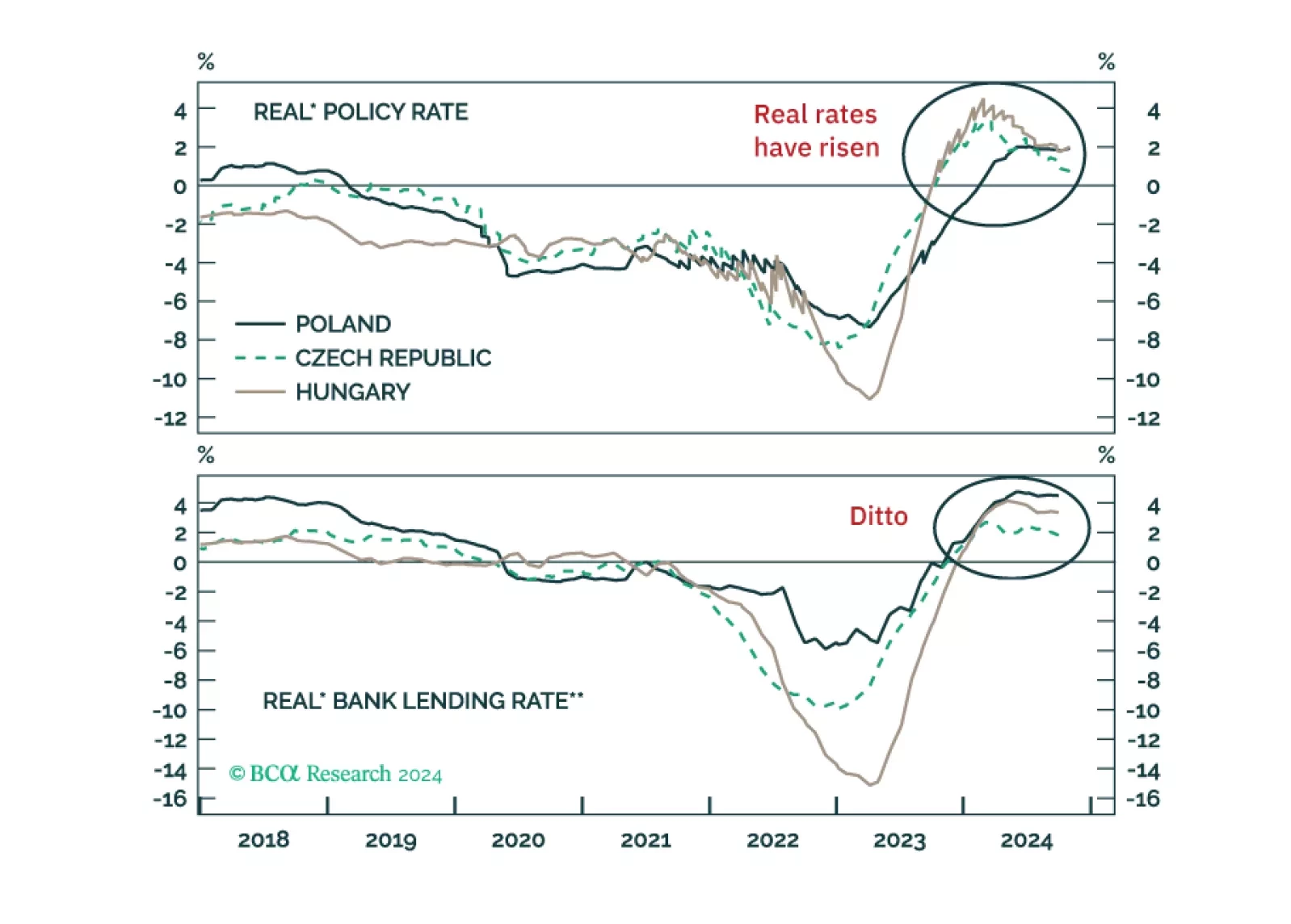

Domestic bond yields in the three major central European markets have recently inched up more than their German counterparts. This is despite economic growth staying quite weak in CE3. What should investors make of it (Chart 1)?Our take is that the CE3 yield differential over German bunds will widen in the coming months. That is due both to CE3 currency depreciations and diverging inflation outlooks. CE3 currencies are headed lower as growth in core Europe will continue to struggle.In addition, persistently high wage growth entails that core inflation in CE3 is unlikely to fall any further in the coming months, even if growth disappoints. The end of their disinflation cycle will prevent CE3 bond yields from declining considerably in the next six to nine months. Currencies And Bonds: The Drivers And Outlook CE3 currencies are heading lower vis-à-vis the greenback and the euro. That is because a crucial driver of these currencies—the growth outlook in core Europe—remains tepid (Chart 2). That is unlikely to change much going forward. Uncertainties surrounding Trump’s looming tariffs on Europe will continue to hurt business sentiments and growth in Europe. While the timing of tariffs is unknown, European capitals are preparing for executive actions shortly after Trump’s inauguration on January 20. A weak CE3 currency outlook is also negative for CE3 domestic bonds. Chart 3 shows that a depreciating currency usually coincides with a widening yield differential of CE3 domestic bonds over German Bunds. That means CE3 bonds are set to underperform their German counterparts in common currency terms as both drivers of return (‘spreads’ and currency) will work against them. Apart from the currency impact, the CE3 inflation outlook is also bond-negative. Core inflation in the central European economies appears to have bottomed out for now. The reason is persistently high wage growth – mostly due to severe labor shortages. The labor force participation rate is very high in these three countries, leaving little spare capacity in the labor force (Chart 4). Since such demographic challenges cannot be resolved anytime soon, wage growth rates will remain steep in the foreseeable future. Chart 5 shows that wage growth rates dictate CE3 core inflation. The latter, therefore, will likely hover above the central bank’s upper target bands in the foreseeable future. That, in turn, will put a floor under bond yields. The bottom line is that CE3 domestic bond spreads versus German bunds will widen both due to CE3 currency weakness and cyclical inflation outlook. That calls for underweighting CE3 domestic bonds vis-à-vis bunds in fixed-income portfolios. CE3 bonds will also underperform their EM counterparts on a similar logic: the cyclical disinflation process is over in CE3 but not in most EM economies. As such, CE3 will likely witness relative bond yield widening vis-à-vis elsewhere in EM. A Whiff Of Stagflation?Weak core European growth usually depresses central Europe's highly connected economies. Indeed, the persistent contraction in European manufacturing orders points toward muted CE3 growth ahead (Chart 6). The latter’s domestic headwinds will accentuate that weakness. These headwinds will hurt the Czech and Hungarian economies much more than the Polish economy (details below). However, as mentioned, inflation will remain above the central bank targets everywhere. That suggests a stagflationary environment. Real policy rates in CE3 have not only turned positive, but they are also higher than pre-pandemic levels (Chart 7, top panel). The same can be said about real bond yields. Real bank lending rates have also become restrictive, especially in Poland and Hungary (Chart 7, bottom panel). Put differently, monetary conditions have tightened meaningfully, which is growth-negative.The central banks of Poland and the Czech Republic recently revised down their growth projections for 2025, while revising up their inflation projections. The Polish and Hungarian central banks have also paused their easing cycles. The Czech National Bank lowered its base rate by 25 basis points earlier this month but acknowledged that inflation will remain above the target next year.All this indicates that policymakers are bracing for a stagflationary environment, in which growth remains low but inflation remains above the central bank’s targets.This also means further policy rate cuts will be difficult to come by. The upshot is that real borrowing costs will remain relatively high, further weighing on growth.Data indicates that domestic demand is already weak, particularly in the Czech Republic and Hungary. This can also be seen in retail sales volume levels – which have remained below their 2021-22 peak (Chart 8). Fiscal policy has been a headwind, too, particularly in the Czech Republic and Hungary this year. Next year, however, the fiscal thrust will be only marginally negative, as per the IMF. To be sure, Poland is much less exposed to a struggling core Europe than the other two. The country is also set to receive a significant EUR 9.4 billion of EU grants and loans in the coming months (in addition to the EUR 6.3 billion they received in 2024 so far). This will help put a floor under its growth, as those funds will be deployed in various infrastructure projects. Overall, the Polish growth will fare relatively better than the other two. Polish core inflation will also likely perk up more than others. Czech inflation, on the other hand, will be the least pronounced. Geopolitical Risk Premium Spikes In Near TermThe Ukraine war escalated in a way that caught global investors’ attention on November 18 when US President Joe Biden gave Ukraine approval to use long-range missiles against Russia, including targets in the Russian heartland.Biden’s action stemmed from North Korea’s deployment of nearly 10,000 troops to fight Ukrainians near Kursk, Russia, where Ukraine invaded in August. The United Kingdom also gave approval for Ukraine to use long-range missiles. Ukraine promptly staged attacks against Russian supply lines using these missiles, triggering a harsh Russian reaction.Russia retaliated by firing a new hypersonic missile against Ukraine and revising its nuclear doctrine to lower the threshold for the use of nuclear weapons. Previously Russia only said it would use the bomb in the event of an existential threat to the state. Now Russia says it will consider an attack by a non-nuclear state (Ukraine) allied with a nuclear state (e.g. the US or UK) as a joint attack and potentially worthy of a nuclear retaliation. In particular, an extensive Ukrainian barrage of US-made missiles and drones targeting interior Russian cities could cross the new threshold.That is a convincing reason for Ukraine to limit the use of the missiles to targets close to its border, sporadically and only to hit military supply lines. Kiev does not have an interest in crossing Russia’s red lines and provoking a nuclear attack when it cannot be certain of the extent of that attack, the targeting, or that NATO would retaliate. Russia, for its part, would prefer not to use nuclear weapons because of the potential radioactive cloud close to home and the risk that NATO would retaliate by staging a conventional military strike against Russian forces operating in Ukraine. The Kremlin cannot be certain since the NATO states have a strong interest in preventing nuclear blackmail from becoming a new norm.Ultimately, Russia will use nukes if Ukraine goes too far – otherwise, it would not have staked its credibility on this new threat. Note that there is a high probability of near-term escalation of the war, including nuclear brinksmanship, even if the odds of a nuclear detonation remain in the low single digits.First, Ukraine’s fear of abandonment – and need to gain leverage ahead of any ceasefire talks – forces Kiev to escalate the war in the short run.Ukraine expects Trump and the Republicans to reduce military and financial aid since they were elected on the back of inflation and will seek to cut government spending. A loss of American support will signal to Europe that the war is effectively decided, as Ukraine will never join NATO.The Europeans want the war to end sooner rather than later because they fear the danger of a spillover into NATO territory as well as rising domestic political opposition. German and French leaders have already spoken to Vladimir Putin since Trump’s election, as they see the writing on the wall. Thus, Ukraine must take the initiative to prevent the West and Russia from foisting a ceasefire upon it, which is precisely what occurred in 2015 after Russia invaded Crimea.Second, the outgoing Biden administration views the incoming Trump administration as a threat to American democracy and a friend to Russian strategy. Trump wants to bring the war to a rapid ceasefire, but Russia would then succeed at establishing a sphere of influence and exposing a lack of resolve on the part of the Western democracies. Hence, Biden is attempting to speed up financial and military aid to Ukraine so that it can improve its war efforts, increase its leverage, and potentially create enough momentum to prevent Trump from utterly abandoning Ukraine or approving a lopsided ceasefire in Russia’s favor. Thus, the war is escalating as we go to press and will continue for at least the final two months of Biden’s “lame duck” presidency. After that, Trump’s inauguration on January 20 creates a clear diplomatic avenue for the reduction of tensions. Later, after Trump takes office, another risk will emerge for central Europe: the risk that Russia will stage a provocation against a NATO country to test whether Trump will “defend every inch” of the alliance’s territory, as Biden pledged to do. If Trump hesitates, Russia will undermine Eastern European trust in NATO, increasing the central European geopolitical risk premium. If not, Russia knows its limits for a while. Bottom Line: There is a major increase in Russia-NATO tensions around the endgame in Ukraine, which should inject a risk premium into Polish, Hungarian, and Czech currency and assets at least for the next few months around the US power transition and possibly for a while longer. Investment ConclusionsCurrency: The Polish zloty has been the strongest of the three currencies over the past year as the markets celebrated Poland’s political return to the European manifold after the elections late last year. Now that event has been largely priced in, and the geopolitical risk is rising again. Investors should expect a relapse in Poland’s currency and share prices. A weak core European growth outlook means all CE3 currencies have a further downside compared to the greenback. Currency investors should stick with our recommendation of shorting an equal-weighted basket of CE3 currencies versus the greenback (Chart 2, above).Fixed Income: Considering the inflation outlook and currency prospects, we recommend that EM domestic bond portfolios downgrade the Czech Republic from overweight to neutral and Poland and Hungary from neutral to underweight.Investors should also take the same stance relative to German bunds: neutral the Czech Republic and underweight the other two (Chart 9).Notably, on October 21, 2024, we closed our long position in Czech domestic bonds. For USD-based investors, this recommendation has returned a 12.7% gain since its inception on December 08, 2022.We also booked profits on our trade “Pay Polish 2-year swap rates / Receive Czech 2-year swap rates,” which yielded 120 bps gains since its initiation on November 22, 2023. Equity: Given the weak growth outlook, the CE3 stock prospects remain lackluster. Tight monetary stances in all three countries and a negative fiscal thrust in the Czech Republic and Hungary will add to their headwinds. EM equity portfolios should downgrade both Polish and Czech stocks from overweight and neutral, respectively, to underweight. Hungary should also remain underweight (Chart 10). The rise in geopolitical risk in the region will likely exacerbate pressures on CE3 assets in the short term.Rajeeb PramanikSenior EM Strategistrajeeb.pramanik@bcaresearch.comMatt Gertken Chief Geopolitical Strategist mattg@bcaresearch.comFollow me onLinkedIn & X