China

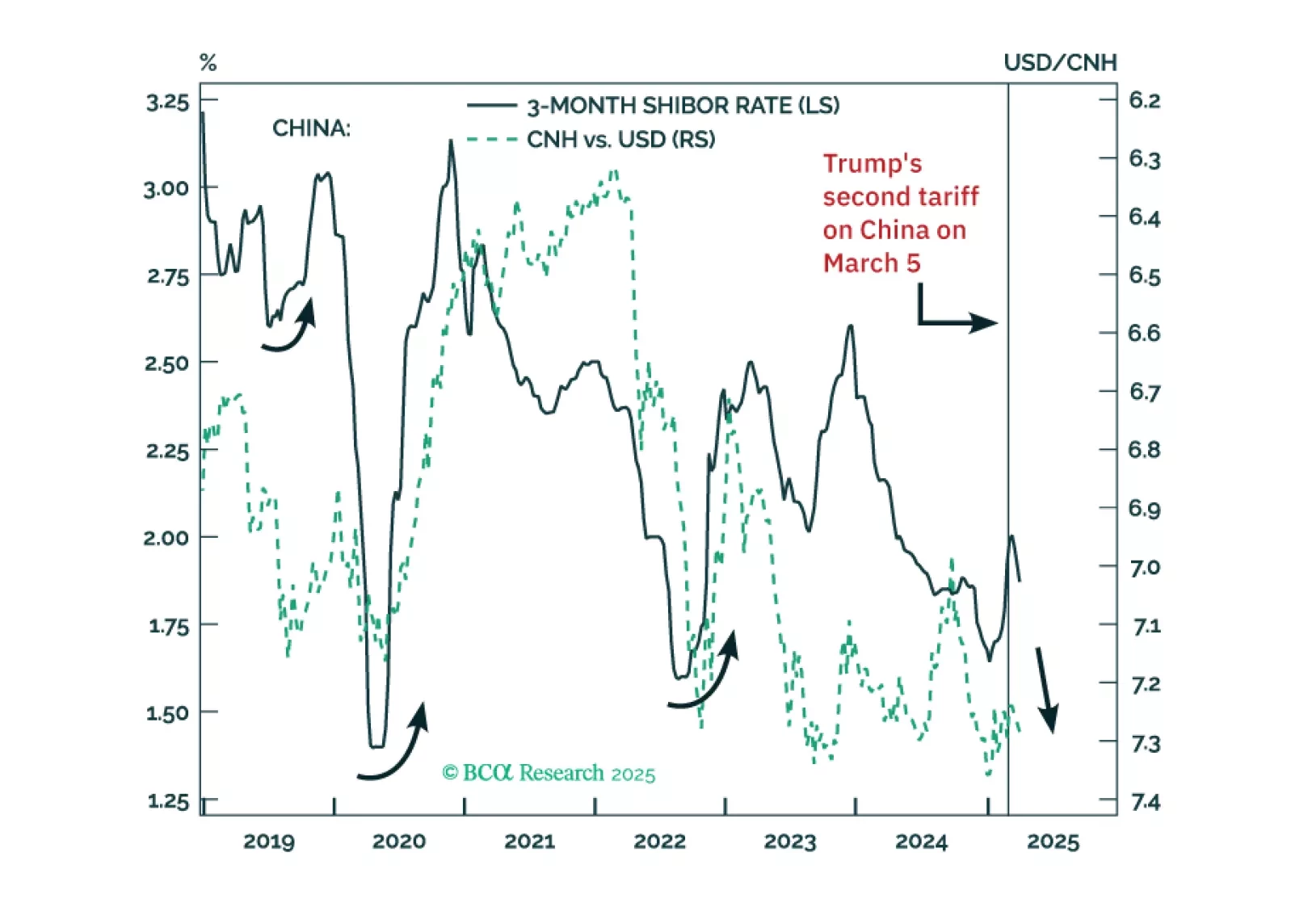

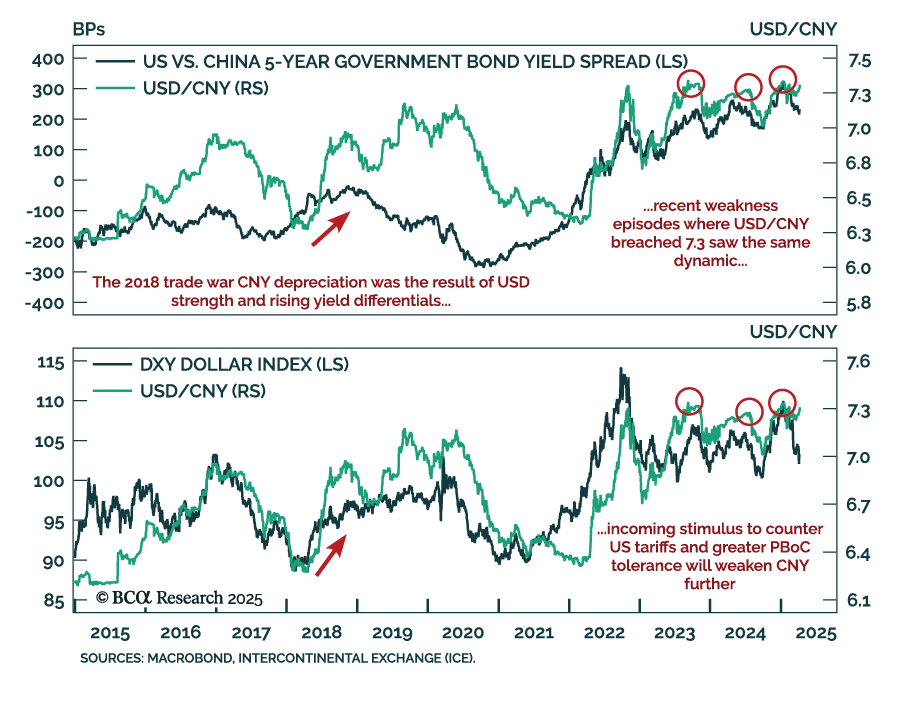

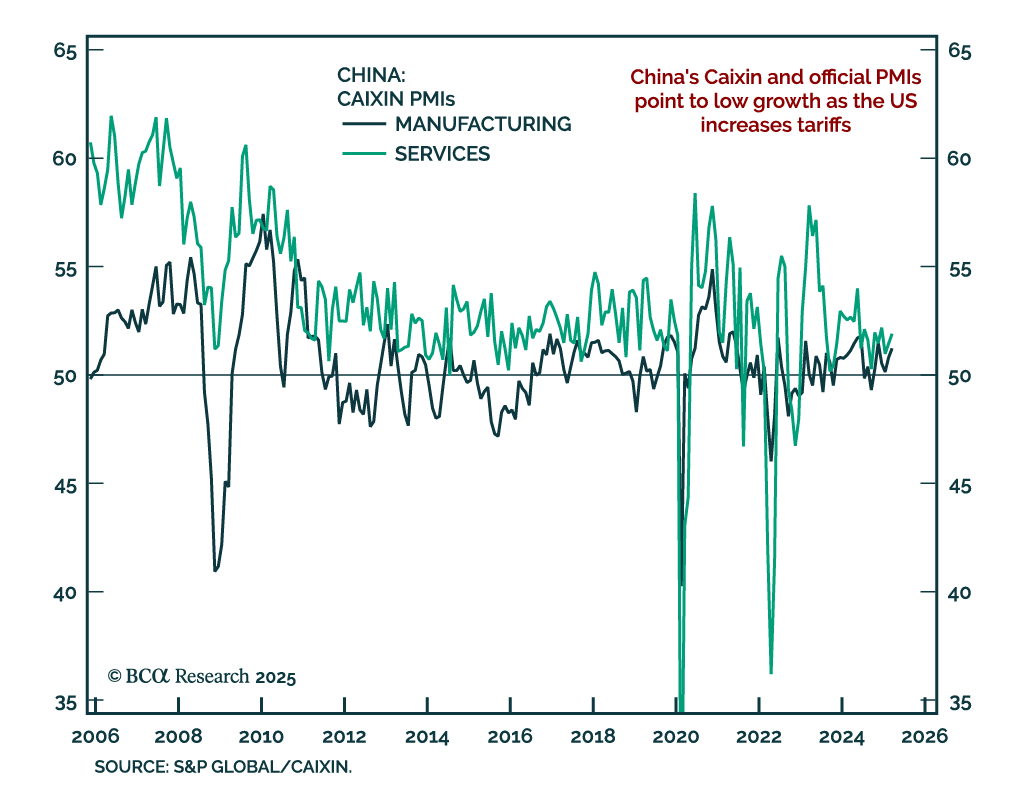

We believe Beijing views these US trade actions as nothing short of a declaration of economic war, not just a trade dispute. The US-China confrontation is set to escalate from here. Chinese authorities will allow the yuan to depreciate materially. Go short CNH against the US dollar. For EM and Asian equity portfolios, we are downgrading Chinese investable/offshore stocks from neutral to underweight.

President Trump imposed tariffs on the world in his first 100 days, as we expected. Tariffs may have catalyzed a recession in the US, given the weakness in consumer sentiment and demand. Trump will soon backpedal and grant exemptions to countries that are negotiating, which he will showcase as proofs of his successful trade policy. While he may backpedal on his tariffs on other countries, China is not likely to receive the same treatment due to the US-China strategic competition.

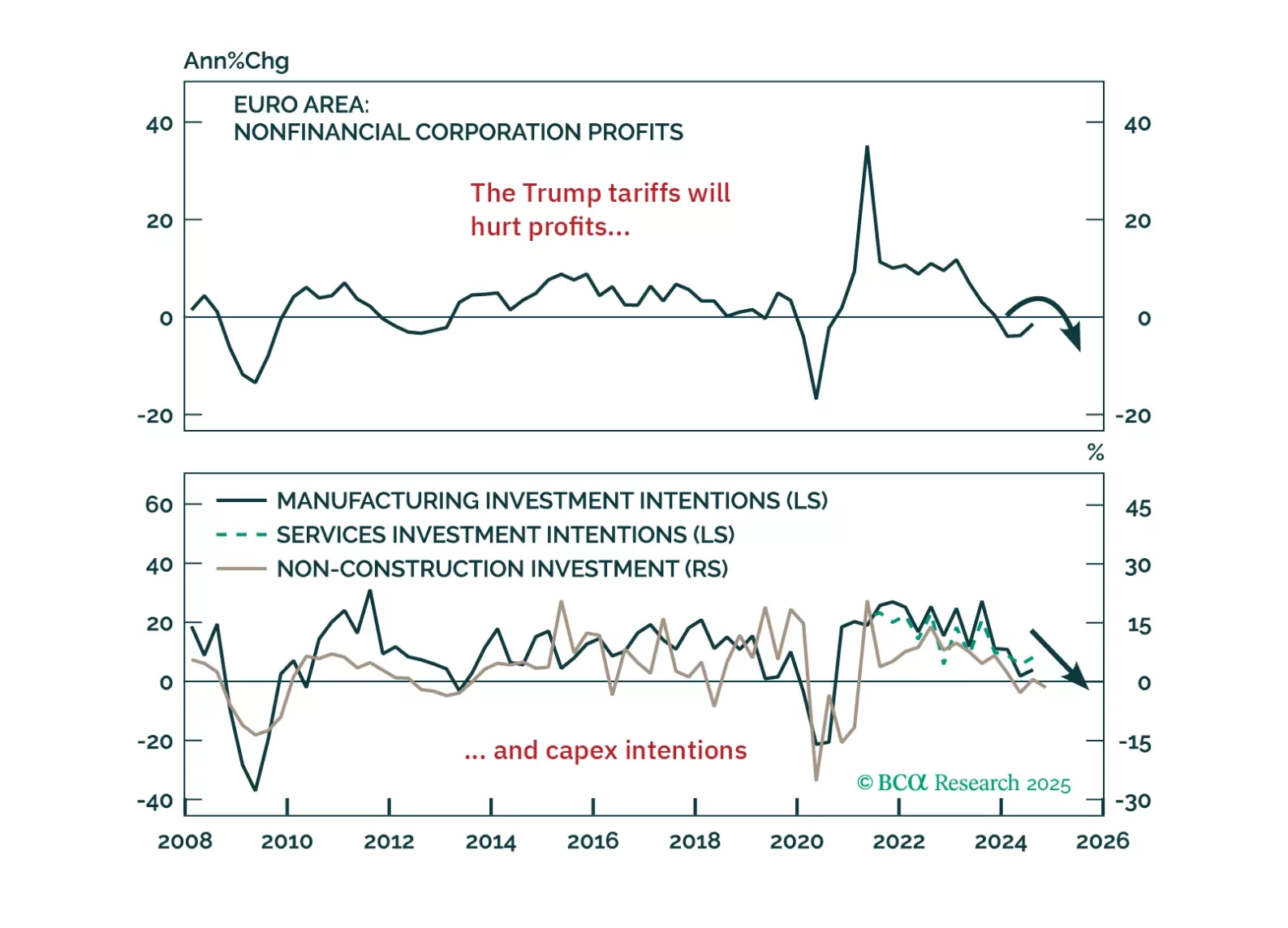

Trump’s tariff shock will push Europe into recession — but it’s also triggering a powerful integration response. In this report, we lay out the tactical case for staying defensive and the structural case for going long European assets when the dust settles.

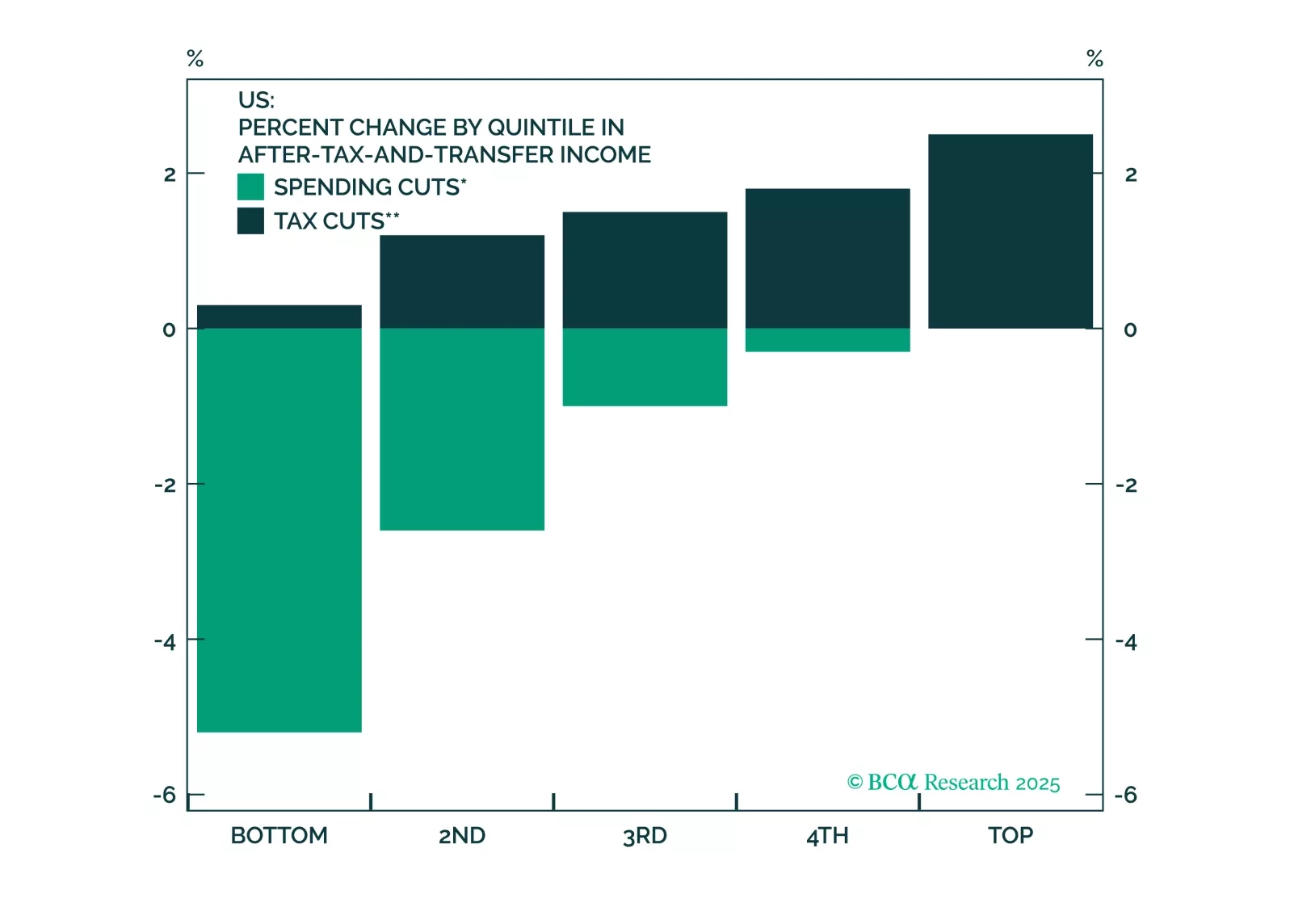

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

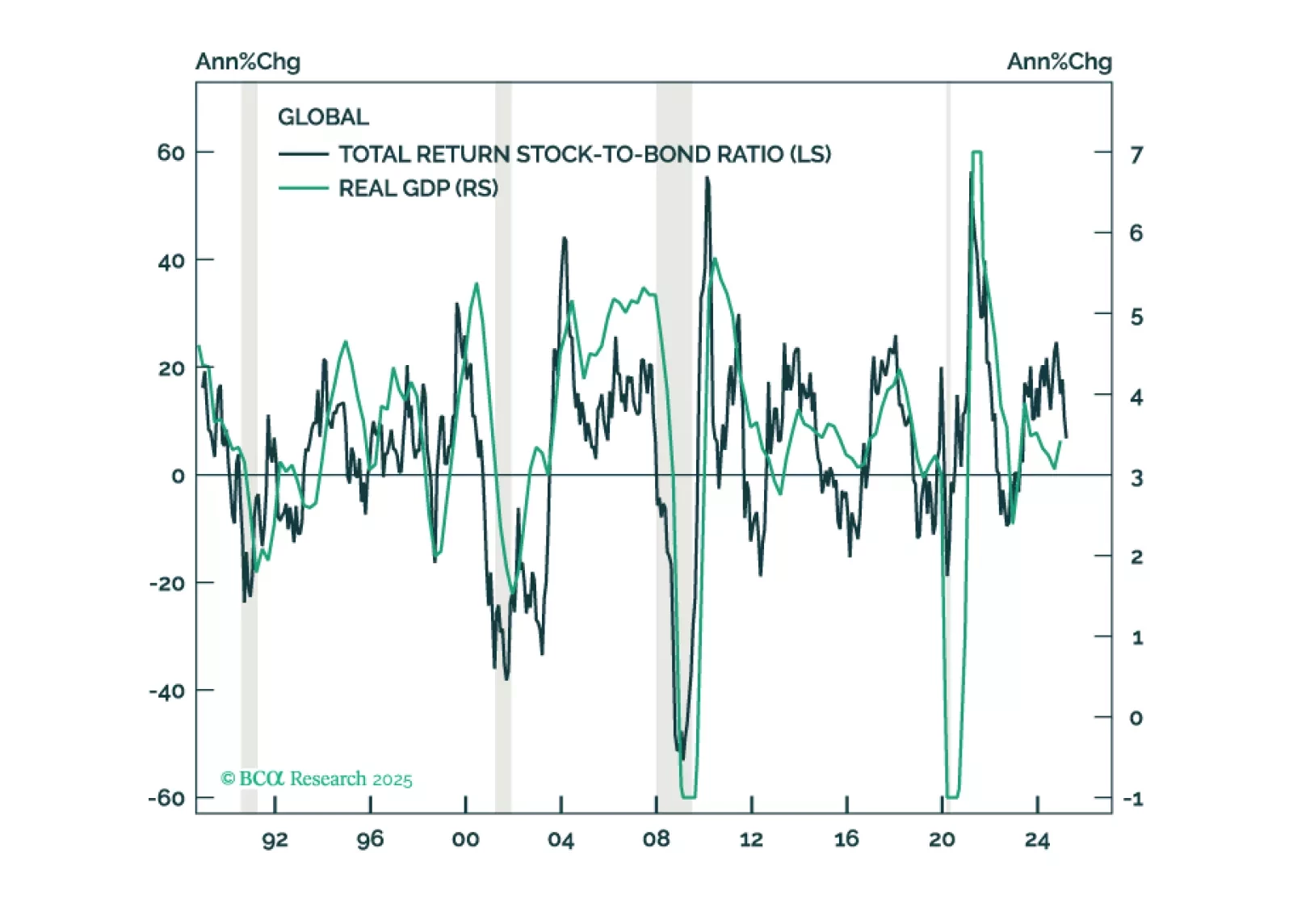

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

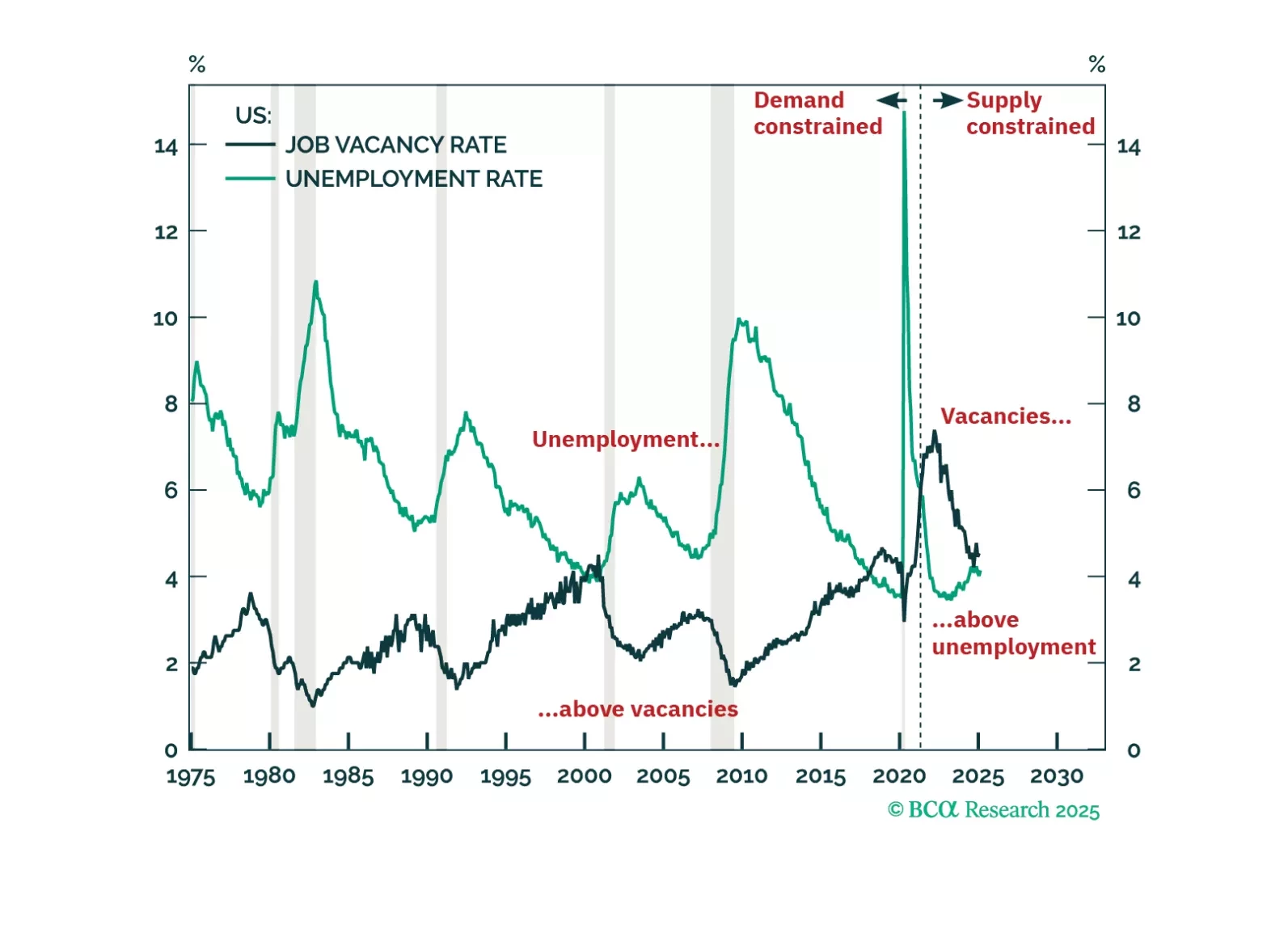

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.