China

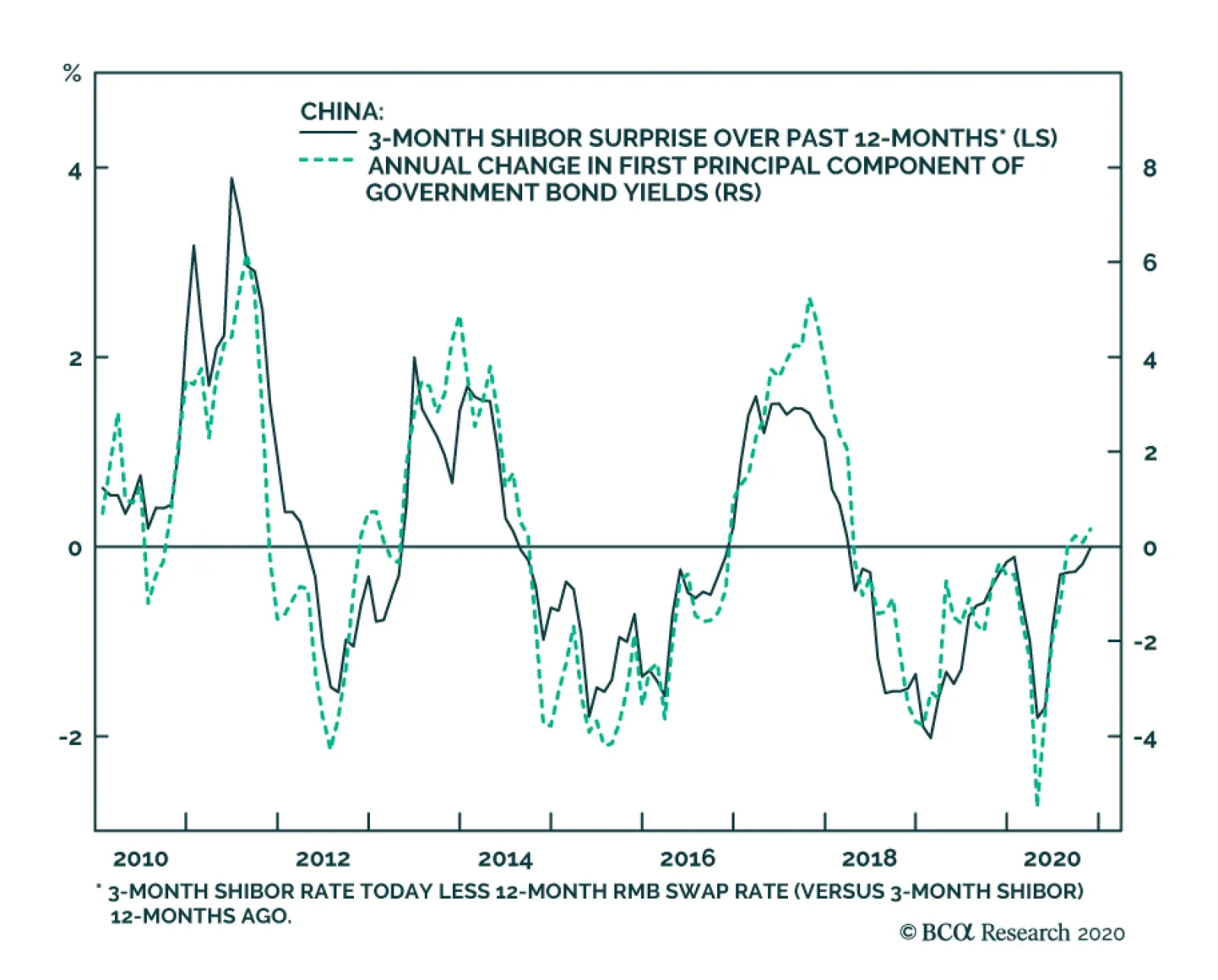

In a Special Report earlier this year, our China Investment Strategy service applied the “Golden Rule Of Bond Investing”, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, to China. The…

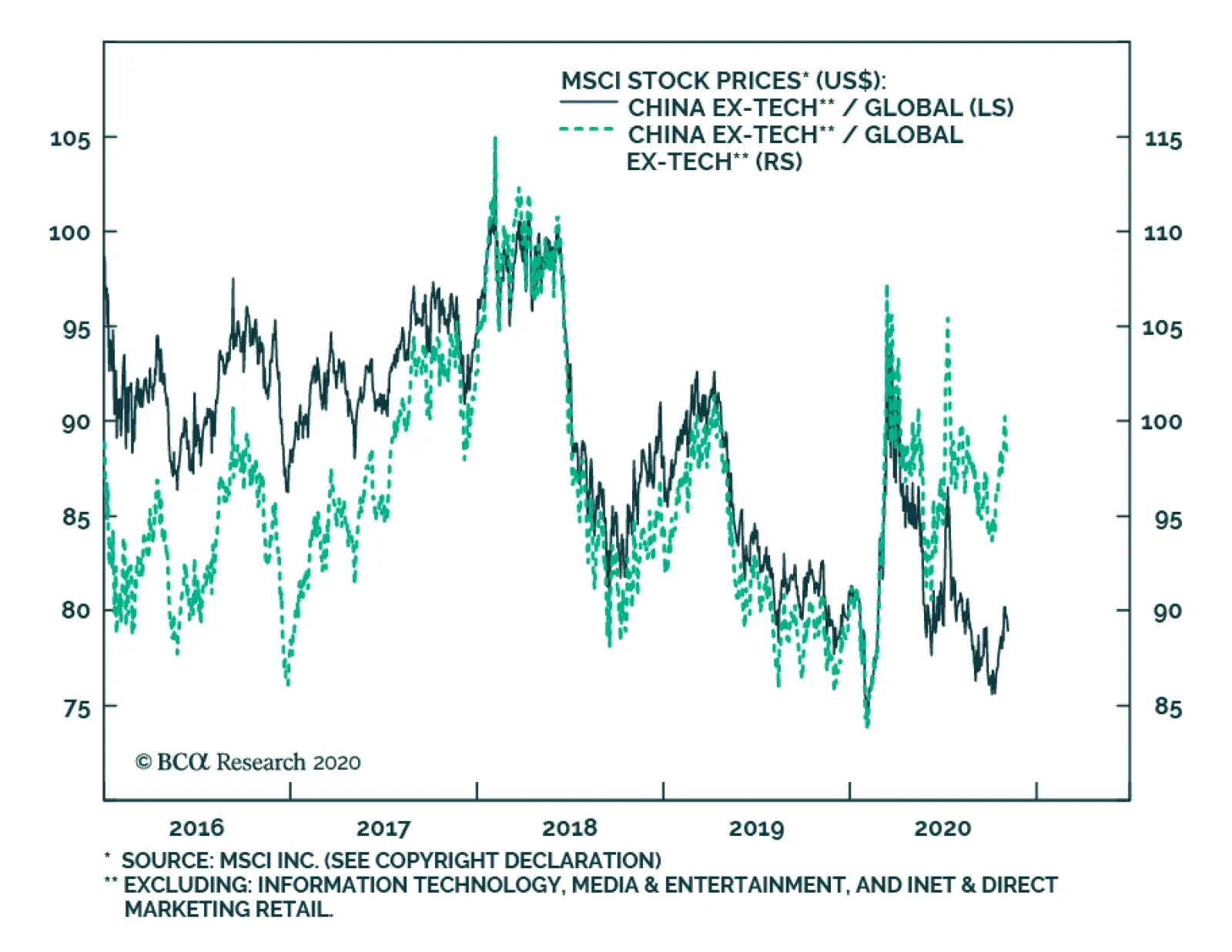

We noted in an Insight earlier this week that the recent outperformance of emerging market stocks has been almost entirely due to China's outperformance, given that the relative performance of EM ex-China versus the global benchmark has recently been flat. …

The global semiconductor industry has been experiencing a record amount of IPOs and M&A deals in recent months. A flurry of IPOs and M&As in any industry often serves as a sign of a top in share prices (Chart 1). Chat 1Will Booming Semiconductor IPOs And M&As Mark A Peak In Share Prices?

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

The basis is that IPO and M&A booms usually occur when investor sentiment on that industry is super optimistic, which often coincides with a top in share prices. Does this mean that semiconductor stocks in general, and the ones in Taiwan and Korea in particular, are at their zenith? Our broad judgement is that semi stocks have not reached a secular peak. First, as we argued in a recent Special Report, the semiconductor industry is in a structural uptrend due to the continuing rollout of 5G networks and phones, a wider adoption of data centers, further technological advancements in artificial intelligence, cloud computing, edge computing and smaller nodes for chip manufacturing. Second, it is critical to differentiate a macro call on semiconductors from a bottom-up call on individual stocks. Not all semi companies have rallied in recent years, i.e., there has been great divergence among global semi stocks as shown in Chart 2. Chat 2The Performance Of Semiconductor Stocks Has Varied Greatly

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Several semiconductor companies – like TSMC, Nvidia and AMD – have achieved technological breakthroughs, putting them in a position to enjoy high order volumes and charge higher prices. Not surprisingly, revenues of these companies have outpaced the industry average by a wide margin (Chart 3). Chat 3Semiconductor Companies' Revenues Have Diverged

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Others – like Intel and Analog Devices - have posted inferior revenue gains because they have fallen behind technologically or because they are specializing in certain types of semiconductors for which demand and pricing have been lackluster. Chat 4One-Off Surge In Demand For Semis Might Be Over

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Finally, if the global reflation trade resumes and global stocks continue advancing, as the first post-US election day suggests, there is little reason for global semiconductor stocks to falter at this moment. From the macro perspective, lower interest rates in the long run will support not-so-cheap semiconductor stock valuations. In addition, companies with access to unique technological capabilities will be able to raise their product prices benefiting their profits. That said, there are also several signs that the global semi demand cycle might have entered a period of indigestion: The one-off demand surge for personal computers and gadgets and one-off ramp up of global server shipments due to the pandemic might be drawing to a close (Chart 4, top panel). Digitimes Research has reported that global server shipments are estimated to have slipped 6% sequentially in Q3 from Q2 and are projected to drop another 12% in Q4 (Chart 4, bottom panel). Unlike those in March-April, renewed lockdowns are unlikely to produce another surge in demand for digital equipment and, hence, for semis. Many people and companies have already settled into working from home. In short, as the effect of the one-off demand surge for digital hardware fades, global semi demand will moderate. Semiconductor companies in general, and the ones in Korea and Taiwan in particular, have greatly benefited from China having stockpiled semiconductors in 2019 and 2020 in preparation for US sanctions on Huawei that went into effect on September 15, 2020 (Chart 5). The US supply ban on semiconductors to China for 5G technology will remain in place regardless of the outcome of the US presidential elections. Restrictions on semi sales to China will weigh on certain semi producers. In addition, smartphone sales in China generally, including 5G smartphone sales, have plunged as of late (Chart 6). Chat 5China Has Been Accumulating Semis Inventories

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Chat 6China: Smartphone Shipments, Including 5G, Are Weak

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Finally, the PMI new orders sub-index for Taiwan’s electronic industry has rolled over, signaling a slowdown in its growth rate (Chart 7). Similarly, the memory chip revenue indicator has recently rolled over, signaling a potential risk to memory stocks such as Samsung and Hynix which make up the Korean technology index (Chart 8). Chat 7A Moderation In The Taiwanese Semis Industry?

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Chat 8Proxy for Value Of Memory Chips And Korean Tech Stocks

Asian Semi Stocks: Upgrade Korea But Not Taiwan

Asian Semi Stocks: Upgrade Korea But Not Taiwan

We have been advocating a neutral allocation to both the Korean and Taiwanese stock markets within the EM equity universe. One of our arguments for this strategy has been a potential escalation in the US-China confrontation going into the US elections. However, this risk has not materialized. We are upgrading the Korean bourse to overweight. As to Taiwan, a contested US election and the resulting vacuum of power in the next couple of months might lead to a rise in all types of geopolitical risks around the world. Taiwan could be one of these. We maintain a neutral allocation to the Taiwanese bourse within an EM equity portfolio. Bottom Line: In absolute terms, Korean and Taiwanese equity performance depends on the direction of global stocks. We will discuss the outlook for global and EM stocks in a Strategy Report to be published early next week when there is more clarity on the outcome of the US presidential elections. Within an EM equity universe, we are upgrading Korean stocks from neutral to overweight but keeping Taiwan’s allocation at neutral. Arthur Budaghyan Chief Emerging Markets Strategist arthur@bcaresearch.com Ellen JingYuan He Associate Vice President ellenj@bcaresearch.com Footnotes

BCA Research's China Investment Strategy service has argued that the Proposal from China’s 14th Five-Year Plan does not change our cyclical view on Chinese assets. The 14th Five-Year Plan has more strategic importance than in the past decade; the plan…

The 14th Five-Year Plan has more strategic importance than in the past decade. Spending on national defense, technological self-sufficiency, public welfare and green energy will likely see substantial increases under the guidelines of a strong central government. The Proposal from the Five-Year Plan does not change our cyclical view on Chinese assets. Beyond mid-2021, the differences in sectoral performance will widen. We will likely begin to trim our position in China’s “old economy” stocks in the first half of 2021.

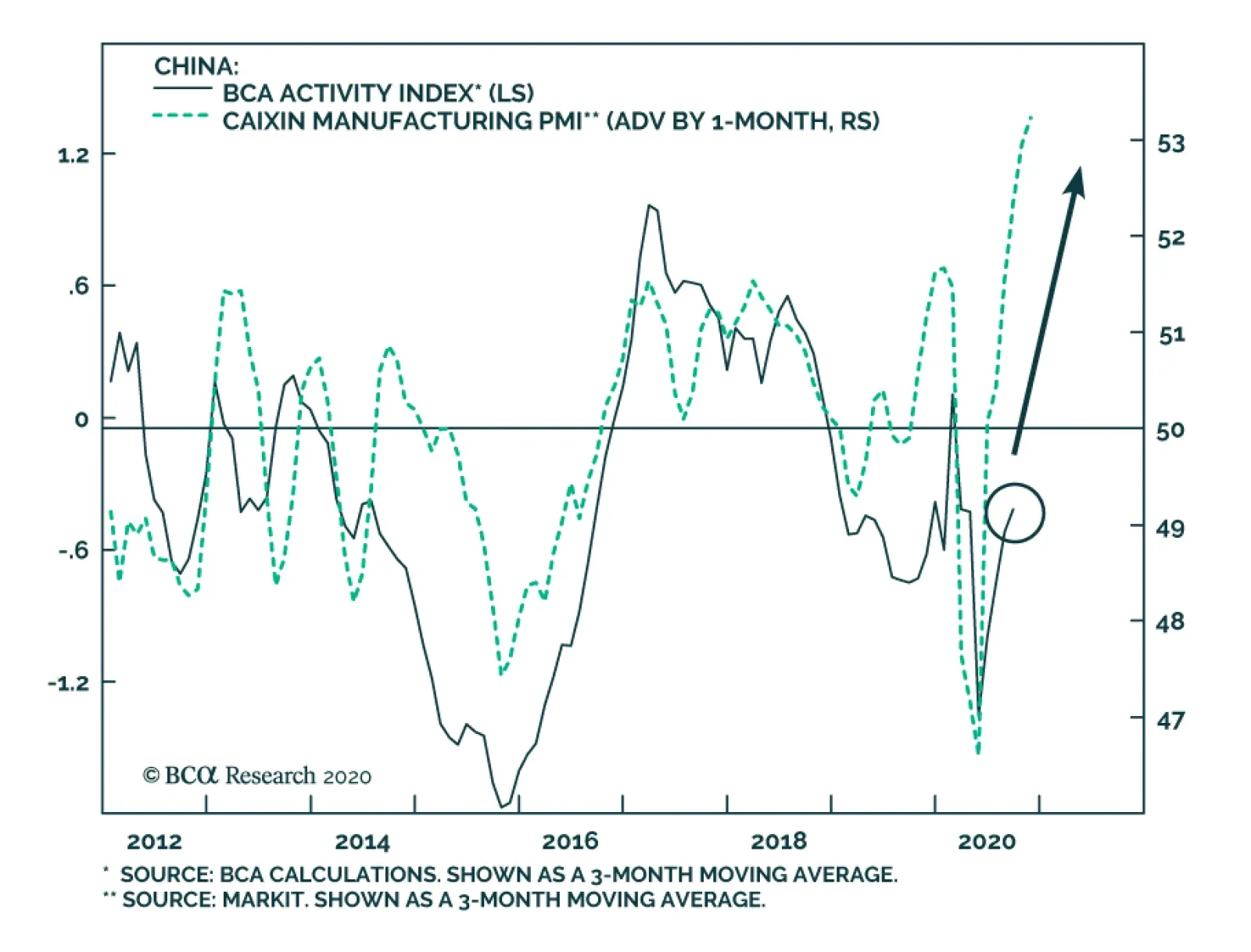

PMI indexes are coincident rather than leading indicators, but they are timely and often act as important confirming indicators. In this regard, the October update to the Caixin manufacturing PMI suggests that the uptrend in our BCA China Activity Index is…

Highlights Global risk assets have more downside in the near term. The US dollar is primed to rebound. Without major fiscal stimulus in the US, the upside in the greenback will be substantial. China’s business cycle recovery will continue but Chinese stocks and China-related plays are over-hyped and will experience a setback. For equity and credit investors, we recommend maintaining a neutral allocation to EM versus their DM counterparts. Feature Global risk assets have been in a twilight zone. On the one hand, there has been enormous uncertainty related to the US elections, the US fiscal stimulus and the impact of renewed social mobility restrictions on economic activity, especially in Europe. On the other hand, ultra-accommodative central banks, zero or negative interest rates on risk-free investments and the possibility of positive news on the COVID-19 vaccine front have until recently precluded a carnage in global risk assets. What will be the path going forward? We believe the risk-off period in global markets will continue in the near run, i.e., there will be a dusk before a sunrise. Hence, investors should maintain dry powder at the moment. Several negative outcomes have a non-trivial probability of occurring over the very near term. Chiefly these include a contested US presidential election or a Republican Senate under a Biden presidency acting as a constraint on large fiscal stimulus. Chart I-1The US Needs $1.5tn (7.4% Of GDP) Of Fiscal Stimulus In 2021 To Have A Neutral Fiscal Thrust

The US Needs $1.5bn (7.4% Of GDP) Of Fiscal Stimulus In 2021 To Have A Neutral Fiscal Thrust

The US Needs $1.5bn (7.4% Of GDP) Of Fiscal Stimulus In 2021 To Have A Neutral Fiscal Thrust

Needless to say, without a large fiscal stimulus package, the US is facing a fiscal cliff. According to the US Congressional Budget Office, the fiscal thrust will be negative 7.4% of GDP in 2021 if no further stimulus is enacted (Chart I-1). The fiscal thrust is the change in the cyclically-adjusted budget deficit. Even if the cyclically-adjusted budget deficit as a share of GDP remains the same, fiscal thrust will be zero. Hence, to achieve a positive fiscal thrust in the US, the fiscal stimulus must be greater than 7.4% of GDP or above $1.5 trillion. Even though Congress eventually approves a large fiscal package, there is a risk that the economy will slip in the interim. To emphasize, we do not mean there will be no fiscal stimulus. The point is that a large fiscal package is possible only if markets riot. With equity and credit markets still richly priced relative to their fundamentals, the carnage in global risk assets will likely continue. With equity and credit markets still richly priced relative to their fundamentals, the carnage in global risk assets will likely continue. Chart I-2The US: Lower Inflation Expectations, Higher Real Rates And A Stronger Dollar

The US: Lower Inflation Expectations, Higher Real Rates And A Stronger Dollar

The US: Lower Inflation Expectations, Higher Real Rates And A Stronger Dollar

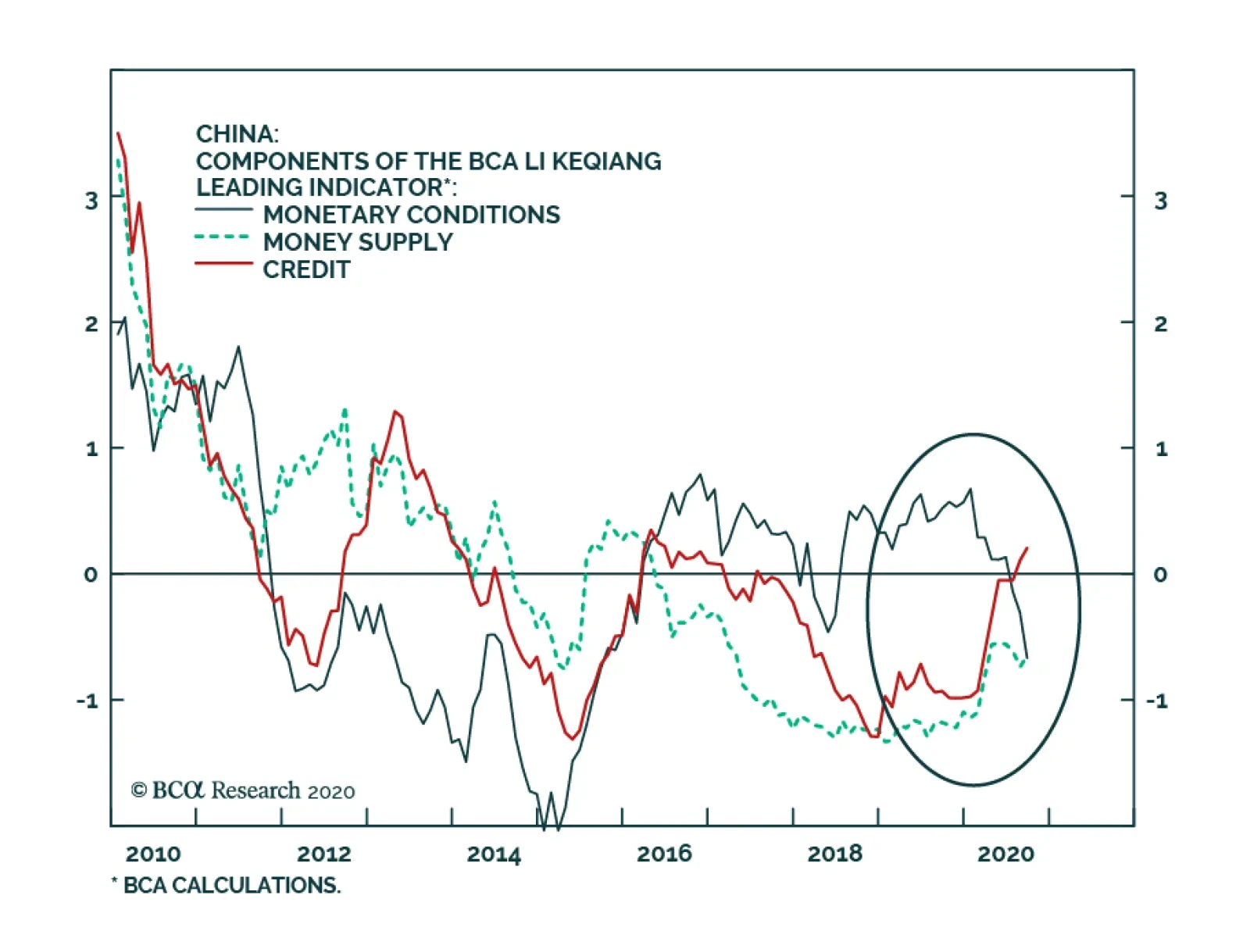

In the absence of a large US fiscal package and amid falling oil prices, US break-even inflation expectations will drop and the TIPS (real) yields will bounce in the near term (Chart I-2). A rebound in TIPS (real) yields will induce a bounce in the US dollar (Chart I-2, bottom panel). Provided that the primary risks presently stem from DM rather than Chinese growth, we recommend maintaining a neutral allocation to EM within respective global equity and credit portfolios. Why not overweight EM versus DM? First, the rebound in the greenback will weigh on EM financial markets. Second, outside China, Korea and Taiwan, EM fundamentals are poor. Net-net, odds of EM out- and under-performance versus DM are, for now, balanced. China: Peak Stimulus, Equities And Commodities China’s business cycle recovery is intact. However, Chinese equities have become fully priced and are at risk of a setback (in absolute terms) along with global share prices. Notably, there are several elements that could trigger a meaningful setback in Chinese stocks. First, the money and credit impulses are about to peak. The top panel of Chart I-3 shows that changes in commercial banks’ excess reserves ratio lead the credit impulse by about six months. The drop in the excess reserves ratio since May foreshadows the top in the private credit impulse. Interbank rates – shown inverted in the bottom panel of Chart I-3 – point to an apex in the narrow money (M1) impulse. Authorities have been shrinking commercial banks’ excess reserves at the PBoC since May/June. Tightening liquidity conditions in the banking system have led to higher interbank rates as well as government and corporate bond yields. Higher borrowing costs will weigh on money and credit growth. Second, the loan approval index of the PBoC banking survey has rolled over (Chart I-4). This implies that bank loan origination will subside going forward. Chart I-3China: Money/Credit Impulses Are At An Apex

China: Money/Credit Impulses Are At An Apex

China: Money/Credit Impulses Are At An Apex

Chart I-4China: Loan Growth To Moderate

China: Loan Growth To Moderate

China: Loan Growth To Moderate

Finally, fiscal stimulus is also peaking. Chart I-5 shows that the issuance of local government bonds is set to dwindle in the coming months. A peak in stimulus does not herald an immediate end of the recovery in the business cycle. China’s combined credit and fiscal spending impulse leads the business cycle by about nine months (Chart I-6). Therefore, even as the credit and fiscal spending impulse reaches an apex, the Chinese mainland’s economic activity will stay firm in H1 2021. Consequently, corporate profits will continue to recover. Chart I-5China: Fiscal Stimulus Is Peaking

China: Fiscal Stimulus Is Peaking

China: Fiscal Stimulus Is Peaking

Chart I-6China: The Economy Will Continue Recovering

China: The Economy Will Continue Recovering

China: The Economy Will Continue Recovering

What do all these imply for share prices? In periods when borrowing costs rise along with accelerating profit growth/improving net EPS revisions, share prices could still advance (Chart I-7). Hence, peak stimulus is not a sufficient reason to turn negative on share prices. Chart I-7China: Share Prices (ex-TMT), EPS Expectations And Corporate Bond Yields

China: Share Prices (ex-TMT), EPS Expectations And Corporate Bond Yields

China: Share Prices (ex-TMT), EPS Expectations And Corporate Bond Yields

That said, there are some signs that the Chinese equity market is overbought and over-hyped, making it vulnerable: A major IPO often marks a top in an asset class. Chart I-8 illustrates that Goldman Sachs’ IPO in 1999 preceded the secular top in US equities, IPOs of KKR and Blackstone in 2007 took place before the US credit bubble and the LBO boom unraveled; and finally, Glencore, the largest commodity trading house, went public in 2011 at the very peak of the secular bull market in commodities. In this respect, will Ant Group’s upcoming IPO mark a major top in Chinese or new economy stocks? Time will tell. Chart I-9 illustrates that Chinese IPO booms were historically associated with equity market tops. The current surge in Chinese IPOs – in various jurisdictions including China, Hong Kong, and the US – is a symptom of an over-hyped market. Chart I-8A Major IPO Often Marks The Top in Respective Asset Classes

A Major IPO Often Marks The Top in Respective Asset Classes

A Major IPO Often Marks The Top in Respective Asset Classes

Chart I-9China: Booming IPOs = An Equity Market Top?

China: Booming IPOs = An Equity Market Top?

China: Booming IPOs = An Equity Market Top?

Finally, new economy stocks in both the US and China have risen by about 20-fold since January 2010. Both in terms of duration and magnitude, their rallies are identical to the bull market in the Nasdaq 100 index in the 1990s (Chart I-10). The striking similarity with those episodes as well as current euphoria among investors about FAANG and Chinese new economy stocks warrant caution. In regard to commodities, in recent months we have been arguing that China is entering a commodity destocking cycle following the major restocking cycle that occurred in April-August. As Chinese imports of key commodities temporarily diminish due to destocking, commodities prices will relapse. Importantly, investor sentiment and net long positions in some key commodities are very elevated, suggesting overbought conditions (Chart I-11). Chart I-10FAANG And Tencent Have Been Tracking The Trajectory Of Nasdaq 100 In The 1990s

FAANG And Tencent Have Been Tracking The Trajectory Of Nasdaq 100 In The 1990s

FAANG And Tencent Have Been Tracking The Trajectory Of Nasdaq 100 In The 1990s

Chart I-11Investors Are Very Bullish On Copper

Investors Are Very Bullish On Copper

Investors Are Very Bullish On Copper

Critically, global mining stocks have been dropping since early September and are signaling a relapse in industrial metals prices (Chart I-12). In brief, commodity prices and commodity plays remain vulnerable. Chart I-12Global Mining Stocks Point To A Relapse In Industrial Commodities Prices

Global Mining Stocks Point To A Relapse In Industrial Commodities Prices

Global Mining Stocks Point To A Relapse In Industrial Commodities Prices

Bottom Line: Marrying the positive outlook for China’s business cycle on the one hand with an impending potential correction in global stocks, the peak in Chinese stimulus and signs of Chinese equity investor euphoria, we conclude that the risk-reward profiles of Chinese stocks and China-related plays in absolute terms are unattractive. That said, we continue recommending overweighting Chinese stocks within an EM equity portfolio. From a cyclical perspective, Chinese corporate profits will outperform EM and DM corporate earnings because China has dealt with the pandemic much better than almost all other countries. An Update On Currencies And Local Fixed-Income We have been shorting a basket of EM currencies – BRL, CLP, ZAR, TRY, KRW and IDR – against an equally-weighted basket of the euro, CHF and JPY. This strategy remains intact. However, we believe the US dollar is primed to stage a major rebound, in general, and versus EM currencies, in particular. Therefore, US dollar-based investors should hedge their currency risk or short the same EM currency basket versus the greenback. In EM local fixed-income markets, we have been receiving 10-year swap rates but have not recommended owning cash domestic bonds because of currency risk. We continue to recommend investors receive 10-year swap rates in the following markets: Mexico, Colombia, Russia, China, India and Korea. We have also been recommending long positions in domestic bonds in certain frontier markets like Egypt, Ukraine, and Pakistan. The global risk-off phase will cause their currencies to relapse versus the US dollar, raising the possibility that local bond yields will rise. Therefore, investors who are long these markets should close these positions. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights China’s 14th Five Year Plan and broader national strategy will continue to provoke opposition from the US and the West, regardless of the US election. China’s economic blueprint will focus on self-sufficiency, “dual circulation” (import substitution), state subsidies, and high-tech advancement – all factors that will continue to provoke western ire. US political polarization creates geopolitical risks, particularly for China, which will support the dollar and US equity outperformance, depending on the election result. If Trump wins, polarization will persist, he will face gridlock at home, and he will thus continue his aggressive foreign and trade policies, with China facing disruptive consequences. The CNY, EUR, and especially TWD would suffer. If Biden wins, he could face either gridlock or full Democratic control. The former case presents a greater risk of a focus on trade and foreign policy. The latter would result in a domestically focused Washington, which gives China breathing space. The CNY and EUR would benefit, but the TWD would face limited upside. Either way, investors are likely to become over-exuberant about assets that are exposed to the US-China relationship in the event of a Biden victory. Over the long run, this is a bull trap. Feature In the years after the 2008 financial crisis, the global news media proclaimed the rise of China and the demise of the United States as a global leader. The US’s free-wheeling democracy and capitalism led to economic collapse, partisan gridlock, and nearly a self-inflicted default on sovereign debt. Meanwhile China’s state-controlled system stimulated its economy, cracked down on the first inklings of unrest in the spring of 2011, and expanded its regional and global influence. The conclusion is similar today in the wake of the COVID-19 crisis. The US has squandered its response to the pandemic, while partisan gridlock threatens the economic recovery. China has suppressed the virus that started within its borders and its economy is rapidly on the mend. The orgy of social unrest and political dysfunction in the US has weighed on its international image and leadership. What the past decade showed, however, is that the first narrative to take hold after a global crisis is not likely to be the final narrative. In fact, the past decade was the most difficult for China since the 1980s. The next decade will be even more challenging. The COVID-19 pandemic brought to an official conclusion the unprecedented economic boom of the past four decades (Chart 1). Though Chinese policy makers have navigated relatively well, the social and political system faces greater challenges in a new economic and international environment. Chinese potential GDP growth has now fallen to 3%, as the labor force contracts and productivity remains flat. Chart 1China Already Plucked The Long-Hanging Fruit

China Already Plucked The Long-Hanging Fruit

China Already Plucked The Long-Hanging Fruit

China is well-situated in the short run to benefit from domestic and global economic stimulus, but over the long run its challenges are significantly underrated. China Faces Headwinds From Abroad Chinese leaders are prepared for any of the possible outcomes in the US election. With regard to US foreign and trade policy, the election is about tactics, not strategy. US grand strategy clearly dictates that Washington focus on curbing China, which is the only country that can challenge the US for global supremacy over the long run. But the US is not alone – other countries are also taking a more skeptical stance toward China’s geopolitical prominence. The result is that China will continue to emphasize self-sufficiency, a centrally guided economic model, and state-supported technological advancement in its fourteenth Five Year Plan for 2021-25 (see Appendix). This policy trajectory, combined with the key policy developments of the past decade, suggests that China’s self-sufficiency drive will continue to attract geopolitical opposition from the US and the West: Capital Controls: China tightened its capital controls aggressively during the financial turmoil of 2015-16. This emergency decision undercut the liberal reform agenda and alienated the western world on one of its critical structural demands. With China having grown its money supply from 175% to 197% of GDP since 2009, and capital flowing out again amid this year’s crisis (Chart 2), Beijing will not be able to fully liberalize its capital account anytime soon. Chart 2China's Capital Controls

China's Capital Controls

China's Capital Controls

Chart 3China's State-Owned Enterprises Revived

China's State-Owned Enterprises Revived

China's State-Owned Enterprises Revived

State-Owned Enterprises: The current administration has struggled with slowing trend growth and deflationary pressures. This is not an environment opportune for restructuring or liquidating inefficient state-owned enterprises (SOEs). It is the opposite of the 1990s, when SOEs were last culled. The regime has instead promised to make SOEs bigger and stronger (Chart 3). While it has pursued reforms to allow more private ownership of state assets, it has also encouraged public ownership of private assets, thus producing “mixed ownership” and a fusion of state and corporate power. The US and western countries resent this reassertion of state-backed economic power, notwithstanding the fact that all countries are increasing state support amid the collapse in global demand. Notably, China will likely resist cutting manufacturing capacity any faster than it will already be cut due to the global recession and foreign protectionism, meaning that stimulus-fueled overcapacity will continue to be a problem for foreign competitors. Chart 4The Tech Race Continues

The Tech Race Continues

The Tech Race Continues

The Tech Race: Beijing is continuing a frantic dash to upgrade its science and technology capabilities in order to lift total factor productivity, which is essential to maintaining growth in the coming decades in the post-export-industrial phase. Expenditures on research and development are skyrocketing, now rivaling the United States. True, R&D spending is flattening out as a percentage of GDP, but this is likely temporary — even faster R&D spending will probably become an official target for the next five years (Chart 4). The full weight of the political system is being thrown behind the goal of creating a “Great Leap Forward” in advanced and emerging technologies. Western countries are increasingly sensitive to China’s advances in semiconductor manufacturing, artificial intelligence, new vehicles, new energy, new materials, and computing. The new strategy of “dual circulation” will consist of import substitution, especially for critical tech goods, and will incorporate programs like “Made in China 2025” as well as “new infrastructure” that are high tech and have become targets of the West. The US and others are openly adopting export controls and reducing supply chain dependency on China. Beijing will struggle to maintain its rapid innovation drive without inviting more punitive measures from the West. Chart 5US Fears China’s Military Rise

Is China Afraid Of Big Bad Biden?

Is China Afraid Of Big Bad Biden?

Military Spending: China adopted a more assertive foreign policy in the mid-2000s and intensified this approach after 2012. Military spending has risen along with economic heft and western experts have long believed that China spends considerably more than it lets on. If we assume that China began to spend 3.75% of GDP per year after its strategic break with the US – a reasonable number in keeping with Russia’s long-term average – then China is narrowing the defense spending gap with the US more rapidly than is widely believed (Chart 5). Given the US’s giant defense spending, this is a continual source of distrust. Bear in mind that China’s defense and security aims are more limited than those of the US, at least in the short run. While the US must maintain the ability to project power globally, China need only grow its regional sphere of influence. Regionalism: While the Xi administration consolidates power within the Communist Party and central government in Beijing, it is also consolidating Beijing’s authority within Greater China. This includes efforts to bring to heel wayward provinces and regions such as Xinjiang, Tibet, Hong Kong, and Taiwan. Much of this is a fait accompli that western governments can do little about. Even in Hong Kong, public opinion is showing signs of resignation to the new legislative powers that Beijing has asserted. However, Taiwan is the clear outlier. Public opinion has shifted sharply against mainland China. Given that Taiwan is the epicenter of the new cold war with the US, both for reasons of political legitimacy as well as technological capability, a fourth Taiwan Strait crisis is looming (Chart 6). China has economic leverage to use first, but if this fails then a military confrontation cannot be ruled out. The above points do not hinge on the US election outcome or other cyclical factors, and highlight that geopolitical tensions will persist, particularly with the United States. The US’s adoption of a confrontational rather than cooperative posture toward China is a paradigm shift in international relations. Unlike Washington’s crackdown on Japanese trade in the 1980s, the US and China do not have an underlying trust or sense of shared security interests. Beijing’s willingness to increase US imports or appreciate its currency arbitrarily, to suit the shifting demands of US administrations, have substantial limits. Economic decoupling will continue in an environment of strategic insecurity (Chart 7). Chart 6Struggles In Greater China

Is China Afraid Of Big Bad Biden?

Is China Afraid Of Big Bad Biden?

Chart 7US Redistributes Trade Deficit

US Redistributes Trade Deficit

US Redistributes Trade Deficit

President Trump’s biggest mistake in pursuing his trade war with China lies in his failure to build a grand alliance, or coalition of the willing, among likeminded liberal democracies. This would have amplified his leverage over China in making demands for structural reform and opening up. But this point can be overstated. China’s international image has collapsed, in Europe and Asia as well as in North America, despite the Trump administration’s diplomatic failures. Much of this effect stems from COVID-19, but that does not mean it is less grave. If the US courts allies in the trade conflict with China, it will find governments willing to cooperate (Chart 8). Chart 8China’s Image Suffers Under Trump

Is China Afraid Of Big Bad Biden?

Is China Afraid Of Big Bad Biden?

Map 1Proxy Battles In Asia Pacific

Is China Afraid Of Big Bad Biden?

Is China Afraid Of Big Bad Biden?

Chart 9US Arms Sales To Taiwan

US Arms Sales To Taiwan

US Arms Sales To Taiwan

China’s perennial geopolitical challenge is shown in Map 1. It is geographically encircled by nations that have grown increasingly wary of its regional ambitions and will reach out to the US and West. These countries wish to continue benefiting from China’s economic rise but seek security guarantees to offset China’s rising strategic clout. The result will be “proxy battles,” in some cases political, in others military (Chart 9). Taiwan, South Korea, the Philippines, and Vietnam each face substantial geopolitical risk. In the case of South Korea and the Philippines, this risk is partially priced by financial markets. But in the case of Taiwan and Vietnam, it is almost entirely underrated. Taiwan has only an ambiguous defense commitment from the US, while Vietnam is a Chinese rival that entirely lacks a security guarantee from the United States. Bottom Line: Geopolitical risk will remain elevated in Asia Pacific regardless of what occurs in the US election. The growth of Chinese power, and its state-led economic model, will ensure that trade tensions persist. These will culminate in strategic conflicts in certain neighboring countries. China Will Re-Consolidate Power When Trump was inaugurated in January 2017, we argued that the looming US-China trade war would not be determined solely by relative economic size and export exposure. Instead, political unity would be a critical factor. While the US ostensibly had the economic advantage, China had the political advantage. The nineteenth National Party Congress would see Xi Jinping consolidate power domestically, while President Trump would struggle with domestic opposition and divisions within the US and the West over his protectionism. Having secured an economic rebound this year, China is likely to consolidate domestic power even further in 2021-22. This period culminates in the critical twentieth National Party Congress. Originally Xi Jinping was expected to step down at this time and hand the reins to the leader of the opposing faction. Now the opposing faction has been laid low, and Xi is likely to promote his faction and entrench his rule. The period will likely be marked with at least one major crackdown on the regime’s political rivals. Ultimately, social and political control will be tightened, particularly beginning in late 2021. These events provide good reasons for anticipating that Chinese monetary, fiscal, and regulatory policy will not tighten drastically, but rather will merely normalize by mid-2021, assuming that the recovery stays on track (Chart 10). Yet this logic only goes so far – it is more bullish for the macro view today and in 2021, than it is in 2022. Obviously the regime wants to avoid a slump in 2021, the hundredth anniversary of the Communist Party, and investors should keep this in mind. But the 2017 party congress was attended by a deleveraging campaign that surprised the world in its intensity. The point is that stability, not rapid growth, is the imperative in 2022. If speculative bubbles have become a greater threat by that time, then the monetary and fiscal policy backdrop will lean hawkish rather than dovish. Tightening central control over the economy helps the Xi administration consolidate power. Chart 10China Still Consolidating Domestic Power, 2021-22

China Still Consolidating Domestic Power, 2021-22

China Still Consolidating Domestic Power, 2021-22

US Polarization A Risk For China If China continues to consolidate, the key question is what will happen in the United States. The answer will be known in short order, but what is critical to observe is that US political polarization is a geopolitical risk, and therefore if it continues to escalate it will be positive for the US dollar and negative for Chinese and other emerging market assets. The past several years have been marked by an increase in US social and political instability. Indeed, according to Worldwide Governance Indicators, the US’s governance has declined while China’s has improved, notably on the issue of political stability and the absence of violence (Chart 11). While these rankings are partial, nevertheless they point to the reality of US political division. The decade’s giant increase in political polarization has coincided with a bull market in US equities and the greenback, best exemplified by the outperformance of the US technology sector (Chart 12). Chart 11US Instability A Source Of Global Risk

Is China Afraid Of Big Bad Biden?

Is China Afraid Of Big Bad Biden?

If President Trump prevails, this trend will continue. Trump cannot win the popular vote, but his regional support could grant him a victory in the Electoral College. Or he could prevail through a contested election adjudicated by the Supreme Court or the House of Representatives. If this should occur, polarization will intensify, as the government’s legitimacy will suffer due to lack of popularity in a democracy. Facing gridlock at home, Trump would pursue trade war – not only with China, but also conceivably with the European Union. The consequence is that a surprise Trump victory (45% odds) would be negative for the euro, the renminbi, and especially the Taiwanese dollar (Chart 13). Chart 12US Polarization Reinforces Safe-Haven Status

US Polarization Reinforces Safe-Haven Status

US Polarization Reinforces Safe-Haven Status

Chart 13Trump Second Term Would Weigh On CNY, EUR, TWD

Trump Second Term Would Weigh On CNY, EUR, TWD

Trump Second Term Would Weigh On CNY, EUR, TWD

However, if former Vice President Biden prevails, he could win in two possible ways: one with gridlock in Congress, the other with a Democratic sweep of the House and Senate. In the former case, US polarization will persist. Biden will be incapable of executing his domestic agenda, as he will be obstructed by a Republican Senate. This will drive him into foreign policy, where he will ultimately prove to be tough on China – and certainly tougher than the Obama administration. In the latter case, a Democratic sweep of legislative and executive branches, Biden will not face domestic constraints and will be primarily focused on an ambitious agenda for rebuilding and rebalancing the US economy, with elements of the New Deal and the Green New Deal. He will be less focused on international affairs, at least initially. Trade risks will decline, along with US fiscal risks, thus producing a higher-growth macro policy environment. In both cases, while we expect a President Biden to seek a diplomatic “reset” with China, he is unlikely to repeal President Trump’s tariffs. Instead he will seek to utilize the leverage that Trump has built up, while pursuing a new strategic and economic dialogue with China. Ultimately this dialogue will be undermined by China’s state-backed economic policies and foreign policy assertiveness (see previous section), as well as Biden’s simultaneous courting of Europe and other liberal democracies. But clearly there is more room for Chinese assets to outperform under a Biden victory, especially a Democratic sweep. Investment Takeaways If Biden wins, the stock market is likely to become overly exuberant about a Biden administration’s positive implications for China-exposed companies (Chart 14). The same can be said for Chinese tech companies that are highly export-oriented (Chart 15). In a Democratic sweep, this rally can be prolonged, as US equities will face greater political risk than international equities. But any rally in assets exposed to the US-China relationship will ultimately be a bull trap, as US grand strategy calls for containing China, while Chinese grand strategy calls for breaking through containment. The US and Chinese tech sectors and Taiwanese assets are by far the most vulnerable to this dynamic, given their lofty valuations. Chart 14Market Over-Optimistic On Biden Boost To China Plays

Market Over-Optimistic On Biden Boost To China Plays

Market Over-Optimistic On Biden Boost To China Plays

Chart 15Chinese Tech Faces Trade Tensions

Chinese Tech Faces Trade Tensions

Chinese Tech Faces Trade Tensions

If we are correct that geopolitical risk will persist for China regardless of US political party, then the primary beneficiaries of Chinese stimulus and US decoupling will be domestic-oriented Chinese equities as well as “China plays” – external markets that export machinery and resources to China, such as Australia, Brazil, and Sweden. China will still invest heavily in traditional infrastructure, property, and manufacturing to shore up demand whenever it sags amid the difficulties of the economic transition. Our China Play Index, designed by Mathieu Savary of our flagship The Bank Credit Analyst, neatly captures the potential for this index to outperform on the back of Chinese stimulus, which will be even more necessary if US policy continues to be punitive (Chart 16). The near term could involve substantial US fiscal risks as well as geopolitical risks with China, which can occur under a gridlocked Biden administration or a second term Trump administration. Over the next year, the looming Chinese and global recovery, combined with ultra-dovish US monetary policy, spells continued downside for the US dollar and upside for Chinese and emerging market currencies and risk assets (Chart 17). But while the dollar may face challenges to its reserve currency dominance, China’s geopolitical risks, at home and abroad, will prevent the renminbi from making more than incremental gains on the dollar. The euro is a much likelier alternative for the foreseeable future. Chart 16China Plays Will Benefit From Reflation

China Plays Will Benefit From Reflation

China Plays Will Benefit From Reflation

Chart 17King Dollar Persists … But Cyclical Downside Looms

King Dollar Persists ... But Cyclical Downside Looms

King Dollar Persists ... But Cyclical Downside Looms

Appendix Table 1China’s 14th Five Year Plan Goals

Is China Afraid Of Big Bad Biden?

Is China Afraid Of Big Bad Biden?

Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com

Chinese Reflation: Money & Credit Growth Versus Rising Real Interest Rates

…

BCA Research's China Investment Strategy service expects Chinese onshore and offshore property stocks to continue underperforming their respective benchmarks. However, the team recommends buying Chinese property developers’ offshore corporate bonds. The…