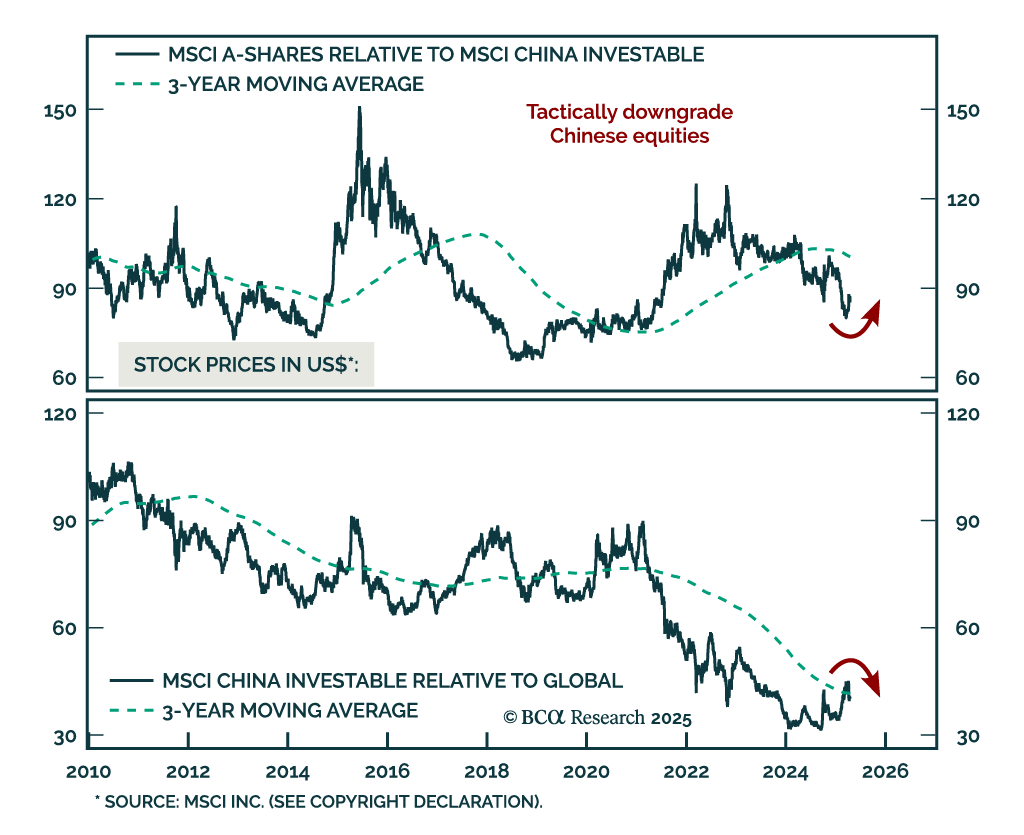

China

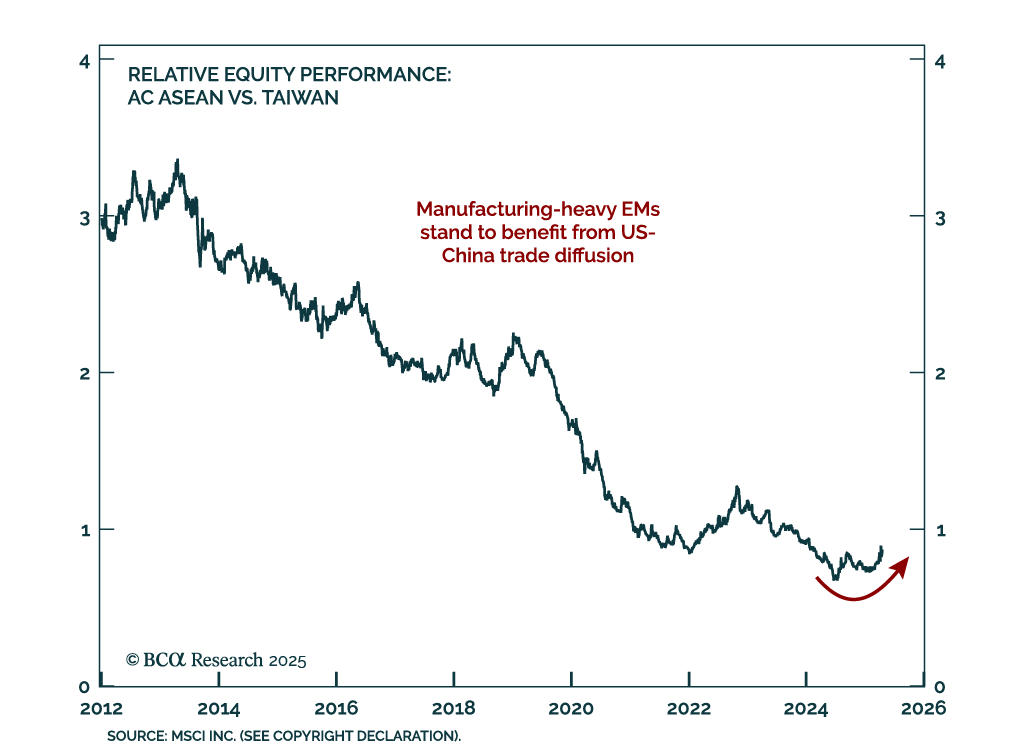

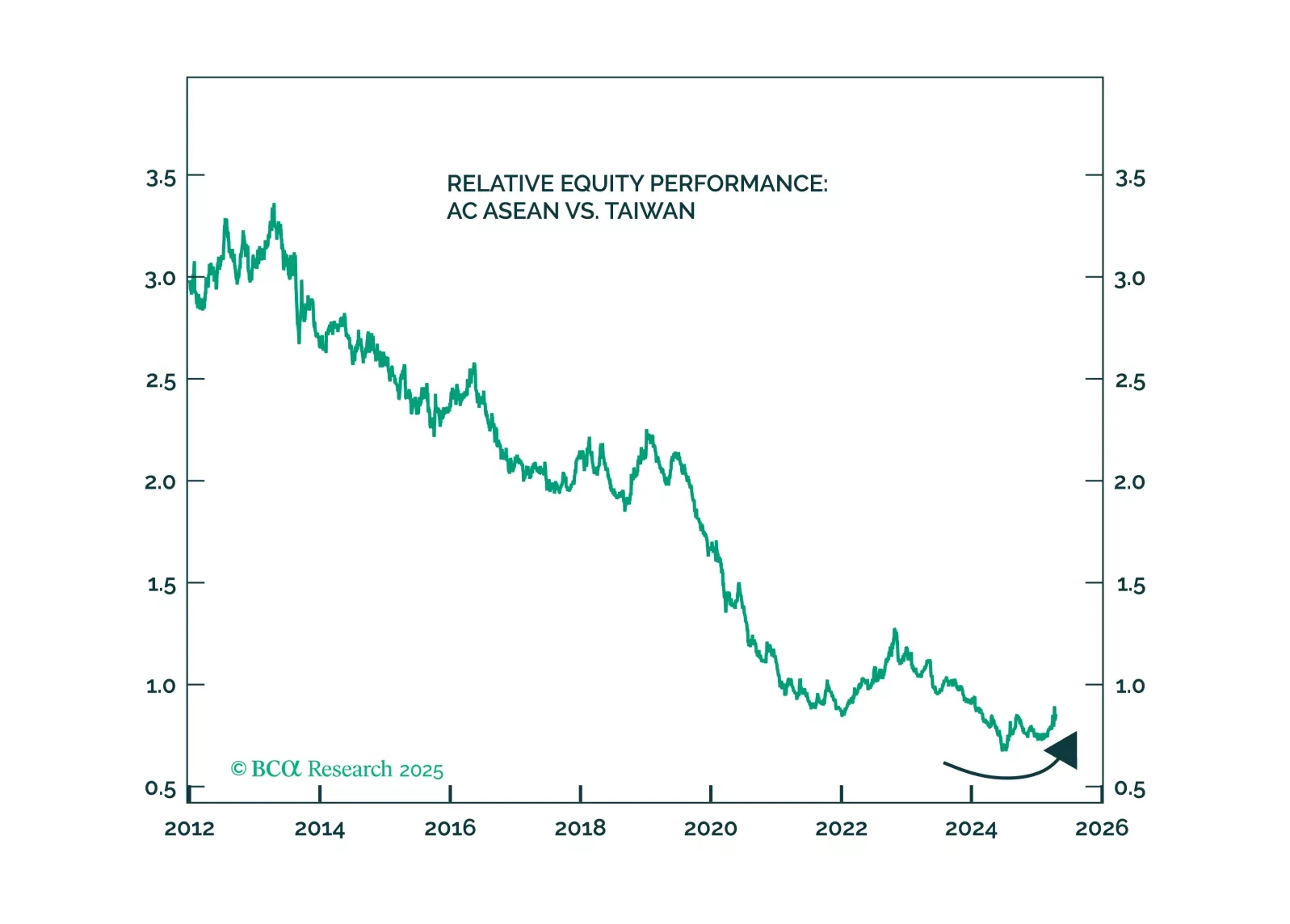

Upgrade the odds of a full-scale war in the Taiwan Strait from 5% to 10%. Rapid escalation of US-China economic war raises the probability of tensions spilling into the military-strategic domain. Investors should buy insurance against this tail risk while it is cheap. Meanwhile, use this year’s trade shock and equity volatility to increase allocation to EM manufacturing states.

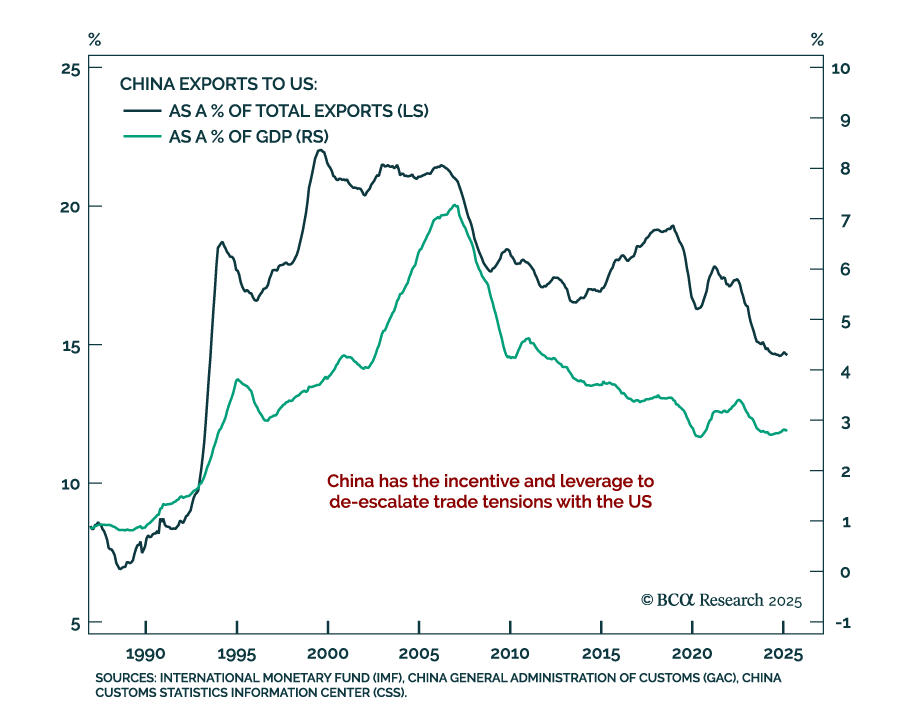

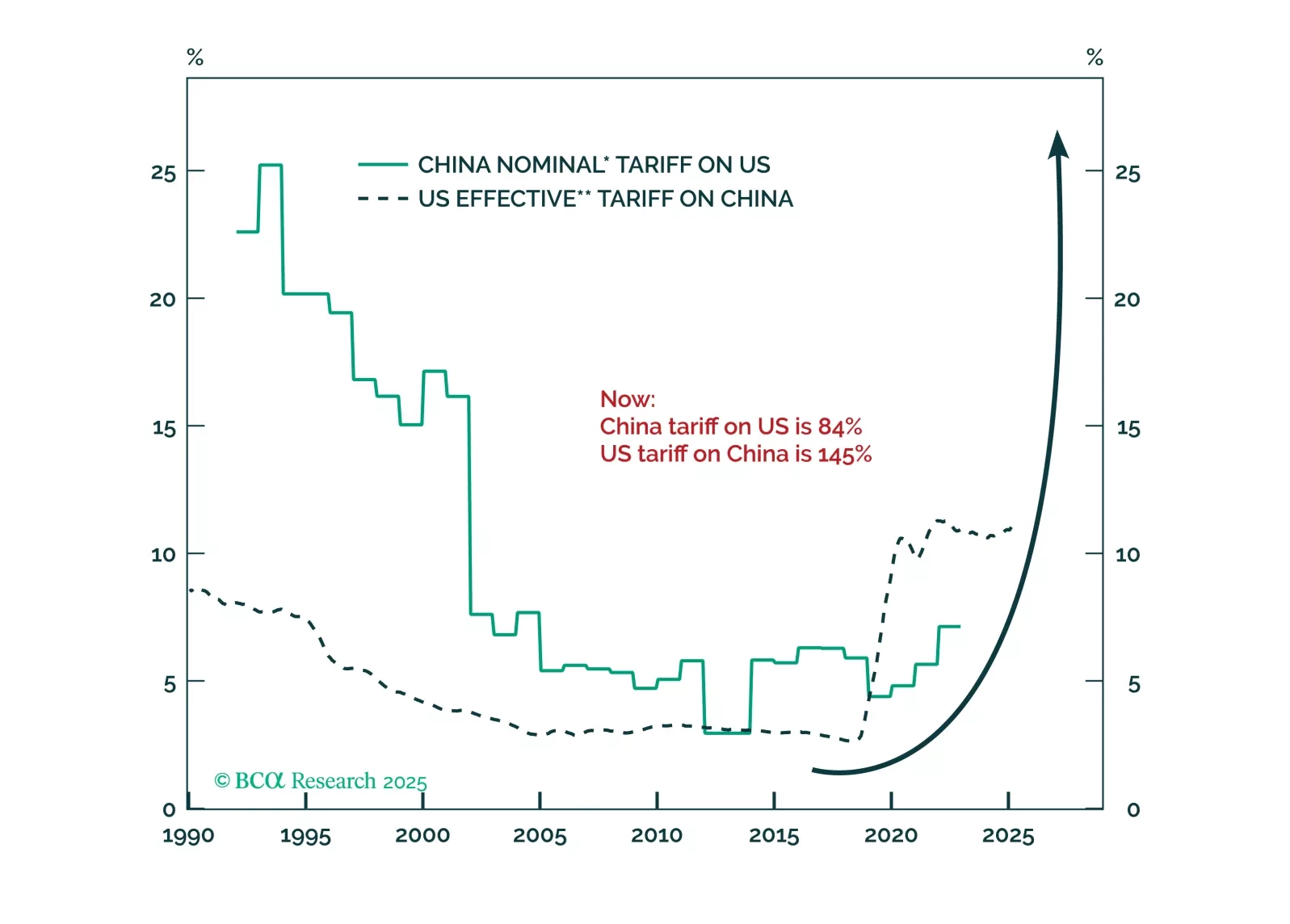

While the United States and China may aim for full decoupling, all they can afford now is some form of trade skirmishes. Increasing economic pressure will eventually force both Washington and Beijing to pursue more proactive negotiations. Until then, internal economic and financial strains are likely necessary to break the stalemate and resume dialogue between the two nations.

Europe’s near-term outlook remains clouded by uncertainty, even after the tariff reprieve. Our latest update breaks down why the risks to growth, profits, and financial conditions are still skewed to the downside — with Sweden standing out as a key bellwether.

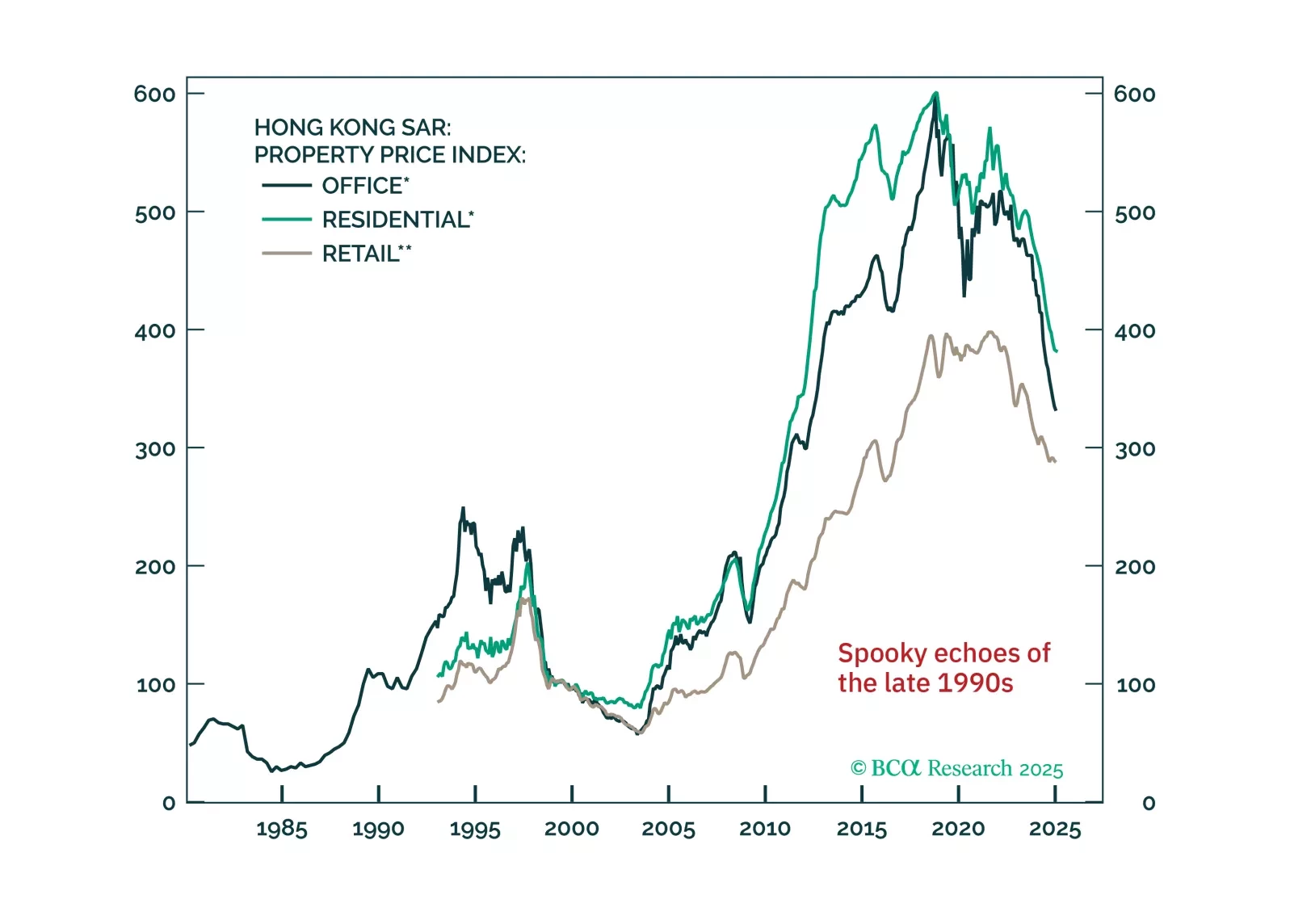

This week, we look at the sustainability of the HKD peg as the next whale to move markets, given what is happening to tariffs. After careful analysis, our bias is that it is here to stay. With the DXY dipping below 100, we are likely to see a rebound, which is actually bad news for the Hong Kong region of China, since it will tighten financial conditions. We have no new short-term trades, but if the peg broke, you want to be short HKD/JPY.

China’s aggressive retaliation against U.S. tariffs will enable President Trump to shift from punishing allies and redirect the trade war toward China. If Beijing does not react to the latest tariffs by doubling its fiscal stimulus, it indicates they are planning something different, as China will encounter economic destabilization. The likelihood of a hybrid military pressure on Taiwan will rise.