China

Oil shocks hit economies with a lag. China will feel the delayed pain of surging oil prices, pushing Beijing toward infrastructure spending as its main tool to prop up growth.

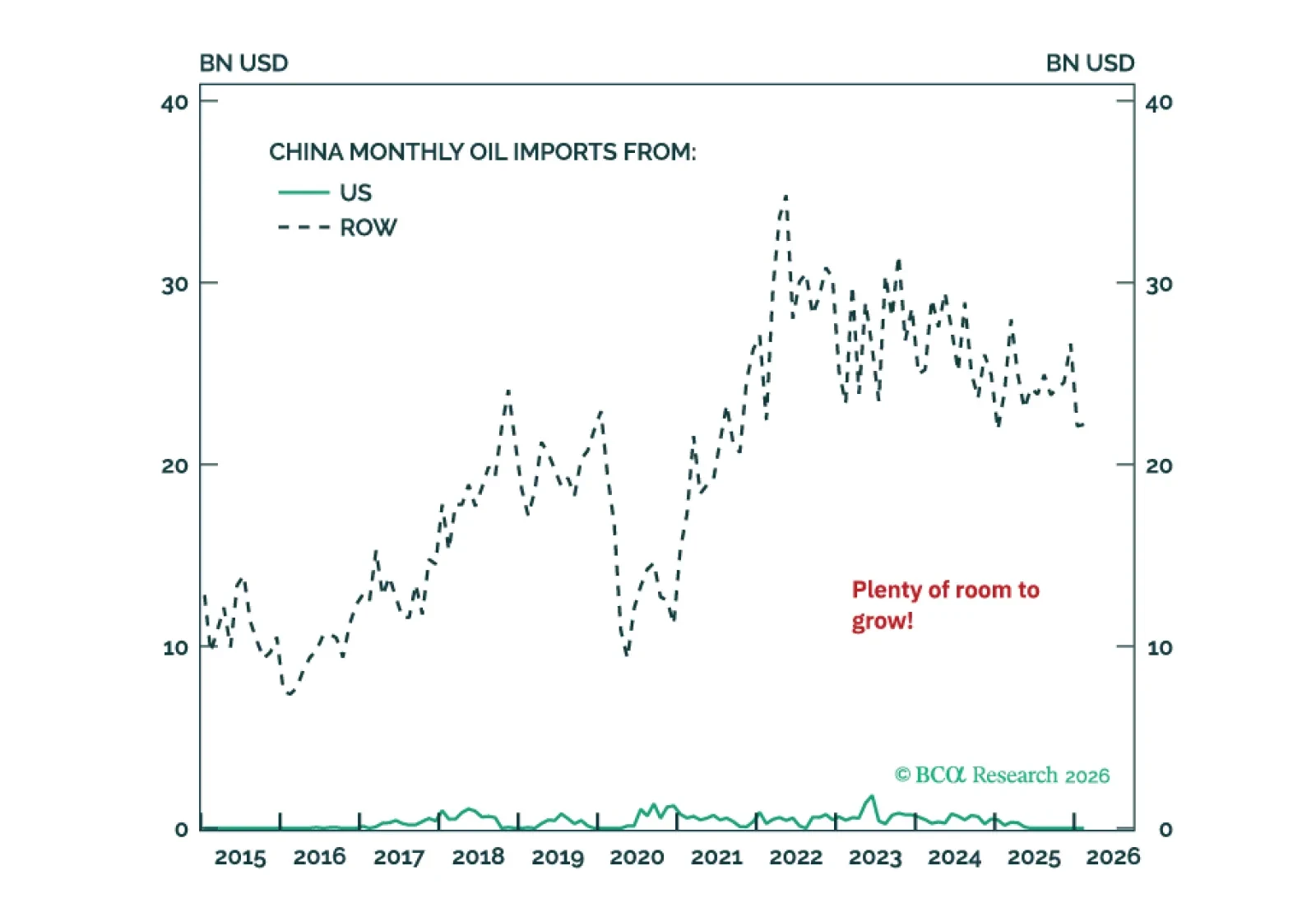

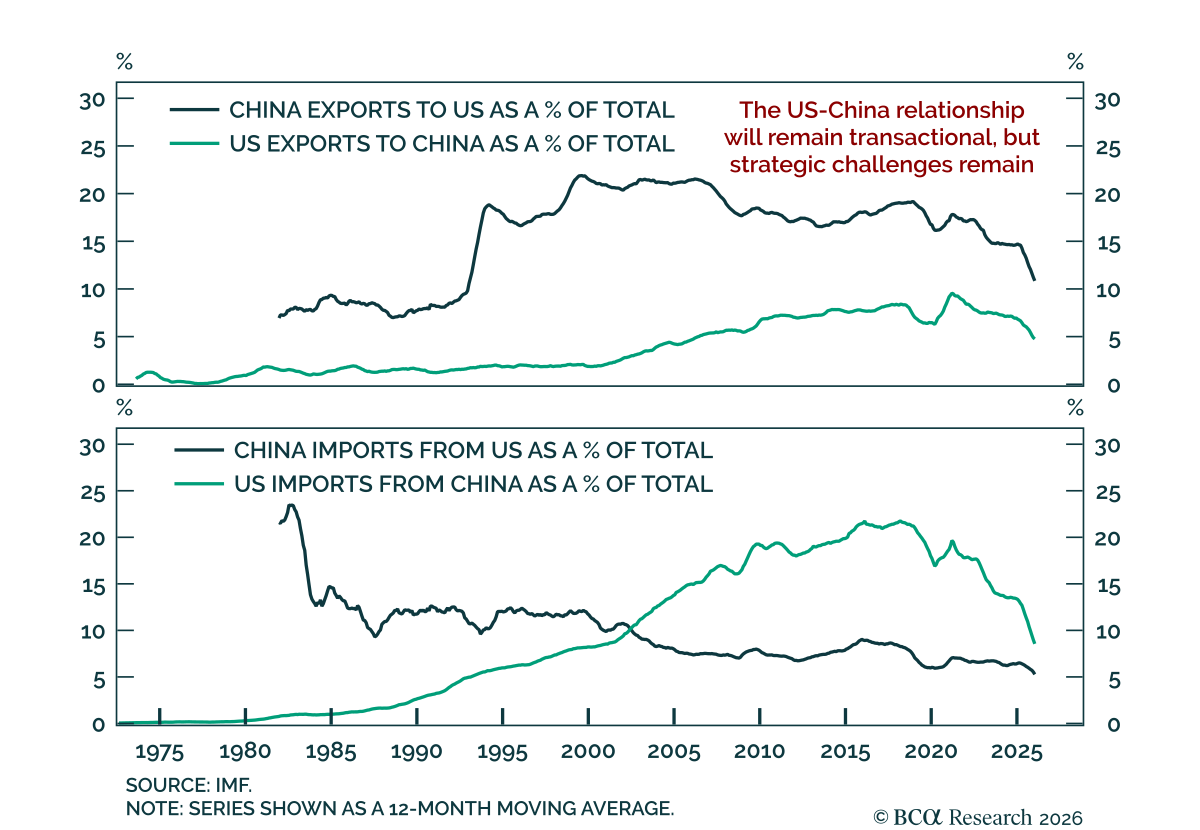

The US-China trade truce is getting bigger and better, but a grand strategic bargain on Iran and Taiwan is not happening.

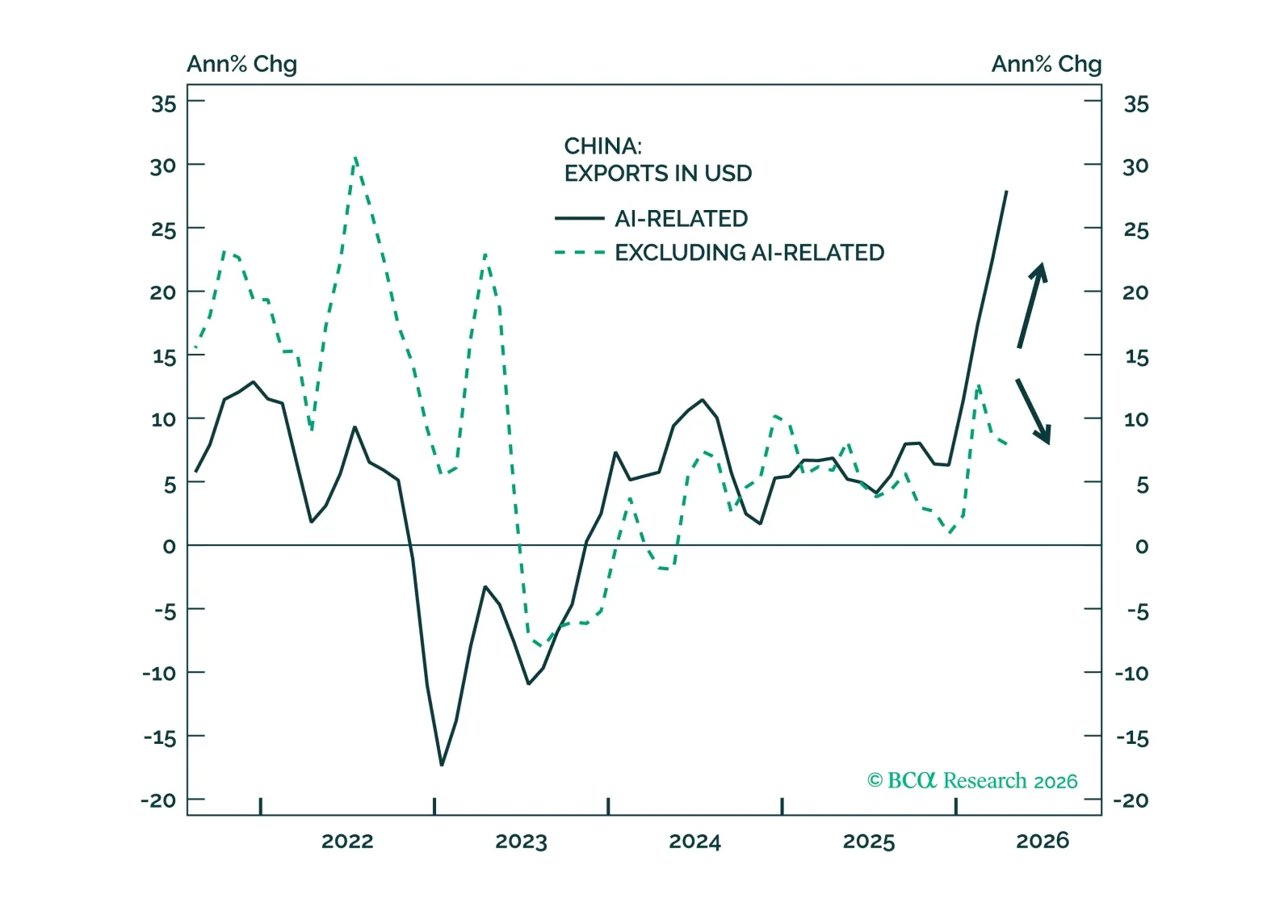

China’s K-shaped economy is widening, with resilient exports and subdued domestic consumption. Over the next 6–12 months, we see a higher probability that global capex momentum persists than China delivers meaningful consumer-focused stimulus.

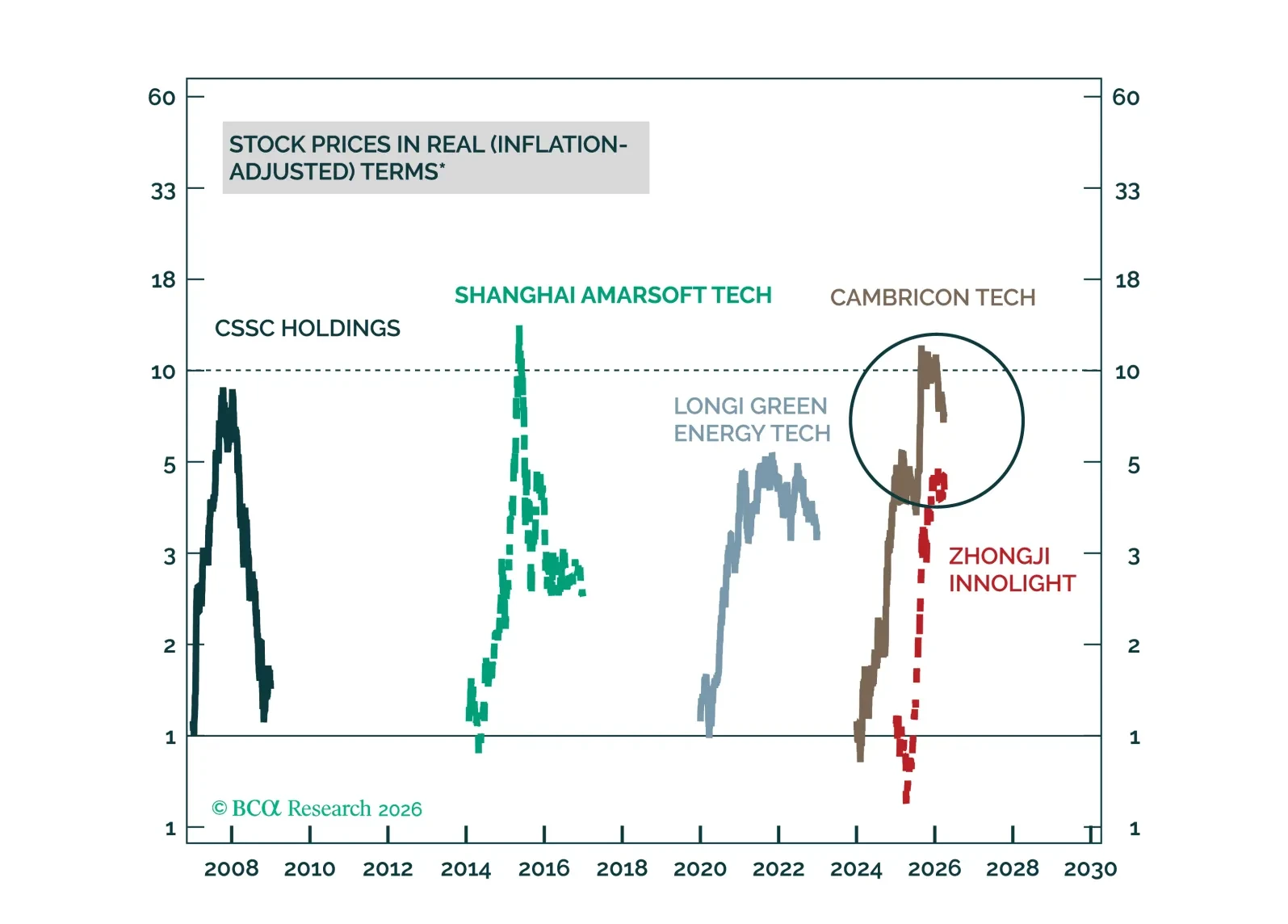

Chinese onshore equities are riding the global “scarcity trade,” powered by tight semi supply and surging alternative-energy demand. How should investors position in this environment?

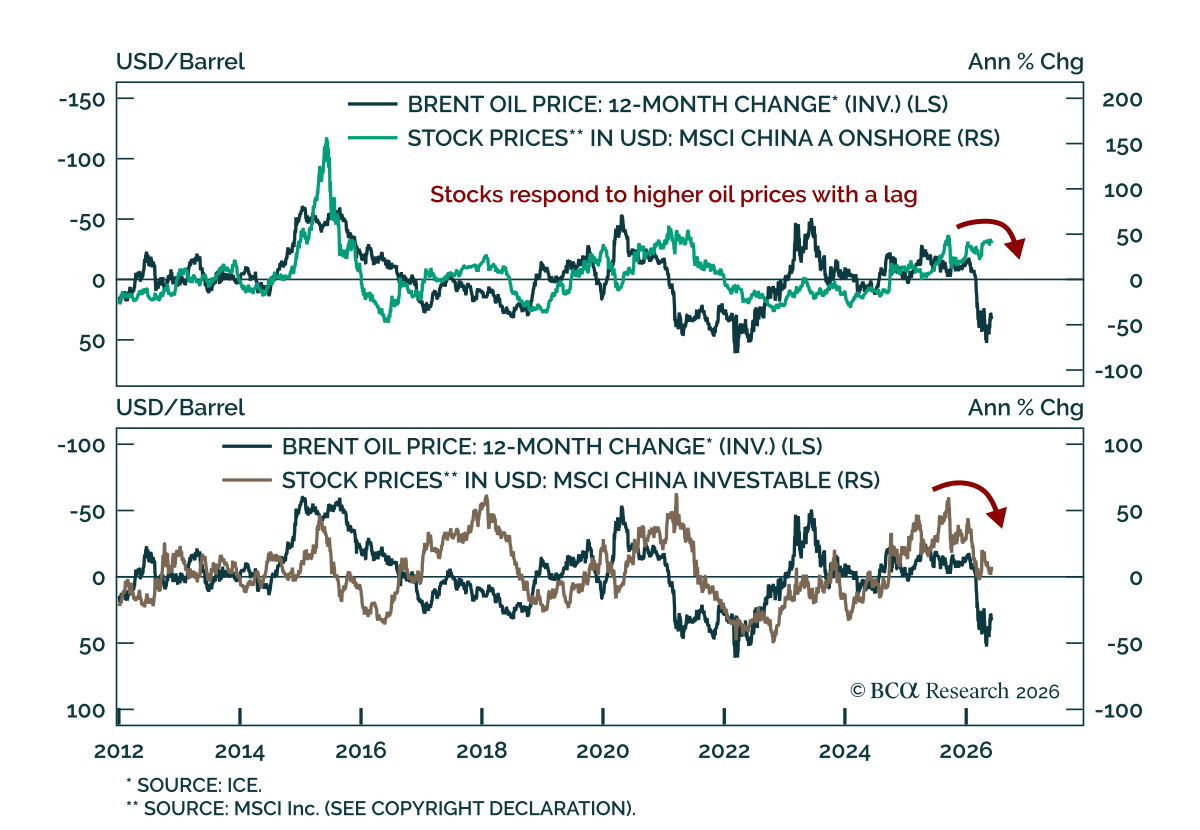

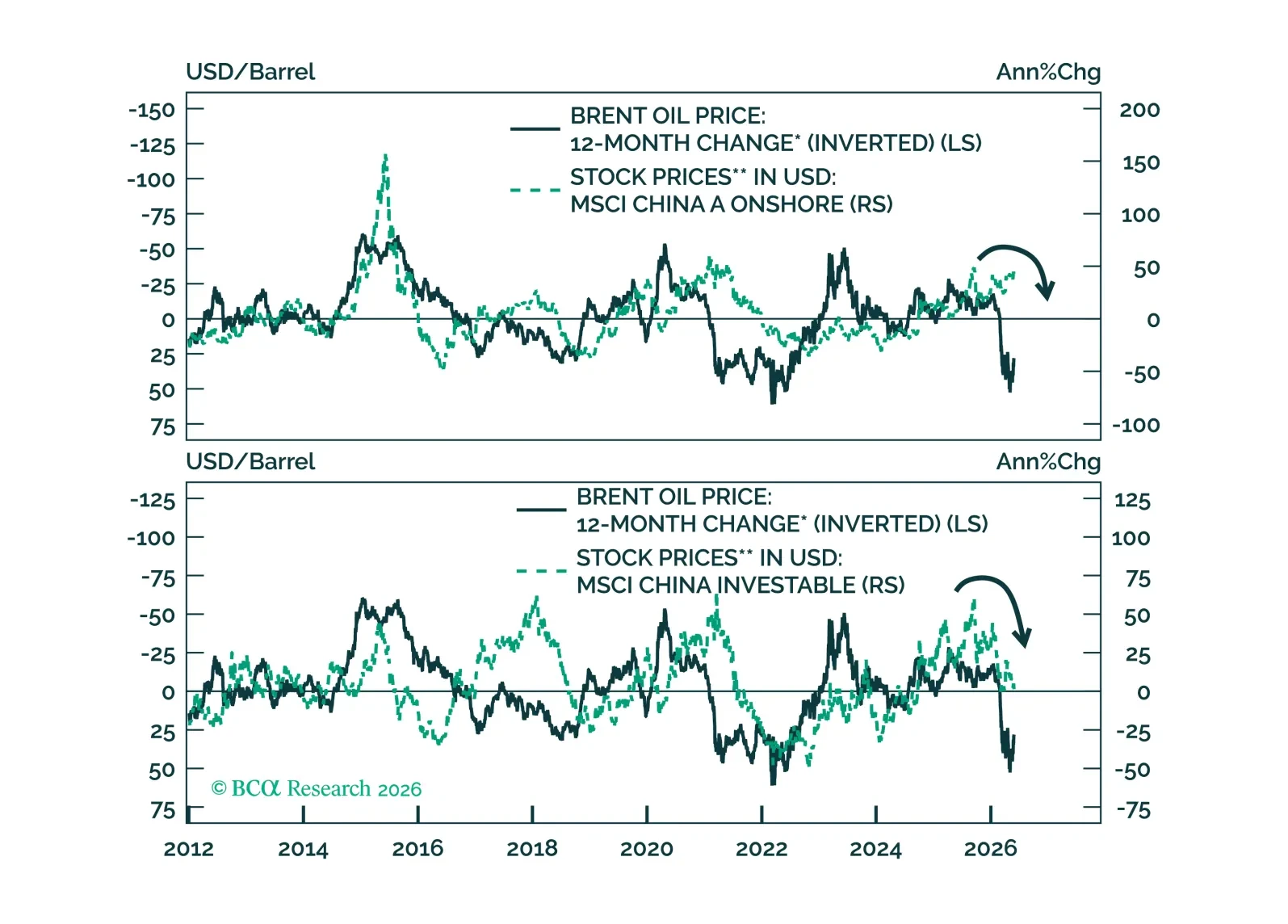

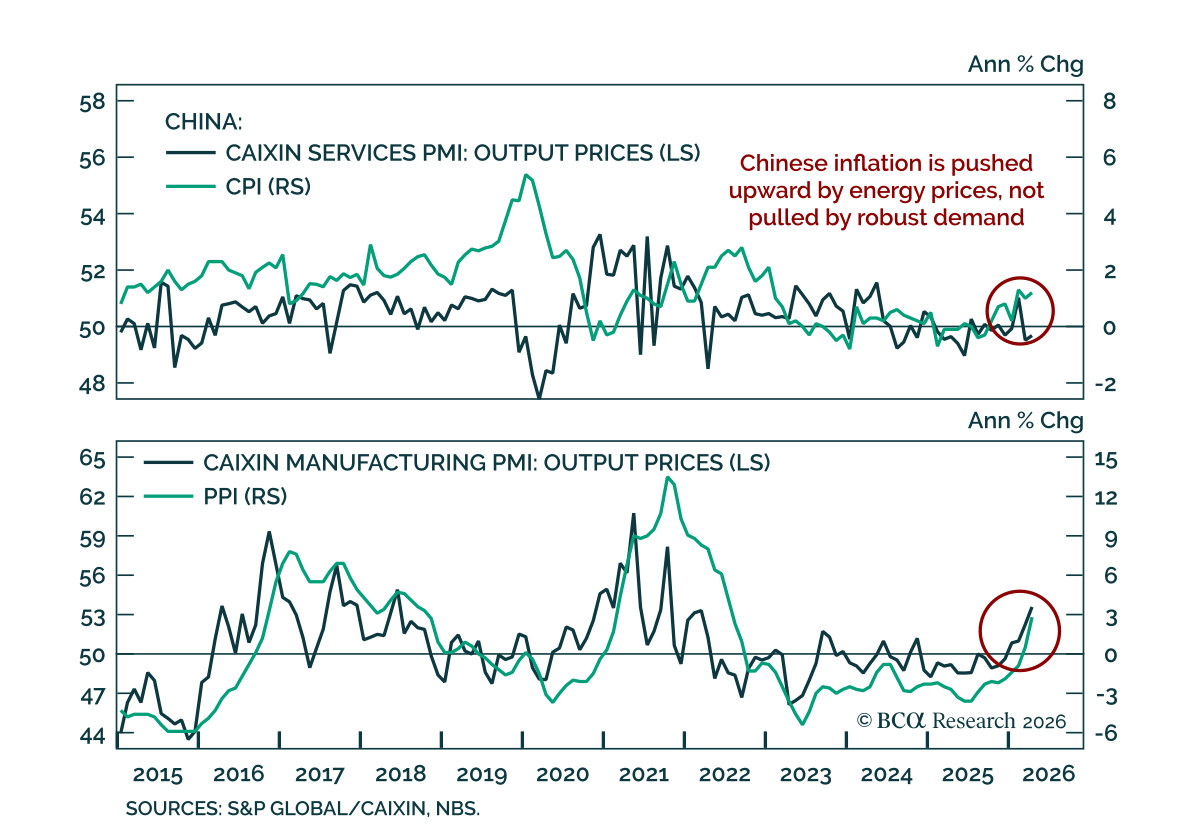

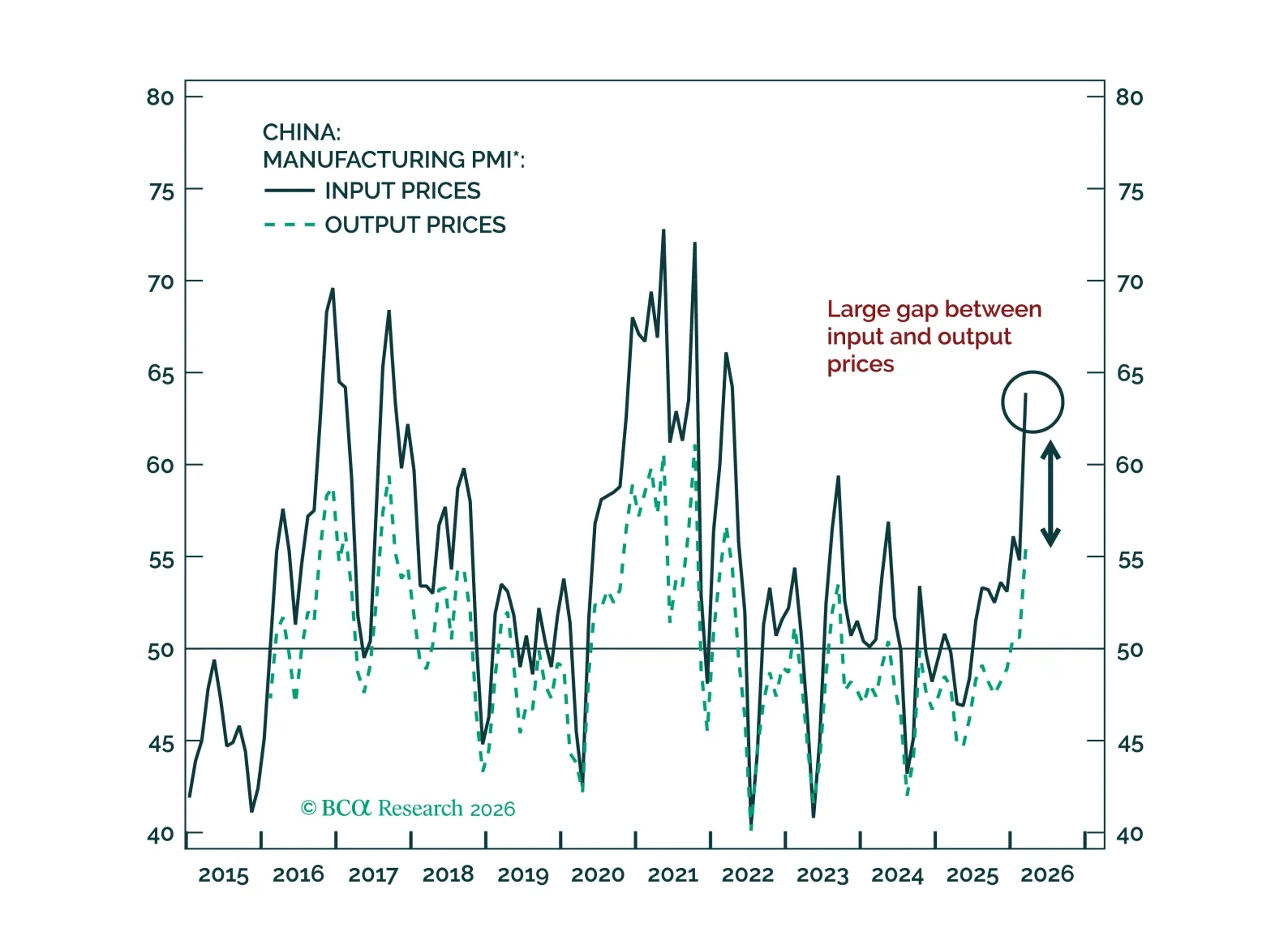

The ceasefire announced on Tuesday may signal peak intensity in the Middle East crisis, but sustained energy price pressures will continue to challenge Chinese corporate profitability.

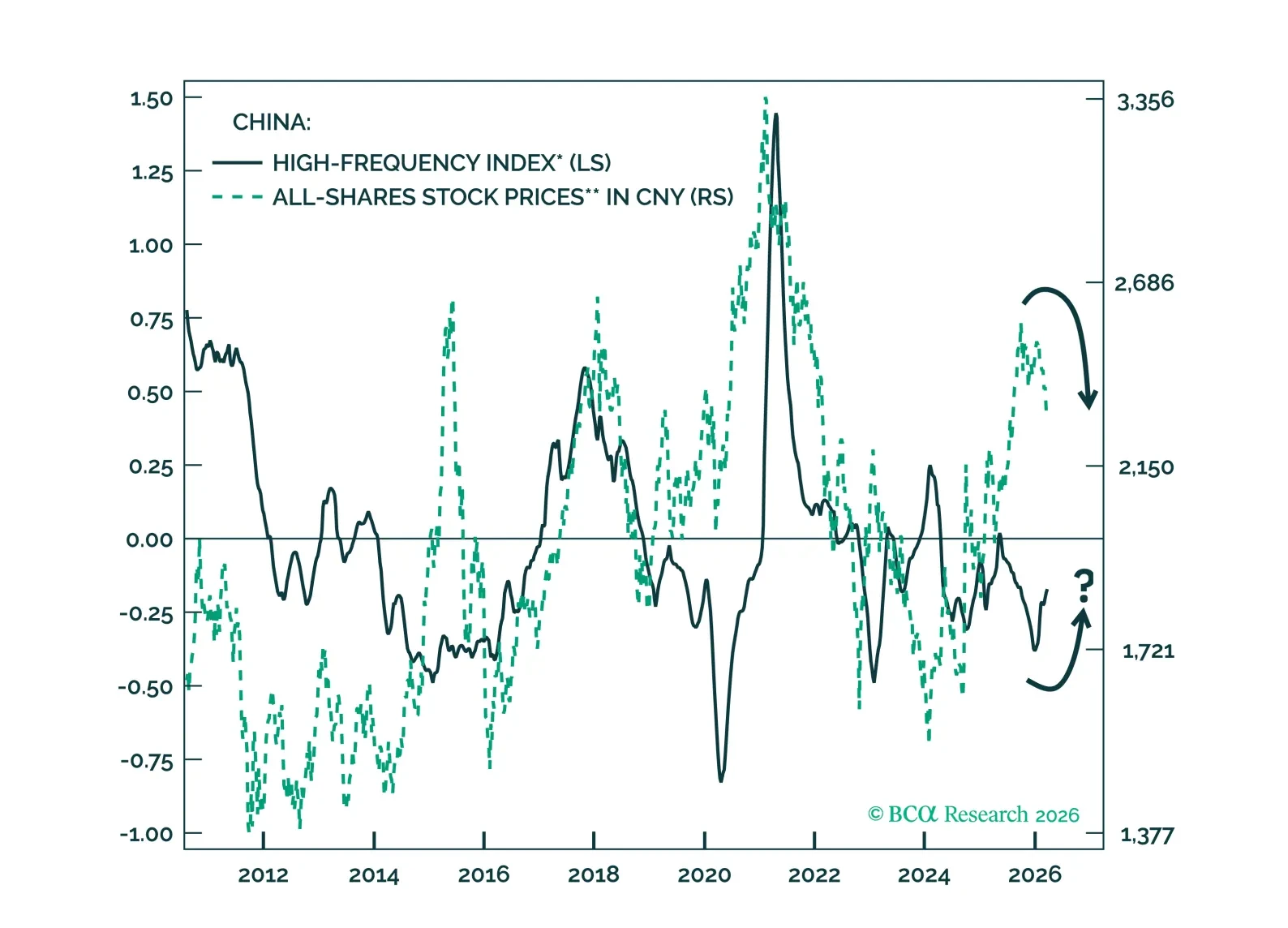

Chinese stock prices are converging with economic growth after a 2025 rally. While the country can endure a short-term oil price shock, it remains susceptible to extended supply disruptions and a global slowdown.