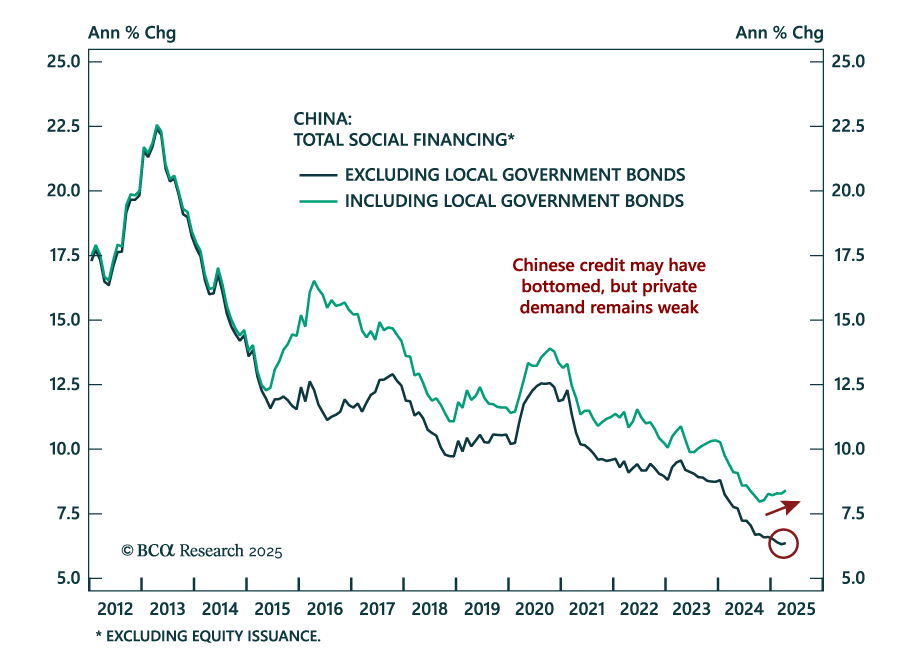

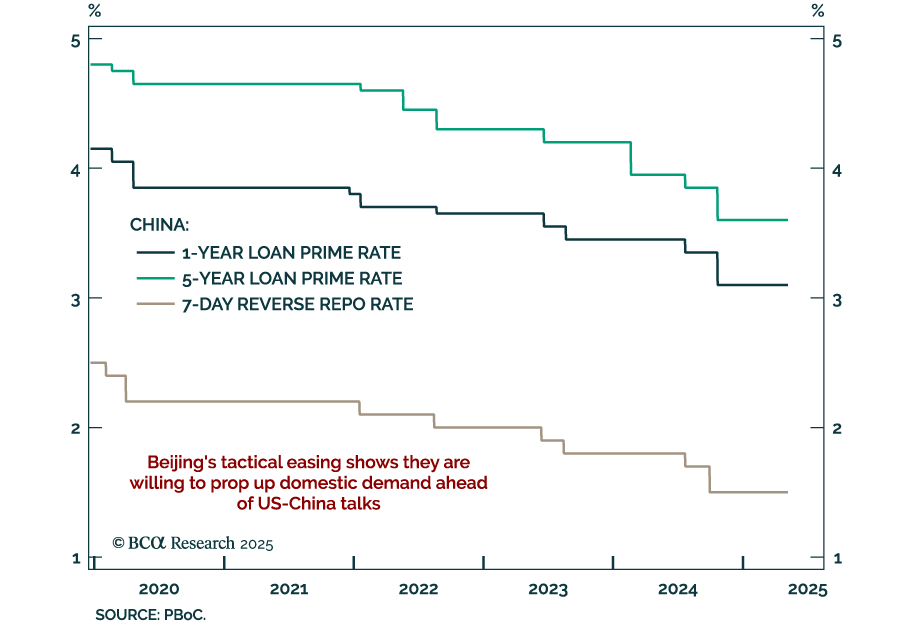

China

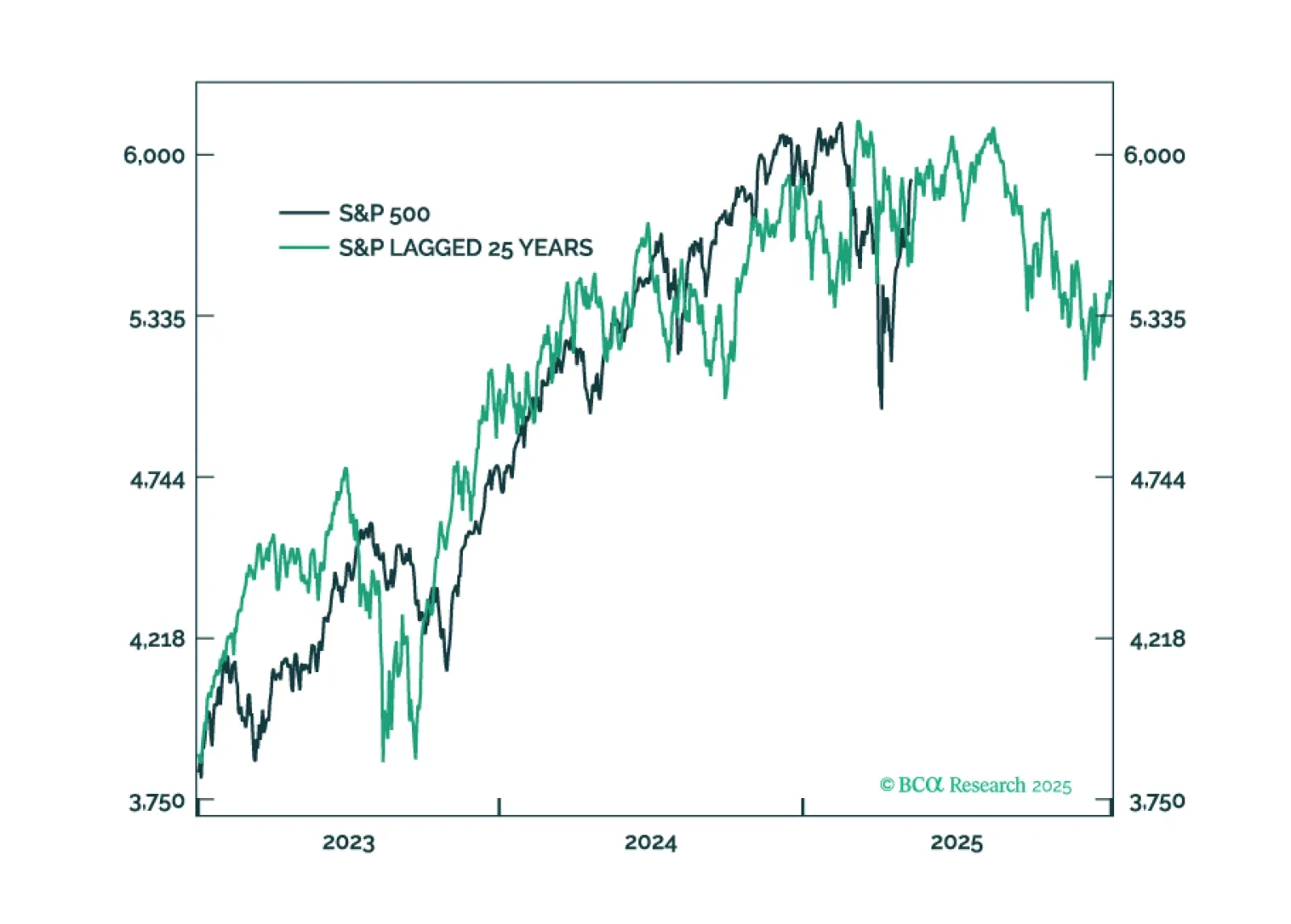

This year’s plunge in tech stocks followed by the recent strong countertrend rally is eerily reminiscent of 2000. But the market and economic parallels between 2025 and in 2000 run much deeper. This report lists 10 striking parallels between 2025 and 2020, then highlights some important differences, and ends by describing how the rest of 2025 might unfold based on a playbook that is: 2025 = ‘2000 with some tweaks.’

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

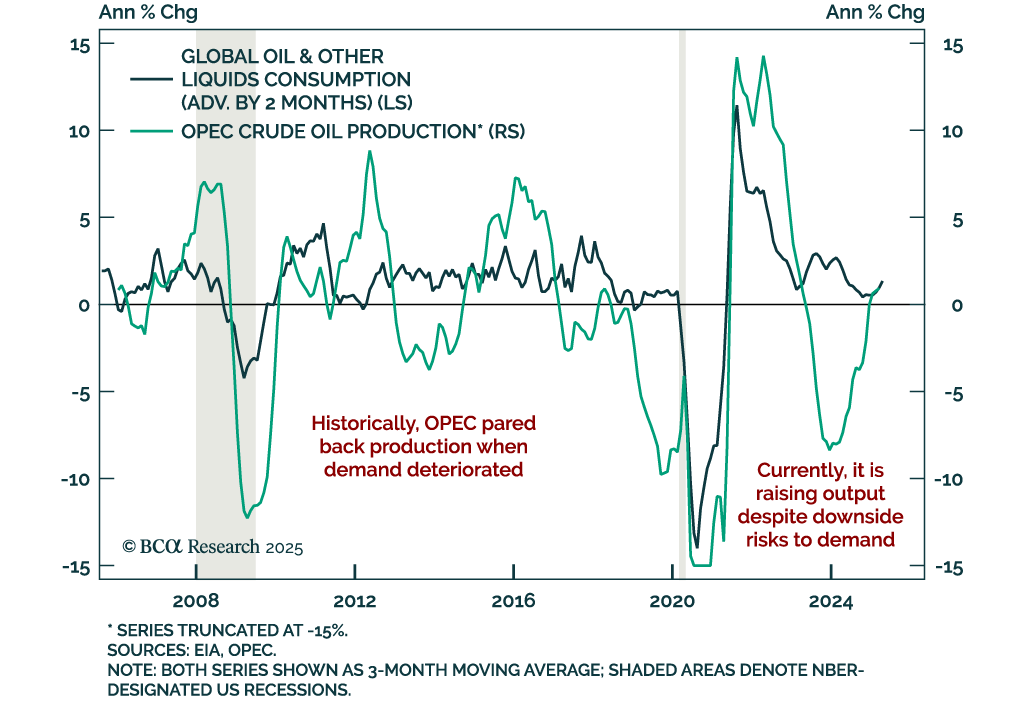

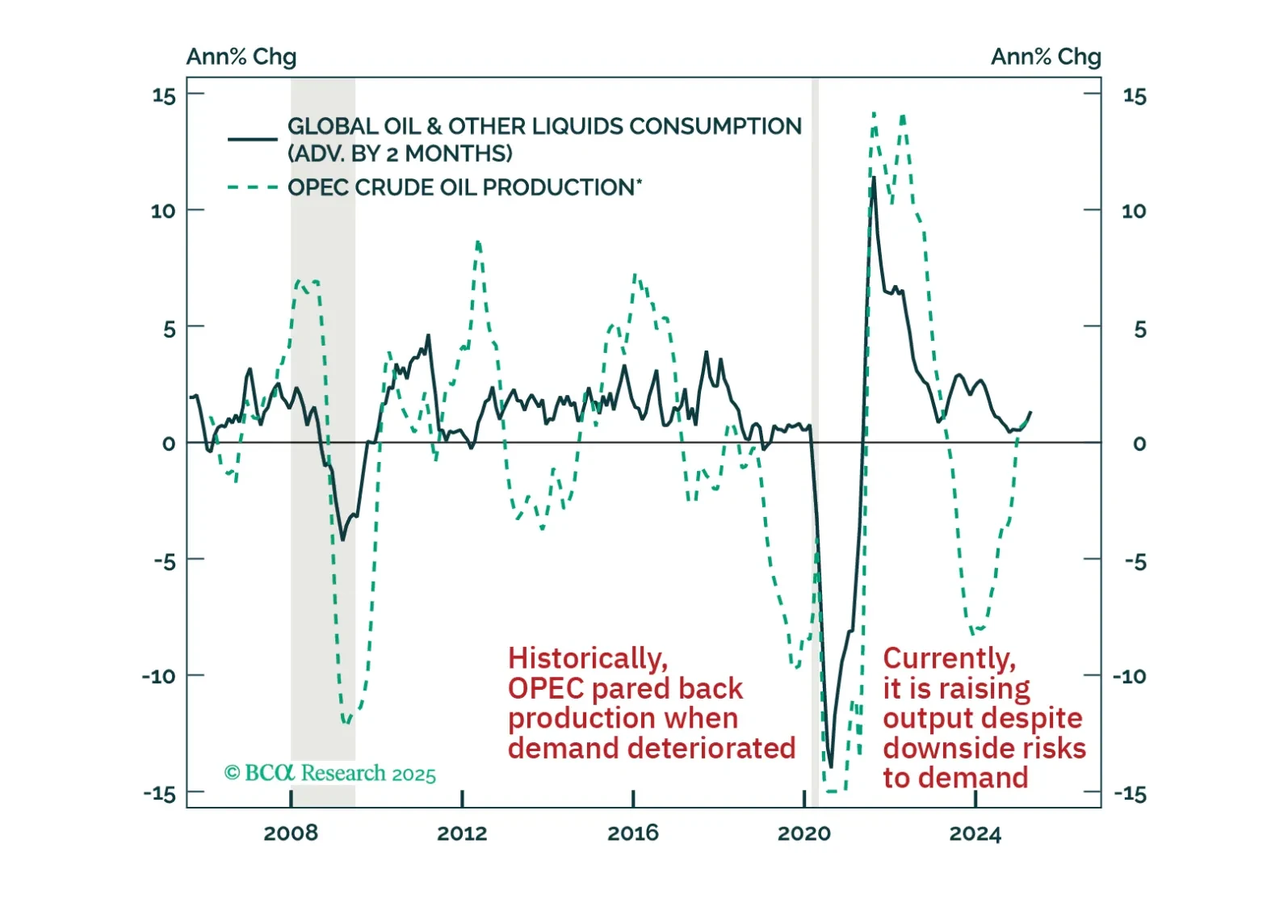

Oil has borne the brunt of the year-to-date deterioration in cyclically sensitive financial assets. It is a key underperformer both within the commodity space and among global risk assets. This underperformance underscores that in addition to the trade war-induced headwind to demand, bearish supply-side developments are also weighing down on crude prices. As we discuss in this report, these dynamics will likely continue exerting downside pressure on oil prices over the coming weeks and months.

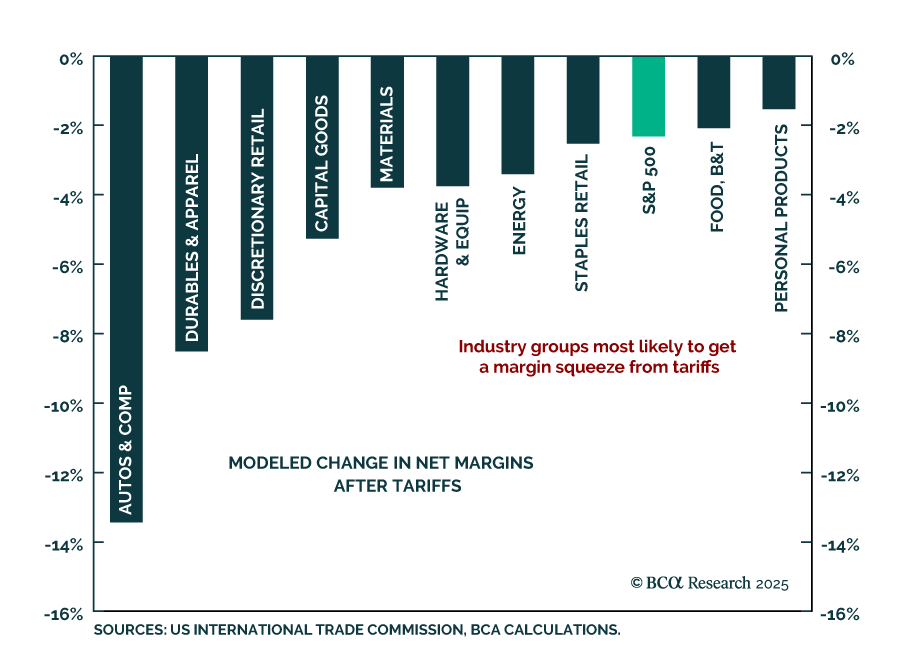

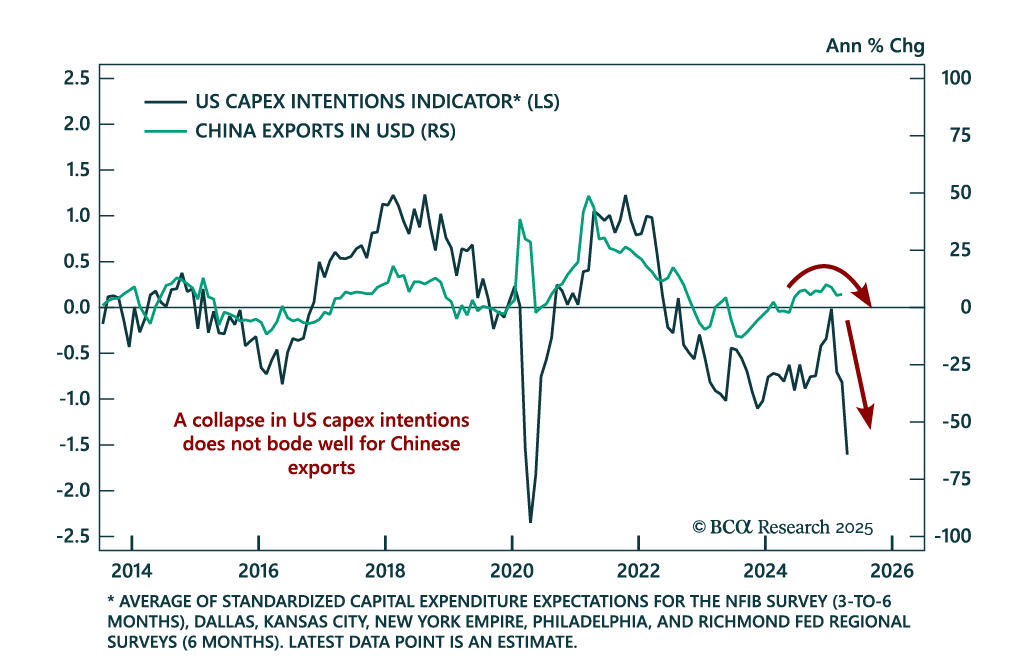

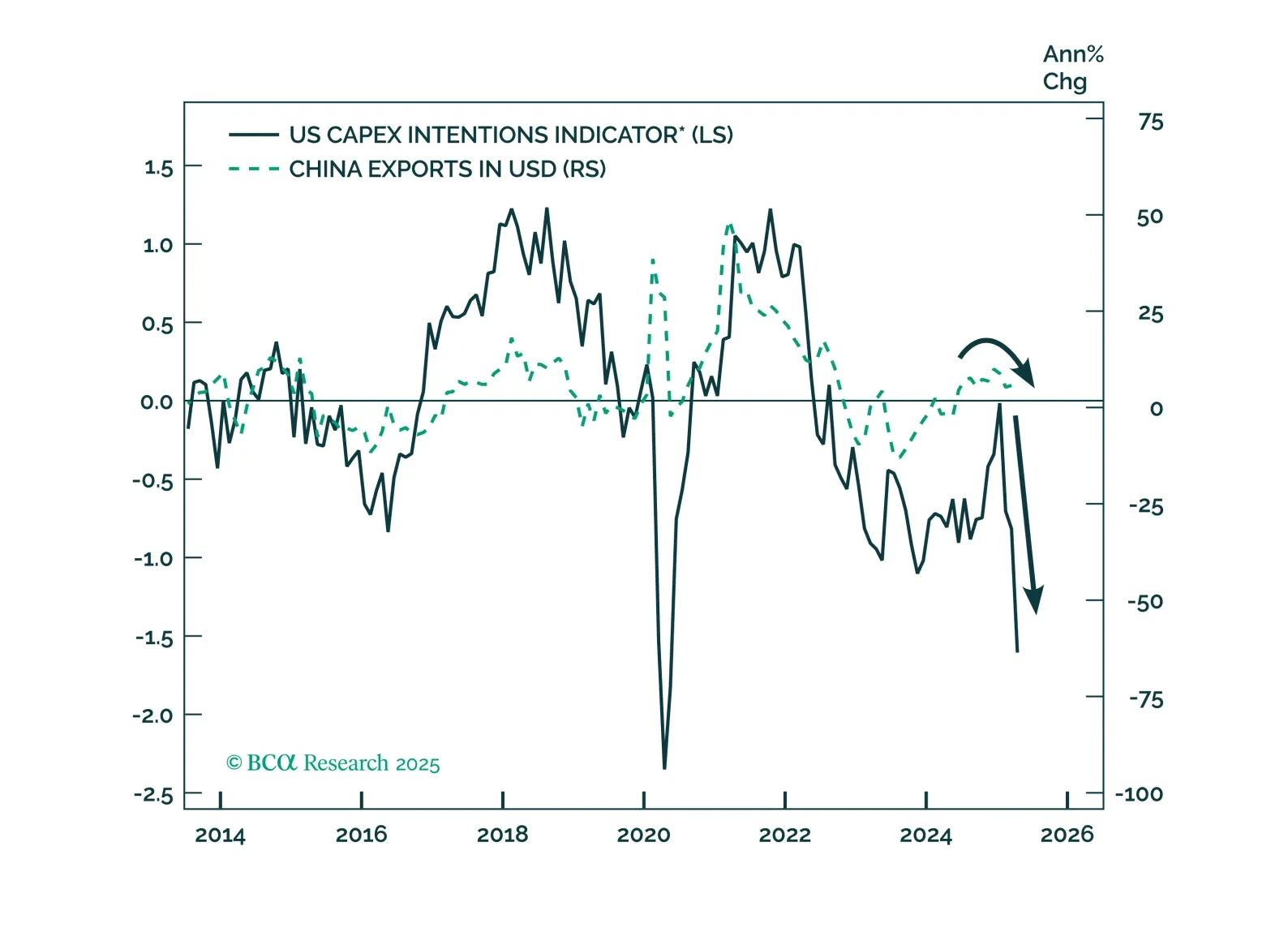

Despite marginal de-escalation in tariffs between the US and China, a sustainable trade agreement remains elusive. In the meantime, economic damage continues to mount, and Chinese equities have yet to fully price in the tariff-induced growth deterioration.

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.