China

Highlights Lower-income Chinese households are overly indebted, while higher-income groups hold too much cash. Apart from real estate and cash, ordinary Chinese people have few choices in allocating their assets. Household consumption has not been stimulated to the same degree as during previous cycles. The recently announced “dual circulation” strategy may not be an imminent solution to China’s chronic high debt, high savings issue. However, an acceleration in policy actions of late may be steps in the right direction in encouraging Chinese households to spend more domestically and to invest in domestic companies. Feature The post-COVID 19 recovery in China’s household consumption has lagged behind other economic segments, such as production and exports. Notably, the pace of consumer spending growth started decelerating almost two years before the pandemic struck the country (Chart 1). Chart 1Chinese Consumers Scaled Back Spending Before COVID-19

Chinese Consumers Scaled Back Spending Before COVID-19

Chinese Consumers Scaled Back Spending Before COVID-19

Chart 2Chinese Households Save Cash, Lots Of It

Chinese Households Save Cash, Lots Of It

Chinese Households Save Cash, Lots Of It

Furthermore, Chinese households have added a total of 8.3 trillion yuan to their bank deposits so far this year, or about 8% of China’s 2019 national output (Chart 2). Outsized cash savings helped to cushion consumers from the pandemic’s economic impact and will support a consumption rebound as China’s economic and service sector activities continue to normalize. However, an acceleration in cash savings and decline in households' propensity to spend would not bode well for a structurally balanced economic growth model. Chinese policymakers recently announced a new “dual circulation” strategy, and fast-tracked several policy actions to facilitate easier access for households to consume luxury goods and participate in the domestic capital markets. The policies will likely have a small, near-term economic impact. But in the long run they can set up a trend which will benefit domestic consumption growth and better utilize the substantial cash holdings among Chinese domiciles. Too Much Saving Or Too Much Debt? While Chinese households have excessive cash savings, they also carry too much debt. Families hold a total of 55 trillion yuan of debt, or 94% of their aggregate disposable income. The debt-to-income ratio is fast approaching that in the US (Chart 3). At the same time, their debt-to-cash ratio, on an aggregate basis, is extremely low relative to other countries (Chart 4). Chart 3Chinese Households Are Almost As Leveraged As The US Ones

Chinese Households Are Almost As Leveraged As The US Ones

Chinese Households Are Almost As Leveraged As The US Ones

Chart 4But They Also Hold Way More Cash Than The US Ones

Chinese Consumers And The “Dual Circulation” Strategy

Chinese Consumers And The “Dual Circulation” Strategy

Chinese people are net savers, and only about 30% of Chinese families are in debt, which is less than half of the number in the US (Chart 5 and Table 1). This means approximately two-thirds of households have a positive net worth. On the other hand, Chinese consumers who borrow are deeply indebted. China’s median debt-to-income ratio is around 180%, according to recent surveys, with the lowest income group carrying debt loads that are a whopping 12 times their income (Table 2). Chart 5Two Thirds Of Chinese Households May Be Debt Free

Chinese Consumers And The “Dual Circulation” Strategy

Chinese Consumers And The “Dual Circulation” Strategy

Table 1Chinese Household Credit Participation Rate

Chinese Consumers And The “Dual Circulation” Strategy

Chinese Consumers And The “Dual Circulation” Strategy

Table 2Chinese Household Debt-To-Income Ratio, By Income Groups

Chinese Consumers And The “Dual Circulation” Strategy

Chinese Consumers And The “Dual Circulation” Strategy

Bottom Line: Lower-income groups are heavily indebted, while higher-income families have too much cash on hand. Too Few Investment Choices Chinese households hold a majority of their assets in real estate investments and cash. The former has seen prices skyrocket, crowding out the discretionary spending capability of lower-income families.1 On the other hand, cash and cash equivalents such as CDs, currently earn a meager 2%. The obsession with holding properties has been reinforced by the astonishing pace of money creation in the past 10 years (Chart 6). Despite sky-high prices, real estate has been the main counter-inflation measure in China. According to the 2019 China Household Finance Survey, nearly 60% of Chinese household debt is in home loans, which is about twice the number compared with the US. Furthermore, the share of second-home loans (as a share of all residential housing loans) escalated from less than 30% in 2011 to 65.9% in 2018, greatly exceeding the share of first home loans. Post-pandemic demand for housing has remained strong and household debt is still expanding faster than nominal disposable income growth (Chart 7). Even though lower-income groups have significantly scaled back on mortgages, given that such a large portion of household assets is tied up in real estate means that any deflation in property prices will have a devastating impact on consumer net worth (Table 2 on Page 4). Consequently, discretionary spending by even middle- and high-income households will be curtailed. Chart 6Helicopter Money In China

Helicopter Money In China

Helicopter Money In China

Chart 7Household Credit Still Expands Faster Than Income Growth

Household Credit Still Expands Faster Than Income Growth

Household Credit Still Expands Faster Than Income Growth

In addition to the long-standing issue of a lack of social safety net, Chinese families’ high cash holdings are due to a lack of investment alternatives. Even though the country has the world’s second largest equity market by value, only 11% of Chinese residents participate in the stock market, a dismal number compared with a 50% equity market participation rate in the US.2 The low participation rate is not surprising: over a 10-year time span, returns on cash have more or less matched returns on A-share stocks (Chart 8). The extreme volatility in Chinese equities has curbed citizens’ enthusiasm to participate in the market. Chart 8Risk-Reward Profile Of Chinese Stocks Hasn't Been Great Over The Past Decade

Risk-Reward Profile Of Chinese Stocks Hasn't Been Great Over The Past Decade

Risk-Reward Profile Of Chinese Stocks Hasn't Been Great Over The Past Decade

Bottom Line: Chinese household profile is characterized by the heavy concentration of cash among higher-income households and the elevated indebtedness of low-income ones stemming from sky-high real estate prices. Is The New “Dual Circulation” Strategy A Solution? Consumer spending in China has been growing rapidly in the past 20 years, at a rate roughly in line with the increase in disposable incomes. Income and consumption growth peaked in 2007 but since then has been dwindling along with falling productivity (Chart 9). Cyclically, the consumption recovery will bring its growth rate back to the pre-COVID 19 level. Demand for real assets and consumer durable goods has been strong after the pandemic (Chart 10). Even the demand for luxury goods has made a comeback.3 Chart 9Chinese Consumption, Income, And Productivity Growth

Chinese Consumption, Income, And Productivity Growth

Chinese Consumption, Income, And Productivity Growth

Chart 10Chinese Consumption Is Recovering

Chinese Consumption Is Recovering

Chinese Consumption Is Recovering

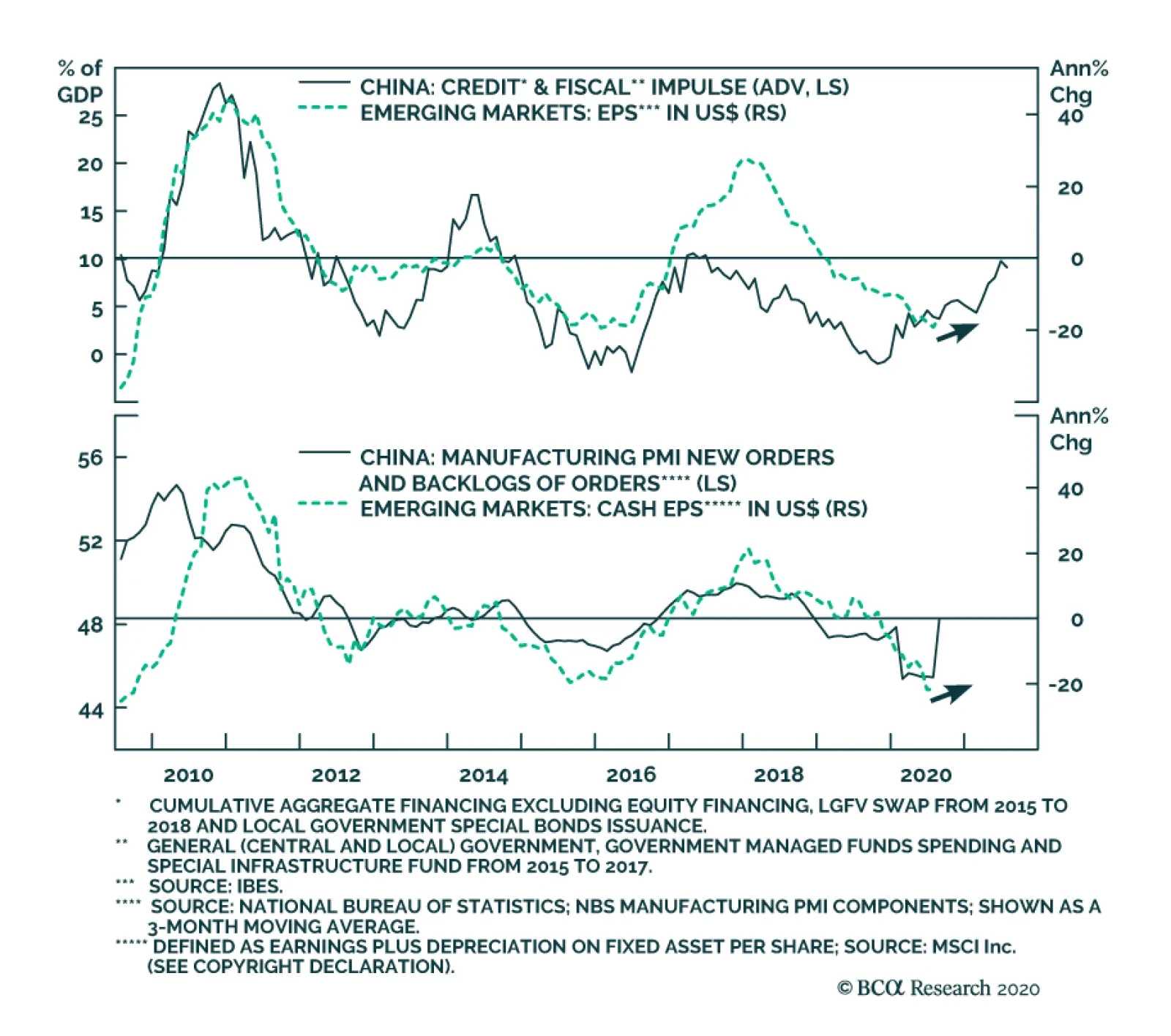

However, for consumption to sustain an expansion rate similar to the past decade, China’s productivity growth must accelerate and, in turn, boost per capita income growth. Conversely, the country would need to maintain a high rate of credit expansion to generate enough economic growth and inflation to spur strong nominal income growth (Chart 11). Credit expansion can boost nominal growth but it is productivity growth that generates per capita income growth. Chart 11Household Credit Impulse Has Been Muted Since 2018

chart 11

Household Credit Impulse Has Been Muted Since 2018

Household Credit Impulse Has Been Muted Since 2018

The recently announced “dual circulation” strategy and an acceleration in policy actions by the Chinese leadership may suggest a different path than in previous cycles. Policymakers seem to focus on changing and upgrading the composition of China’s existing consumption base rather than boosting consumption growth through monetary stimulus in the household sector. Moreover, they are looking to change the configuration of family savings and investments. Our colleagues at BCA Research's Emerging Markets Strategy have stated that improvements in the turnover of consumers’ bank deposits and cash, if successful, may allow China to slow its overall credit and money growth but still sustain a steady nominal GDP growth rate.4 Details of the new “dual circulation” strategy are sparse, but we think the following developments in the past couple of months are relevant to investors: Bringing home overseas consumption and reducing the service trade deficit: China fast-tracked policies that target duty-free shopping venues, a strategy designed to lure Chinese consumers back to the domestic market. Beijing made unprecedented moves to invigorate Hainan province’s duty-free shopping and issue new licenses to allow companies to operate duty-free shops both online and offline. In the past five years, Chinese residents have spent an average of 250 billion USD annually shopping overseas. Purchases of duty-free products overseas account for a small share of China’s 12.5 trillion yuan retail industry. Nonetheless, repatriating some overseas consumption would allow China to not only narrow its service trade deficit, but also to create more service businesses and jobs internally (Chart 12). The move signifies that Chinese policymakers are committed to change domestic consumer spending behavior while upgrading the retail industry. However, we remain cautious on retail stocks in the next 6 to 12 months. Retail growth has not yet rebounded to its pre-pandemic level, and the valuations in retail-sector stocks are overly stretched (Chart 13). Chart 12China Has Been Running A Huge Service Trade Deficit

China Has Been Running A Huge Service Trade Deficit

China Has Been Running A Huge Service Trade Deficit

Chart 13Retail Sector Valuations Are Elevated

Retail Sector Valuations Are Elevated

Retail Sector Valuations Are Elevated

Increasing households’ equity holdings in domestic companies: Direct financing in the form of equities and corporate bonds only accounts for about 15% of total social financing, compared with 65% in bank lending. Chinese corporations rely mostly on bank loans and retained earnings, whereas US companies are heavily dependent on equity financing. The “dual circulation” strategy encourages more direct financing for SMEs, science and technology companies. It also explicitly calls for a greater household participation in the financial markets, which would guide more savings into domestic capital markets. In the past few months, the government has accelerated financial market reforms aimed at providing easier access for corporations and individuals to domestic equity markets. In the first half of this year, 119 companies went public in Shanghai and Shenzhen; these companies raised about 140 billion yuan, which was more than double the amount from a year ago. New individual investor accounts on the Shanghai exchange rose by 30% (year to date) from a year ago. Notably, both the IPO and household participation rates resemble the onset of the boom-bust cycle in 2015. However, this time Chinese regulators have been much more vigilant and restrictive about over-leveraging, acting early and removing some steam from retail investor rush (Chart 14). Chart 14Chinese Authorities Have Less Tolerance For Equity Market Leverage

Chinese Authorities Have Less Tolerance For Equity Market Leverage

Chinese Authorities Have Less Tolerance For Equity Market Leverage

Chart 15Chinese Stocks Still Have Upside Potentials

Chinese Stocks Still Have Upside Potentials

Chinese Stocks Still Have Upside Potentials

It remains to be seen whether the authorities will be able to boost and sustain consumer confidence in the domestic equity market. The efforts by the Chinese government will either succeed by securing a gradual and healthy secular bull market, or they will fail by triggering another boom-bust cycle in the domestic market. Either way, investors should stay overweight Chinese stocks on at least a 6-month horizon (Chart 15). Jing Sima China Strategist jings@bcaresearch.com Footnotes 1Households in the bottom 40 percentile in China have no discretionary spending capacity. “Can China Avoid the Middle Income Trap?” Damien Ma, Foreign Policy, March 2016 2投保基金公司《2019年度全国股票市场投资者状况调查报告》and Pew Research Center. 3China ‘Revenge Spending’ Offsets Plunge in Luxury Goods Revenue 4Please see Emerging Markets Strategy Special Report "China’s Rebalancing: Will Consumers Rise To The Challenge?" dated August 29, 2019, available at ems.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

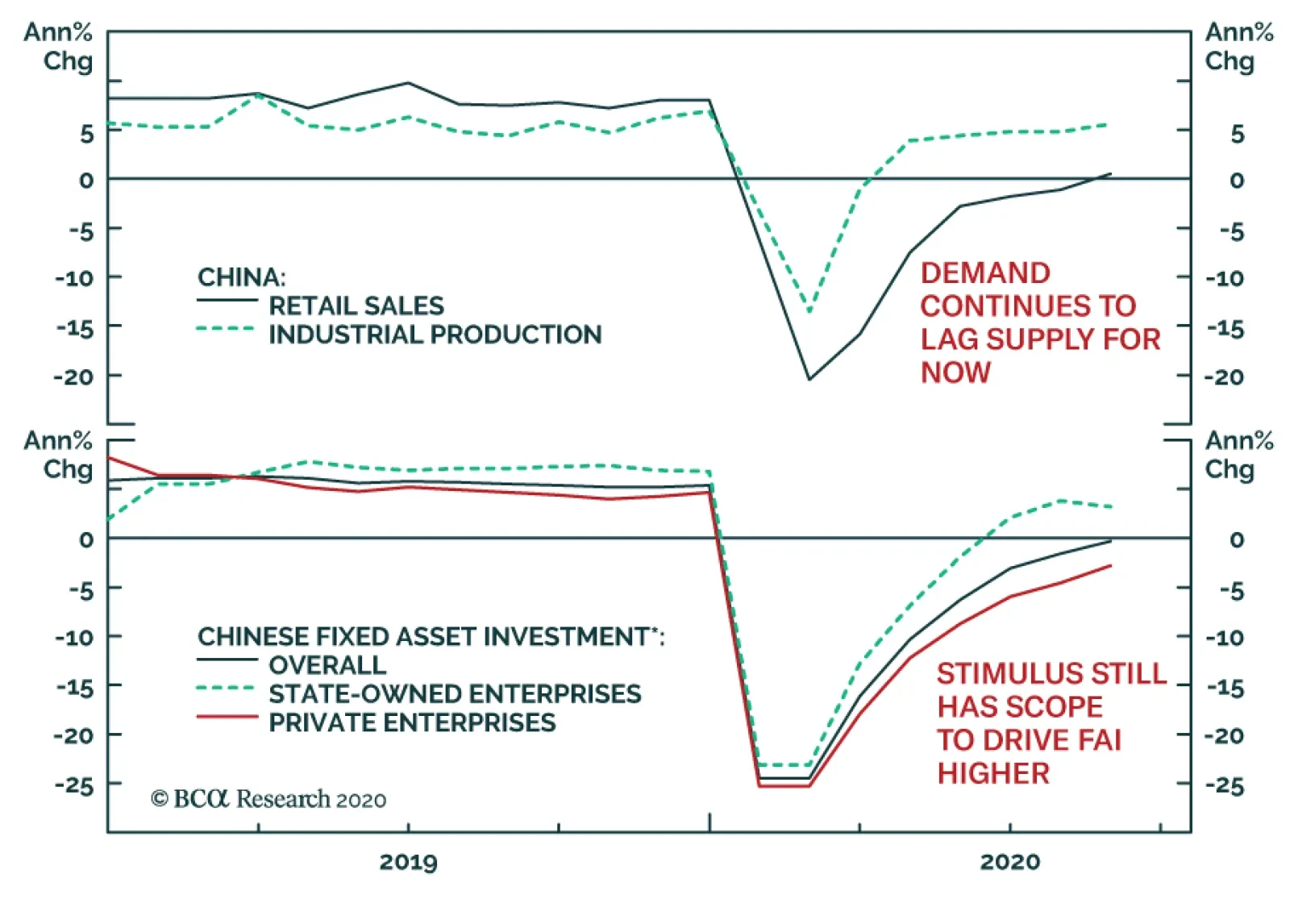

In August, China’s industrial production strengthened further, rising to 5.6% year-on-year and beating consensus expectations of 5.1%. Fixed-asset investment also picked up, moving up from -1.6% to -0.3% year-on-year. While private capex continues to…

In August, China’s credit trends continued to point to a positive outcome for the global industrial cycle. While new loans only met expectations of CNY 1.28 trillion, total social financing (TSF) blew past expectations of CNY 2.59 trillion by rising by…

Highlights China’s surge in refined copper imports allows it to cover a structural short position it has in this critical commodity – mostly in its unrefined state – and ensures the stimulus being deployed to revive its economy ahead of the 100th anniversary of the founding of the Communist Party in July will not falter due to a lack of basic raw materials (Chart of the Week). We expect continued resilience in commodities generally into 2021 – particularly in base metals, iron ore and crude oil – as markets realize China’s Communist Party is intent on showcasing its brand of policy-driven, vertically integrated capitalism as the engine of its robust economic growth. As with oil, we expect copper demand will benefit from a weaker USD and stronger global trade. The odds of a COVID-19 vaccine being available by year-end or early 2021 remain favorable, which also will support a revival in demand.1 We are keeping our COMEX copper forecast at $3.00/lb at end-2020, and expect 2021 to finish at $3.15/lb. We would not be surprised by higher prices, and are, therefore, getting long December 2021 COMEX copper at tonight's close. Feature The surge in refined copper imports hedged Chinese firms against supply disruptions caused by the pandemic and reduced availability of scrap copper on global markets this year. COVID-19 may have derailed the Communist Party’s realization of the “Chinese Dream” this year, wherein the leadership vowed real per-capita GDP would double in the decade ending in 2020, but it is unlikely to diminish the celebration of the Party’s 100th anniversary in July.2 Chart of the WeekVol Falls As Know Unknowns Are Resolved

Vol Falls As Know Unknowns Are Resolved

Vol Falls As Know Unknowns Are Resolved

The global commodity-demand destruction caused by the COVID-19 pandemic depressed the prices of commodities generally, particularly those which China is structurally short – e.g., copper, iron ore, oil and natural gas. As terrible as the pandemic has been in human terms, it has allowed Chinese firms and the State Reserve Bureau to sharply increase imports of refined copper, which rose 34% in the January-to-July period to 2.5mm MT amid such low prices, which bottomed at $2.10/lb in late March and now are trading above $3.00/lb.3 China accounts for more than 50% of global refined copper consumption and ~ 40% of refined production (Chart 2).4 Chart 2China Dominates Metals Consumption

China's Copper Buying Spree Heralds Communist Party's Centenary Celebrations

China's Copper Buying Spree Heralds Communist Party's Centenary Celebrations

The surge in refined copper imports hedged Chinese firms against supply disruptions caused by the pandemic and reduced availability of scrap copper on global markets this year. Global copper ore and concentrate supply fell ~ 3% y/y in 2Q20, led by a 28% decline in Peru’s mine production, according to the World Bureau of Metal Statistics (Chart 3). This was a result of containment policies that limited mining activities to slow the pandemic’s spread in Latin America. In Chile, COVID-19 cases stabilized in recent months at around 100 per million people (Chart 4). In Peru, cases have been declining since August, but from an elevated level. Supply is expected to recover rapidly as these economies reopen, but further mine disruptions remain a risk. Chart 3Peru's Copper Ore Supplies Recovering

Peru's Copper Ore Supplies Recovering

Peru's Copper Ore Supplies Recovering

Chart 4COVID-19 Copper Supply Risks Falling

COVID-19 Copper Supply Risks Falling

COVID-19 Copper Supply Risks Falling

Commodity-Demand Indicators Move Higher we expect the effect of expansionary monetary and fiscal policies globally will continue to show up in our indicators and for the US dollar to resume its downward trajectory. Global central banks and government stimulus unleashed in the wake of the COVID-19 pandemic, combined with a depreciating US dollar, pushed our commodity-demand indicators higher over the last few months (Chart 5). This supported copper prices, which are up 42% since their March 23 low. Moreover, the pickup in economic activity in China’s major trading partners provided further support to copper demand, given that ~ 17% of China’s copper consumption comes from exports of products containing copper (Chart 6).5 Chart 5Commodity Demand Is Reviving

Commodity Demand Is Reviving

Commodity Demand Is Reviving

Chart 6Expect Chinese Employment Gains As Economy Continues To Recover

Expect Chinese Employment Gains As Economy Continues To Recover

Expect Chinese Employment Gains As Economy Continues To Recover

For the balance of 2H20, we expect the effect of expansionary monetary and fiscal policies globally will continue to show up in our indicators and for the US dollar to resume its downward trajectory. These are key factors driving our positive view on metal – especially copper – prices. Communist Party’s 100th Anniversary Will Boost Commodity Prices China’s buying spree for commodities it is structurally short – particularly copper, iron ore and oil – minimizes the risk fiscal and monetary stimulus deployed to revive its economy will be derailed this year or next. This is particularly important next year: We expect stimulus will continue and will be hitting the economy full force in time for the Communist Party’s centennial celebrations in July. For the infrastructure and construction spending that will be spurred by the massive stimulus, this is critical to spurring employment – a key goal of the Party’s domestic harmony focus – domestic manufacturing, services, and exports (Chart 6).6 This will keep demand for copper – and commodities generally – strong into 2021, as markets realize China’s Communist Party is intent on showcasing its brand of policy-driven, vertically integrated capitalism as the engine of its world-beating economic performance. And, because stocks of critical commodities are increasing as stimulus is hitting the domestic economy next year, the risk of massively inflating prices while the county is celebrating the Party’s centennial in July – as happened following the Global Financial Crisis (GFC) – is minimized, but not completely eliminated (Chart 7). Chart 7COMEX Stocks Will Move To China

COMEX Stocks Will Move To China

COMEX Stocks Will Move To China

That said, we still expect copper to move higher next year. In our modeling of prices, we note world PMIs, EM FX rates, the USD, also drive copper prices, in addition to those factors discussed above specific to China. We expect COMEX high-grade copper prices to end 2020 at $3.00/lb, and to average $3.11/lb next year (Chart 8). On the back of this expectation, we are getting long December 2021 COMEX copper at tonight’s close, expecting 2021 to end at $3.15/lb. Chart 8Copper Prices Expected To Increase

Copper Prices Expected To Increase

Copper Prices Expected To Increase

Risks To Our Copper View Geopolitical risks remain the chief threat to our bullish copper view. The US Presidential election campaign rhetoric, in particular, has turned bellicose vis-à-vis China, with President Donald Trump threatening to “decouple” economically from China if he is reelected.7 These sorts of pronouncement threaten to escalate what could now be considered a trade dispute to an all-out trade war, particularly if it includes sanctions against US firms investing in manufacturing and services in China, as Trump promises. At the limit, this would put a long-term bid under the USD, and reverse the nascent recovery in commodity demand resulting from a weaker dollar. Outright military confrontation between the US and China also is a risk, particularly as tensions in the South China Sea and the Asia-Pacific region continue. The most likely confrontation would be an escalation of hostilities resulting from a naval or aerial face-off, the number of which has been steadily increasing. The threat of a second wave of COVID-19 also remains a risk, particularly if it results in another round of lockdowns globally. That said, we believe the odds of this are very low, as the capacity to absorb another shutdown in economic activity in DM and EM economies likely has been exhausted by measures already implemented this year. It is highly unlikely any economy can afford another round of economic shutdown without triggering an economic depression. Bottom Line: China’s surge in refined copper imports allows it to cover its structural short position in the commodity, and, equally importantly, to ensure an expected revival of economic activity into 2021 – when the Communist Party celebrates its 100th anniversary – will not falter because it lacks basic raw materials. We are keeping our COMEX copper forecast at $3.00/lb at end-2020, and expect 2021 prices to average $3.11/lb. On the back of this expectation, we are getting long December 2021 COMEX copper at tonight’s close. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Hugo Bélanger Associate Editor Commodity & Energy Strategy HugoB@bcaresearch.com Commodities Round-Up Energy: Overweight Brent prices dipped below $40/bbl for the first time since mid-June. Prior to this move, prices had been stable in a narrow range around $43/bbl since mid-June. Pessimism is increasing re the outlook for demand, as Saudi Arabia reduced its official selling prices (OSPs) for crude delivered to Asian buyers by $1.40/bbl. The negative sentiment was exacerbated by the selloff in tech stocks that began last Thursday. WTI net speculative positions are down to 20% of total open interests vs. 22% in July, as hedge funds exit oil markets. Base Metals: Neutral The LMEX index is up 4% over the past four weeks, supported by higher metals’ consumption and imports in China. Moreover, mobility trends in Europe, Japan, and the US have begun to turn up again in recent weeks based on Apple mobility data. The recovery in China’s economic activity remains the main pillar of our base metals outlook. However, Europe, Japan, and the US still represent a non-negligible share of global metal demand (e.g. ~ 24% copper consumption). Hence, the recent uptick in mobility data is constructive for base metal prices. Precious Metals: Neutral Gold prices are down 2% since last week, pressured by a slight increase in the US dollar and real rates. The divergence in COVID-19 cases between the US and Europe increases the risk of a short-term bounce higher if this leads to the US economy outperforming that of the EU (Chart 9). Still, mounting geopolitical risks ahead of the US election, lower-for-longer interest rates, and a resumption of the downward trend in the USD over the medium term should support gold later this year. Ags/Softs: Underweight Soybean prices remain steady, near 2-year highs. The USDA crop progress report listed 55% of soybeans in good or excellent condition for the week ending September 6, 2020. This is a substantial deterioration compared to 66% in those categories last week and 73% at the beginning of August. Corn futures were supported by similar weak supply fundamentals. The USDA reported 55% of corn crops in good or excellent condition against 62% the previous week. Going forward, it will be important to monitor the DXY as it has been strengthening since the beginning of September and could be a headwind to these commodity prices if it breaks to the upside (Chart 10). Chart 9EU Cases Are Rising

EU Cases Are Rising

EU Cases Are Rising

Chart 10US DXY Strengthening

US DXY Strengthening

US DXY Strengthening

Footnotes 1 Please see Lower Vol As OPEC 2.0 Gains Control, published September 3, 2020, for additional discussion of vaccine availability. 2 Please see Iron Ore, Steel Poised For Rally, which we published February 13, 2020, for a discussion of the commodity-market implications of China’s dual policy goals of doubling GDP between 2010 and 2020 and preparing for the celebration of the 100th anniversary of the founding of the Chinese Communist Party in 1921. It is available at ces.bcaresearch.com. 3 Please see China's July refined copper imports surge 90% on year boosted by open arbitrage published by S&P Global Platts September 1, 2020. 4 China also accounts for close to 50% of copper ore imports, according to he Observatory of Economic Complexity (OEC). 5 Please see The Impact of the COVID-19 Pandemic on World Copper Supply, published by the International Copper Study Group on May 21, 2020. 6 For an update of the stimulus measures and China’s economic performance, please see China Macro And Market Review published September 9, 2020, by our China Investment Strategy colleagues. It is available at cis.bcaresearch.com. 7 Please see Trump threatens to ‘decouple’ U.S. economy from China, accuses Biden of ‘treachery’ published by marketwatch.com September 7, 2020. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Trade Recommendation Performance In 2020 Q2

Lower Vol As OPEC 2.0 Gains Control

Lower Vol As OPEC 2.0 Gains Control

Commodity Prices and Plays Reference Table Trades Closed in 2020 Summary of Closed Trades

Lower Vol As OPEC 2.0 Gains Control

Lower Vol As OPEC 2.0 Gains Control

BCA Research's China Investment Strategy service concludes that the fundamentals are supportive of a positive cyclical view on Chinese stocks. Despite some pullbacks in the prices of Chinese stocks of late, we do not think that the cyclical upturn in…

Highlights Economic data in August point to a faster recovery in demand than in production. The service-sector recovery is picking up speed; consumption growth remains negative, but will benefit from a steady rebound in the service sector. The strong upward momentum in China’s stock prices, on the other hand, has lost some steam since the second half of July. Policy supports and improving economic fundamentals still warrant a constructive stance on Chinese stocks over the coming 6 to 12 months. Feature Both soft and hard data released over the past couple of weeks indicate that China’s economic recovery remains on track. August’s official PMI new orders sub-index continued to advance, and the official non-manufacturing PMI made the largest month-to-month improvement since March when the Chinese economy reopened. Hard economic data, such as exports and sales of homes, cars and retail goods, show that both external and domestic demand growth is strengthening. Chart 1Chinese Stocks Taking A Breather From July's Rally, Despite Improving Economic Fundamentals

Chinese Stocks Taking A Breather From July's Rally, Despite Improving Economic Fundamentals

Chinese Stocks Taking A Breather From July's Rally, Despite Improving Economic Fundamentals

Despite the economic improvement, the July rally in Chinese stocks faltered in August and into the first week of September. Although stock prices are still 12-15% higher than the end of June and continue to outperform global benchmarks, they are slightly below their mid-July peak in absolute terms (Chart 1). The pause in China’s stock market was inevitable because of the stunning pace of acceleration in early July, which saw margin lending rise to explosive levels that invited Chinese policymakers to cool the market. Last week’s corrections in the high-flying US tech stock prices also dragged down some of the Chinese tech sector's top performers. US sanctions targeting China’s tech companies may exacerbate downward pressure on the sector’s performance. Therefore, we continue to recommend that investors hold a neutral position for the next three months on Chinese tech stocks, in both absolute and relative terms. The outlook for China’s economic growth and monetary conditions supports our constructive view on the overall Chinese stocks, over a cyclical (6 -12 months) horizon. In the near term, we prefer offshore stocks outside of the tech sphere, and prefer onshore semiconductor stocks within a global semi equity portfolio. China’s “old economy” sectors, such as industrials and materials, will continue to benefit from the ongoing massive stimulus. Furthermore, the semiconductor sector has become China’s new poster child, as the country ramps up longer-term, earnings-friendly policy supports to develop its domestic semiconductor industry and counter the Trump administration’s restrictions.1 Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Tables 1 and 2 present key developments in China’s economic and financial market performance in the past month, and we highlight several aspects below: China’s NBS manufacturing PMI was essentially unchanged in August (51 vs. 51.1 in July), but details of the survey imply that what has underpinned an industrial sector improvement this year remains in place. Although the production sub-index slowed, the new orders component increased, indicating that demand is strengthening relative to supply (Chart 2). The export orders component of the manufacturing PMI and the newly released trade data are both improving, suggesting that external demand is also holding up (Chart 2, bottom panel). The steel industry’s PMI fell to 47 in August from 49.2. As noted in last month’s China Macro And Market Review,2 the consistent outperformance in production recovery relative to demand since Q1 has led to an inventory buildup and a pullback in production. Inventory destocking will likely impede China’s imports of major commodities until the laggard recovery in industrial demand sustainably outpaces production (Chart 3). Chart 2Demands Are Improving On Both Domestic And External Fronts...

Demands Are Improving On Both Domestic And External Fronts...

Demands Are Improving On Both Domestic And External Fronts...

Chart 3...But Inventory Buildup Is Temporarily Impeding Production And Imports

...But Inventory Buildup Is Temporarily Impeding Production And Imports

...But Inventory Buildup Is Temporarily Impeding Production And Imports

Chart 4Accelerating Service Sector Recovery Should Give A Boost To Consumption

Accelerating Service Sector Recovery Should Give A Boost To Consumption

Accelerating Service Sector Recovery Should Give A Boost To Consumption

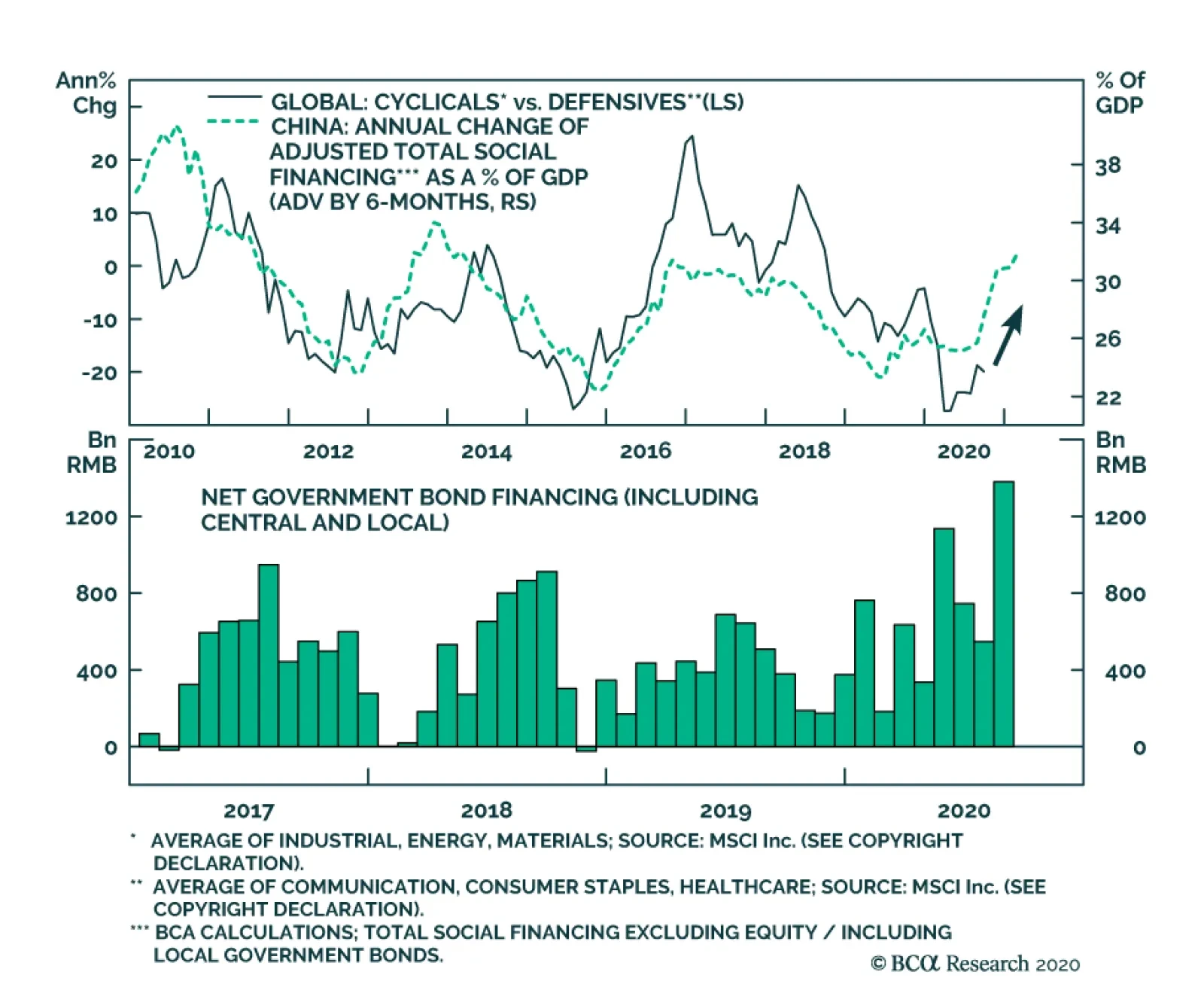

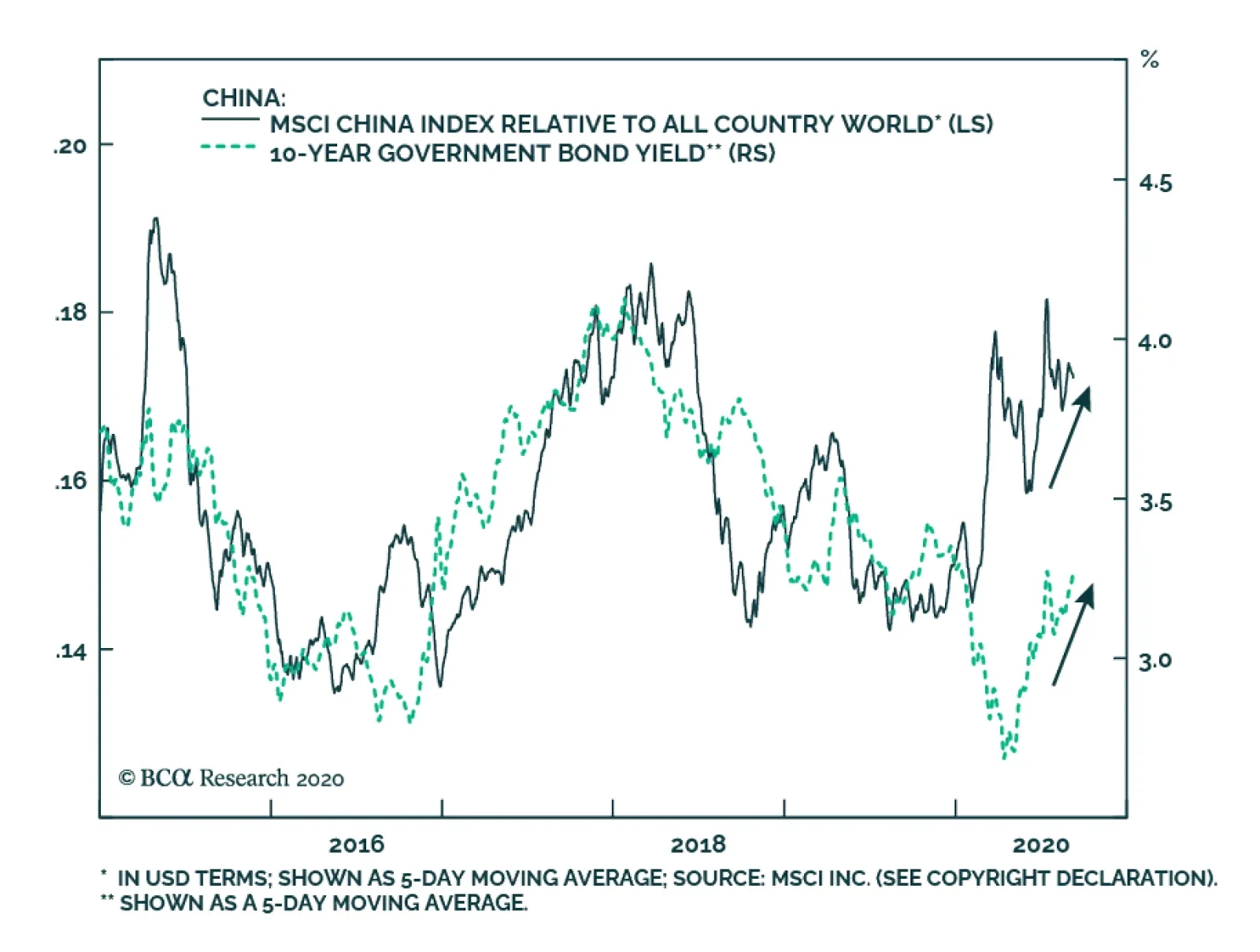

Despite a minor drop in the construction PMI sub-index due to heavy rains and floods in China’s central provinces, the acceleration in service activities pushed the non-manufacturing PMI to its highest level since early 2018 (Chart 4). China’s domestic COVID-19 infection rate remains low, giving rise to a rebound in service sector’s activities, such as tourism, catering, sports and entertainment. The resumption rate of theater operations reached 88% by the end of August. While the year-over-year growth rate in total retail sales of consumer goods remains negative, household purchases from larger enterprises registered a 2.2% increase in July (Chart 4, bottom panel). The normalization of activities in the service sector, coupled with the upcoming holiday season in September/October, will further support China’s household consumption recovery. China’s central bank and housing authorities have reportedly rolled out new rules to curb borrowing among overly indebted property developers. We do not expect the new directions to have a significant impact on our near-term outlook for real estate activities. Bank loans account for less than 15% of Chinese property developers’ funds, compared with down payments at 35%. Therefore, strong housing demand should more than offset any potential pullback in bank lending to property developers (Chart 5). Despite some pullbacks in the prices of Chinese stocks of late, we do not think that the cyclical upturn in Chinese stocks has run its course. Even though the PBoC seems to have normalized its post-COVID 19 monetary policy, monetary conditions remain very accommodative and fiscal stimulus will accelerate the pace of credit expansion through Q3.3 Continued money creation should prop up both China’s economic recovery and stock outperformance, in absolute terms and relative to global benchmarks. In addition, 10-year government bond yields rose 15bps in the past month and are now 66bps above their April low. The mounting bond yields on the back of an improved economic outlook, coupled with the continued outperformance in Chinese cyclical stocks over defensives, also support our constructive view on Chinese stocks on a 6-to-12 month basis (Chart 6). Chart 5Demand Should Continue Driving Property Sector Growth

Demand Should Continue Driving Property Sector Growth

Demand Should Continue Driving Property Sector Growth

Chart 6Fundamentals Are Supportive Of A Positive Cyclical View On Chinese Stocks

Fundamentals Are Supportive Of A Positive Cyclical View On Chinese Stocks

Fundamentals Are Supportive Of A Positive Cyclical View On Chinese Stocks

Chinese tech company stocks suffered losses last week due to selloffs in the global equity market led by US tech stocks. Technology is at the root of the ongoing US-China struggle, which we discussed in our weekly report on Aug 12.4 Given that the MSCI China index is heavily weighted towards some of China’s tech giants (e.g.: Alibaba, Tencent and Baidu), Chinese investable stocks are more vulnerable to both gyrations in the US tech sector and the escalating tech war between the US and China. As such, we continue to recommend that investors overweight investable stocks that are exposed to China’s “old economy” sectors. An acceleration in China’s demand-side recovery and a normalization of service activities will bode well for the performance of cyclical sectors, such as industrials and materials (Chart 7). In addition, we continue to overweight Chinese onshore semiconductor stocks relative to their global peers. Despite some volatility in recent weeks, we believe the structural upcycle in the Chinese onshore semi sector will continue, driven by Chinese policymakers’ ramped-up policy initiatives to support the nation’s domestic semiconductor research and production (Chart 8). Some of the fiscal and monetary incentives such as multi-year tax exemptions and cheaper bank credits will boost the sector’s longer-term growth prospects, whereas policies like government funding support and prioritized initial public offerings will push up the sector’s near-term multiple expansion. Chart 7Stick To "Old Economy" Chinese Stocks For The Time Being

Stick To "Old Economy" Chinese Stocks For The Time Being

Stick To "Old Economy" Chinese Stocks For The Time Being

Chart 8Chinese Semis On A Policy-Driven Structural Upturn

Chinese Semis On A Policy-Driven Structural Upturn

Chinese Semis On A Policy-Driven Structural Upturn

Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Footnotes 1, 4Please see China Investment Strategy Weekly Report "Sticking With Chinese “Old Economy” Stocks In A Widening Tech War," dated August 12, 2020, available at cis.bcaresearch.com 2, 3Please see China Investment Strategy Weekly Report "China Macro And Market Review," dated August 5, 2020, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

China’s NBS PMI painted a picture of a bifurcated economy in August. While the Composite PMI rose to 54.5 from 54.1, the Manufacturing index softened slightly to 51 from 51.1. Nonetheless, the Non-Manufacturing gauge rose to 55.2 from 54.2. Meanwhile, the…

Highlights US-China relations in 2020 consist of a gentleman’s agreement to keep the Phase One trade deal in place and aggressive maneuvering in every other policy area. Stimulus is unlikely to be curtailed in the US or China yet, which means brinkmanship will eventually lead to a negative surprise for markets. But it is just as unlikely to come after the election as before. Joe Biden would only initially benefit Chinese equities – trade and tech conflict is a secular trend. North Korea is not a red herring, but South Korea is still a geopolitical investment opportunity more than a risk, especially relative to Taiwan. Feature Chart 1US Power Struggle Raises Risk To Rally

US Power Struggle Raises Risk To Rally

US Power Struggle Raises Risk To Rally

The “everything is awesome” rally continues, with US tech stocks unfazed by rising domestic and international risks. However, according to The Lego Movie 2, everything is not that awesome. The Treasury market smells trouble and long-dated yields remain subdued, despite a substantial new dose of monetary policy dovishness (Chart 1, top panel). In the near term we agree with the bears and remain tactically long 10-year Treasuries. Global policy uncertainty remains extremely elevated despite dropping off a bit from the heights of the pandemic lockdowns. US uncertainty, which is now rising relative to global, will climb through November and possibly all the way through Inauguration Day on January 20 (Chart 1, bottom panels). A contested election is not a low-probability event now that President Trump is making a comeback in the election race. President Trump’s comeback could generate a counter-trend bounce in the US dollar (Chart 2A). His comeback is not based in online betting odds but in battleground opinion polls (Chart 2B). Former Vice President Joe Biden is currently polling the same against Trump as Hillary Clinton did in 2016. Chart 2ATrump Staging A Comeback, But US Consumers Flagging

Trump Staging A Comeback, But US Consumers Flagging

Trump Staging A Comeback, But US Consumers Flagging

Chart 2BTrump Staging A Comeback, But US Consumers Flagging

The Trump-Xi Gentleman’s Agreement - GeoRisk Update

The Trump-Xi Gentleman’s Agreement - GeoRisk Update

Why should Trump be less negative for the greenback than Biden? First, Trump is a protectionist who would turn to aggressive foreign and trade policy when it became clear that most of his other legislative priorities would not make it past the Democratic House of Representatives. Unilateral, sweeping tariffs against China, and possibly the EU and various other nations, would weigh on global trade and economic recovery and hence support the dollar. Second, Trump’s populism means he would pursue growth at all costs, which means that US growth would increase relative to that of the rest of the world. Democrats, by contrast, would raise taxes and regulations that would have to be offset by new spending, weighing on growth at least at first. Thus Trump would inject animal spirits into the US economy while dampening those spirits abroad; Biden would do the opposite. The dollar may not rally sustainably, but it would be flat or fall less rapidly than if Biden and the Democrats reduced trade risks abroad while deterring domestic private investment. It is not yet clear that Trump’s comeback will have legs. The nation is still in thrall to the pandemic, recession, and social unrest, which undermine a sitting president. US consumer confidence has fallen, as anticipated (Chart 2, bottom panel). Trump should still be seen as an underdog despite his incumbent status. A Trump comeback could precipitate a counter-trend bounce in the US dollar. Nevertheless, our quantitative election model gives Trump a 45% chance of victory, up from 42% last month. Florida has shifted back into the Republican column – albeit as a “toss up” state with a roughly even chance of going either way (Chart 3). The shift reflects improvement in state leading economic indexes as a result of the V-shaped recovery in the economy thus far. Chart 3Trump Nearly Regains Florida In Our Quantitative Election Model, Odds Of Victory 45%

The Trump-Xi Gentleman’s Agreement - GeoRisk Update

The Trump-Xi Gentleman’s Agreement - GeoRisk Update

Assuming Trump signs a new relief bill in September, which is working its way through Congress as we speak, we will upgrade our subjective odds from 35% to something closer to our quantitative model (and the market consensus). While Trump is less negative for the dollar than Biden, the dollar may fall anyway, at least beyond any near-term bounce. First, monetary policy is ultra-dovish. As we go to press, Fed Chairman Jerome Powell has given a sneak preview of the Fed’s strategic review of monetary policy at the Kansas City Fed’s annual Jackson Hole summit (this time hosted in cyberspace instead of Wyoming). Powell met expectations that the Fed will adopt average inflation targeting. Inflation will be allowed to overshoot the 2% inflation target to compensate for periods of undershooting. Maximum employment will be the goal rather than an attempt to prevent excessive deviation from the Fed’s estimates of neutral unemployment. This means US growth and inflation will push real rates lower and weaken the dollar. Moreover, as mentioned, Trump’s big spending would eventually drive investors away from the dollar, especially in the context of global economic recovery. Trump, like Biden, would refuse to impose fiscal austerity amid high unemployment. The one area where he would be able to compromise with House Democrats would be spending bills, as in his first term. The US budget deficit and trade deficit would remain very large, showering the world with dollar liquidity. Risk-on currencies will attract buyers in a new global business cycle. Republicans and Democrats have released their policy platforms following their national conventions. We will revisit these platforms in detail in a future report. The Democratic platform is the one that matters most because the Democrats are more likely to win full control of Congress and thus be capable of enacting their preferred policies. Their platform is reflationary, but in seeking to rebalance the economy to reduce financial and social disparities through more progressive tax policy it would offset some of the fiscal spending. Biden would also moderate foreign policy and trade policy, launching a new dialogue with China to manage tensions. The dollar would fall faster in this environment. Bottom Line: President Trump is staging a comeback in the election campaign. If the comeback receives a boost from fiscal stimulus, Trump could pull off a Harry Truman-style surprise victory. This would precipitate a bounce in the US dollar in the near term. Over the medium term, the dollar should continue falling due to US debt monetization and global recovery. The Trump-Xi Gentleman’s Agreement Has Two Months Left Financial markets have largely ignored US-China strategic tensions this year because the two countries are puffing themselves up with monetary and fiscal stimulus. Going forward, either the stimulus will falter, or the US-China conflict will escalate to the point of triggering a negative surprise for markets. Chart 4US-China: Embracing While Struggling

US-China: Embracing While Struggling

US-China: Embracing While Struggling

China is unlikely to pull back on stimulus measures. It cannot do so when unemployment has spiked and the economy is experiencing the weakest growth in over 40 years. Authorities said as much during the annual July Politburo meeting on the economy (a meeting that has often marked turning points in policy), when they pledged to maintain accommodative policy and to speed up local government issuance of special bonds. Money supply is growing briskly. The market is validating the signal from China’s easy monetary policies and robust credit expansion. Our China Play Index – which consists of the Australian dollar, iron ore prices, Brazilian equities, and Swedish equities – continues to rally smartly, breaking above its 2019 peaks (Chart 4, top panel). The risk to this view is that the People’s Bank of China may not provide additional monetary easing in the near term, as the Politburo signaled that monetary policy would be more flexible and targeted in the second half of the year. The three-month Shanghai interbank rate has been rising since April. Politically, Chinese authorities would benefit from releasing negative news or statements that would undermine President Trump’s reelection campaign. However, Beijing would not make consequential moves merely to spite Trump. Its primary interest lies in its own stability. Credit growth will continue growing at its current clip through most of the rest of the year and fiscal spending will expand, particularly to support infrastructure projects. The US Congress is also likely to add more stimulus before the election, as noted above. Thus with both countries stimulating, the risk is that they escalate their strategic confrontation to the point that it causes a negative surprise in financial markets. Will this occur? The US-China relationship in 2020 has been characterized by (1) a gentleman’s agreement to adhere to the Phase One trade deal, which was reaffirmed by top negotiators this week; (2) an aggressive pursuit of national interest in every other policy area. Beijing accelerated its power grab in Hong Kong; the US accelerated up its ban on Chinese tech. Chinese imports of US commodities are naturally much weaker than projected due to economic reality but neither side has an interest in exiting the deal. The renminbi continues to appreciate against the dollar on the back of Chinese and global recovery (Chart 4, second and third panels). Nevertheless a new burst of stimulus will lower the hurdle to President Trump taking additional punitive measures against China. The administration could have paused after its major decision to finalize its ban on business with Huawei and other tech firms, which ostensibly even extends to foreign firms that use US-designed parts in sales to China. It did not. Trump is maintaining the pressure with new sanctions over China’s militarization of the South China Sea. Washington is also likely to kick Chinese companies off US stock exchanges if they fail to meet transparency and accounting standards. Trump is not only burnishing his “tough on China” credentials against Democratic candidate Joe Biden – the US’s recent measures are unlikely to be repealed under either president in the coming years. Chart 5China Faces Internal And External Political Pressures

China Faces Internal And External Political Pressures

China Faces Internal And External Political Pressures

Therefore stimulus will enable US actions and Chinese reactions that will eventually trigger a pullback in financial markets. Chinese tech equities are reflecting this headwind. Equities ex-tech are likely to outperform (Chart 5, top panel). A Biden victory does not prevent Trump from taking punitive measures against China on his way out of office, to solidify his legacy as the Man Who Confronted China, so Chinese tech will remain at risk. Biden would be more favorable for emerging market equities because his administration would speed the dollar’s decline. A change of government in the US would temporarily disrupt the US’s overall policy assault against China. Biden’s foreign and trade policies would be more predictable and orthodox than Trump’s. Over a twelve month period, after a shot across the bow to warn that he is not a lightweight, Biden would probably attempt a diplomatic reset with China – a new round of engagement and dialogue that would support the Chinese equity rally. Eventually this reset would fail, however, and Biden would all the while be working up a coalition of democracies to pressure China to change its behavior – not only on trade but also on unions, carbon emissions, and human rights. Externally focused Chinese companies will remain exposed to the harmful secular trend of US-China power struggle regardless of the US election outcome. Coming out of the secretive leaders’ conclave at the Beidaihe resort in August, it is clear once again that Chinese domestic politics is not conducive to smooth US-China relations. Chinese political risk remains underrated. Our GeoRisk indicator is gradually picking up on this trend, and so are other quantitative political risk indicators such as that provided by GeoQuant (Chart 5, second panel). President Xi Jinping has been dubbed the “Chairman of Everything” due to his tendency to promote a neo-Maoist personality cult and thus shift Chinese governance from consensus-rule to personal rule. He is once again reportedly considering taking on the title of “Chairman” of the Communist Party, a position that only Mao Zedong has held.1 More importantly he is re-energizing his domestic anti-corruption campaign, i.e. political purge, this time against law enforcement. Xi had already seized control of China’s domestic security forces but controlling the police is even more critical in a period of high unemployment, slow growth, and social unrest (Chart 5, third panel). Xi’s attempt to re-consolidate power ahead of the Communist Party centennial in 2021 and especially the twentieth national party congress in 2022 is already under way. China’s domestic and international political environment is a risk for the renminbi, which we noted is rallying forcefully on the global rebound. We will not join this rally until the US election is decided at minimum. With the US posing a long-term threat, Beijing is speeding up its attempts to diversify away from the US dollar, both in trade settlements and foreign exchange reserves. Reliance on the dollar leaves Chinese banks and companies vulnerable to US financial sanctions, which have harmed US rivals like Russia and Iran. Over the long run there is a lot of upside for the yuan given its very low level of global penetration (about 2% of both SWIFT transactions and global foreign exchange reserves) and yet China’s very high share of global trade (about 15%). Cross-border settlements in RMB are recovering gradually after the steep drop-off following 2016. Beijing is also allowing foreign investors greater access to onshore financial markets where they will hold more and more RMB-denominated assets. However, the yuan will not become a reserve currency anytime soon given China’s state-controlled economy and closed capital account. We favor the euro, yen, and other G7 currencies as alternatives to the dollar. Hong Kong equities have suffered from the combination of Xi Jinping’s centralization of power and the US-China strategic conflict. The above analysis suggests that while they may get a temporary reprieve, the secular outlook is uninspiring. However, the Hong Kong monetary authorities are capable of managing the dollar peg. They have been able to manage dollar strength over the past decade, including the COVID-19 dollar run-up, and foreign exchange reserves are more than ample. By contrast, a sharp drop in the dollar can be handled even more easily by printing additional HKD. Eventually shifting to a trade basket, or a renminbi peg, is to be expected. The US election may support the Chinese equity rally if Biden wins, but tech equities should continue to underperform the rest of the bourse due to US grand strategy. Bottom Line: We prefer to play China’s growth recovery via outside countries that export into China, such as Sweden, Australia, and Brazil. The US election may support the Chinese equity rally if Biden wins, but tech equities should continue to underperform the rest of the bourse due to US grand strategy which will remain focused on constraining China’s tech ambitions. North Korea Is Not A Red Herring – But Taiwan Is Entirely Underrated The Taiwan Strait remains the chief geopolitical risk. Xi Jinping’s reassertion of Beijing’s supremacy within China’s sphere of influence has led to a backlash in Taiwanese politics and a confrontational posture across the Strait that is being expressed in saber-rattling and low-level economic sanctions that could easily escalate. Chart 6Taiwan Remains #1 Geopolitical Risk

Taiwan Remains #1 Geopolitical Risk

Taiwan Remains #1 Geopolitical Risk

Military exercises and jingoistic rhetoric are also heating up, not only directly relating to Taiwan but also in the neighboring South China Sea, which is critical to national security for all geopolitical actors in Northeast Asia. On August 26 Beijing testing two anti-ship ballistic missiles known as “aircraft carrier killers” in the South China Sea (the DF-21D and the DF-26B). We have long argued that the lack of clarity over whether the US would uphold its defense obligations to Taiwan makes the situation ripe for misunderstandings. The US Naval Institute has recently confirmed the validity of fears about a full-scale conflict in the near term.2 Neither Beijing nor Taipei nor Washington has crossed a red line. But China’s imposition of legislative dependency on Hong Kong highlights the incompatibility of the Communist Party’s governing model with western liberalism. The “one country, two systems” formulation has become unacceptable to the Taiwanese people, who want to preserve their autonomy indefinitely. The US ban on doing business with Huawei extends to foreign companies that use US parts or designs, squeezing Taiwanese companies (Chart 6, top panel). War is possible, but our base case still holds that the mainland will first use economic means. In particular it will impose economic sanctions, either precipitating or in response to a Fourth Taiwan Strait Crisis. The market continues to underrate the enormous risk to the Taiwanese dollar, as captured by the low level of our risk indicators (Chart 6, second panel). We continue to recommend shorting Taiwan relative to emerging markets. Taiwan is a short relative to South Korea, in particular, which stands to benefit from any negative turn of events in cross-strait relations. Korean equities are finally perking up, though the US tech war with China is weighing on the South Korean tech sector (Chart 7, top panel). We see this as a geopolitical opportunity given that both China and the US will need South Korean companies as they divorce each other. Korean political risk, however, may also be shifting from adequately priced to underrated. The risk premium has trended upward since President Trump’s diplomatic overture to leader Kim Jong Un stopped making progress (Chart 7, second and third panels). We have largely dismissed concerns about North Korea since the reduction of tensions in late 2017 due to our assessment that diplomacy would remain on track throughout Trump’s first term. This has proved to be the case, but it is still possible that North Korea could prove globally relevant before the US election. Chart 7North Korea A Non-Negligible Risk

North Korea A Non-Negligible Risk

North Korea A Non-Negligible Risk

The reason stems from rumors of Kim Jong Un’s health problems earlier this year. We noted at the time that it was suspicious that preparations for Kim’s sister, Kim Yo Jong, to take on greater responsibilities within the Politburo of the Worker’s Party seemed to predate reports of Kim Jong Un’s illness. For the North Korean state to continue to promote her implies that something may indeed be amiss. In fact, she has missed two Politburo meetings after her aggressive public relations campaign against South Korea was called off this summer. It is possible she got too much attention as the Number Two person in the regime. The South Korean National Intelligence Service is debating her status with the Defense Ministry and Unification Ministry. What is clear is that Kim Jong Un is preparing a new five-year economic plan, to be launched in January 2021, and that he is eager to share any blame for disastrous internal conditions in the country amid the global pandemic and recession. The market is typically correct not to hyperventilate over North Korean risks, but after 2016 North Korea is no longer a “red herring.” First, any domestic power struggle would occur at an immensely inconvenient time given the breakdown in US-China trust. Second, as the North manages any internal problems through its opaque and untested political process, it could be pressed into making a show of force that would either embarrass and antagonize President Trump, or provoke a forceful response from a future President Biden, given that North Korea in theory has the raw capability to deliver a crude nuclear weapon to the continental United States. If any US president makes a show of force, it will antagonize China and could lead to a major standoff. This would upset the markets at least temporarily. We are long Korean equities and would also look favorably on Korean tech. A geopolitical risk premium could temporarily undercut these stocks if North Korean diplomacy fails around the US election. But the risk is globally relevant only if Pyongyang somehow sparks a standoff between the US and China. Otherwise a major Korean peninsula crisis is far less of a concern than that of a crisis in the Taiwan Strait. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1Financial Times. 2 See Admiral James A. Winnefeld and Michael J. Morell, "The War That Never Was?" US Naval Institute Proceedings 146: 8 (August 2020), usni.org. Section II: GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Section III: Geopolitical Calendar

Highlights Historically, soft-budget constraints have typically been followed by periods of poor equity market performance. Soft-budget constraints could produce two distinct economic scenarios: malinvestment or inflation. Both are negative for equity investors. Odds are that the US will continue to pursue easy money policies, sowing the seeds of US equity underperformance in the years ahead. In contrast to the US, EM (ex-China, Korea and Taiwan) are presently facing hard-budget constraints, which will weigh on their growth in the near term. However, forced restructuring could boost efficiency and productivity leading to their equity and currency outperformance in the coming years. Unlike other developing economies, China is not currently facing hard-budget constraints. However, the structural overhang from the past 10 years of soft-budget constraints is lingering on and in some cases is increasing. The Thesis The consensus in the investment industry is that cheap money and ample stimulus are good for share prices. We do not disagree with this thesis when it is applied to the near and medium-term equity strategy. However, excessive stimulus and easy money policies — we refer to these as soft-budget constraints — bode ill for share prices in the long run. The investment relevance of this thesis is as follows. Since March, the US has implemented the largest fiscal and central bank stimulus in the world and will likely continue doing so in the coming years (Chart I-1). Such soft-budget constraints will likely support the US economy for now. Nevertheless, they will also sow seeds of future US equity underperformance and currency depreciation. Conversely, many emerging economies (excluding China) have failed to provide sufficient fiscal and credit support to their economies (Chart I-2). The resulting hard-budget constraints will foreshadow their economic underperformance vis-à-vis the US in the coming months. Chart I-1Soft-Budget Policies Will Likely Become Structural In The US

Soft-Budget Policies Will Likely Become Structural In The US

Soft-Budget Policies Will Likely Become Structural In The US

Chart I-2EM Ex-China, Korea And Taiwan Are Facing Hard-Budget Constraints

EM Ex-China, Korea And Taiwan Are Facing Hard-Budget Constraints

EM Ex-China, Korea And Taiwan Are Facing Hard-Budget Constraints

That said, hard-budget constraints will force companies in these EM economies into deleveraging, restructuring and improving efficiency. Ultimately, such hard-budget constraints will benefit EM shareholders in the long run. This thesis has been a key rationale behind our decision to close the short EM / long S&P 500 strategy on July 30, and to turn negative on the US dollar on July 9. In the months ahead, we will be looking for an opportunity to upgrade EM equities to overweight versus the S&P500. BOX 1 Gauging Budget Constraints In our opinion, the best way to gauge budget constraints for the real economy is by monitoring changes in the money supply. This is due to the following reasons: First, net changes in the money supply account for all net loan origination. Second, the money supply also reflects the monetization of public and private debt by the central bank and commercial banks. When a central bank and commercial banks acquire a security from or lend to a non-bank entity, they create new money “out of thin air”. No one needs to save for the central bank and commercial banks to lend to or purchase a security from a non-bank. In short, savings versus spending decisions by economic agents (non-banks) do not change the stock of money supply. We have deliberated on these topics at length in past reports. Securities transactions among non-banks do not create new or destroy existing deposits, i.e., they have no impact on the money supply. Rather, these constitute an exchange of securities and existing deposits between sellers and buyers. Provided these types of transactions do not expand the money supply, they do not, according to our framework, alter budget constraints. Finally, the broad money supply, not central bank assets, is the ultimate liquidity available to economic agents to purchase goods and services as well as invest in both real and financial assets. Commercial banks’ excess reserves at the central bank – a large item on the central bank balance sheet - do not constitute a part of the broad money supply. Empirical Evidence The following are examples of soft-budget constraints that were followed by periods of weakening productivity growth, diminishing return on capital and poor equity market performance: 1. China’s soft budget constraints in 2009-10 Due to the post-Lehman crisis stimulus, the change in broad money exploded above 40% of GDP (Chart I-3, top panel). The economy boomed from early 2009 until early 2011 as cheap and abundant money super-charged investment and consumption. Chart I-3China: Easy Money Presaged Falling Return On Assets And Equity Underperformance

China: Easy Money Presaged Falling Return On Assets And Equity Underperformance

China: Easy Money Presaged Falling Return On Assets And Equity Underperformance

However, Chinese share prices — the MSCI China Investable equity index excluding technology, media and telecom (TMT) — peaked in H1 2011 in absolute terms (Chart I-3, second panel). Relative to the global equity index excluding TMT, the Chinese investable stocks index began underperforming in late 2010 (Chart I-3, third panel). The basis for this equity underperformance was falling return on assets for non-financial companies due to capital misallocation, breeding inefficiencies and diminishing productivity gains (Chart I-3, bottom two panels). In China, the excessive stimulus of 2009 and 2010 and ensuing recurring rounds of soft-budget constraints put a floor under the economy but have destroyed shareholder value. 2. Money overflow in EM ex-China in 2009-10. China’s boom in 2009-10 produced a bonanza for other emerging economies. Not only Chinese imports from developing economies boosted the latter’s balance of payments and income but also international investors rushed into EM equity and fixed income. EM companies and banks took advantage of easy financing and their international borrowing skyrocketed. Finally, EM policy makers stimulated and domestic bank credit boomed. This period of soft-budget constraints led to complacency, lower productivity, falling return on capital and/or inflation in the following years (Chart I-4). Their financial markets performance in the 10 years that followed the soft-budget constraints in 2009-10 has been dismal. The share price index of EM ex-China, Korea and Taiwan as well as the total return on their currencies (including the carry) versus the US dollar have been in a bear market (Chart I-4, bottom two panels). 3. The credit and equity bubbles in Japan, Korea and Taiwan of the late 1980s Money and credit bubbles proliferated in Japan, Korea and Taiwan in the late 1980s (Chart I-5, Chart I-6 and Chart I-7). Chart I-4EM Ex-China, Korea And Taiwan: Easy Money In 2009-10 Sowed Seeds Of Bear Market

EM Ex-China, Korea And Taiwan: Easy Money In 2009-10 Sowed Seeds Of Bear Market

EM Ex-China, Korea And Taiwan: Easy Money In 2009-10 Sowed Seeds Of Bear Market

Chart I-5Japan: Easy Money Produced Equity Bubble And Lower Productivity Growth

Japan: Easy Money Produced Equity Bubble And Lower Productivity Growth

Japan: Easy Money Produced Equity Bubble And Lower Productivity Growth

Chart I-6Korea: Easy Money Produced Equity Bubble And Lower Productivity Growth

Korea: Easy Money Produced Equity Bubble And Lower Productivity Growth

Korea: Easy Money Produced Equity Bubble And Lower Productivity Growth

Chart I-7Taiwan: Easy Money Produced Equity Bubble And Lower Productivity Growth

Taiwan: Easy Money Produced Equity Bubble And Lower Productivity Growth

Taiwan: Easy Money Produced Equity Bubble And Lower Productivity Growth

Their productivity growth rolled over in the late 1980s amid easy money policies. Share prices deflated in Japan, Korea and Taiwan in the 1990s (please refer to the middle and bottom panels of Charts I-5, I-6 and I-7). Chart I-8ASEAN In 1990s: Soft-Budget Constraints Heralded Productivity Demise

ASEAN In 1990s: Soft-Budget Constraints Heralded Productivity Demise

ASEAN In 1990s: Soft-Budget Constraints Heralded Productivity Demise

4. The boom-bust cycle in emerging Asia ex-China in the 1990s Soft-budget constraints prevailed in many emerging Asian economies in the first half of the 1990s. Foreign money inflows and domestic bank credit produced an economic boom. The consequences of such soft-budget constraints were debt-financed malinvestment, falling return on assets and massive current account deficits (Chart I-8). All of these culminated in epic currency and banking crises. 5. The credit bubbles in the US and Europe leading to the 2008 crash Lax credit standards propelled credit and property booms in the US and Southern Europe in the period of 2002-2007. Broad money ballooned in the euro area and swelled in the US (please refer to Chart I-1 on page 2). These property bubbles unraveled in 2007-08. These are well known, and we will not delve into the details. Soft-Budget Constraints Lead To Malinvestment Or Inflation Soft-budget constraints could produce two distinctive economic scenarios – malinvestment or inflation. Both are negative for equity investors. The malinvestment scenario occurs when easy money propels undisciplined capital spending. Easy and abundant money boosts medium-term growth and, thereby, creates the illusion of an economic miracle. The latter renders companies, creditors, investors and government officials complacent. Creditors lend a lot and do so based on optimistic assumptions while companies expand hastily and invest carelessly. The result is capital misallocation, i.e., companies pour money into projects that do not ultimately produce sufficient cash flow. Equity investors project high growth expectations into the future and bid up share prices. Government officials preside over an unsustainable growth trajectory overlooking lurking systemic risks and deteriorating economic fundamentals. Easy money and unlimited financing typically bode ill for efficiency and productivity— this is simply due to human nature. Companies neglect efficiency considerations and, as a result, productivity stagnates. Consequently, cost overruns and unprofitable investments suffocate corporate profits. Declining corporate earnings at a time of expanded capital base culminate in a collapse of return on capital. This is the crucial reason why share prices drop. As profits and return on capital decline, companies retrench by cutting costs and halting investment spending. Defaults mushroom, leading creditors to cut new financing. The inflation scenario transpires when easy money boosts consumption more than investment. Easy money and unlimited financing lift household income and consumption. This can arise from a large fiscal stimulus or private sector's borrowing and spending. On the one hand, robust household income growth inevitably leads to higher wage growth expectations. On the other hand, limited investment brings about productivity stagnation. Mounting wages and languishing productivity growth lead to rising unit labor costs and, ultimately, result in a corporate profit margin squeeze. Faced with corporate profit margin shrinkage, companies either raise prices, i.e., pass through higher costs, or retrench by shedding labor and shrinking capital spending even further. The latter produces a widespread economic downturn, and stifles business profits and share prices. A symptom of higher inflation is a wider current account deficit. With an economy’s productive capacity lagging behind demand, the gap between the two can be filled in by imports. In addition, escalating domestic costs make a country less competitive, which inhibits exports and bloats imports. When a central bank is unwilling to tighten monetary policy meaningfully amid high and rising inflation and/or a widening current account deficit, it falls behind the inflation curve. This constitutes a very bearish backdrop for the exchange rate. Currency depreciation erodes the country’s equity returns in common currency terms versus other bourses. Can an economy with soft-budget constraints, i.e., booming money growth, avoid both malinvestment and inflation? Yes, it can if it is able to boost productivity growth so that it avoids systemic capital misallocation (i.e., investments produce reasonable returns to pay off to creditors and shareholders) and escapes higher inflation by expanding output faster to meet growing demand. However, achieving higher productivity growth amid soft-budget constraints is easier said than done. Bottom Line: The scenario of malinvestment has been playing out in China since 2009. Capital misallocation also occurred in the US and parts of Europe during the 2002-2007 credit boom, and took place in Japan, Korea and Taiwan in the late 1980s. Malinvestment, with some elements of inflation, occurred in emerging Asian countries prior the 1997-98 crises as well as in many EM economies like India, Indonesia and Brazil in 2009-2012. Investment Implications It is fair to say that the unprecedented economic downturn in the US warranted an exceptionally large stimulus. The question for the next several months and years is whether US authorities will: overstay easy policies and make soft-budget constraints a permanent feature of the US economy, or tighten policy earlier than warranted, or navigate policy perfectly so that the economy is neither too hot nor too cold. Our sense is that US authorities will overstay their easy money policies. If the US continues to pursue macro policies in the form of soft-budget constraints, will the nation experience malinvestment or inflation? Our sense is that the US will likely experience asset bubbles and inflation. As the Federal Reserve stays behind the inflation curve in the coming years, the US dollar will be in a multi-year downtrend. Hence, the strategy should be selling the greenback into rebounds. We switched our short positions in select EM currencies— such as BRL, CLP, ZAR, TRY, KRW, IDR and PHP —away from the US dollar to an equal-weighted basket of the euro, CHF and JPY on July 9. For now, EM currencies will lag DM currencies. US equity outperformance versus the rest of the world is in the late innings (Chart I-9). The pillars of US equity underperformance in common currency terms will be excessive US equity valuations, a potential new era of US return on capital underperforming the rest of the world and greenback depreciation. Chart I-9US Equity Outperformance Is In Very Late Stages

US Equity Outperformance Is In Very Late Stages

US Equity Outperformance Is In Very Late Stages

The top panel of Chart I-10 illustrates that the difference between US investors owning international stocks and non-US investors holdings of US equities is at a record low. This reveals that both US and foreign investors currently "over-own" US stocks versus non-US equities. Perfect timing of a structural trend reversal is impossible, but we believe US equity outperformance will discontinue before year-end. That was the rationale behind terminating our short EM / long S&P 500 strategy and upgrading EM equity allocation from underweight to neutral. In contrast to the US, EM (ex-China, Korea and Taiwan) are presently facing hard-budget constraints which will weigh on their economic performance in the near term. This is why we are not rushing to upgrade EM stocks and currencies to overweight. However, the lack of cheap money will force these EM countries and their companies to do the right things: deleverage households and companies, clean up and recapitalize their banking systems and undertake corporate restructuring. Ultimately, hard-budget constraints will likely sow the seeds of high productivity and, with it, equity and currency outperformance in the years to come. China is a tricky case. On a positive note, it has not stimulated as much during the pandemic as it did in 2009. Besides, policymakers are now aware of the ills that come with soft-budget constraints and have been working hard to address these. Critically, the Chinese population, businesses and the authorities are all united in the nation’s confrontation with the US. Complacency in this context is not a major risk and the focus on efficiency and productivity will be razor sharp. On the negative side, the credit, money and property bubbles that had not been dealt with before the pandemic are now increasing with the stimulus. Continued malinvestment and falling return on capital in China’s old economy sectors is signified by the very poor performance of China’s cyclical “old economy” stocks (Chart I-11, top panel). In turn, bank share prices are making new cyclical lows underscoring their worsening structural outlook (Chart I-11, bottom panel). Chart I-10Global Equity Investors Over-Own US Stocks Versus International Ones

Global Equity Investors Over-Own US Stocks Versus International Ones

Global Equity Investors Over-Own US Stocks Versus International Ones

Chart I-11Chinese Equities: "Old Economy" Cyclicals And Banks Are Dismayed By Structural Malaises

Chinese Equities: "Old Economy" Cyclicals And Banks Are Dismayed By Structural Malaises

Chinese Equities: "Old Economy" Cyclicals And Banks Are Dismayed By Structural Malaises

Weighing the pros and cons, we infer that the cyclical recovery in China has further to run. This will support China’s growth and equity outperformance for now. That is why we continue to recommend overweighting China within an EM equity portfolio. However, as the credit and fiscal impulses fade starting in H1 next year, structural malaises will resurface posing risks to China’s equity outperformance. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations