China

Highlights The US is withdrawing from the Middle East and South Asia and making a strategic pivot to Asia Pacific. The third quarter will see risks flare around Iran and the US rejoin the 2015 Iranian nuclear deal. The result is briefly negative for oil prices but the rise of Iran is a new geopolitical trend that will increase Middle Eastern risk over the long run. The geopolitical outlook is dollar bullish, while the macroeconomic outlook is getting less dollar-bearish due to China’s risk of over-tightening policy. Stay neutral USD and be wary of commodities and emerging markets in the third quarter. European political risk is bottoming. The German and French elections are at best minor risks. However, the continent is ripe for negative black swans, especially due to Russian aggression. Go tactically long global large caps and defensives. Feature Chart 1Three Key Views On Track (So Far)

Three Key Views On Track (So Far)

Three Key Views On Track (So Far)

We chose “No Return To Normalcy” as the theme of our 2021 outlook. While the COVID-19 vaccine promised economic recovery, we argued that normalization would create complacency regarding fundamental changes that have taken place in the geopolitical environment. A contradiction between an improving macroeconomic backdrop and a foreboding geopolitical backdrop would develop in 2021 and beyond. The “reflation trade” has begun to lose steam as we go to press. However, global recovery will still be the dominant story in the second half of the year as vaccination spreads. The question for the third quarter and the rest of the year is whether reflation will continue. As a matter of forecasting, we think it will. But as a matter of investment strategy, we are taking a more defensive stance until China relaxes economic policy. In our annual outlook we highlighted three key geopolitical views: (1) China’s headwinds, both at home and abroad (2) US détente with Iran and pivot to Asia (3) Europe’s opportunity. All three trends are broadly on track and can be illustrated by looking at equity performance in the relevant regions for the year so far: Chinese stocks sold off, UAE stocks rallied, and European stocks rallied (Chart 1). However, these trends are not exclusively tied to absolute equity performance. The most important question is what happens to global growth and the US dollar as these three key views continue. Stay Neutral On The Dollar It paid off for us to maintain a neutral stance on the dollar. True, the global recovery and exorbitant US trade and budget deficits are bearish for the dollar and bullish for other currencies. But the greenback’s “counter-trend bounce” is proving more formidable than many investors expected. The fundamentals of the American economy and global position remain strong. Since the outbreak of COVID-19, the US has secured its recovery with fiscal policy, maintained rule of law amid a contested election, innovated and distributed vaccines, benefited from more flexible social restrictions, refurbished global alliances, and put pressure on its geopolitical rivals. In essence, the combined effect of President Trump’s and Biden’s policies has been to make America “great again” (Chart 2). From a geopolitical perspective, the dollar is appealing. Chart 2Trump-Biden Make America Great Again?

Trump-Biden Make America Great Again?

Trump-Biden Make America Great Again?

In addition, the first two geopolitical views mentioned above – China’s headwinds and the US-Iran détente – imply a negative environment for China and the renminbi. The reason for the US to do a suboptimal deal with Iran, both in 2015 and 2021, is to reduce the risk of war and buy time to enable a strategic pivot to Asia Pacific. Three US presidents have been elected on the pledge to conclude the “forever wars” in the Middle East and South Asia. Biden is withdrawing US troops from Afghanistan in September. There can be little doubt Biden is committed to an Iran deal, which is supposed to free up the US’s hands (Chart 3). Meanwhile the US public and Congress are unified in their desire to better defend US interests against China’s economic and military rise. There has not yet been a stabilization of US-China policies. Biden is not likely to hold a summit with Chinese President Xi Jinping until late October at earliest – and that is a guess, not a confirmed summit. The Biden administration has completed its review of China policy and is maintaining the Trump administration’s hawkish posture, as predicted. The US and China may resume their strategic and economic dialogue at some point but it is impossible to go back to the status quo ante 2015. That was the year the US adopted a more confrontational stance toward China – a stance later supercharged by Trump’s election and trade tariffs. The hawkish consensus on China is one of the rare unifying factors in a deeply divided America. The Biden administration explicitly says the US-China relationship is now defined by “competition” instead of “engagement.”1 One exception to this neutral view on the dollar has been our decision to go long the Japanese yen and Swiss franc, which has not panned out so far. Our reasoning is that geopolitical risk will boost these currencies but otherwise the reduction of geopolitical risk will weigh on the dollar in the context of global growth recovery. So far geopolitical risk has remained subdued while the US dollar has outperformed. We are still sympathetic to these safe-haven currencies, however, as they are attractively valued as long as one expects geopolitical risks to materialize (Chart 4). Chart 3US Pivot To Asia Runs Through Iran

US Pivot To Asia Runs Through Iran

US Pivot To Asia Runs Through Iran

Our third key view, that EU was the real winner of the US election last year, remains on track. This is marginally positive for the euro at the expense of the dollar. Given the above points, we favor an equal-weighted basket of the euro and the dollar relative to the renminbi (Chart 5). Chart 4Safe-Haven Currencies Attractive

Safe-Haven Currencies Attractive

Safe-Haven Currencies Attractive

Chart 5Favor Euro And Dollar Over Renminbi

Favor Euro And Dollar Over Renminbi

Favor Euro And Dollar Over Renminbi

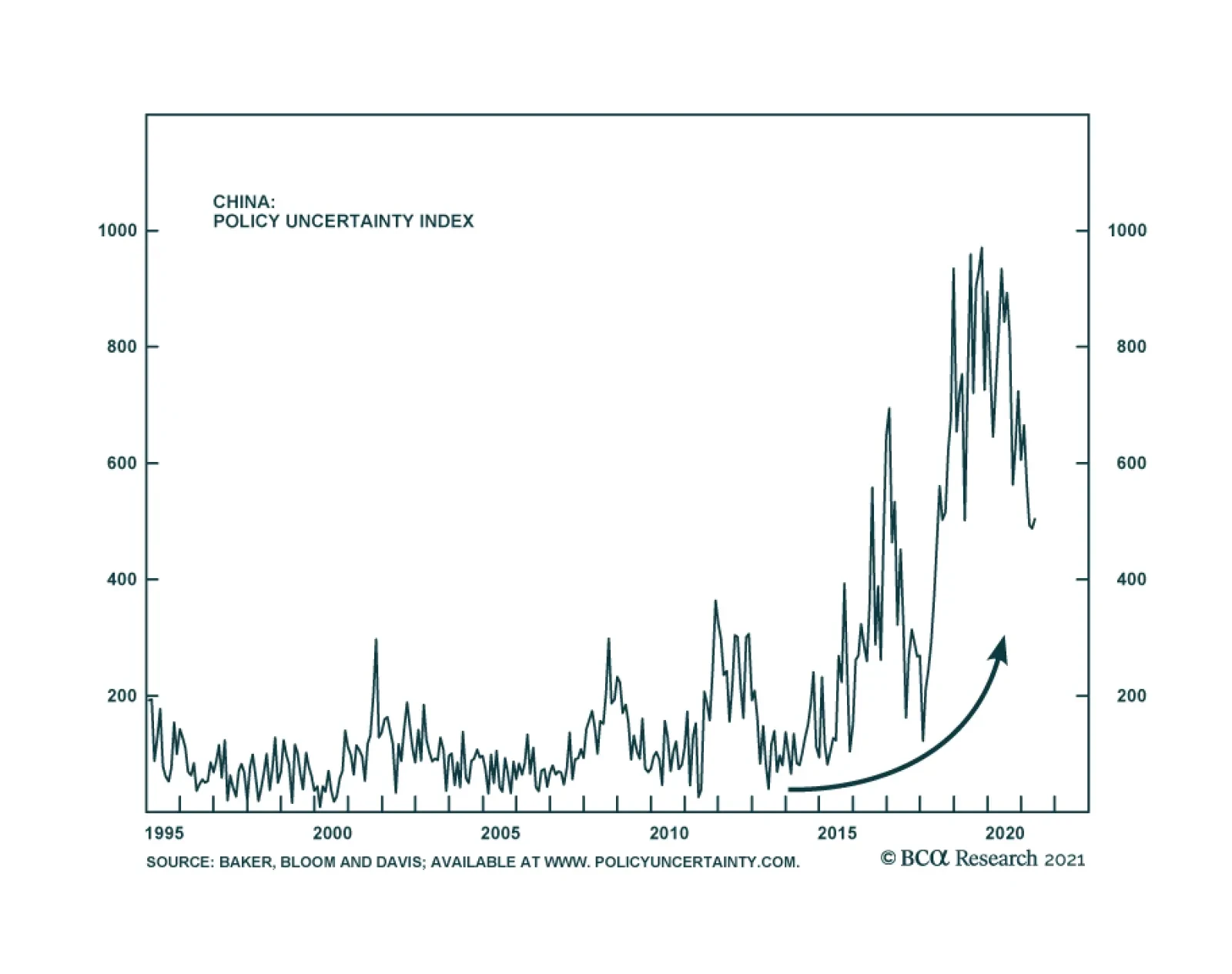

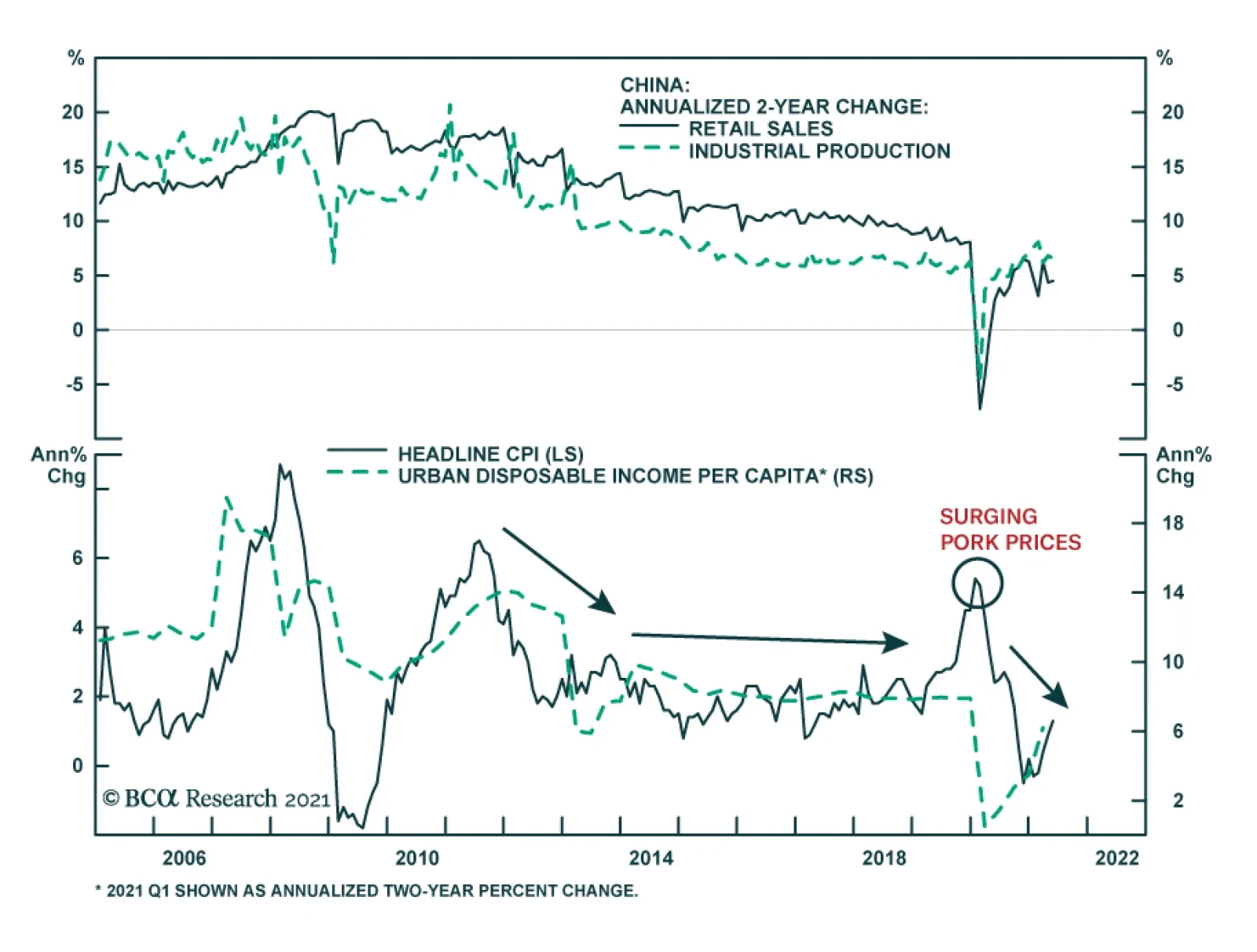

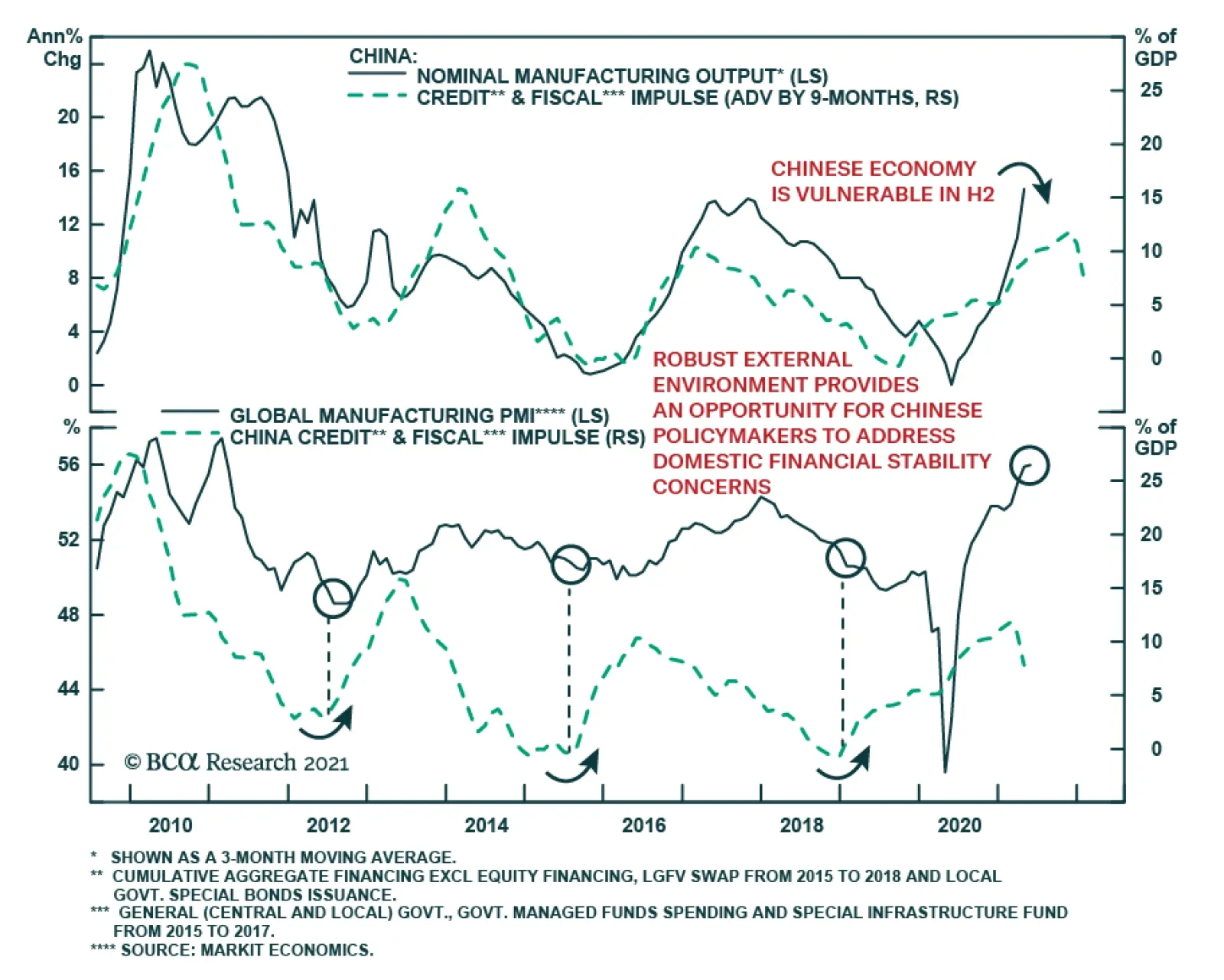

The geopolitical outlook is dollar-bullish. The macroeconomic outlook is dollar-bearish, except that China’s economy looks to slow down. We expect China to ease policy in the second half of the year but it may come late. We remain neutral dollar in the third quarter. Wait For China To Relax Policy July 1 marks the centenary of the Communist Party of China. The main thing investors should know is that the Communist Party predates China’s capitalist phase by sixty years. The party adopted capitalism to improve the economy – it never sacrificed its political or foreign policy goals. This poses a major geopolitical problem today because the Communist Party’s consolidation of power across Greater China, symbolized by Beijing’s revocation of Hong Kong’s special status in 2019, has convinced the western democracies that China is no longer compatible with the liberal world order. China launched a 13.8% of GDP monetary-and-fiscal stimulus over 2018-20 due to the trade war and COVID-19 pandemic. So the economy is stable for the hundredth anniversary celebration. The centenary goals are largely accomplished: GDP is larger, poverty is nearly extinguished, although urban incomes are still lagging (Chart 6). General Secretary Xi Jinping will mark the occasion with a speech. The speech will contribute to his governing philosophy, Xi Jinping Thought, a synthesis of communist Mao Zedong Thought and the pro-capitalist “socialism with Chinese characteristics” pioneered by General Secretary Deng Xiaoping in the 1980s-90s. The effect is to reassert Communist Party and central government primacy after the long period of decentralization that enabled China’s rapid growth phase. It is also to endorse an inward economic turn after the four-decade export-manufacturing boom. The Xi administration’s re-centralization of policy has entailed mini-cycles of tightening and loosening control over the economy. The administration leans against the country’s tendency to gorge itself on debt and grow at any cost – until it must lean the other way for fear of triggering a destabilizing slowdown. For this reason Beijing tightened policy proactively last year, producing a sharp drop in money, credit, and fiscal expansion in 2021 that now threatens to undermine the global recovery. By our measures, any further tightening will result in undershooting the regime’s money and credit targets, i.e. overtightening, and hence threaten to drag on the global recovery (Chart 7). Chart 6China's Communist Party Centenary Goals

China's Communist Party Centenary Goals

China's Communist Party Centenary Goals

Chart 7China Verges On Over-Tightening Policy

China Verges On Over-Tightening Policy

China Verges On Over-Tightening Policy

Overtightening would be a policy mistake with potentially disastrous consequences. So the base case should be that the government will relax policy rather than undermine the post-COVID recovery. However, investors cannot be confident about the timing. The 2015 financial turmoil and renminbi devaluation occurred because policymakers reacted too slowly. One reason to believe policy will be eased is that after July 1 the government will turn its attention to the twentieth national party congress in 2022, the once-in-five-years rotation of the Central Committee and Politburo. The party congress begins at the local level at the beginning of next year and culminates in the fall of 2022 with the national rotation of top party leaders. Xi Jinping was originally slated to step down in 2022. So he needs to squash any last-minute push against him by opposing factions of the party. He may have himself named chairman of the Communist Party, like Mao before him. Most importantly he will put his stamp on the “seventh generation” of China’s leaders by promoting his followers into key positions. All of this suggests that the Xi administration cannot risk triggering a recession, even if its preferences remain hawkish on economic policy. Policy easing could come as early as the end of July. As a rule of thumb, we have noticed that the Politburo’s July meeting on economic policy is often an inflection point, as was the case in 2007, 2015, 2018, and 2020 (Table 1). Some observers claim the April Politburo meeting already signaled an easing in policy, although we do not see that. If July clearly signals relaxation, global investors will cheer and emerging market assets and commodities will rise. Table 1China’s Politburo Often Hits Inflection Point On Economic Policy In July

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Still we maintain a defensive posture going into the third quarter because we do not have a high level of confidence that policymakers will act preemptively. A market riot may precede and motivate the inflection point in policy. Also the negative impact of previous policy tightening will be felt in the third quarter. China plays and industrial metals are extremely vulnerable to further correction (Chart 8). Chart 8China Plays And Metals Vulnerable To Further Correction

China Plays And Metals Vulnerable To Further Correction

China Plays And Metals Vulnerable To Further Correction

The earliest occasion for a Biden-Xi summit comes at the end of October, as mentioned. While US-China talks will occur at some level, relations will remain fundamentally unstable. While a Biden-Xi summit may improve the atmosphere and lead to a new round of strategic and economic dialogue, or Phase Two trade talks, the fact is that the US is seeking to contain China’s rise and China is seeking to break out of the strictures of the US-led world order. The global elite and mainstream media will put a lot of emphasis on the post-Trump return to diplomatic “normalcy” and summits. But this is to overemphasize style at the expense of substance. Note that the positive feelings of the Biden-Putin summit on June 16 fizzled in less than a week when Russia allegedly dropped bombs in the path of a British destroyer in the Black Sea. The US and UK were training Ukraine’s military. Britain denies any bombs were dropped but Russia says next time they will hit their target. (More on this below.) This episode is instructive for US-China relations: summitry is overrated. China is building a sphere of influence and the US no longer believes dialogue alone is the answer. Tit-for-tat punitive measures and proxy battles in China’s neighboring areas, from the Korean peninsula to the Taiwan Strait to the South and East China Seas, are the new normal. Bottom Line: Tactically, stay defensive on global risk assets, especially China plays. Strategically, maintain a constructive outlook on the cycle given the global recovery and China’s need eventually to relax monetary and fiscal policy. US-Iran Deal Likely – Then The Real Trouble Starts The US will likely rejoin the 2015 Iranian nuclear deal (Joint Comprehensive Plan of Action) by August and pull out of its longest-ever war in Afghanistan in September. The US is wrapping up its “forever wars” to meet the demands of a war-weary public. Ironically, the long-term consequence is to create power vacuums that invite new geopolitical conflicts in the context of the US’s great power struggle with China and Russia. But for now a deal with Iran – once it is settled – reduces geopolitical risk by reducing the odds of military escalation in the region. The Iran talks are more significant than the Afghanistan pullout. We are confident in a deal because Biden can rejoin the 2015 deal unilaterally – it was never approved by the US Senate as a formal treaty. The Iranians will not support any militant action so aggressive as to scupper a deal that offers them the chance of reviving their economy at a critical time in the regime’s history. Reviving the deal poses a downside risk for oil prices in the third quarter though not over the long run. It is negative in the short run because investors will have to price not only Iran’s current and future production (Chart 9) but also any resulting loss of OPEC 2.0 discipline. Brent crude is trading at $76 per barrel as we go to press, above the $65-$70 per barrel average that our Commodity & Energy Strategy service expects to see over the coming five years (Chart 10). Chart 9Iran's Oil Production Will Return

Iran's Oil Production Will Return

Iran's Oil Production Will Return

Chart 10Brent Price Faces Short-Term Downside Risk From Iranian Crude

Brent Price Faces Short-Term Downside Risk From Iranian Crude

Brent Price Faces Short-Term Downside Risk From Iranian Crude

The oil price ceiling is enforced by the cartel of oil producers who fear that too high of prices will incentivize US shale oil production as well as the global shift to renewable energy. The Russians have always dragged their feet over oil production cuts and are now pushing for production hikes. The government needs an oil price of around $50-55 per barrel for the budget to break even. The Saudis need higher prices to break even, at $70-75 per barrel. Moscow must coordinate various oil producers, led by the country’s powerful oligarchs and their factions, which is inherently more difficult than the Saudi position of coordinating one producer, Aramco. The Russians and Saudis have maintained cartel discipline so far in 2021, as expected, because the wounds of the market-share war last year are still raw. They retreated from that showdown in less than a month. However, a major escalation in Saudi Arabia’s strategic conflict with Iran could push the Saudis to seek greater market share at Iran’s expense, as occurred before the original Iran deal in 2014-15. Hence our view that the risk to oil prices will shift from the upside to the downside in the second half of the year if the US-Iran deal is reconstituted. Over the long run, the deal is not negative for oil prices. The deal is a tradeoff for lower geopolitical risk today but higher risk in the future. The reason is that Iran’s economic recovery will strengthen its strategic hand and generate a backlash in the region. The global oil supply and demand balance will fluctuate according to circumstances but regional conflict will inject a risk premium over time. Biden’s likely decision to rejoin the 2015 deal should be seen as a delaying tactic. It is impossible to go back to 2015, when the US had mustered a coalition of nations to pressure Iran and when Iran’s “reformist” faction stood to receive a historic boost from the opening of the country’s economy. Now the US lacks a coalition and the reformists are leaving office in disgrace, with the hardliners (“principlists”) taking full power for the foreseeable future. Iran is happy to go back to complying with a deal that consists of sanctions relief in exchange for temporary limits on its nuclear program. The 2015 deal’s restrictions on Iran’s nuclear program begin expiring in 2023 and continue to expire through 2040. Biden has no chance of negotiating a newer and more expansive deal that extends these sunset clauses while also restricting Iran’s ballistic missile program and regional militant activities. He will say that easing sanctions is premised on a broader “follow on” deal to achieve these US goals. But the broader deal is unlikely to materialize anytime soon. The Iranians will commit to future talks but they will have no intention of agreeing to a more expansive deal unless forced. The country’s leaders will never abandon their nuclear program after witnessing the invasions of non-nuclear Libya and Ukraine – in stark contrast with nuclear-armed North Korea. Moreover Biden cannot possibly reassemble the P5+1 coalition with Russia and China anytime soon. The US is directly confronting these states. They could conceivably work with the US when Iran is on the brink of obtaining nuclear weapons but not before then. They did not prevent North Korea. The Supreme Leader Ali Khamenei, the soon-to-be-inaugurated President Ebrahim Raisi, the Iranian Revolutionary Guard Corps, the Ministry of Intelligence, and other pillars of the regime are focused exclusively on strengthening the regime in advance of Khamenei’s impending succession sometime in the coming decade. The succession could easily lead to domestic unrest and a political crisis, which makes the 2020s a critical period for the Islamic Republic. With Tehran focused on a delicate succession, it is not a foregone conclusion that Iran will go on the offensive to expand its sphere of influence immediately after the US deal. But sooner or later a major new geopolitical trend will emerge: the rise of Iran. With sanctions removed, trade and investment increasing, and Chinese and Russian support, Iran will be capable of pursuing its strategic aims in the region more effectively. It will extend its influence across the “Shia Crescent,” including Iraq. The fear that this will inspire in Israel and the Gulf Arab states has already generated a slow-boiling war in the region. This war will intensify as the US will be reluctant to intervene. The purpose of the deal is to enable the war-weary US to reduce its active involvement in the region. The US foreign policy and defense establishment do not entirely see it this way – they emphasize that the US will remain engaged. But US allies in the Middle East will not be convinced. The region already has a taste for the way this works after the US’s precipitous withdrawal from Iraq in 2011, which lead to the rise of the Islamic State terrorist group. Biden will try not to be so precipitous but the writing is on the wall: the US will reduce its focus and commitment. A scramble for power in the region will begin the moment the ink dries on Biden’s signature of the JCPA. Israel and the Arab states are forming a de facto alliance – based on last year’s Abraham Accords – to prepare for Iran’s push to dominate the region. Even if Iran is not overly aggressive (a big if), Israel and the Gulf Arabs will overreact as a result of their fear of abandonment. They will also seek to hedge their bets by improving ties with the Chinese and Russians, making the Middle East the scene of a major new proxy battle in the global great power struggle. As a risk to our view: if the Biden administration changes course this summer and refuses to lift sanctions or rejoin the Iran deal – low but not zero probability – then tensions with Iran will explode almost instantaneously. The Iranians will threaten to close the Strait of Hormuz and a crisis will erupt in the third or fourth quarter. Bottom Line: The US will most likely rejoin the Iranian nuclear deal by August to avoid an immediate crisis or war. The Biden administration will wager that it can lend enough support to regional allies to keep Iran contained. This might work, as the Iranians will focus on fortifying the regime ahead of its leadership succession. However, Iran’s hardline leadership will see an opportunity in America’s withdrawal from its “forever wars.” Iran will increasingly cooperate with Russia and China. Iran’s conflict with Israel and Saudi Arabia will be extremely difficult to manage and will escalate over time, quite possibly creating a revolution or war in Iraq. The Gulf Arabs are already under immense pressure from the green energy revolution. Thus while oil prices might temporarily fall on the return of Iranian exports, they will later see upward pressure from a new wave of Middle Eastern instability. European Political Risk Has (Probably) Bottomed By contrast with all the above we have viewed Europe as a negligible source of (geo)political risk in 2021. European policy uncertainty is falling in Europe relative to these other powers and the rest of the world (Chart 11). Chart 11Europe's Relative Policy Uncertainty Bottoming

Europe's Relative Policy Uncertainty Bottoming

Europe's Relative Policy Uncertainty Bottoming

Chart 12EU Break-Up Risk Hits Floor (Again)

EU Break-Up Risk Hits Floor (Again)

EU Break-Up Risk Hits Floor (Again)

The risk of a break-up of the European Union has wilted and remains at historic lows (Chart 12). There is no immediate threat of any European countries emulating the UK and attempting to exit. Even Italian support for the euro has surged. Immigration flows have plummeted. European solidarity is not on the ballot in the upcoming German and French elections. Germany is choosing between the status quo and a “green revolution” that would not really be a revolution due to the constraints of coalition politics. The Greens have lost some momentum relative to their polling earlier this year but underlying trends suggest they will surprise to the upside in the September 26 vote (Charts 13A and 13B). They embrace EU solidarity, robust government spending, weariness with the Merkel regime, and concerns about climate change, Russia, China, and social justice. Chart 13AGerman Greens Will Surprise To Upside

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Chart 13BGerman Greens Will Surprise To Upside

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

We expect the Greens to surprise to the upside. But as they are forced into a coalition with the ruling Christian Democrats then they will be limited to raising spending rather raising taxes (Table 2). The market will cheer this result. Table 2German Greens’ Ambitious Tax Hike Proposals

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

If the Greens disappoint then a right-leaning government and too early fiscal tightening could become a risk – but it is a minor risk because Merkel’s hand-picked successor, the CDU Chancellor Candidate Armin Laschet, will be pro-Europe and fiscally dovish, just like the mainstream of his party under Merkel. The only limitation on this dovishness is that it would take another global shock for there to be enough votes in the Bundestag to loosen the schuldenbremse or “debt brake.” In France, President Emmanuel Macron is likely to win re-election – the populist candidate Marine Le Pen remains an underdog who is unlikely to make it through France’s two-round electoral system. In Italy, Prime Minister Mario Draghi is overseeing a national unity coalition that will dole out EU recovery funds. An election cannot be held ahead of the presidential election in January, which will be secured by the establishment parties as a major check on any future populist ruling coalition. The risk in these countries, as in Spain and elsewhere, is that neoliberal structural reform and competitiveness are falling by the wayside. Fiscal largesse is positive for securing the recovery but long-term growth potential will remain depressed (Chart 14). Chart 14European And Global Fiscal Stimulus (Updated June 2021)

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Europe remains stuck in a liquidity trap over the long run. It depends on the rest of the world for growth. This is a problem given that China’s potential growth is slowing and there is no ready substitute that will prop up global growth. Europe is increasingly ripe for negative “black swan” events. The power vacuum in the Middle East described above will lead to instability and regime failures that will threaten European security. Russia will remain aggressive, a reflection of its crumbling structural foundations. The Putin administration has not changed its strategy of building a sphere of influence in the former Soviet Union and pushing back against the West, as signaled by the threat to bomb ships that sail in Crimean waters – a unilateral expansion of Russia’s territorial waters following the Crimean invasion. The Biden administration is not seeking anything comparable to the diplomatic “reset” with Russia from 2009-11, which ended in acrimony. In other words, European political risk may be bottoming as we speak. Investment Takeaways Chart 15Limited Equity Upside From Likely US Infrastructure Bill

Limited Equity Upside From Likely US Infrastructure Bill

Limited Equity Upside From Likely US Infrastructure Bill

US Peak Fiscal Stimulus: The Biden administration is highly likely to pass an infrastructure package through Congress, either as a bipartisan deal with Republicans or as part of the American Jobs Plan. The result is another $1-$1.5 trillion fiscal stimulus, albeit over an eight-year period, with infrastructure funding taking until 2024-25 to ramp up. Biden’s other plans probably will not pass before the 2022 midterm election, which will likely bring gridlock. Investors are well aware of these proposals and the policy setting will probably be frozen after this year. Hence there is limited remaining upside for global materials sector and US infrastructure plays (Chart 15). The extravagant US fiscal thrust of 2020-21 will turn into a huge fiscal drag in 2022 (Chart 16). The Federal Reserve, however, will remain ultra-dovish as long as labor market slack persists – regardless of who is at the helm. Chart 16US Fiscal Drag Very Large In 2022

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Chart 17Go Long Large Caps And Defensives

Go Long Large Caps And Defensives

Go Long Large Caps And Defensives

China’s Headwinds Persist: China may or may not ease policy in time to prevent a market riot. China plays and industrial metals are highly exposed to a correction and we recommend steering clear. US-Iran Deal Weighs On Oil Price: Tactically we are neutral on oil and oil plays. An Iran deal could depress oil prices temporarily – and potentially in a major way if the Saudis agree with the Russians on increasing production. Fundamentals are positive but depend on the OPEC 2.0 cartel. The cartel faces the risk that higher prices will incentivize both alternative oil providers and the green revolution. Europe’s Opportunity: We continue to see the euro and European stocks offering value. Given the troubles with Russia we favor developed Europe plays over emerging Europe. The German election would be a bullish catalyst for European assets but headwinds from China will prevail, which is negative for cyclical European stocks. The Russian Duma election, also in September, creates high potential for Russia to clash with the West between now and then. Tactically, go long global large caps and defensives (Chart 17). Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Independent Vermont Senator Bernie Sanders recently felt it was necessary to warn against a second cold war. Sanders, a democratic socialist, is a reliable indicator of the left wing of the Democratic Party and a dissenter who puts pressure on the center-left Biden administration. His fears underscore the dominance of the new hawkish consensus. Appendix China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan – Province Of China

Taiwan Territory: GeoRisk Indicator

Taiwan Territory: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Australia

Australia: GeoRisk Indicator

Australia: GeoRisk Indicator

Highlights Entering 2H21, oil and metals' price volatility will rise as inventories are drawn down to cover physical supply deficits brought about by the re-opening of major economies ex-China. As demand increases and oil and metals supply become more inelastic, forward curves will backwardate further. This will weaken commodity-price correlations with the USD and boost commodity-index returns. Going into next week's OPEC 2.0 meeting, the Kingdom of Saudi Arabia (KSA) and Russia likely will hold off on further production increases, until greater clarity around US-Iran negotiations and the return of Iran as a bona fide exporter is available. Chinese authorities will release 100k MT of copper, aluminum and zinc into tight domestic markets in July. A two-day rally followed the news. Since bottoming in March 2020, the XOP and XME ETFs covering oil and gas producers and metals miners are up ~ 218% and ~ 196%, respectively, following the ~ 230% move in crude oil and the ~ 100% rise copper prices. Higher volatility will present buying opportunities for these ETFs (Chart of the Week). We remain long commodity index exposure – S&P GSCI and COMT ETF – expecting steeper backwardations. We will go long the PICK ETF at tonight's close again, after being stopped out last week with a 23.9% return. Feature Heading into 2H21, industrial commodity markets will continue to tighten. In the case of oil, this is caused by OPEC 2.0's production-management strategy – i.e., keeping supply below demand – and capital discipline among producers in the price-taking cohort.1 Base metals, on the other hand, are tightening because demand is recovering much faster than supply.2 Re-opening of major economies will boost refined-product demand in oil markets – e.g., gasoline and jet fuel – which will leave refiners little choice but to continue drawing on inventories to cover supply shortfalls in the near term (Chart 2). Chart of the WeekResources ETFs Follow Prices Higher

Resources ETFs Follow Prices Higher

Resources ETFs Follow Prices Higher

Chart 2Refiners Will Continue Drawing Crude Investments

Refiners Will Continue Drawing Crude Investments

Refiners Will Continue Drawing Crude Investments

Base metals – particularly copper and aluminum – will remain well bid in the face of constrained supply and higher consumption ex-China. Despite China's widely anticipated decision to release strategic stockpiles of copper, aluminum and zinc next month into a tight domestic market – which we flagged last month – continued inventory draws will be required to cover physical deficits in these markets, particularly in copper (Chart 3).3 Chart 3Copper Inventories Will Draw As Demand Ex-China Rises

Copper Inventories Will Draw As Demand Ex-China Rises

Copper Inventories Will Draw As Demand Ex-China Rises

Chart 4Steeper Backwardation, Higher Volatility

Oil, Metals Vol Creates Buying Opportunities

Oil, Metals Vol Creates Buying Opportunities

Higher Vol On The Way As demand for industrial commodities increases and inventories continue to draw, forward curves will become more backwardated – i.e., material delivered promptly (next day or next week) will command a higher price than commodities delivered next month or next year: Consumers value current supply above deferred supply, and producers and merchants have to charge more to cover inventory replacement costs, which increase when prompt demand outstrips supply. The steepening of forward curves for industrial commodities will lead to higher price volatility in oil and metals markets, particularly copper: Demand will confront increasingly inelastic supply. In this evolution, prices will be forced to allocate inelastic supply as demand increases. Sometimes-sharp changes in price are required to equilibrate available supply with demand when this happens. This can be seen clearly in oil markets, but it holds true for all storable commodities (Chart 4).4 Investment Implications Industrial commodity markets are entering a more volatile phase, which will be characterized by sharp price movements up and down over the short term, as demand continues to outpace supply. Our analysis suggests this is the beginning of a more volatile phase in industrial commodity markets. The balance of risk in industrial commodity prices will remain to the upside as volatility increases. In the short term, fundamental imbalances can be addressed over a relatively short months-long horizon – i.e., OPEC 2.0 can release spare capacity over a 3-4 month interval to accommodate rising demand – so that price increases do not destroy demand as oil-exporters are rebuilding their fiscal balance sheets. Base metals markets will have a tougher time in the short run finding the supply to meet surging demand, but it can be done over the next year or so without prices getting to the point where demand-destruction sets in. Over the medium to long term, investor-owned oil and gas producers literally are being directed by policymakers, shareholders and courts toward an extended wind-down of production and investment in future production. Markets have been pricing through just such a situation in the post-COVID-19 world, with OPEC 2.0 managing supply against falling demand and still managing to reduce inventories significantly. If the world follows the IEA's pathway to a decarbonized future – in which no investment in new oil or gas production is required after 2025 – this will become the status quo for these markets going forward.5 Metals producers, on the other hand, are being encouraged to increase marketable supply at a rapid pace to accommodate demand driven by the build-out of renewable energy – chiefly wind and solar – and the grids that will be required to move this energy. Producers, however, remain reluctant to do so, fearing their capex investment to build out supply will produce physical surpluses that depress returns, similar to the last China-led commodity super-cycle. Supplying the necessary base metals to make this happen will be difficult at best, according to Ivan Glasenberg, CEO at Glencore. At this week's Qatar Economic Forum, he said copper supply will have to double between now and 2050 to meet expected demand for this critical metal. “Today, the world consumes 30 million tonnes of copper per year and by the year 2050, following this trajectory, we’ve got to produce 60 million tonnes of copper per year,” he said. “If you look at the historical past 10 years, we’ve only added 500,000 tonnes per year … Do we have the projects? I don’t think so. I think it will be extremely difficult.”6 The volatility we are expecting in oil, gas and base metals prices, will present buy-the-dip opportunities in related equities vehicles. Since bottoming in March 2020, the XOP and XME ETFs covering oil and gas producers and metals miners are up ~ 218% and ~ 196%, respectively, matching the ~ 230% move in crude oil and the ~ 100% rise in copper prices. We remain long commodity index exposure – S&P GSCI, which is up 5.9% and the COMT ETF, which is up 7.6% – expecting steeper backwardations. The trailing stop on our MSCI Global Metals & Mining Producers ETF (PICK) position recommended 10 December 2020 was elected, which stopped us out with a gain of 23.9%. We are getting long the PICK again at tonight's close. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish Commercial crude oil stocks in the US (ex-SPR barrels) fell 7.6mm barrels w/w in the week ended 18 June 2021, according to the US EIA. Including products, US crude and product inventories were down 5.8mm barrels. US domestic crude oil production was down 100k b/d, ending the week at 11.1mm b/d. Overall product supplied, the EIA's proxy for refined-product demand, was up 180k b/d at 20.75mm b/d, which is 129k b/d below 2019 demand for the same period. At 9.44mm b/d, gasoline demand was just below comparable 2019 consumption of 9.47mm b/d, while jet-fuel demand remains severely depressed vs. comparable 2019 consumption at 1.58mm b/d (vs. 1.92mm b/d). Distillate demand (e.g., diesel fuel) for the week ended 18 June 2021 was 3.95mm b/d vs. 3.97mm b/d for the comparable 2019 period. Base Metals: Bullish Benchmark spot iron ore (62% Fe) prices are holding above $210/MT in trading this week, as demand for the steel input remains strong in China (Chart 5). The Chinese Communist Party (CCP) increased its level of intervention in the iron ore market this week, launching investigations into “malicious speculation,” vowing to “severely punish” anyone found to be engaged in such behavior, according to ft.com.7 Benchmark iron ore prices hit $230/MT in May. We continue to expect exports from Brazil to pick up in 2H21, which will push prices lower in 2H21. Precious Metals: Bullish In the aftermath of last Wednesday’s FOMC meeting gold prices lost nearly $86/oz (Chart 6). Our colleagues at BCA Research's USBS believe markets are paying too much attention to the Fed’s dot plots, and not to the central bank’s verbal guidance.8 Originally, the Fed stated that it will only start raising interest rates once a checklist of three conditions have been met. This checklist includes guidance on actual and expected inflation rates and the labor market. Gold prices did not react to Chair Powell's testimony before the House Select Subcommittee on the Coronavirus Crisis. Ags/Softs: Neutral US spring wheat prices are rallying on the back of dry weather in the northern Plains, while forecasts for benign crop weather in the Midwest pressured soybeans lower this week, according to successfulfarming.com. Chart 5

BENCHMARK IRON ORE 62% FE, CFR CHINA (TSI) GOING DOWN

BENCHMARK IRON ORE 62% FE, CFR CHINA (TSI) GOING DOWN

Chart 6

US Dollar To Keep Gold Prices Well Bid

US Dollar To Keep Gold Prices Well Bid

Footnotes 1 Please see our most recent oil price forecasts published last week in Balance Of Risks Tilts To Higher Oil Prices. It is available at ces.bcaresearch.com. 2 Please see A Perfect Energy Storm On The Way published on June 3, 2021 for further discussion. 3 Please see Less Metal, More Jawboning published on May 27, 2021, which flagged China's likely decision to release strategic stockpiles of base metals. 4 Chart 4 shows implied volatility as a function of the slope of the forward curve, i.e., the difference between the 1st- and 13th-nearby futures divided by the 1st-nearby future vs implied volatilities for Brent and WTI options. This modeling extends Kogan et al (2009), mapping realized volatilities calculated using historical settlements of crude oil futures against the slope of crude oil futures conditioned on 6th- vs. 3rd-nearby futures returns (in %). Please see Kogan, L., Livdan, D., & Yaron, A. (2009), "Oil Futures Prices in a Production Economy With Investment Constraints." The Journal of Finance, 64:3, pp. 1345-1375. 5 Please see fn 2's discussion of the IEA's Net Zero by 2050, A Roadmap for the Global Energy Sector beginning on p. 5 under The Case For A Carbon Tax. 6 Please see Copper supply needs to double by 2050, Glencore CEO says published on June 23, 2021 by reuters.com. Of course, being a copper producer with large-scale base-metals projects due to come on line in the next year or so, Mr. Glasenberg could be talking his book, but as Chart 3 shows, copper has been and likely will be in physical deficits for years. 7 Please see China cracks down on iron ore market, published by ft.com on June 21, 2021. 8 Please see How To Re-Shape The Yield Curve Without Really Trying, published on June 22, 2021. Investment Views and Themes Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

Image

Highlights The ongoing transition to a post-pandemic state and fiscal policy are either positive or net-neutral for risky asset prices. Fiscal thrust will turn to fiscal drag over the coming year, but the negative impact this will have on goods spending will likely be offset by a significant improvement in services spending, and thus is not likely to cause a concerning slowdown in overall economic activity. A modestly hawkish shift in the outlook for monetary policy is likely over the coming year, potentially occurring over the late summer or early fall in response to outsized jobs growth. However, such a shift is not likely to become a negative driver for risky asset prices over the coming 6-12 months, barring a major rise in market expectations for the neutral rate of interest. This may very well occur once the Fed begins to raise interest rates, but not likely before. Investors should overweight risky assets within a multi-asset portfolio, and fixed-income investors should maintain a below-benchmark duration position. We continue to favor value over growth on a 6-12 month time horizon, although growth may outperform in the near term. A bias toward value over the coming year supports an overweight stance toward global ex-US equities, and an overall pro-risk stance favors bearish US dollar bets. Feature Three factors continue to drive our global macroeconomic outlook and our cyclical investment recommendations. The first factor is our assessment of the global progress that is being made on the path to a post-pandemic state, and the return to pre-COVID economic conditions; the second is the likely contribution to growth from fiscal policy over the coming year; and the third is the outlook for monetary policy and whether or not monetary conditions will remain stimulative for both economic activity and financial markets. If the world continues to progress meaningfully on the path to a post-pandemic state, and if the impact of fiscal and monetary policy remains in line with market expectations, then we see no reason to alter our recommended investment stance. Equity market returns will be modest over the coming 6 to 12 months in this scenario given how significantly stocks have rebounded from their low last year, but we would still expect stocks to outperform bonds and would generally be pro-cyclically positioned. We present below our assessment of these three factors and their potential to deviate from consensus expectations over the coming year, to determine their likely impact on economic activity and financial markets. The Ongoing Transition To A Post-Pandemic World Chart I-1Enormous Progress Has Been Made In The Fight Against COVID-19

Enormous Progress Has Been Made In The Fight Against COVID-19

Enormous Progress Has Been Made In The Fight Against COVID-19

Chart I-1 highlights that meaningful progress continues to be made in vaccinating the world's population against COVID-19. North America and Europe continue to lead the rest of the world based on the share of people who have received at least one dose, but South America continues to make significant gains, and recent data updates highlight that Asia and Oceania are also making meaningful progress. Africa is the clear laggard in the war against SARS-COV-2 and its variants, but progress there has been delayed, at least in part, by India’s export restrictions of the Oxford-AstraZeneca/COVISHIELD vaccine. This suggests that, while Africa will continue to lag, the share of Africans provided with a first dose of vaccine will begin to rise once India resumes its exports and deliveries to African countries under the COVAX program continue. If variants of the disease were not a source of concern, Chart I-1 would highlight that the full transition to a post-pandemic economy over the next several months would be near certain. However, as evidenced by the recent decision in the UK to postpone the lifting of COVID-19 restrictions by 4 weeks due to the spreading of the Delta variant, the global economy is not entirely out of the woods yet. Encouragingly, the delay in the UK genuinely appears to be temporary. Chart I-2 highlights that while the number of confirmed UK COVID-19 cases has been rising over the past month, the uptick in hospitalizations and fatalities has so far been quite muted. Importantly, the rise in hospitalizations appears to be occurring among those who have not yet been fully vaccinated, underscoring that variants of the disease are only truly concerning if they are vaccine-resistant. The evidence so far is that the Delta variant is more transmissible and may increase the risk of hospitalization, but that two doses of COVID-19 vaccine offer high protection. Of course, vaccines only offer protection if you get them, and evidence of vaccination hesitancy in the US is thus a somewhat worrying sign. Chart I-3 shows that the daily pace of vaccinations in the US has slowed significantly from mid-April levels, resulting in a slower rise in the share of the population that has received at least one dose (second panel). On this metric, the US has recently been outpaced by Canada, and the gap between the UK and the US is now widening. Germany and France are close behind the US and may surpass it soon. Chart I-2The UK Delay In Removing Restrictions Seems Genuinely Temporary

The UK Delay In Removing Restrictions Seems Genuinely Temporary

The UK Delay In Removing Restrictions Seems Genuinely Temporary

Chart I-3Recent Vaccination Progress In The US Has Been Underwhelming

Recent Vaccination Progress In The US Has Been Underwhelming

Recent Vaccination Progress In The US Has Been Underwhelming

Sadly, Chart I-4 highlights that there is a political dimension to vaccine hesitancy in the US. The chart shows that state by state vaccination rates as a share of the population are strongly predicted by the share of the popular vote for Donald Trump in the 2020 US presidential election. Admittedly, part of this relationship may also be capturing an urban/rural divide, with residents in less-dense rural areas (which typically support Republican presidential candidates) perhaps feeling a lower sense of urgency to become vaccinated against the disease. Chart I-4The US Politicization Of Vaccines Raises The Risk From COVID-19 Variants

July 2021

July 2021

But given the clear politicization that has already occurred over some pandemic control measures, such as the wearing of masks, Chart I-4 makes it difficult to avoid the conclusion that the same thing has occurred for vaccines. This is unfortunate, and seemingly raises the risk that the Delta variant may spread widely in red states over the coming several months, potentially delaying economic reopening, or risking the reintroduction of pandemic control measures. However, there are two counterarguments to this concern. First, non-vaccine immunity is probably higher in red than blue states, and CDC data suggest that this effect could be large. While this figure is still preliminary and subject to change (and likely will), the CDC estimates that only 1 out of 4.3 cases of COVID-19 were reported from February 2020 to March 2021. Taken at face value, this implies that there were approximately 115 million infections during that period, compared with under 30 million reported cases. That gap accounts for 25% of the US population, and given that red states were slower to implement pandemic control measures last year and their residents often more resistant to the measures, it stands to reason that a disproportionate share of unreported cases occurred in these states. Second, as noted above, the evidence thus far suggests that the Delta variant is not vaccine resistant, at least for those who are fully vaccinated. This is significant because if Delta were to spread widely in red states over the coming several months, the resulting increase in hospitalizations would likely convince many vaccine hesitant Americans to become vaccinated out of fear and self-interest – two powerfully motivating factors. Thus, the Delta variant may become a problem for the US in the fall, but if that occurs a solution is not far from sight. And, in other developed countries where vaccine hesitancy rates appear to be lower, it would seem that a new, vaccine-resistant variant of the disease would likely be required in order to cause a major disruption in the transition to a post-pandemic state. Such a variant could emerge, but we have seen no evidence thus far that one will before vaccination rates reach levels that would slash the odds of further widespread mutation. Fiscal Policy: Passing The Baton To Services Spending Chart I-5 highlights that US fiscal policy is set to detract from growth over the coming 6-12 months, reflecting the one-off nature of some of the fiscal response to the pandemic. This is true outside of the US as well, as Chart I-6 highlights that the IMF is forecasting a two percentage point increase in the Euro Area’s cyclically-adjusted primary budget balance, representing a significant amount of fiscal drag relative to the past two decades. Chart I-5Fiscal Thrust Will Eventually Turn To Fiscal Drag In The US…

July 2021

July 2021

Should investors be concerned about the impact of fiscal drag on advanced economies over the coming year? In our view, the answer is no. The reason is that much of the fiscal response in the US and Europe has been aimed at supporting income that has been lost due to a drastic reduction in services spending, which will continue to recover over the coming months as the effect of the pandemic continues to ebb. Chart I-7 underscores this point by highlighting the “gap” in US consumer goods and services spending relative to its pre-pandemic trend. The chart highlights that US goods spending is running well above what would be expected, whereas there is a sizeable gap in services spending (which accounts for approximately 70% of US personal consumption expenditures). Goods spending will likely slow as fiscal thrust turns to fiscal drag, but services spending will improve meaningfully – aided not just by a post-pandemic normalization in economic activity, but also by the sizeable amount of excess savings that US households have accumulated over the past year (Chart I-7, panel 2). Chart I-6... And In Europe

... And In Europe

... And In Europe

Chart I-7But Reduced Transfers Will Only Impact Spending On Goods, Not Services

But Reduced Transfers Will Only Impact Spending On Goods, Not Services

But Reduced Transfers Will Only Impact Spending On Goods, Not Services

While some of these savings have already been deployed to pay down debt and some may be permanently saved in anticipation of higher future taxes, the key point for investors is that the negative impact on goods spending from reduced fiscal thrust will be offset by a significant improvement in services spending, and thus is not likely to cause a concerning slowdown in overall economic activity. Monetary Policy: A Modestly Hawkish Shift Is Likely This leaves us with the question of whether or not monetary policy will become a negative driver for risky asset prices over the coming 6-12 months, which is especially relevant following last week’s FOMC meeting. The updated “dot plot” following the meeting shows that 7 of the 18 FOMC participants anticipate a rate hike in 2022, and the majority (13 members) expect at least one rate hike before the end of 2023, raising the median forecast for the Fed funds rate to 0.6% by the end of that year. Chart I-8 highlights that while 10-year Treasury yields remains mostly unchanged following the meeting, yields moved higher at the short-end and middle of the curve. Chart I-8The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

Investor fears that the Fed may shift in a significantly hawkish direction at some point over the next year have been far too focused on inflation, and far too little focused on employment. It is not a coincidence that the Fed’s guidance was updated following the May jobs report, which saw a stronger pace of jobs growth relative to April. Table I-1 updates our US Bond Strategy service’s calculations showing the average monthly nonfarm payroll growth that will be required for the unemployment rate to reach 3.5-4.5% assuming a full recovery in the participation rate, which is the range of the Fed’s NAIRU estimates. May’s payroll growth number of 560k implies that the Fed’s maximum employment criterion will be met sometime between June and September next year, if monthly payroll growth continues at that pace. Table I-1Calculating The Distance To Maximum Employment

July 2021

July 2021

Chart I-9Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

It is currently difficult to assess with great confidence what average payroll growth will prevail over the coming year, but we noted in last month’s report that there were compelling arguments in favor of outsized jobs growth this fall.1 In addition to those points, we note the following: Blue states have generally been slower to reopen their economies, and Chart I-9 highlights that these states have consequently been slower to return to their pre-pandemic unemployment rate. Among blue states, California and New York are the largest by population, and it is notable that both states only lifted most COVID-19 restrictions on June 15 – including the wearing of masks in most settings. This implies that services jobs are likely to grow significantly in these states over the coming few months. Both consensus private forecasts as well as the Fed’s expectation for real GDP growth imply that the output gap will be closed by Q4 of this year (Chart I-10). These expectations appear to be reasonable, given the substantial amount of excess savings that have been accumulated by US households and the fact that monetary policy remains extremely stimulative. When the output gap turned positive during the last economic cycle, the unemployment rate was approximately 4% – well within the Fed’s NAIRU range. Chart I-10 also shows that the Fed’s 7% real GDP growth forecast for this year would put the output gap above its pre-pandemic level, when the unemployment rate stood at 3.5%. In fact, it is possible that annualized Q2 real GDP growth will disappoint current consensus expectations of 10%, due to the scarcity of labor supply (scarcity that will be eased by labor day when supplemental unemployment insurance benefit programs end). Were Q2 GDP to disappoint due to supply-side limitations, it would strengthen the view that job gains will be very strong this fall ceteris paribus, as it would highlight that real output per worker cannot rise meaningfully further in the short-term and that stronger growth later in the year will necessitate very large job gains. Chart I-11 highlights that US air travel and New York City subway ridership have already returned close to 75% and 50% of their pre-pandemic levels, respectively. Based on the trend over the past three months, the chart implies that air travel will return to its pre-pandemic levels by mid-October of this year, and New York City subway ridership by June 2022. This underscores that travel-related services employment will recover significantly in the fall, and that jobs in downtown cores will rebound as office workers progressively return to work. Chart I-10Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Chart I-11Services Employment Will Recover In The Fall

Services Employment Will Recover In The Fall

Services Employment Will Recover In The Fall

On the latter point, one major outstanding question affecting the outlook for monetary policy is the magnitude of the likely permanent impact of work from home policies on employment in central business districts. Fewer office workers commuting to downtown office locations suggests that some jobs in the leisure & hospitality, retail trade, professional & business services, and other services industries will never return or will be very slow to do so, arguing for a longer return to maximum employment (and the Fed’s liftoff date). We examine this question in depth in Section 2 of this month’s report, and find that the “stickiness” of work from home policies will likely cause permanent central business job losses on the order of 575k (or 0.35% of the February 2020 labor force). While this would be non-trivial, when compared with a pre-pandemic unemployment rate of 3.5%, WFH policies alone are not likely to cause a long-term deviation from the Fed’s maximum employment objective. Outsized jobs growth this fall, at a pace that quickly reduces the unemployment rate, argues for a first Fed rate hike that is even earlier than the market expects. Chart I-12 presents The Bank Credit Analyst service’s current assessment of the cumulative odds of the Fed’s liftoff date by quarter; we believe that it is likely that the Fed will have raised rates by Q3 of next year, and that a rate hike in the first half of 2022 is a possibility. These odds are slightly more aggressive than those presented by our fixed-income strategists in a recent Special Report,2 but are consistent with their view that the Fed will raise interest rates by the end of next year. Chart I-12The Bank Credit Analyst’s Assessment Of The Odds Of The First Rate Hike

July 2021

July 2021

The odds presented in Chart I-12 are also more hawkish than the Fed funds rate path currently implied by the OIS curve, meaning that we expect investors to be somewhat surprised by a shifting monetary policy outlook at some point over the coming year, potentially over the next 3-6 months. Payroll growth during the late summer and early fall will be a major test for the employment outlook, and is the most likely point for a hawkish shift in the market’s view of monetary policy. Is this likely to become a negative driver for risky asset prices over the coming 6-12 months? In our view, the answer is “probably not.” While investors tend to focus heavily on the timing of the first rate hike as monetary policy begins to tighten, the reality is that it is the least relevant factor driving the fair value of 10-year Treasury yields. Investor expectations for the pace of tightening and especially for the terminal Fed funds rate are far more important, and, while it is quite possible that expectations for the neutral rate of interest will eventually rise, it seems unlikely that this will occur before the Fed actually begins to raise interest rates given that most investors accept the secular stagnation narrative and the view that “R-star” is well below trend rates of growth (we disagree).3 Chart I-13 highlights the fair value path of 10-year Treasury yields until the end of next year, assuming a 2.5% terminal Fed funds rate, no term premium, and a rate hike pace of 1% per year. The chart highlights that while government bond yields are set to move higher over the coming 6-12 months, they are likely to remain between 2-2.5%. This would drop the equity risk premium to a post-2008 low (Chart I-14), which would further reduce the attractiveness of stocks relative to bonds. But we doubt that this would be enough of a decline to cause a selloff, and it would still imply a stimulative level of interest rates for households and firms. Chart I-1310-Year Yields Will Rise Over The Coming Year, But Not Sharply

10-Year Yields Will Rise Over The Coming Year, But Not Sharply

10-Year Yields Will Rise Over The Coming Year, But Not Sharply

Chart I-14Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Investment Conclusions Among the three factors driving our global macroeconomic outlook and our cyclical investment recommendations, continued progress on the path toward a post-pandemic state and fiscal policy remain either positive or mostly neutral for risky assets. A potentially hawkish shift in the outlook for monetary policy this fall remains the chief risk, but we expect the rise in bond yields over the coming year to remain well-contained barring a sea change in investor expectations for the terminal Fed funds rate – which we believe is unlikely to occur before the Fed begins to raise interest rates. Consequently, we continue to recommend that investors should overweight risky assets within a multi-asset portfolio, and that fixed-income investors should maintain a below-benchmark duration position. We expect modest absolute returns from global equities, but even mid-single digit returns are likely to beat those from long-dated government bonds and cash positions. While value stocks may underperform growth stocks over the coming 3-4 months,4 rising bond yields over the coming year will ultimately favor value stocks and will likely weigh on elevated tech sector (and therefore growth stock) valuations (Chart I-15). Chart I-16 highlights that the attractiveness of US value versus growth is meaningfully less compelling for the S&P 500 Citigroup indexes, suggesting that investors should continue to favor MSCI-benchmarked value over growth positions over a 6-12 month time horizon.5 Chart I-15Value Is Extremely Cheap

Value Is Extremely Cheap

Value Is Extremely Cheap

Chart I-16Value Vs. Growth: The Benchmark Matters

Value Vs. Growth: The Benchmark Matters

Value Vs. Growth: The Benchmark Matters

The likely outperformance of value versus growth also has implications for regional allocation within a global equity portfolio. The US is significantly overweight broadly-defined technology relative to global ex-US stocks, and financials – which are overrepresented in value indexes – have already meaningfully outperformed in the US this year compared with their global peers and are now rolling over (Chart I-17). This underscores that investors should favor ex-US stocks over the coming year, skewed in favor of DM ex-US given that China’s credit impulse continues to slow (Chart I-18). Chart I-17Favor Global Ex-US Stocks Over The Coming Year

Favor Global Ex-US Stocks Over The Coming Year

Favor Global Ex-US Stocks Over The Coming Year

Chart I-18Concentrate Global Ex-US Exposure In Developed Markets

Concentrate Global Ex-US Exposure In Developed Markets

Concentrate Global Ex-US Exposure In Developed Markets

Finally, global ex-US stocks also tend to outperform when the US dollar is falling, and we would recommend that investors maintain a short dollar position on a 6-12 month time horizon despite the recent bounce in the greenback. Chart I-19 highlights that the dollar remains strongly negatively correlated with global equity returns, and that the dollar’s performance over the past year has been almost exactly in line with what one would have expected given this relationship. Thus, a bullish view toward global stocks implies both US dollar weakness and global ex-US outperformance over the coming year. Chart I-19A Bullish View Towards Global Stocks Implies A Dollar Bear Market

A Bullish View Towards Global Stocks Implies A Dollar Bear Market

A Bullish View Towards Global Stocks Implies A Dollar Bear Market

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst June 24, 2021 Next Report: July 29, 2021 II. Work From Home “Stickiness” And The Outlook For Monetary Policy Work from home policies, originally designed as emergency measures in the early phase of the COVID-19 pandemic, are likely to be “sticky” in a post-pandemic world. This will negatively impact the labor market in central business districts, via reduced spending on services by office workers. The potential impact of working from home is often cited as an example of what is likely to be a lasting and negative effect on jobs growth, but we find that it is not likely to be a barrier to the labor market returning to the Fed’s assessment of “maximum employment.” The size of the impact depends importantly on whether employee preferences or employer plans for WFH prevail, but our sense is that the latter is more likely. A weaker pace of structures investment in response to elevated office vacancy rates will likely have an even smaller impact on growth than the effect of reduced central business district services employment. The contribution to growth from structures investment has been small over the past few decades, office building construction is a small portion of overall nonresidential structures, and there are compelling arguments that the net stock of office structures will stay flat, rather than decline. Our analysis suggests that job growth over the coming year could be even stronger than the Fed and investors expect, possibly resulting in a first rate hike by the middle of next year. This would be earlier than we currently anticipate, but it underscores that fixed-income investors should remain short duration on a 6-12 month time horizon, and that equity investors should favor value over growth positions beyond the coming 3-4 months. The outlook for US monetary policy over the next 12 to 18 months depends almost entirely on the outlook for employment. Many investors are focused on the potential for elevated inflation to force the Fed to raise interest rates earlier than it currently anticipates, but it is the progress in returning to “maximum employment” that will determine the timing of the first Fed rate hike – and potentially the speed at which interest rates rise once policy begins to tighten. In this report, we estimate the extent to which the “stickiness” of working from home (WFH) policies and practices could leave a lasting negative impact on the US labor market. We noted in last month's report that a large portion of the employment gap relative to pre-pandemic levels can be traced to the leisure & hospitality and professional and business services industries, both of which – along with retail employment – stand to be permanently impaired if the office worker footprint is much lower in a post-COVID world.6 Using employee surveys and a Monte Carlo approach, we present a range of estimates for the permanent impact of WFH policies on the unemployment rate, and separately examine the potential for lower construction of office properties to weigh on growth. We find that the impact of reduced office building construction is likely to be minimal, and that WFH policies may structurally raise the unemployment rate by 0.3 to 0.4%. While non-trivial, when compared with a pre-pandemic unemployment rate of 3.5%, WFH policies alone are not likely to cause a long-term deviation from the Fed’s maximum employment objective. Relative to the Fed’s expectations of a strong, lasting impact on the labor market from the pandemic, this suggests that job growth over the coming year could be even stronger than the Fed and investors expect, possibly resulting in a first rate hike by the middle of next year. This would be earlier than we currently anticipate, but it underscores that fixed-income investors should remain short duration on a 6-12 month time horizon, and that equity investors should favor value over growth positions beyond the coming 3-4 months (a period that may see outperformance of the latter). Quantifying The Labor Market Impact Of The New Normal For Work In a January paper, Barrero, Bloom, and Davis (“BBD”) presented evidence arguing why working from home will “stick.” The authors surveyed 22,500 working-age Americans across several survey “waves” between May and December 2020, and asked about both their preferences and their employer’s plans about working from home after the pandemic. Chart II-1 highlights that the desired amount of paid work from home days (among workers who can work from home) reported by the survey respondents is to approximately 55% of a work week, suggesting that a dramatic reduction in office presence would likely occur if post-pandemic WFH policies were set fully in accordance with worker preferences. Chart II-1Employee Preferences Imply A Dramatic Reduction In Post-COVID Office Presence

July 2021

July 2021

However, Table II-1 highlights that employer plans for work from home policies are meaningfully different than those of employees. The table highlights that employers plan for employees to work from home for roughly 22% of paid days post-pandemic, which essentially translates to one day per week on average.7 BBD noted that CEOs and managers have cited the need to support innovation, employee motivation, and company culture as reasons for employees’ physical presence. Managers believe physical interactions are important for these reasons, but employees need only be on premises for about three to four days a week to achieve this. Table II-1 also shows that employers plan to allow higher-income employees more flexibility in terms of working from home, and less flexibility to employees whose earnings are between $20-50k per year. Table II-1Employer Plans, However, Imply Less Working From Home Than Employees Prefer

July 2021

July 2021

Based on the survey results, BBD forecast that expenditure in major cities such as Manhattan and San Francisco will fall on the order of 5 to 10%. In order to understand the national labor market impact of work from home policies and what implications this may have on monetary policy, we scale up BBD’s calculations using a Monte Carlo approach that incorporates estimate ranges for several factors: The percent of paid days now working from home for office workers The amount of money spent per week by office workers in central business districts (“CBDs”) The number of total jobs in CBDs The percent of CBD jobs in industries likely to be negatively impacted by reduced office worker expenditure The average weekly earnings of affected CBD workers The average share of business revenue not attributable to strictly variable expenses The percent of affected jobs likely to be recovered outside of CBDs Our approach is as follows. First, we calculate the likely reduction in nationwide CBD spending from reduced office worker presence by multiplying the likely percent of paid days now permanently working from home by the number of total jobs in CBDs and the average weekly spending of office workers. This figure is then increased due to the estimated acceleration in net move outs from principal urban centers in 2020 (Chart II-2); we assume a 5% savings rate and an average annual salary of $50k for these resident workers, and assume that all of their spending occurred within CBDs. We also assume that roughly 50% of jobs connected to this spending are recovered. Chart II-2Fewer Residents Will Also Lower Spending In Central Business Districts

July 2021

July 2021

Then, we calculate the gross number of jobs lost in leisure & hospitality, retail trade, and other services by multiplying this estimate of lost spending by an estimate of non-variable costs as a share of revenue for affected industries, and dividing the result by average weekly earnings of affected employees. For affected CBD employees in the administrative and waste services industry, we simply assume that the share of jobs lost matches the percent of paid days now permanently working from home. Finally, we adjust the number of jobs lost by multiplying by 1 minus an assumed “recovery” rate, given that some of the reduction in spending in CBDs will simply be shifted to areas near remote workers’ residences. We assume a slightly lower recovery rate for lost jobs in the administrative and waste services industry. Table II-2 highlights the range of outcomes for each variable used in our simulation, and Charts II-3 and II-4 present the results. The charts highlight that the distribution of outcomes based on employer WFH intensions suggest high odds that nationwide job losses in CBDs due to reduced office worker presence will not exceed 400k. Based on average employee preferences, that number rises to roughly 800-900k. Table II-2The Factors Affecting Permanent Central Business District Job Losses

July 2021

July 2021

Chart II-3The Probability Distribution Of CBD Jobs Lost…

July 2021

July 2021

Chart II-4…Based On Our Monte Carlo Approach

July 2021

July 2021

This raises the question of whether employer plans or employee preferences for WFH arrangements will prevail. Our sense is that it will be closer to the former, given that we noted above that employer WFH plans are the least flexible for employees whose earnings are between $20-50k per year (who are presumably employees who have less ability to influence the policy of firms). Chart II-5 re-presents the projected job losses shown in Chart II-4 as a share of the February 2020 labor force, along with a probability-weighted path that assumes a 75% chance that employer WFH plans will prevail. The chart highlights that WFH arrangements would have the effect of raising the unemployment rate by approximately 0.35%. However, relative to a pre-pandemic starting point of 3.5%, this would raise the unemployment rate to a level that would still be within the Fed’s NAIRU estimates (Chart II-6). Therefore, the “stickiness” of WFH arrangements alone do not seem to be a barrier to the labor market returning to the Fed’s assessment of “maximum employment,” suggesting that the conditions for liftoff may be met earlier than currently anticipated by investors. Chart II-5CBD Job Losses Will Not Be Trivial, But They Will Not Be Enormous

July 2021

July 2021

Chart II-6Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

The Impact Of Lower Office Building Construction A permanently reduced office footprint could also conceivably impact the US economy through reduced nonresidential structures investment, as builders of commercial real estate cease to construct new office towers in response to expectations of a long-lasting glut. However, several points highlight that the negative impact on growth from US office tower construction will be even smaller than the CBD employment impact of reduced office worker presence that we noted above. First, Chart II-7 highlights the overall muted impact that nonresidential building investment has had on real GDP growth by removing the contribution to growth from nonresidential structures and for overall nonresidential investment. The chart clearly highlights that the historically positive contribution to real US output from capital expenditures over the past four decades has come from investment in equipment and intellectual property products, not from structures. Chart II-8 echoes this point, by highlighting that US real investment in nonresidential structures has in fact been flat since the early-1980s, contributing positively and negatively to growth only on a cyclical basis (not on a structural basis). Chart II-7Structures Have Not Contributed Significantly To US Growth For Some Time

Structures Have Not Contributed Significantly To US Growth For Some Time

Structures Have Not Contributed Significantly To US Growth For Some Time

Chart II-8Nonresidential Structures Investment Has Been Flat For Four Decades

Nonresidential Structures Investment Has Been Flat For Four Decades

Nonresidential Structures Investment Has Been Flat For Four Decades

Second, Table II-3 highlights that office properties make up a small portion of investment in private nonresidential structures. In 2019, nominal investment in office structures amounted to $85 billion, compared with $630 billion in overall structures investment, meaning that office properties amounted to just 13% of structures investment. Table II-3Office Structures Investment Is A Small Share Of Total Structures Investment

July 2021

July 2021

Table II-4Conceivably, Vacant Office Properties Could Be Converted To Luxury Residential Units

July 2021

July 2021