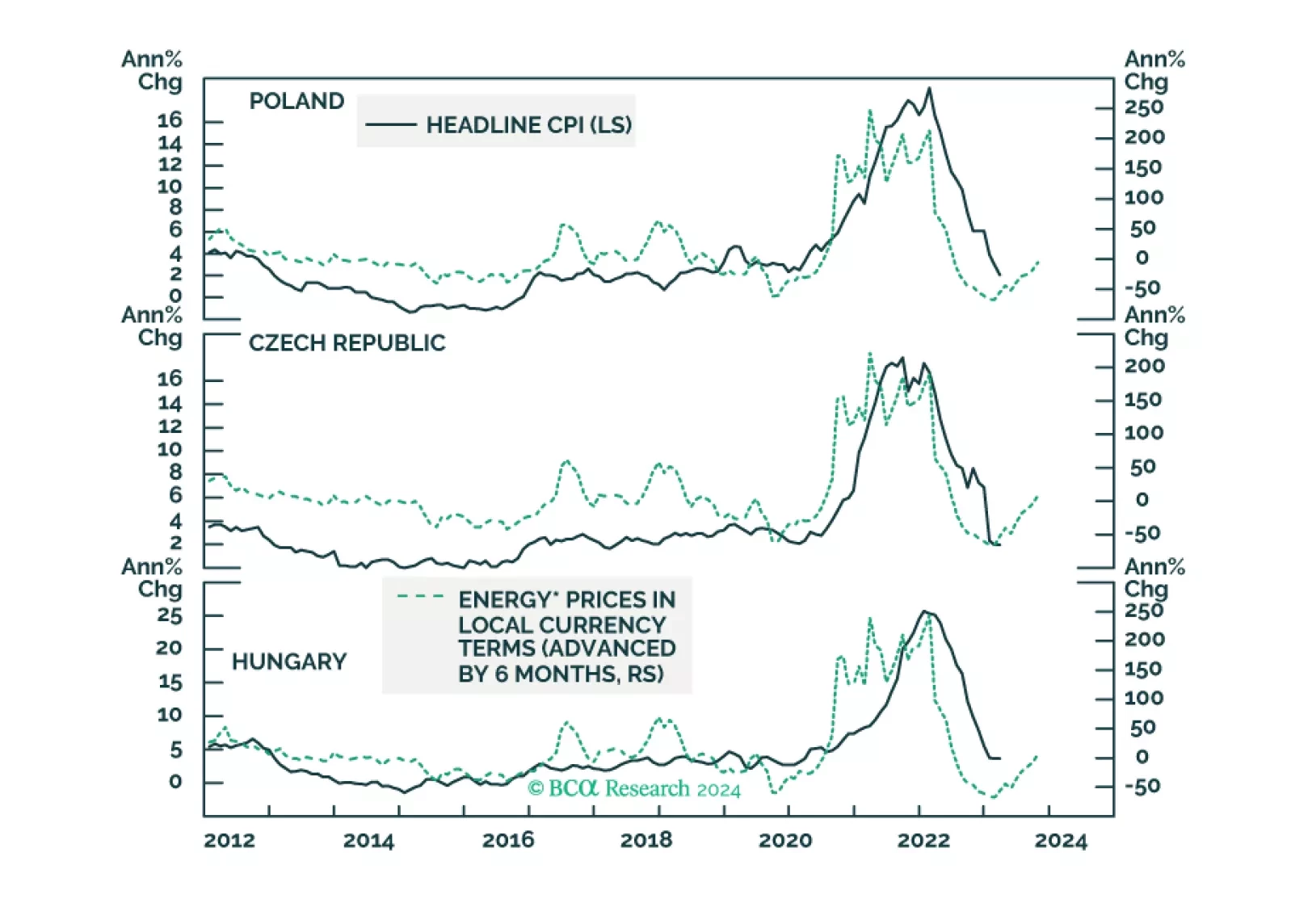

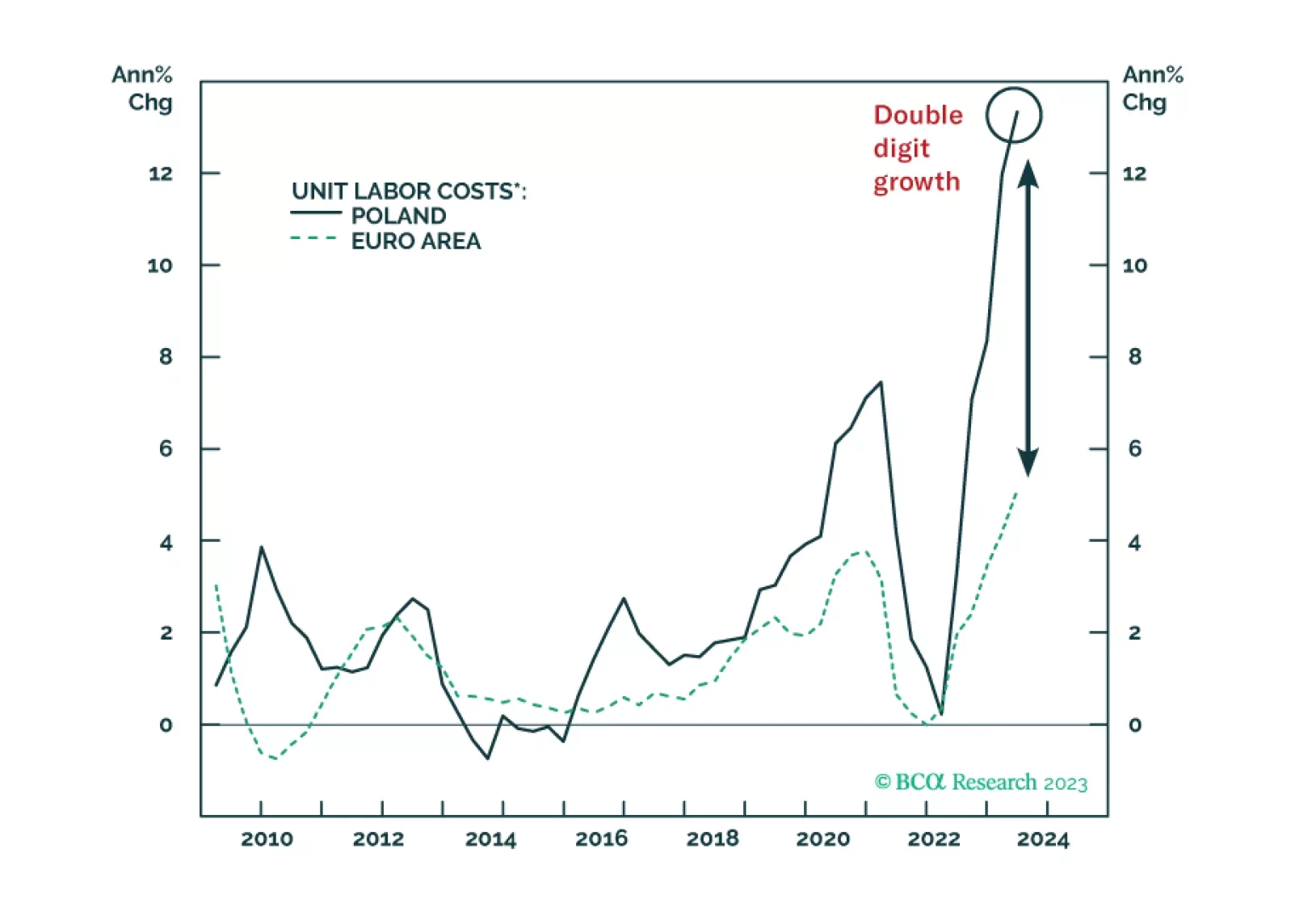

Executive Summary Poland: Wages Are Surging Hungary is exhibiting classic signs of an overheating economy –as rising inflation coincides with very strong domestic demand. Yet, authorities are still pursuing very stimulative monetary and fiscal policies. The upcoming appointments of new Czech National Bank (CNB) governor Aleš Michl and three new monetary policy board members entails a dovish shift in monetary policy. Core inflation in Poland will continue to rise due to the unfolding wage-price spiral. The reluctance of policymakers to tighten monetary and fiscal policies substantially in such an environment heralds a weaker currency and higher local bond yields. Continue to underweight Central European equities and local currency bonds relative to their respective EM benchmark. Underweight Central European local currency bonds within European core bond portfolio. Recommendation INITIATION DATE RETURN Receive Czech And Pay Polish 10-Years Swap Rates 2022-03-08 100 BPS Long CZK/Short HUF 2021-06-03 12.4% Short PLN/Long USD 2022-03-02 3.1% Bottom Line: The Hungarian and Polish economies are overheating, yet their monetary and fiscal policies remain accommodative. This is negative for their currencies and local bonds. Even though the incoming leadership of the Czech central bank will cultivate a more dovish stance than the current leadership, Czech macro policies are less stimulative than those in Hungary and Poland. By extension, the Czech currency and local bonds will outperform their Hungarian and Polish counterparts. Hungary: Classic Overheating Chart 1Hungary Is Overheating The Hungarian economy is exhibiting signs of classic overheating as rising inflation coincides with very strong domestic demand (Chart 1). Yet, authorities are not tightening monetary and fiscal policies meaningfully. The central bank is well behind the inflation curve. Accordingly, the currency will continue to depreciate and local bond yields will rise. The only way to reverse these dynamics is for authorities to tighten monetary or fiscal policies dramatically, which will likely cause a recession. Looking forward, authorities will continue to pursue their pro-growth agenda despite the unfolding wage-price spiral. Inflation is broad-based and will accelerate further. High inflation is not limited to goods. Core, trimmed-mean and service inflation are also very high, in some cases in double digits (Chart 2). Chart 2Hungary: Inflation Is Broad-Based Chart 3Hungary: Wage Growth Is In Double Digits Hungary’s labor market is tight, and wages are surging (Chart 3). Notably, wage growth is in double digits and is well above core inflation. Wage growth will remain robust as the government is set to boost public wages and the private sector is struggling to fill vacant positions. Employment is at an all-time high, and the number of unemployed people is approaching pre-pandemic lows (Chart 4). Strong employment and solid real wage growth will support consumer spending for now. Despite a major slowdown in the euro area, Hungarian exports will suffer less than those of other EU members. Almost 50% of Hungary’s manufacturing output comes from automotive, food and beverages, as well as industrial electrical equipment sectors. Demand for these sectors remains robust despite a potential drop in demand for consumer goods in the EU. Despite the central bank raising rates by a cumulative 530 bps since June 2021, real policy rates and real commercial bank lending rates (deflated by core CPI) are at all-time lows, and money and private credit are booming (Chart 5). In brief, the central bank remains behind the inflation curve. The National Bank of Hungary (NBH) has also been the most aggressive central bank in the region in monetization of public debt and corporate debt. There is little evidence to suggest that it is planning to tighten liquidity as a means of reining in inflation. Chart 4Hungary: Labor Market Is Currently Very Tight Chart 5Hungary: Money And Credit Are Booming Chart 6Hungary: Twin Deficit Fiscal policy will remain loose and unorthodox measures will likely persist. Government primary spending has reached 46% of GDP and is unlikely to retrench much. In particular, in response to the EU’s recent €7.2 billion (4.6% of GDP) cut in funding to Hungary, prime minister Orbán has announced spending cuts and tax hikes to prop up government revenues (Chart 6, top panel). The government has imposed “windfall” taxes1 on some firms or industries where profits are excessive from the government’s perspective. The majority of spending cuts (€3 billion or 2% of GDP) will be in public investments. Meanwhile, authorities continue subsidizing household utility bills and raising public wages and pensions. This will keep consumption strong. A very wide current account and trade deficits are also signs that the economy is overheating (Chart 6, bottom panel). Bottom Line: Super-loose monetary and fiscal policies amid an overheating economy warrant further currency depreciation and higher bond yields. The Czech Republic: A Policy Shift Coming The recent appointments of Czech National Bank (CNB) governor Aleš Michl and three new monetary policy board members entails a dovish shift in monetary policy. Notably, Aleš Michl, a current board member of the monetary policy committee, has been a strong opponent of the CNB’s hawkish stance alongside current board member Oldřich Dědek. Both men have been the only two of the seven-member committee to vote against rate hikes in the past eight meetings. In addition, President Zeman recently appointed three new members to the monetary policy committee to replace hawkish members that have reached the end of their terms. These new appointments are likely to be aligned with the forthcoming CNB governor’s dovish approach to monetary policy. Chart 7Czech Output Gap And Core Inflation Altogether, these appointments will result in a major shift in the CNB’s monetary policy board, whereby at least four out of the seven board members will likely vote against further rate hikes after July. Therefore, the CNB policy will undergo a dovish pivot. This will occur at a time when genuine inflation is still high and inflationary pressures are intense: The very large positive output gap heralds persistent inflationary pressures (Chart 7, top panel). Indeed, core and trimmed-mean CPIs are surging, which suggest that inflation is broad-based (Chart 7, bottom panel). Job vacancies exceeding the number of unemployed people entails a very tight labor market (Chart 8). The upshot is rising wages (Chart 9). Domestic consumption remains robust due to considerable household income gains. Chart 8The Czech Republic: Labor Shortages Are Pervasive Chart 9Wage Growth Is Lower In Czech Than In Hungary And Poland Chart 10Fiscal Policy Is Tightening More In Czech Than In Hungary And Poland On the one hand, a dovish monetary policy shift is negative for the Czech koruna. On the other hand, the country’s fiscal thrust will still be negative this and next year (Chart 10). This is in contrast to Hungary and Poland. Besides, the central bank considers a weak currency to be a risk to its “fulfilment of price stability” and regards the “easing of the monetary conditions” as “inappropriate”. Last month, the CNB board convened in an emergency meeting to announce the selling of foreign exchange reserves to stem volatility in the currency. The Czech Republic has a lot of foreign exchange reserves that could be utilized to stem any large moves in the koruna. Even newly appointed governor Aleš Michl considers a strong koruna to be an important part of his mandate. His recent comments to local media suggest that the CNBs’ intention is to defend the currency against any medium to long-term weakness: “I want a strong koruna based on long-term cash flows to the country and investor interest in the Czechia. The koruna has not strengthened in trend since 2008. Everyone is only evaluating short-term fluctuations, but they do not perceive this significant change. The koruna will only be strong if we have long-term balanced public finances.” Overall, the selling of foreign exchange reserves to defend the currency will tighten monetary conditions and prevent short-term interest rates from falling. Whenever a central bank sells foreign currency, it is forced to purchase local currency which lowers commercial banks’ excess reserves at the central bank. The latter could reduce money origination by commercial banks. While long-term bond yields could rise as the central bank falls behind the inflation curve, the currency will likely be range bound versus the euro for some time. Bottom Line: Even though the central bank is shifting into a dovish mode, it will maintain the policy of a strong currency. Plus, the fiscal policy will be tightening, which is not the case in Hungary and Poland. We reiterate our long CZK / short HUF trade. Poland: Misguided Macro Policy Chart 11Poland: Wages Are Surging Inflation in Poland will continue to rise due to the unfolding wage-price spiral (Chart 11). Besides, the central bank is still behind the inflation curve, and fiscal policy has not tightened substantially. The reluctance of policymakers to tighten monetary and fiscal policies amid the wage-price spiral warrants a weaker currency. Also, a top in domestic bond yields might not be imminent. A buying opportunity in Polish local currency bonds will emerge only when authorities take measures to bring down inflation and when geopolitical tensions between Russia and the west abide. The central bank and government continue to blame inflation on the war in Ukraine, i.e., on supply-side factors rather than excessive domestic demand. Chart 12Poland: Consumer Spending Has Overshot Contrary to policymaker rhetoric, Poland is experiencing an inflationary boom, whereby rising inflation is not only the result of supply-side bottlenecks but is also due to excessive demand. Chart 12 illustrates that retail sales have overshot above a reasonable uptrend trajectory. Critically, the labor market is very tight. As a result, wage growth is skyrocketing both in nominal and real terms. With productivity growth well below wage growth, unit labor costs are accelerating. This will squeeze company profit margins and lead these to hike selling prices to protect profit margins. With such robust income growth, consumers might accept higher prices and the wage-price spiral will likely be sustained. Meantime, fiscal policy will remain accommodative at least throughout early 2023, until the scheduled parliamentary elections take place. The government has provided subsidies on energy and has cut the VAT rate. These programs effectively amount to stimulus for households. Chart 13Poland: Interest Rates Are Very Low/Negative In addition, the central bank will not likely hike rates aggressively. Recent comments by central bank governor Adam Glapinski appear to suggest that the National Bank of Poland (NBP) is likely to pause or slow its rate hikes. Even though the central bank has hiked its policy rate by 590 bps in the past 12 months, real policy and prime lending and mortgage rates as well as government bond yields remain very negative (Chart 13). This signifies that the monetary tightening has been insufficient. Lastly, in the current geopolitical climate, Poland is the most vulnerable among Central European nations to any escalation between Russia and the west. This is due to its extensive border with Ukraine, and due to it being the transit route for arms into Ukraine from the west. Poland has adopted a hard stance on Russia. This makes Poland an easy target for Russian rhetoric. While chances of direct conflict are slim, any further escalation by Russia will make Polish financial markets vulnerable to selloff. Bottom Line: For now, investors should continue to underweight Polish domestic bonds within both EM local currency bonds and core European bond portfolios. Also, we continue to recommend shorting PLN versus the USD. Investment Recommendations The Hungarian and Polish economies are overheating, and their monetary and fiscal policies remain accommodative. This is negative for their currencies and local bonds. Even though the incoming leadership of the Czech central bank will be more dovish than the current leadership, Czech macro policies are less stimulative than those in Hungary and Poland. Hence, the inflation outlook is more benign for the Czech economy than it is in Hungary and Poland. By extension, the Czech currency and local bonds will outperform their Hungarian and Polish counterparts. Chart 14Our Trade: Long CZK / Short HUF In light of this, we recommend the following to investors: Underweight Central European local currency bonds within European core bond portfolio. Keep the long CZK / short HUF trade (Chart 14); Hold onto the short PLN / long USD trade. Maintain the relative rates trade of receiving Czech and paying Polish ten-year rates. This spread has widened by 100 bps since our recommendation on March 8, 2022. Maintain underweight in local bonds and equities for Central Europe relative to their respective EM benchmarks. Andrija Vesic Associate Editor andrijav@bcaresearch.com Footnotes 1 A windfall tax is extra tax on profits of a particular company or industry that is deemed to have earned excessive profits.