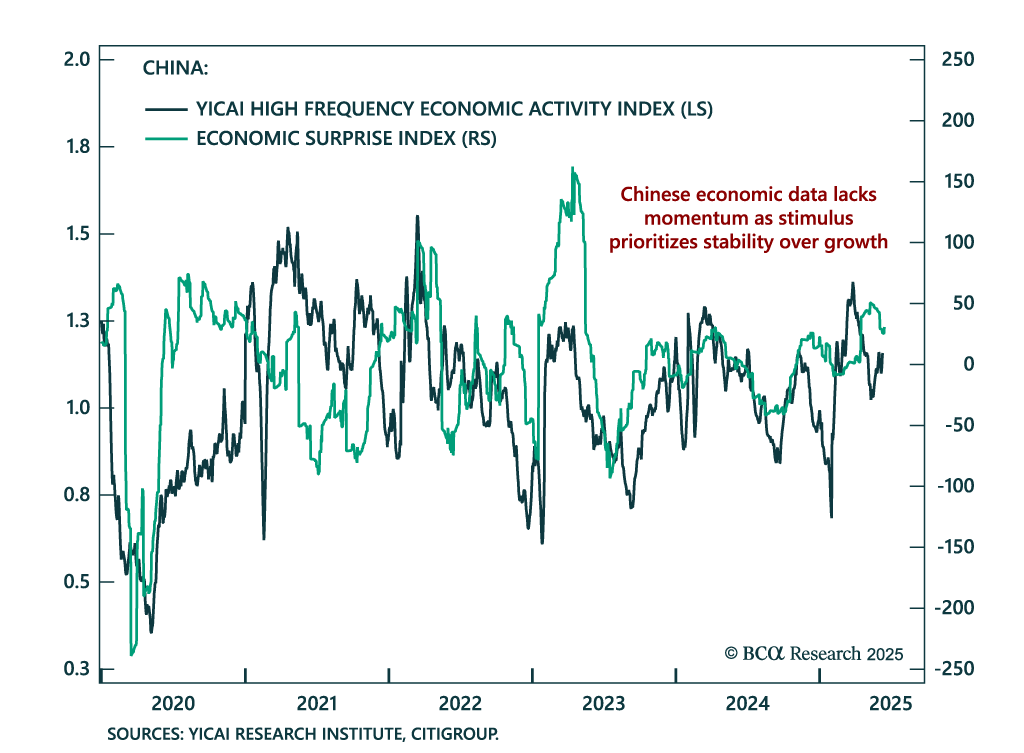

China

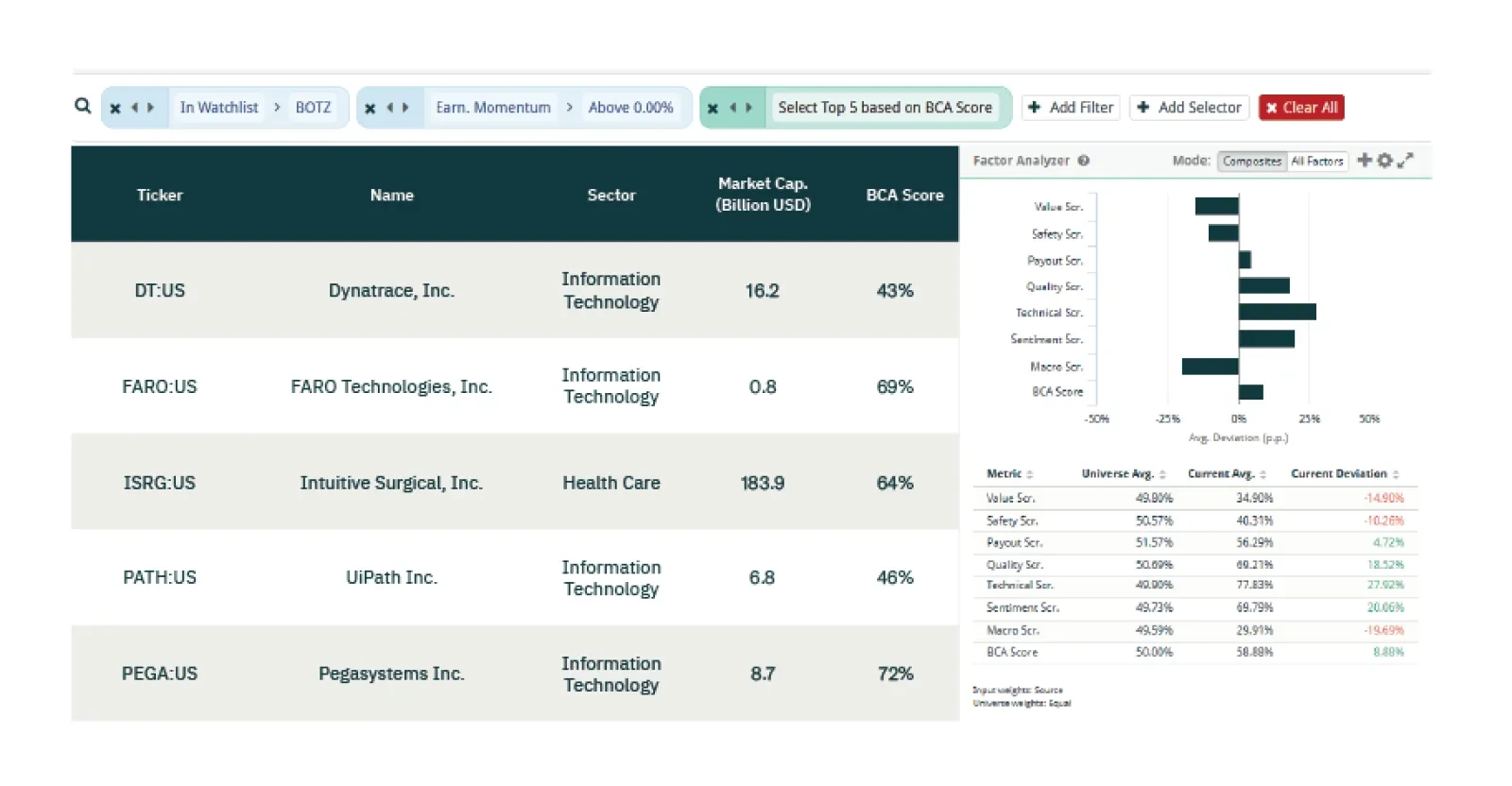

This week our three screeners explore equity trades in Robotics, European Quality and Technical, and Hong Kong.

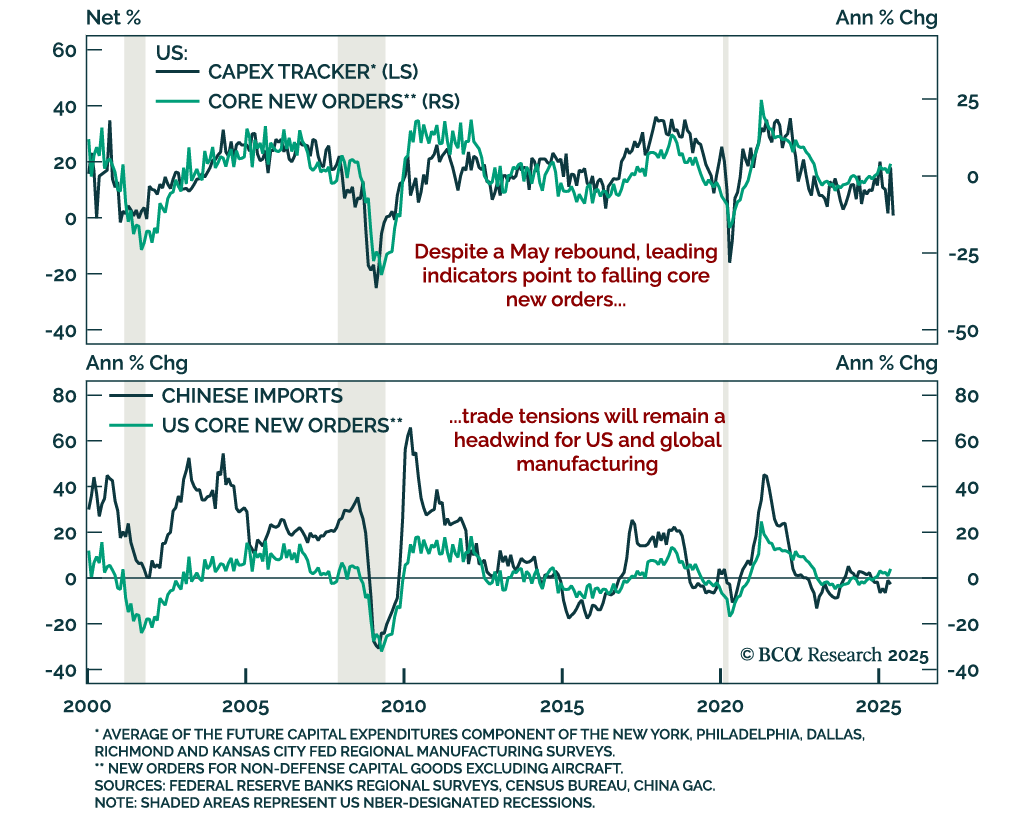

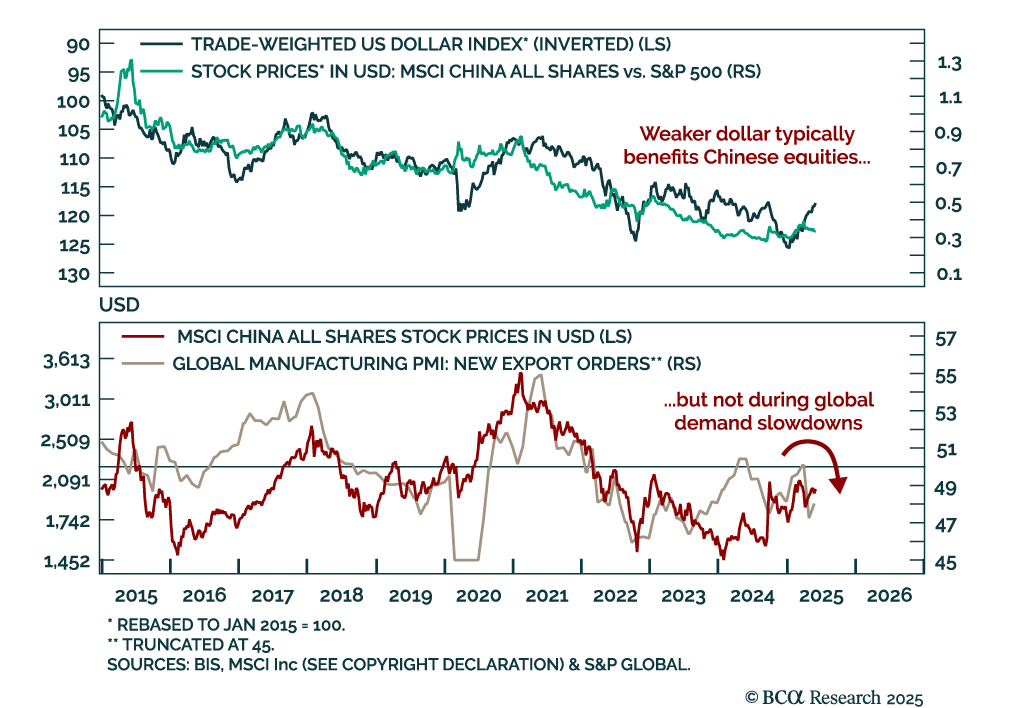

The London Sino-US trade talks offered hope of de-escalation, but Chinese equities remain under pressure from deflationary headwinds and lack a clear macro catalyst to trend higher.

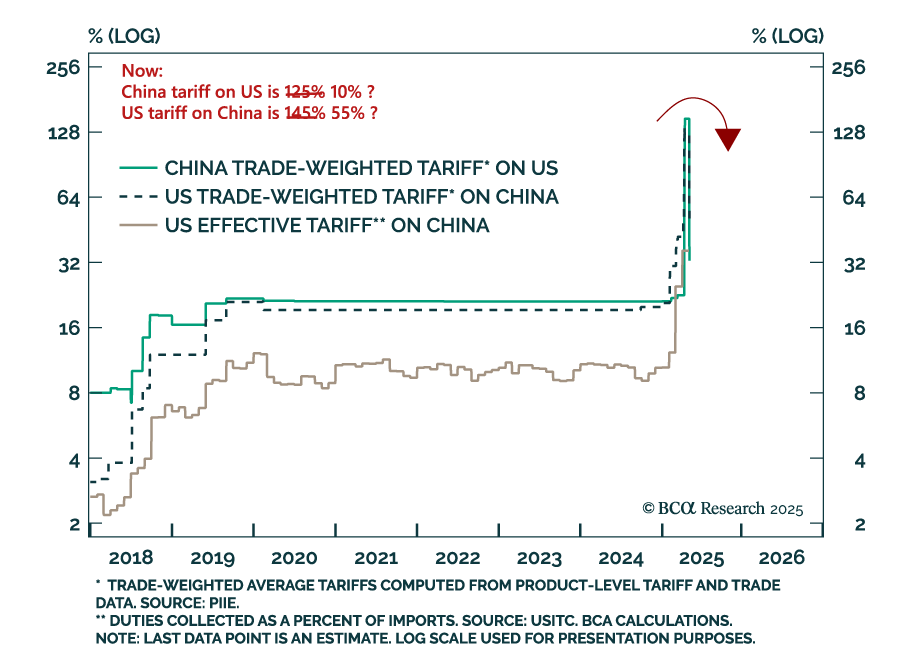

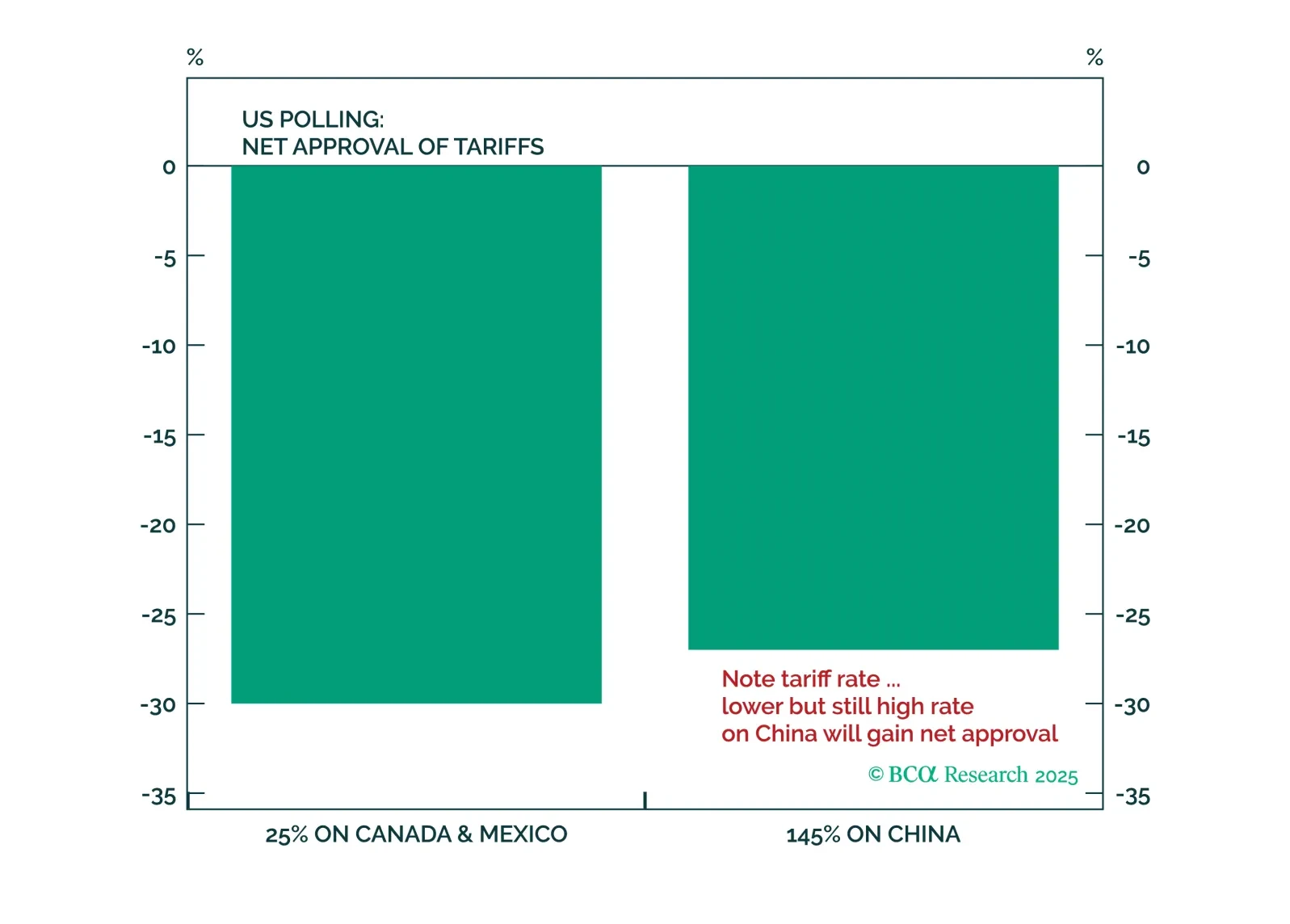

President Trump faces new restrictions on his trade powers coming from the US judicial branch, but they will not prevent him from continuing to restrict trade and investment with China. Rather, they will establish some curbs against entirely arbitrary executive tariffs, especially when wielded against US allies and partners.

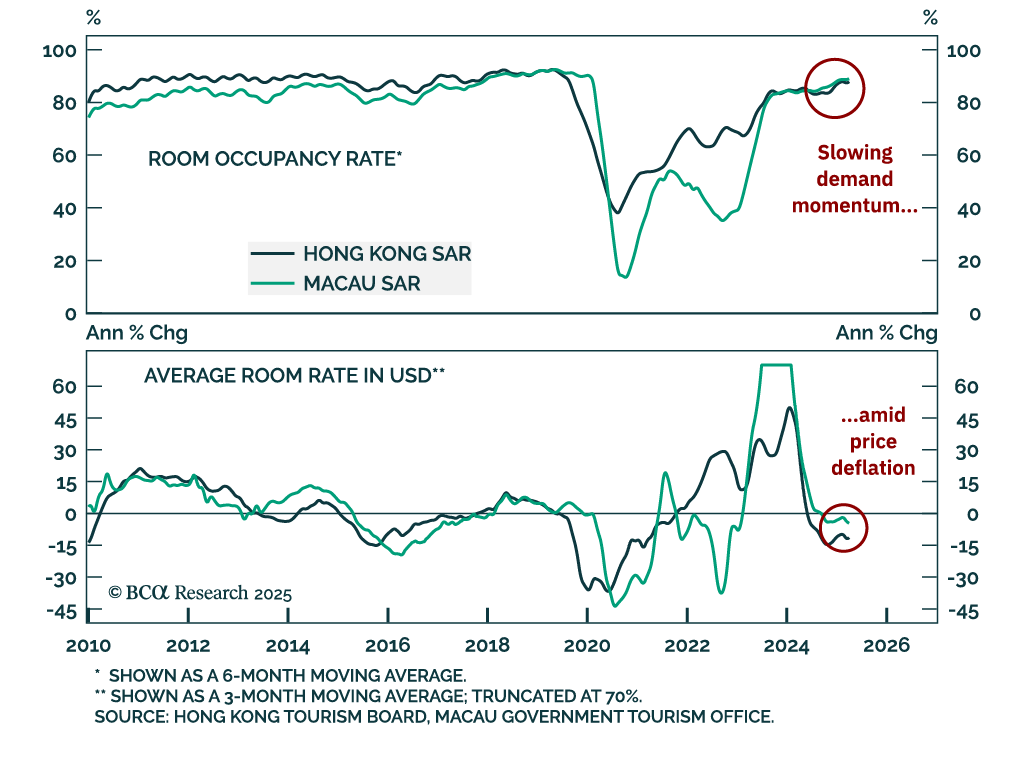

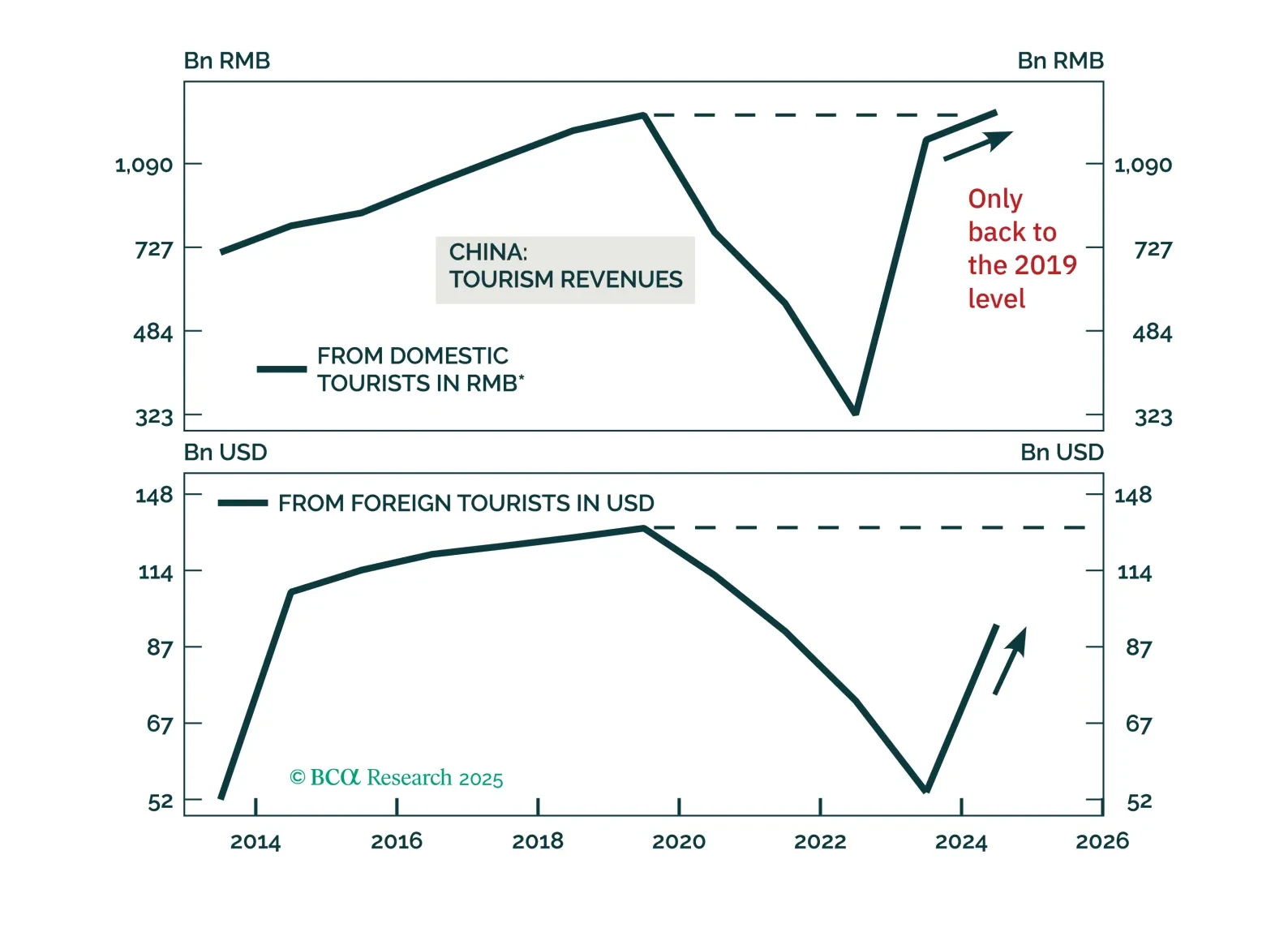

Chinese tourism will continue growing, but investors should be mindful not to overpay for Chinese tourism stocks by extrapolating their past double-digit revenue growth into the future.

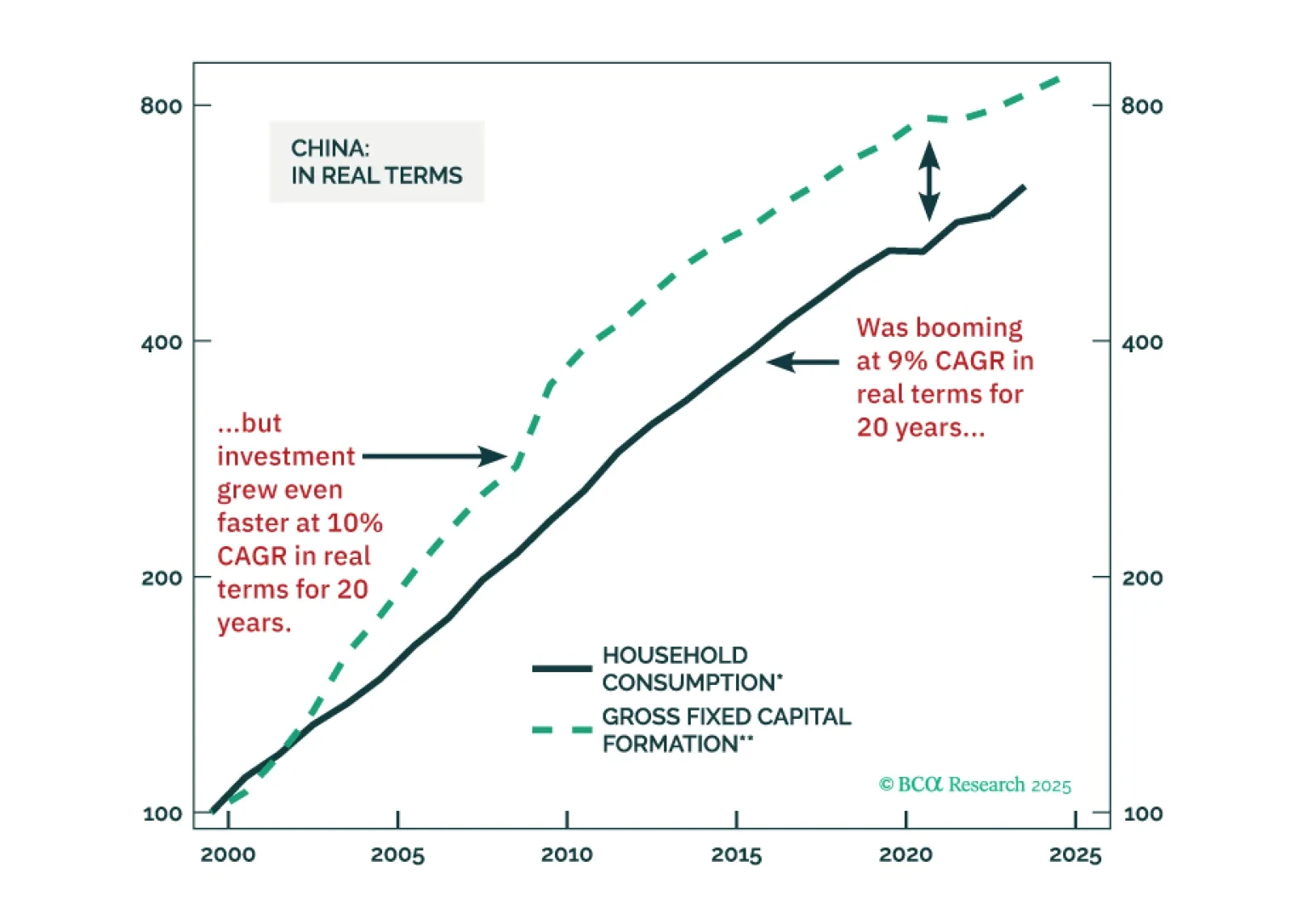

The prevailing narrative around the world is that Chinese households are not spending enough and that China has overly relied on exports for economic growth. Some parts of this conjecture are incorrect. The primary economic imbalance in China is neither inadequate consumption nor outsized exports. The main economic excess is overinvestment.