China

Highlights The current pace in the recovery of China’s domestic demand has not been robust enough to fully offset the impact from the collapse in exports. The level of industrial inventory jumped to a five-year high, but it will likely be transitional. We expect the inventory overhang to subside when the recovery speed in demand catches up with supply in H2. While the gap is widening between stock prices and economic fundamentals in the US, Chinese equity prices have been more “well behaved” in the past month. We continue to overweight Chinese stocks in the next 6 to 12 months and favor Chinese onshore corporate bonds overall and SOEs in particular. Feature China’s Caixin and official PMIs in April highlighted the knock-on effects on the Chinese economy from a collapse in external demand. Although China’s domestic economy continued its rebound, the pace of the improvement has not been robust enough to offset rapidly weakening exports. This was evident in the widening gap between supply and demand in April. The sharp contraction in the global economy in Q1 will likely deepen in Q2 because the lockdowns in Europe and the US started in the later part of Q1 and have mostly remained in place through end-April. We expect global demand to significantly worsen in April and May, generating strong headwinds to China’s near-term recovery. Chinese authorities have been prompted to step up their stimulus efforts due to a fast deterioration in global growth. The government recently approved an additional 1-trillion yuan in local government special-purpose bond issuance, which is scheduled to be fully dispersed by the end of May. China’s stimulus, strongly focused on boosting investment and economic growth, should fuel Chinese stock and industrial metal prices in the next 6 to 12 months. Tables 1 and 2 below highlight key developments in China’s economic and financial market performance in the past month. Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

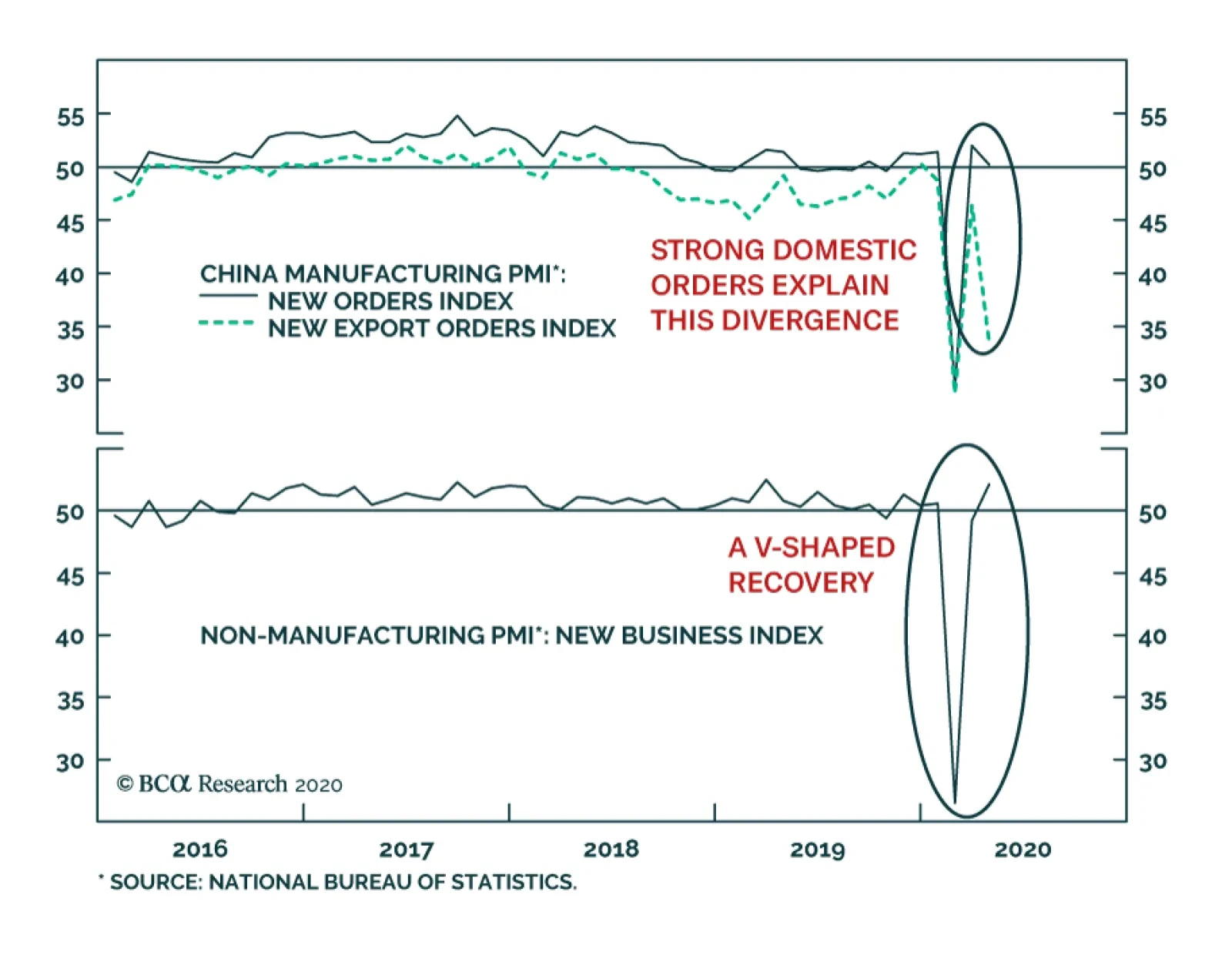

Chart 1Construction Sector Has Seen The Strongest Rebound

Construction Sector Has Seen The Strongest Rebound

Construction Sector Has Seen The Strongest Rebound

China’s domestic demand partially offset a collapse in exports in April. The official manufacturing PMI slipped to 50.8 in April from 52 in the previous month. The Caixin PMI survey, which is skewed towards smaller and more export-oriented firms, returned to contractionary territory in April following a brief rebound in March. The retreat in both PMI readings highlights how a worldwide lockdown of businesses has shaken China’s manufacturing sector (Chart 1, top panel). This exogenous negative impact will likely worsen in Q2. China's domestic economy continued its slow recovery through April. The official PMI’s new orders subcomponent declined by only 2 percentage points, despite a collapse of new export orders to 33.5. Moreover, the new orders subcomponent of the non-manufacturing PMI survey increased from 49.2 to 52.1, with the construction subcomponent reverting to its pre-pandemic level. The construction employment subcomponent also confirms that the industry has shown the strongest rebound among sectors in the Chinese economy (Chart 1, middle and bottom panels). Chart 2Home Sales Are Likely To Accelerate

Home Sales Are Likely To Accelerate

Home Sales Are Likely To Accelerate

China’s housing market also continued to improve in April. Chart 2 (top panel) shows that the demand for both residential housing and floor space started rebounding in March. The high frequency data indicate the year-over-year growth rate in home sales in China’s 30 large- and medium-sized cities turned positive in April (Chart 2, middle panel). The rapid expansion in home sales in the past weeks may be due to recent discount promotions, but we anticipate housing prices to remain stable this year in line with the Chinese leadership’s policy direction (“houses are for living, not for speculation”). We also expect that the number of home sales will accelerate. Local governments will significantly ramp up land sales this year to make up for their large revenue shortfalls. The central government will continue to gradually relax real estate purchase restrictions. The more property market-friendly policies, coupled with extremely accommodative monetary conditions, will encourage a healthy rally in property market investment and housing demand in H2 (Chart 2, bottom panel). So far most improvement in China’s domestic demand seems to be concentrated in the construction sector. The slow pace of manufacturers’ capacity utilization suggests that China’s industrial output growth is unlikely to return to its pre-pandemic rate in Q2. As of April 25, among the official PMI surveyed enterprises, the resumption rate of large- and medium-sized enterprises was 98.5%. However, only 77.3% of them reported that they were operating at 80% or higher of their usual capacity utilization rates.1 Chart 3Pressure On Inventory Should Start To Ease In H2

Pressure On Inventory Should Start To Ease In H2

Pressure On Inventory Should Start To Ease In H2

The imbalance in the recoveries of China’s supply and demand has led to a pileup in inventory, the highest level in five years (Chart 3). The combination of excessive inventory and low demand has weakened China’s factory pricing power and profit growth. However, in our view, the inventory overhang will be temporary, and the factory price contraction is unlikely to turn into a deep deflation such as the one in 2009 or the long-lasting deflationary cycle from 2012-2015. The level of industrial inventory has been much lower than it was during the four years leading to the 2008/2009 global financial crisis (GFC) and the 2015/2016 deep deflationary cycle. The deflation in factory prices also has been relatively mild compared with the two previous phases. Moreover, an extremely tight monetary policy and protracted inventory destocking period that contributed to the collapse in global raw material prices in 2012 are not present. Declines in China’s manufacturing, raw material and mining prices are synchronized, echoing the GFC when global demands nose-dived and pushed international oil and raw material prices into deep contractions. Our baseline scenario of an incremental re-opening of the global economy, a peak in the US dollar, and a recovery in the oil market in H2, all support our view that the deflation in China’s producer prices should not last beyond Q3. Given that exports’ share to China’s GDP is currently half of what it was in 2008, the weakness in global demand will be much less of a drag on China’s domestic manufacturing sector than during the GFC. Chart 4Logistics Bottleneck Still In Place

Logistics Bottleneck Still In Place

Logistics Bottleneck Still In Place

Additionally, the drawdown in April’s raw material inventory and an increase in the official PMI’s supplier delivery subcomponents suggest that some lingering logistical bottlenecks may be at play, preventing China’s domestic business operations from recuperating at full speed (Chart 4). We expect a further relaxation of intra- and inter-provincial travel restrictions following the National People’s Congress (NPC) on May 22 in Beijing. This easing should help to accelerate the normalization in both manufacturing activities and inventory levels. The outperformance of Chinese equity prices versus global stocks has eased significantly in the past month (Table 3 and Chart 5). The moderation suggests that investors may be starting to factor in a slower-than-expected economic recovery in China. Near-term risks are still high for further selloffs in both Chinese and global stocks. Nevertheless, we think the rapid advancement in global stock prices in the past month, particularly the SPX, means that Chinese stocks are not as overbought as in February and March. The widening gap between US equity prices and economic fundamentals makes the SPX more vulnerable to near-term uncertainties surrounding global economic recovery. We maintain our view that a combination of massive Chinese stimulus and the momentum in China’s economic recovery in H2 should support an outperformance in Chinese stocks in the next 6 to 12 months. Table 3Chinese Stocks Advanced Much Less Than SPX In April

China Macro And Market Review

China Macro And Market Review

Chart 5Chinese Stocks Less Overbought Now

Chinese Stocks Are Less Overbought Now

Chinese Stocks Are Less Overbought Now

The bull steepening in the government bond yield curve since March 23 flattened a bit in the last week of April, but it remains heightened with the short end of the yield curve falling much faster than the long end (Chart 6). This suggests that domestic investors expect China’s ultra-easy monetary policy to remain in place in the near term due to uncertainties surrounding the global pandemic and a slow economic upturn. At the same time, investors do not believe the weakness in the Chinese economy will persist long enough to warrant a sustained easy monetary policy regime. In addition, China’s 10-year government bond yield fell by 60bps so far this year, about half of the drop in the 10-year US Treasury bond yield (Chart 6, bottom panel). Even though we think the long end of the government bond yield curve has yet to bottom,2 the relatively stable return and RMB exchange rate make Chinese government bonds a safe bet for global investors seeking less risky assets. Chart 6Chinese 10-Year Government Bond Yield Has Not Capitulated

Chinese 10-Year Government Bond Yield Has Not Capitulated

Chinese 10-Year Government Bond Yield Has Not Capitulated

Chart 7Chinese Onshore Corporate Bonds Still Offer Solid Returns

Chinese Onshore Corporate Bonds Still Offer Solid Returns

Chinese Onshore Corporate Bonds Still Offer Solid Returns

Chart 7 highlights that the ChinaBond Corporate Bond total return index remains in a solid uptrend in both local currency and USD terms, despite the incredible strength in the USD since March. We continue to recommend onshore corporate bond positions in the coming 6-12 months.For domestic investors, we favor a diversified portfolio of SOE corporate bonds. Even though bond defaults will likely rise in the next 6-12 months, they will probably remain lower than what the market is currently pricing in. Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Footnotes 1NBS’s interpretation of China April PMI. http://www.stats.gov.cn/tjsj/sjjd/202004/t20200430_1742576.html 2Please see China Investment Strategy Weekly Report "Three Questions Following The Coronacrisis," dated April 23, 2020, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

In sharp contrast to the US, the Chinese PMIs were soft. When looking at overall manufacturing activity, there is little redeeming feature. However, the details of the survey reveal that the export sector is a drag on activity, not the domestic economy. …

Highlights Over the past 24 hours the White House has taken several steps indicating that President Trump is adopting the “war president” posture in the run-up to the US election. The intensity of the US-China rivalry can escalate dramatically. We maintain our defensive tactical positioning and are going long US 10-year treasuries. Feature The phrase “World War III” or #WWIII went viral earlier this year in response to a skirmish between the US and Iran (Chart 1). Only four months later, the US and China are escalating a strategic rivalry that makes the Iran conflict look paltry by comparison (Chart 2). Chart 1US-Iran Tensions Were Just A Warm-Up

#WWIII

#WWIII

Chart 2The Thucydides Trap

The Thucydides Trap

The Thucydides Trap

Fortunately, the two great powers are constrained by the same mutually assured destruction that constrained the US and the Soviet Union during the Cold War. They are also constrained by the desire to prevent their economies from collapsing further. Unfortunately, the intensity of their rivalry can escalate dramatically before reaching anything truly analogous to the Berlin Airlift or Cuban Missile Crisis – and these kinds of scenarios are not out of the question. Safe haven assets will catch a bid and the recovery in US and global risk assets since the COVID selloff will be halted. We maintain our defensive tactical positioning and will close two strategic trades to book profits and manage risk. In the wake of the pandemic and recession, geopolitics is the next shoe to drop. The War President Over the past 24 hours the White House has taken several steps indicating that President Trump is adopting the “war president” posture in the run-up to the US election: Export controls: Trump has gone forward with new export controls on “dual-purpose” technologies – those that have military as well as civilian applications, in a delayed reaction to China’s policy of civil-military technological fusion. The Commerce Department has wide leeway in whether to grant export licenses under the rule – but it is a consequential rule and would be disruptive if enforced strictly. Supply chain de-risking: Trump is also going forward with new restrictions on the import of foreign parts for US power plants and electricity grid. The purpose is to remove risks from critical US infrastructure. COVID investigation: Trump has hinted that the novel coronavirus that causes the COVID-19 disease may have originated in the Wuhan Institute of Virology. The Director of National Intelligence issued a statement indicating that the Intelligence Community does not view the virus as man-made (not a bio-weapon), but is investigating the potential that the virus transferred to humans at the institute. The State Department had flagged the institute for risky practices long before COVID. Trump avoided the bio-weapon conspiracy theory and is focused on the hypothesis that the laboratory’s investigations into rare coronaviruses led to the outbreak. New tariffs instead of reparations: Director of the National Economic Council Larry Kudlow denied that the US would stop making interest and principal payments on some Chinese holdings of US treasuries. He said that the “full faith and credit of the United States’ debt obligation is sacrosanct. Absolutely sacrosanct.” Trump denied that this form of reparations, first floated by Republican Senator Marsha Blackburn of Tennessee, was under consideration. Instead he suggested that new tariffs would be much more effective, raising the threat for the first time since the Phase One trade deal was agreed in principle in December. Strategic disputes: Tensions have flared up in specific, concrete ways across the range of US-Chinese relations – in the cyber-realm, psychological warfare, Korean peninsula, Taiwan Strait, and South China Sea. These could lead to sanctions. The war president posture is one in which President Trump recognizes that reelection is extremely unlikely in an environment of worse than -4.8% economic growth and likely 16% unemployment. Therefore he shifts the basis of his reelection to an ongoing crisis and appeals to Americans’ patriotism and desire for continuity amid crisis. Bottom Line: Protectionism is not guaranteed to work, and therefore it was not ultimately the path Trump took last year when he still believed a short-term trade deal could boost the economy. Now the bar to protectionism has been lowered. The Decline Of US-China Relations President Trump may still be bluffing, China may take a conciliatory posture, and a massive cold war-style escalation may be avoided. However, it is imprudent to buy risk assets on these reasons today, when the S&P 500’s forward price-to-earnings ratio stands at 20.15. It is more prudent to prepare for a historic escalation of tensions first, buy insurance, then reassess. Why? Because the trajectory of US-China relations is empirically worsening over time. US household deleveraging and the Chinese shift away from export-manufacturing (Chart 3) broke the basis of strong relations during the US’s distractions in Iraq and Afghanistan and China’s “peaceful rise” in the early 2000s. US consumers grew thriftier while Chinese wages rose. Not only has China sought economic self-sufficiency as a strategic objective since General Secretary Xi Jinping took power in 2012, but the Great Recession, Trump trade war, and global pandemic have accelerated the process of decoupling between the two economies. Decoupling is an empirical phenomenon, and it has momentum, however debatable its ultimate destination (Chart 4). Obviously policy at the moment is accelerating decoupling. Chart 3The Great Economic Divorce

The Great Economic Divorce

The Great Economic Divorce

Chart 4Decoupling Is Empirical

Decoupling Is Empirical

Decoupling Is Empirical

The US threat to cease payments on some of China’s Treasury holdings is an inversion of the fear that prevailed in the wake of 2008, that China would sell its treasuries to diversify away from dependence on the US and the greenback. China did end up selling its treasuries, but the US was not punished with higher interest rates because other buyers appeared. The US remains the world’s preponderant power and ultimate safe haven (Chart 5). By the same token, Trump and Kudlow naturally poured water on the threat of arbitrarily stopping payments because that would jeopardize America’s position. Chart 5Treasuries Can't Be Weaponized By Either Side...

Treasuries Can't Be Weaponized By Either Side...

Treasuries Can't Be Weaponized By Either Side...

Chart 6... But Tariffs Can And Will Be

... But Tariffs Can And Will Be

... But Tariffs Can And Will Be

Instead Trump is threatening a new round of trade tariffs. Since the US runs a large trade deficit with China, and China is more exposed to trade generally, the US has the upper hand on this front. But it is important to notice that US tariff collections as a share of imports bottomed under President Obama (Chart 6). The US shift away from free trade toward protectionism occurred in the wake of the 2008 financial crisis. President Trump then popularized and accelerated this policy option in an aggressive and unorthodox way. Trade tariffs are a tool of American statecraft, not the whim of a single person, who may exit the White House in January 2021 anyway. The retreat from globalization is not a passing fancy. Today’s recession also marks the official conclusion of China’s historic 44 year economic boom – and hence a concrete blow to the legitimacy of the ruling Communist Party (Chart 7). The more insular, autarkic shift in the Communist Party’s thinking is not irreversible, but there are no clear signs that Xi Jinping is pivoting toward liberalism after eight years in power. Chart 7Recession Destabilizes The 'G2' Powers

Recession Destabilizes The 'G2' Powers

Recession Destabilizes The 'G2' Powers

China’s unemployment rate has been estimated as high as 20.5% by Zhongtai Securities, which then retracted the estimate (!). It is at least at 10%. Moreover 51 million migrant workers vanished from the job rolls in the first quarter of the year. Maximum employment is the imperative of East Asian governments, especially the Communist Party, which has not dealt with joblessness since the late 1990s. The threat to social and political stability is obvious. The party will take extraordinary measures to maintain stability – not only massive stimulus but also social repression and foreign policy distraction to ensure that people rally around the flag. Xi Jinping has tried to shift the legitimacy of the party from economic growth to nationalism and consumerism, the “China Dream.” But the transition to consumer growth was supposed to be smooth. Financial turmoil, the trade war, and now pandemic and recession have forced the Communist Party off the training wheels well before it intended. Xi’s communist ideology, economic mercantilism, and assertive foreign policy have created an international backlash. The US is obviously indulging in nationalism as well. A stark increase in inequality and political polarization exploded in President Trump’s surprise election on a nationalist and protectionist platform in 2016 (Chart 8). All candidates bashed China on the campaign trail, but Trump was an anti-establishment leader who disrupted corporate interests and followed through with his tariff threats. The result is that the share of Americans who see China’s power and influence as a “major threat” to the United States has grown from around 50% during the halcyon days of cooperation to over 60% today. Those who see it as a minor threat have shrunk to about a quarter of the population (Chart 9). Chart 8A Measure Of Inequality In The US

A Measure Of Inequality In The US

A Measure Of Inequality In The US

Chart 9US Nationalism On The Rise

#WWIII

#WWIII

Chart 10Broad-Based Anti-China Sentiment In US

#WWIII

#WWIII

As with US tariff policy, the bipartisan nature of US anger toward China is significant. More than 60% of Democrats and more than 50% of young people have an unfavorable view of China. College graduates have a more negative opinion than the much-discussed non-college-educated populace (Chart 10). Already it is clear, in Joe Biden’s attack ads against Trump, that this election is about who can sound tougher on China. The debate is over who has the better policy to put “America first,” not whether to put America first. Biden will try to steal back the protectionist thunder that enabled Trump to break the blue wall in the electorally pivotal Rust Belt in 2016 (Map 1). Biden will have to win over these voters by convincing them that he understands and empathizes with their Trumpian outlook on jobs, outsourcing, and China’s threats to national security. He will emphasize other crimes – carbon emissions, cyber attacks, human rights violations – but they will still be China’s crimes. He will return to the “Pivot to Asia” foreign policy of his most popular supporter, former President Barack Obama. Map 1US Election: Civil War Lite

#WWIII

#WWIII

Bottom Line: Economic slowdown and autocracy in China, unprecedented since the Cultural Revolution, is clashing with the United States. Broad social restlessness in the US that is resolving into bipartisan nationalism against a peer competitor, unprecedented since the struggle with the Soviets in the 1960s, is clashing with China. Now is not the time to assume global stability. Constraints Still Operate, But Buy Insurance The story outlined above is by this time pretty well known. But the “Phase One” trade deal allowed global investors to set aside this secular story at the beginning of the year. Now, as Trump threatens tariffs again, the question is whether he will resort to sweeping, concrete, punitive measures against China that will take on global significance – i.e. that will drive the financial markets this year. Trump is still attempting to restore his bull market and magnificent economy. As long as this is the case, a constraint on conflict operates this year. It is just not as firm or predictable. Therefore we are looking for three things. Chart 11Trump May Seek A Crisis ‘Bounce’ To Popularity

#WWIII

#WWIII

First, will President Trump’s approval rating benefit so much from his pressure tactics on China that he finds himself driven into greater pressure tactics? This raises the risk of policy mistakes. Second, will Trump’s approval rating fall into the doldrums, stuck beneath 43%, as the toll of the recession wears on him and popular support during the health crisis fades? “Lame duck” status would essentially condemn him to electoral loss and incentivize him to turn the tables by escalating the conflict with China. Presidents are not very popular these days, but a comparison with Trump’s two predecessors shows that while he can hardly obtain the popularity boost that Obama received just before the 2012 election, he could hope for something at least comparable to what George W. Bush received amid the invasion of Iraq (Chart 11). (Trump has generally been capped at 46% approval, the same as his share of the popular vote in 2016.) The reason this is a real risk, not a Shakespearean play, is outlined above: however cynical Trump’s political calculus, he would be reasserting US grand strategy in the face of a great power that is attempting to set up a regional empire from which, eventually, to mount a global challenge. Thus if he is convinced he cannot win the election anyway, this risk becomes material. Investors should take seriously any credible reports suggesting that Trump is growing increasingly frustrated with his trailing Biden in head-to-head polls in the swing states. Third, will China, under historic internal stress, react in a hostile way that drives Trump down the path of confrontation? China has so far resorted to propaganda, aircraft carrier drills around the island of Taiwan, and maritime encroachments in the South China Sea – none of which is intolerably provocative to Trump. A depreciation of the renminbi, a substantial change to the status quo in the East or South China Seas, or an attempt to vitiate US security guarantees regarding US allies in the region, could trigger a major geopolitical incident. A fourth Taiwan Strait crisis is fully within the realm of possibility, especially given that Taiwan’s “Silicon Shield” is fundamentally at stake. While we dismiss rumors of Kim Jong Un’s death in North Korea, any power vacuum or struggle for influence there is of great consequence in today’s geopolitical context. Aggressive use of tariffs always threatened to disrupt global trade and financial markets, but tariffs function differently in the context of a global economic expansion and bull market, as in 2018-19, than they do in the context of a deep and possibly protracted recession. Trump has a clear political incentive to be tough on China, but an equally clear financial and economic incentive to limit sweeping punitive measures and avoid devastating the stock market and economy. If events lower the economic hurdle, then the political incentive will prevail and financial markets will sell. Bottom Line: However small the risk of Trump enacting sweeping tariffs, the downside is larger than in the 2018-19. The stock market might fall by 40%-50% rather than 20% in an all-out trade war this year. Investment Takeaways Go tactically long US 10-year treasuries. Book a 9.7% profit on our long 30-year US TIPS trade. Close long global equities (relative to US) for a loss of 3.8%. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com

Chinese automobile sales plunged 42% year-on-year over the first quarter of this year, due to the Covid-19 lockdowns (Chart II-1). We still expect auto sales in China to be flat or very mildly negative year-on-year over the period of April-December of this year. First, official data shows the growth rate for nominal disposable income was falling toward zero, but realistically it was probably negative in the first quarter (Chart II-2, top panel). Very sluggish household income growth – in combination with the still-elevated uncertainty of the job market (Chart II-2, bottom panel) – will restrain Chinese auto demand. Chart II-1Auto Sales In China: A Rate Of Change Recovery Ahead

Auto Sales In China: A Rate Of Change Recovery Ahead

Auto Sales In China: A Rate Of Change Recovery Ahead

Chart II-2Sluggish Household Income Growth Will Constrain Chinese Auto Demand

Sluggish Household Income Growth Will Constrain Chinese Auto Demand

Sluggish Household Income Growth Will Constrain Chinese Auto Demand

While household income growth will recover from current level later this year, it will likely remain much lower than the previous years’ 8-9% growth. Second, Chinese households are already quite leveraged. Their debt levels reached over 94% of annual disposable income, almost as high as in the US (Chart II-3). Third, peer-to-peer lending – an important source of auto loans in recent years – has shrunk considerably and is unlikely to pick up this year (Chart II-4). Chart II-3Chinese Household Debt Burden Is High

Chinese Household Debt Burden Is High

Chinese Household Debt Burden Is High

Chart II-4Auto Financing Has Become More Scarce

Auto Financing Is Becoming More Scarce

Auto Financing Is Becoming More Scarce

Bank lending rates for household consumption loans and peer-to-peer lending rates are currently about 5% and 10%, respectively. Such borrowing costs are restrictive given the tame growth of household income. Finally, the stimulus packages intended to boost automobile demand this year are no greater than they were last year. This entails that the net stimulus is close to zero. The focus of this year’s stimulus remains on the demand for new energy vehicles (NEV), which is in line with the central government’s strategic goal. Given that NEVs account for only 5% of auto sales, any boost to NEV demand is unlikely to make a huge difference in aggregate auto sales. Another boost to auto sales is the relaxation of license controls in the first-tier cities. The extent of these measures is so far considerably smaller than it was last year. About 60,0001 additional new license plates have so far been added, accounting for only 0.2% of Chinese auto sales. This number was 180,000 last year.2 This year local governments in 16 cities announced cash subsidies for auto buyers.3 Despite larger geographic coverage, the amount of cash subsidies is similar to what it was last year – at about 3% of the retail price. This is too small to make any meaningful impact on auto sales. Investment Implications The lack of considerable new stimulus for auto purchases and lower household income growth will make the recovery in passenger car sales halting and hesitant. Chinese auto stock prices in the domestic A-share market are breaking down (Chart II-5). Lingering demand contraction as well as possible price cuts will further curtail auto producers’ profits. Disappointing Chinese auto sales will lead to sluggish auto production and, consequently, to weak demand for metals like steel, aluminum and zinc. Chinese auto exports will outpace its imports (Chart II-6). As China accounts for about 30% of global auto sales and production, rising net exports of automobiles from China may diminish other global producers’ margins. Chart II-5Avoid Chinese Auto Stocks For Now

Avoid Chinese Auto Stocks For Now

Avoid Chinese Auto Stocks For Now

Chart II-6Rising Chinese Auto Net Exports Are Negative To Other Global Auto Producers

Rising Chinese Auto Net Exports Are Negative To Other Global Auto Producers

Rising Chinese Auto Net Exports Are Negative To Other Global Auto Producers

Ellen JingYuan He Associate Vice President ellenj@bcaresearch.com Footnotes 1Shanghai announced to add 40,000 new license plates this year while Hangzhou increased 20,000 new license plates. 2There were 100,000 additional license plates approved by Guangzhou province and an additional 80,000 by Shenzhen in 2019. 3The cash subsidies are about RMB1000-3000 for buying regular cars, RMB3000-5000 for car replacement (e.g., scrapping their autos with Emission Standard 3 and buying autos with new Emission Standard 6), and RMB5000-10,000 for NEV purchases.

Analyses on Chinese autos and Brazil are available below. Highlights The Fed’s aggressive monetization of public and some private debt has inspired investors to allocate cash to risk assets However, a number of cyclical indicators continue to flash red or amber, suggesting this rally is not about a cyclical economic recovery. Continue underweighting EM equities and credit markets versus their DM counterparts. We will wait for a correction to assess whether to maintain or close our shorts on EM currencies. Feature Neither the ongoing plunge in corporate profits nor a great deal of uncertainty about the economic outlook justify this rally. It seems the sole driver of the rally from March’s lows has been the Federal Reserve’s enormous purchases of various securities. These unprecedented actions are crowding out investors into riskier parts of fixed-income markets and persuading them to purchase equities. Neither the ongoing plunge in corporate profits nor a great deal of uncertainty about the economic outlook justify this rally. It Has Not Been About Profits And Valuations In the past two months, the S&P 500 index has experienced not only the fastest and steepest crash on record, but also the speediest rebound (Chart I-1). Investors have had to make swift investment decisions amid extremely low economic visibility. Chart I-1The S&P 500: The Fastest Crash And Speediest Recovery

The S&P 500: The Fastest Crash And Speediest Recovery

The S&P 500: The Fastest Crash And Speediest Recovery

Indeed, it is fair to say that during the mayhem and carnage many investors operated on a “sell now, think later” principle, and on the subsequent rebound with a “buy now, ask questions later” framework. Remarkably, the plunge and subsequent recovery in global share prices has been so rapid that even equity analysts’ forward earnings estimates cannot keep up. The top panel of Chart I-2 illustrates that the global forward EPS usually tracks the world equity index. When share prices rally, analysts upgrade their earning expectations; when equities sell off, analysts’ downgrade their earnings outlooks. In the past month, analysts have continued to slash forward EPS estimates despite the strong equity rebound. As a result, the 12-month forward P/E ratio for global stocks is back to its post-2008 highs (Chart I-2, bottom panel). Chart I-2Rising Share Prices Amid Collapsing Forward Earnings

Rising Share Prices Amid Collapsing Forward Earnings

Rising Share Prices Amid Collapsing Forward Earnings

Chart I-3China: A Decoupling Between Economy And Equities

China: A Decoupling Between Economy And Equities

China: A Decoupling Between Economy And Equities

Elsewhere, Chart I-3 illustrates China’s domestic orders for 5000 industrial enterprises historically correlated with the Shanghai Composite equity index. Since early this year, domestic orders have plummeted due to the country-wide lockdown. Yet equity prices in China have not fallen enough to reflect the downfall in economic activity and corporate profits. This underscores that investors’ purchases of global and Chinese stocks in the past month have been driven by factors other than the corporate profit outlook. This leaves two rationales for justifying roaring equity purchases in recent weeks: (1) liquidity overflows due to central banks’ balance sheet expansion, and (2) valuations. We examine the first argument in this report and will revisit the topic of equity valuations in forthcoming publications. In a nutshell, although equity valuations may be cheap in EM, Europe and Japan, they are expensive in the US. Nevertheless, the US stock market has been substantially outperforming EM and DM ex-US equities. Further, the most expensive stocks in the US – FAANGM – have by far outperformed the rest. Chart I-4China: A Decoupling Between New And Old Economy Stocks

China: A Decoupling Between New And Old Economy Stocks

China: A Decoupling Between New And Old Economy Stocks

In China, the ChiNext index – a Nasdaq proxy of the onshore market – has massively outperformed the Shanghai Composite index, which is dominated by “old” economy stocks (Chart I-4). The trailing P/E ratios on the ChiNext and Shanghai Composite indexes are 62 and 14, respectively. In short, the fact that most expensive equity segments/sectors have outperformed suggests that cheap valuation have not been the key driver of this rally. Bottom Line: Neither profits nor considerations of equity valuations have been the driving factor behind the recent equity rally. The Sole Driver Of This Rally The Fed’s aggressive monetization of public and some private debt has inspired investors to allocate cash to risk assets. The US broad money supply is surging at a record pace, both in nominal and real terms (Chart I-5). Is there too much money relative to the size of financial assets? Chart I-5US Broad Money Supply Is Booming

US Broad Money Supply Is Booming

US Broad Money Supply Is Booming

Today we explore how the level of US broad money supply (M2) relates to the market cap of all bonds and stocks denominated in US dollars. US broad money (M2) supply encompasses all deposits and cash of residents and non-residents in and outside the US. Chart I-6 exhibits the ratio of US broad money supply (M2) relative to the sum of: Chart I-6The US: Broad Money Supply Relative To Equity And Bond Market Capitalization

The US: Broad Money Supply Relative To Equity And Bond Market Capitalization

The US: Broad Money Supply Relative To Equity And Bond Market Capitalization

the US equity market capitalisation (the Wilshire 5000); the market cap values of all US-dollar bonds, including government, corporate, mortgage-backed securities, asset-backed securities and commercial mortgage backed securities (the Bloomberg Barclays US Aggregate Index); the market cap value of US dollar-denominated bonds issued by EM governments and corporations; minus the Fed’s and US commercial banks’ holdings of all types of securities. The higher this ratio is, the more US dollar deposits (liquidity) is available per one dollar of outstanding securities – excluding those held by the Fed and US commercial banks. Based on the past 25 years, the US M2-to-market value of securities ratio is somewhat elevated. This means liquidity is relatively abundant. However, this may not preclude the ratio from drifting higher like it did in 2008. This scenario would be consistent with a renewed selloff in equity and credit markets. Interestingly, back in January, the ratio was almost at a 20-year low – i.e., money supply (liquidity) was tight relative to the market value of outstanding US dollar-denominated securities. This was contrary to the prevalent perception in the global investment community that in 2019 the advances in share prices and credit markets were liquidity-driven. We discussed what constitutes pertinent liquidity for financial assets in our January 16 report titled, A Primer On Liquidity. The key takeaways of the report were: Money supply – not central bank assets – is the ultimate liquidity available to economic agents to purchase goods and services as well as invest in both real and financial assets. Changes in the velocity of money are as important as those in money supply. Yet forecasting changes in the velocity of money is a near-impossible task, as it entails foreseeing the behavior of economic agents. A large and expanding stock of money in and of itself does not guarantee greater liquidity for asset markets. Gauging liquidity flows to asset markets boils down to predicting investor behavior. Liquidity flows into financial assets when “animal spirits” among investors improve, and vice versa. Bottom Line: Even though the US money supply is expanding at a record pace, the key to financial asset price fluctuations is willingness among investors to purchase those assets. In turn, willingness to allocate cash to securities is generally driven by (1) the potential income and cash flow generation by securities issuers; (2) uncertainty related to future income (the risk premium); and (3) the opportunity cost of holding cash. Presently, the opportunity cost of holding cash is the sole reason to buy risky securities. Cash flow/income generation is currently impaired for the majority of equities and credit instruments. Further, there is a great deal of uncertainty about issuers’ ability to generate cash/income for investors – i.e., the required risk premium should be very high. All of these circumstances make the risk-reward profile of this rally poor. Reasons To Fade This Rally There are several market-based indicators that do not corroborate a further run-up in EM and DM equity prices. Our Risk-On / Safe-Haven Currency Ratio has struggled to gain traction (Chart I-7, top panel). It is not confirming the rebound in EM share prices. It is essential to emphasize that this indicator is agnostic to the direction of the US dollar, as it is calculated as the ratio of cyclical commodities currencies (AUD, NZD, CAD, ZAR, BRL, MXN, CLP, RUB, and IDR) versus safe-haven currencies such as the Swiss franc and Japanese yen on a total-return basis – i.e., all exchange rates include the cost of carry. Chart I-7Various Reflation Indicators Have Been Slugish

Various Reflation Indicators Have Been Slugish

Various Reflation Indicators Have Been Slugish

Our Reflation Confirming Indicator has not been sending a strong bullish reflation signal either (Chart I-7, bottom panel). This indicator is composed of an equally-weighted average of industrial metals, platinum and US lumber prices. The Global Cyclical-to-Defensive Equity Sectors Ratio has formed a classic head-and-shoulders pattern, and has broken down (Chart I-8, top panel). The latest rebound has not altered this pattern. Therefore, the path of least resistance for this ratio is still down, which entails underperformance of the global cyclical equity sector versus global defensives. The latter often occurs in selloffs. Similarly, the relative performance of Swedish versus Swiss non-financial stocks has failed to rebound, having experienced a major breakdown in March (Chart I-8, bottom panel). Swedish non-financial stocks are much more cyclical than Swiss ones. Finally, the global business cycle is experiencing its deepest recession in the post-World War II period, with the pace and nature of the recovery remaining highly uncertain. Chart I-9 portends global EPS in SDR, which is the proper measure given the greenback’s weight in SDR is 58%, the euro’s 39%, the yen’s 11%, and the yuan’s 1%. Chart I-8Global Cyclical Stocks Have Not Outperformed

Global Cyclical Stocks Have Not Outperformed

Global Cyclical Stocks Have Not Outperformed

Chart I-9Global Corporate EPS In Perspective

Global Corporate EPS In Perspective

Global Corporate EPS In Perspective

Global EPS shrank by 28% in 2001-2002 and by 40% in the 2008 recession. Given the current recession will be deeper, global EPS will likely shrink by about 50%. We do not think equity markets are discounting such a dire outcome after the recent rally. Bottom Line: A number of cyclical indicators continue to flash red or amber, suggesting this rally is not about a cyclical economic recovery. Investment Strategy We closed our short position in EM equities on March 19, and on the March 26 report we argued that it was too late to sell but still too early to buy. Given the rally in global equities is overstretched from a short-term perspective, we will wait for a correction to assess whether to maintain or close our shorts on EM currencies. Chart I-10EM Currencies And S&P 500

EM Currencies And S&P 500

EM Currencies And S&P 500

That said, we maintained our underweights in both EM stocks and credit versus their DM peers. Also, we have continued to short EM currencies versus the US dollar. Chart I-10 demonstrates that EM currencies have failed to rally despite the strong rebound in the S&P 500. Given the rally in global equities is overstretched from a short-term perspective, we will wait for a correction to assess whether to maintain or close our shorts on EM currencies. For dedicated EM equity managers, our recommended overweights are Korea, Thailand, Vietnam, Russia, central Europe, Mexico and Peru. Our underweights are Brazil, South Africa, Turkey, Indonesia, India and the Philippines. We are neutral on other bourses. Last week we published two reports for fixed-income investors: EM: Foreign Currency Debt Strains and EM Domestic Bonds And Currencies. In the first report we assessed individual EM countries' vulnerabilities to foreign debt and discussed strategies for EM sovereign and corporate credits. In the second report, we upgraded our stance on EM local markets from underweight to neutral. Before upgrading to a bullish stance, we would first need to upgrade our stance on EM currencies. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Chinese Auto Sales: Disappointments Ahead Chinese automobile sales plunged 42% year-on-year over the first quarter of this year, due to the Covid-19 lockdowns (Chart II-1). We still expect auto sales in China to be flat or very mildly negative year-on-year over the period of April-December of this year. First, official data shows the growth rate for nominal disposable income was falling toward zero, but realistically it was probably negative in the first quarter (Chart II-2, top panel). Very sluggish household income growth – in combination with the still-elevated uncertainty of the job market (Chart II-2, bottom panel) – will restrain Chinese auto demand. Chart II-1Auto Sales In China: A Rate Of Change Recovery Ahead

Auto Sales In China: A Rate Of Change Recovery Ahead

Auto Sales In China: A Rate Of Change Recovery Ahead

Chart II-2Sluggish Household Income Growth Will Constrain Chinese Auto Demand

Sluggish Household Income Growth Will Constrain Chinese Auto Demand

Sluggish Household Income Growth Will Constrain Chinese Auto Demand

While household income growth will recover from current level later this year, it will likely remain much lower than the previous years’ 8-9% growth. Second, Chinese households are already quite leveraged. Their debt levels reached over 94% of annual disposable income, almost as high as in the US (Chart II-3). Third, peer-to-peer lending – an important source of auto loans in recent years – has shrunk considerably and is unlikely to pick up this year (Chart II-4). Chart II-3Chinese Household Debt Burden Is High

Chinese Household Debt Burden Is High

Chinese Household Debt Burden Is High

Chart II-4Auto Financing Has Become More Scarce

Auto Financing Is Becoming More Scarce

Auto Financing Is Becoming More Scarce

Bank lending rates for household consumption loans and peer-to-peer lending rates are currently about 5% and 10%, respectively. Such borrowing costs are restrictive given the tame growth of household income. Finally, the stimulus packages intended to boost automobile demand this year are no greater than they were last year. This entails that the net stimulus is close to zero. The focus of this year’s stimulus remains on the demand for new energy vehicles (NEV), which is in line with the central government’s strategic goal. Given that NEVs account for only 5% of auto sales, any boost to NEV demand is unlikely to make a huge difference in aggregate auto sales. Another boost to auto sales is the relaxation of license controls in the first-tier cities. The extent of these measures is so far considerably smaller than it was last year. About 60,0001 additional new license plates have so far been added, accounting for only 0.2% of Chinese auto sales. This number was 180,000 last year.2 This year local governments in 16 cities announced cash subsidies for auto buyers.3 Despite larger geographic coverage, the amount of cash subsidies is similar to what it was last year – at about 3% of the retail price. This is too small to make any meaningful impact on auto sales. Investment Implications The lack of considerable new stimulus for auto purchases and lower household income growth will make the recovery in passenger car sales halting and hesitant. The lack of considerable new stimulus for auto purchases and lower household income growth will make the recovery in passenger car sales halting and hesitant. Chinese auto stock prices in the domestic A-share market are breaking down (Chart II-5). Lingering demand contraction as well as possible price cuts will further curtail auto producers’ profits. Disappointing Chinese auto sales will lead to sluggish auto production and, consequently, to weak demand for metals like steel, aluminum and zinc. Chinese auto exports will outpace its imports (Chart II-6). As China accounts for about 30% of global auto sales and production, rising net exports of automobiles from China may diminish other global producers’ margins. Chart II-5Avoid Chinese Auto Stocks For Now

Avoid Chinese Auto Stocks For Now

Avoid Chinese Auto Stocks For Now

Chart II-6Rising Chinese Auto Net Exports Are Negative To Other Global Auto Producers

Rising Chinese Auto Net Exports Are Negative To Other Global Auto Producers

Rising Chinese Auto Net Exports Are Negative To Other Global Auto Producers

Ellen JingYuan He Associate Vice President ellenj@bcaresearch.com Brazil: Not Out Of The Woods Yet We believe risks to Brazilian assets remain to the downside. Political infighting among various branches of power and state institutions will depress consumer and business confidence, lengthening the recession. Chart III-1Brazil: Recurring Crises

Brazil: Recurring Crises

Brazil: Recurring Crises

Political infighting among various branches of power and state institutions will depress consumer and business confidence, lengthening the recession (Chart III-1). Political turmoil also reduces the probability of structural reforms. This combined with a delayed economic recovery will further strain the already precarious public debt dynamics. First, the country is in a full-blown political crisis. The Supreme Court's decision to reject Bolsonaro's nomination for Director of the Federal Police manifests broad-based political infighting among Brazilian institutions. Further, the Supreme Court has started an investigation into the President as calls for impeachment intensify among both the public and the Congress. The rift between President Bolsonaro and Congressional President Maia is especially worrisome. Given Maia’s future political ambitions, we do not expect a truce between the two. On the contrary, they will continue to stand off in order to assert control over the fragmented Congress. As a result, structural reforms such as the national tax program and privatizations will be delayed. Second, Bolsonaro’s popularity is also plunging due to his slow and controversial response to the COVID-19 outbreak. This week, Bolsonaro’s disapproval ratings jumped above those of former president Lula da Silva, and public support for impeachment is now over 54%. Third, Congress has allowed the government to go over the limit of fiscal spending this year, which has resulted in almost 1.2 trillion reais in emergency fiscal spending, or about 16% of GDP. This will push the gross public debt-to-GDP ratio to well above 100% by the end of 2020. Chart III-2This Large Gap Makes Public Debt Dynamics Untenable

This Large Gap Makes Public Debt Dynamics Untenable

This Large Gap Makes Public Debt Dynamics Untenable

In order to stabilize its public debt-to-GDP ratio, a government’s borrowing costs should be below nominal GDP growth. Brazil fails to meet this condition. Local currency interest rates at 5.5% are well above nominal GDP growth, which will likely be negative in 2020 (Chart III-2). This assures unsustainable debt dynamics. Finally, in terms of monetary policy, the central bank’s policy rate cuts have not been efficiently transmitted to the real economy, as discussed in our March 31st Special Report. Borrowing costs for companies and households remain elevated relative to their nominal income growth. Overall, the sole feasible way for Brazil to stabilize its public debt-to-GDP ratio is to push nominal GDP growth above interest rates. Further, this is only possible with falling interest rates and further material currency depreciation. The continued currency devaluation represents a risk to foreign investors holding local assets. Investment Recommendations Continue to underweight Brazil within EM equity and credit portfolios. We reiterate our trade to short the BRL versus the US dollar. Even though the BRL is moderately cheap (Chart III-3), there is still considerable downward pressure on the currency. The BRL is tightly correlated with commodities prices (Chart III-4). Until these do not bottom out, the real will continue depreciating. Critically, the real needs to depreciate to lift nominal GDP growth above borrowing costs. The latter is essential to stabilize public debt dynamics. Chart III-3The BRL Is Only Modestly Cheap

The BRL Is Only Modestly Cheap

The BRL Is Only Modestly Cheap

Chart III-4The BRL Correlates With Commodities Prices

The BRL Correlates With Commodities Prices

The BRL Correlates With Commodities Prices

Finally, we are underweight both local currency and US$ denominated bonds in Brazil due to worrisome public debt dynamics and high foreign currency stress. Juan Egaña Research Associate juane@bcaresearch.com Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 Shanghai announced to add 40,000 new license plates this year while Hangzhou increased 20,000 new license plates. 2 There were 100,000 additional license plates approved by Guangzhou province and an additional 80,000 by Shenzhen in 2019. 3 The cash subsidies are about RMB1000-3000 for buying regular cars, RMB3000-5000 for car replacement (e.g., scrapping their autos with Emission Standard 3 and buying autos with new Emission Standard 6), and RMB5000-10,000 for NEV purchases. Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

BCA Research's China Investment Strategy service expects the recovery in Chinese domestic demand to pick up momentum in the second half of this year. A modest recovery in oil prices in Q3 will not be enough to return China's PPI to positive territory. Even…

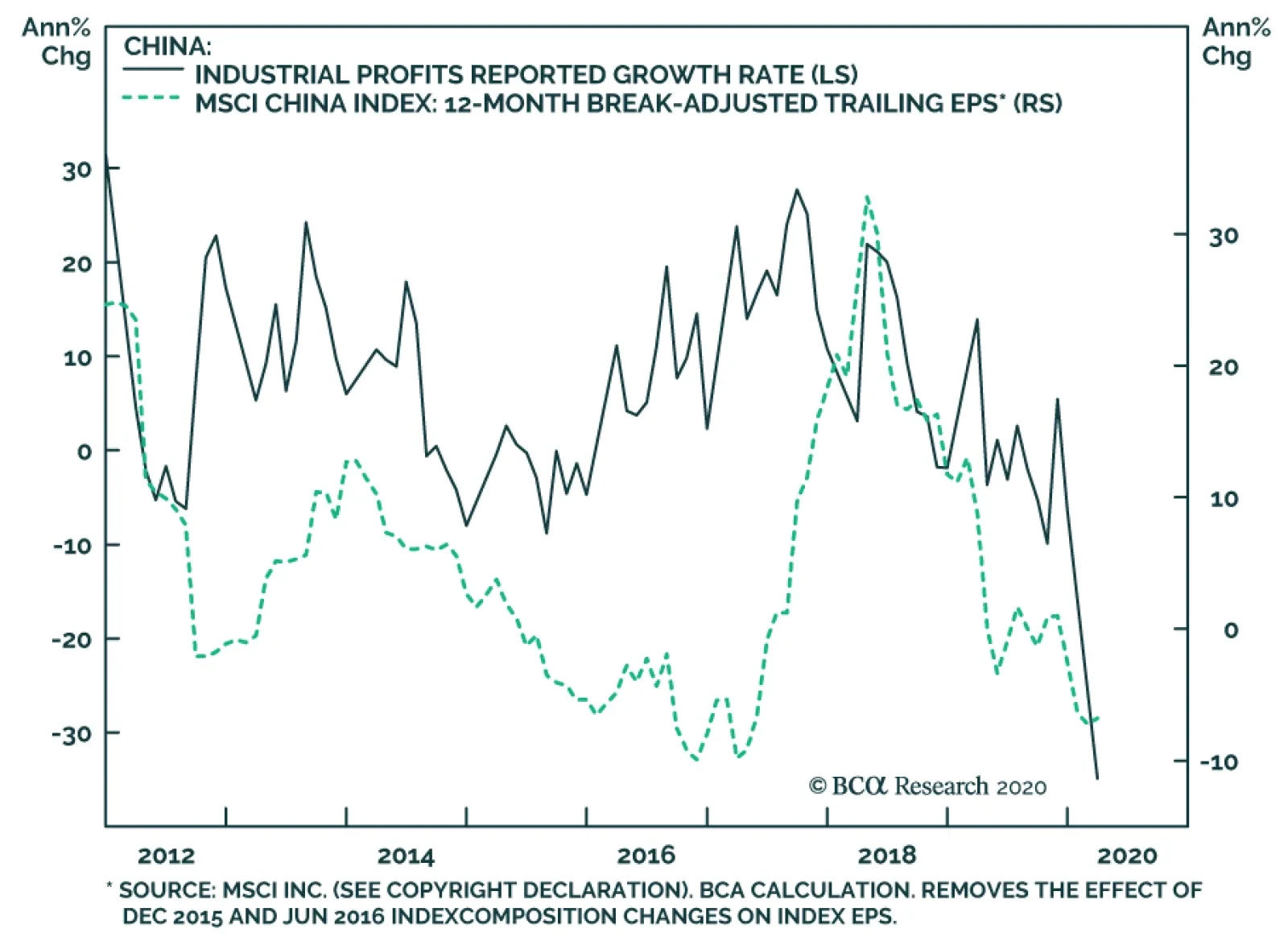

Highlights Even as a net oil importer, China loses more than it gains when oil prices collapse. An oil price collapse generates a formidable deflationary force, which will further depress China’s industrial pricing power and profit growth in Q2. There are early signs that demand in some sectors is gaining traction in the first three weeks of April. A full removal of travel restrictions in late May in China should help speed up the return of domestic business activities. We maintain our view that China’s economic recovery will pick up momentum in H2, underpinning our cyclical overweight stance on Chinese risk assets. Feature The nosedive in oil futures last week was a rude awakening of the enormous and unpredictable impact the pandemic has on the global economy and financial markets. WTI futures for May 2020 delivery fell to -$40.40 per barrel on April 20, an unprecedented event. The collapse in oil prices since March will generate substantial deflationary headwinds to China’s economy in the months ahead (Chart 1). Producer prices are already in contraction. An imported deflation from low oil prices will weaken industrial pricing power even more, pushing up real rates. China’s industrial profit growth also moves in lockstep with producer prices. A deepening in PPI contraction means industrial profit growth will remain underwater, underscoring our view that the near-term outlook for Chinese stocks is yet to turn sanguine (Chart 2). Chart 1Falling Oil Prices: A Substantial Deflationary Force

Falling Oil Prices: A Substantial Deflationary Force

Falling Oil Prices: A Substantial Deflationary Force

Chart 2Deflation Weakens Industrial Profit Growth

Deflation Weakens Industrial Profit Growth

Deflation Weakens Industrial Profit Growth

Oil prices will likely rebound in Q3 when the global economy re-opens, oil supply cuts take hold and the US dollar peaks. Our Commodity and Energy strategist estimates that WTI spot prices will reach $38/barrel by end-2020.1 A modest recovery in oil prices alone will not be enough to lift Chinese producer prices back to positive. The substantial reflationary efforts from China’s policymakers since Q1 should start to have an impact on the real economy in H2. The exponential credit growth should effectively prop up investment and consumption growth, and reduce inventory overhang in the industrial sector. We expect industrial producer prices and profits to turn slightly positive in Q3/Q4, underpinning our constructive view on Chinese stocks in the next 6- to 12-months. Oil Price Collapse: A Bane, Not A Boon China, as a net oil importer, stands to lose more than gain in an oil price war. This is contrary to commonly held economic theory that net oil importing countries are winners from cheaper oil. In theory falling oil prices reduces import prices, improves net oil importers’ term of trade, and in turn contributes positively to their GDP growth. In reality oil prices rarely fall in isolation. A precipitous fall in oil prices is almost always triggered by a sharp decline in global demand, accompanied with a spike in the US dollar, and results in a turmoil in the global financial markets (Chart 3). Therefore, depending on where an economy is positioned in the global value chain, a net oil importer may lose even more than a net oil exporter when oil prices collapse. Chart 3Global Trade Remains Under Pressure Until Dollar Peaks

Global Trade Remains Under Pressure Until Dollar Peaks

Global Trade Remains Under Pressure Until Dollar Peaks

Chart 4China Loses More From Falling Trade Than Gains From Falling Oil Prices

China Loses More From Falling Trade Than Gains From Falling Oil Prices

China Loses More From Falling Trade Than Gains From Falling Oil Prices

At only 14% of world oil consumption, China’s demand for oil alone is not enough to support a price recovery. But as a global manufacturing powerhouse, the benefits China has gained from cheaper oil in the past cycles were often more than offset by the economic and financial shocks from an oil price collapse (Chart 4). The small positive contribution to China’s GDP growth via savings on oil import bills is further discounted by losses from China’s own oil and oil-product exports (Chart 4, middle panel). China’s oil and gas sector does not necessarily benefit from collapsing oil prices. The country’s domestic oil exploration becomes deeply unprofitable when international oil prices collapse. Falling domestic demand for finished oil products and rising competition in the industry when prices are low squeeze out any extra profits for oil refineries (Chart 5). Chart 5China’s Energy Sector Suffers Too In An Oil Bear Market

China's Energy Sector Suffers Too In An Oil Bear Market

China's Energy Sector Suffers Too In An Oil Bear Market

Chart 6Energy Costs: A Small Part Of Chinese CPI

Energy Costs: A Small Part Of Chinese CPI

Energy Costs: A Small Part Of Chinese CPI

Chart 7US Consumers Benefit Much More From An Oil Price Decline Than Chinese Consumers

US Consumers Benefit Much More From An Oil Price Decline Than Chinese Consumers

US Consumers Benefit Much More From An Oil Price Decline Than Chinese Consumers

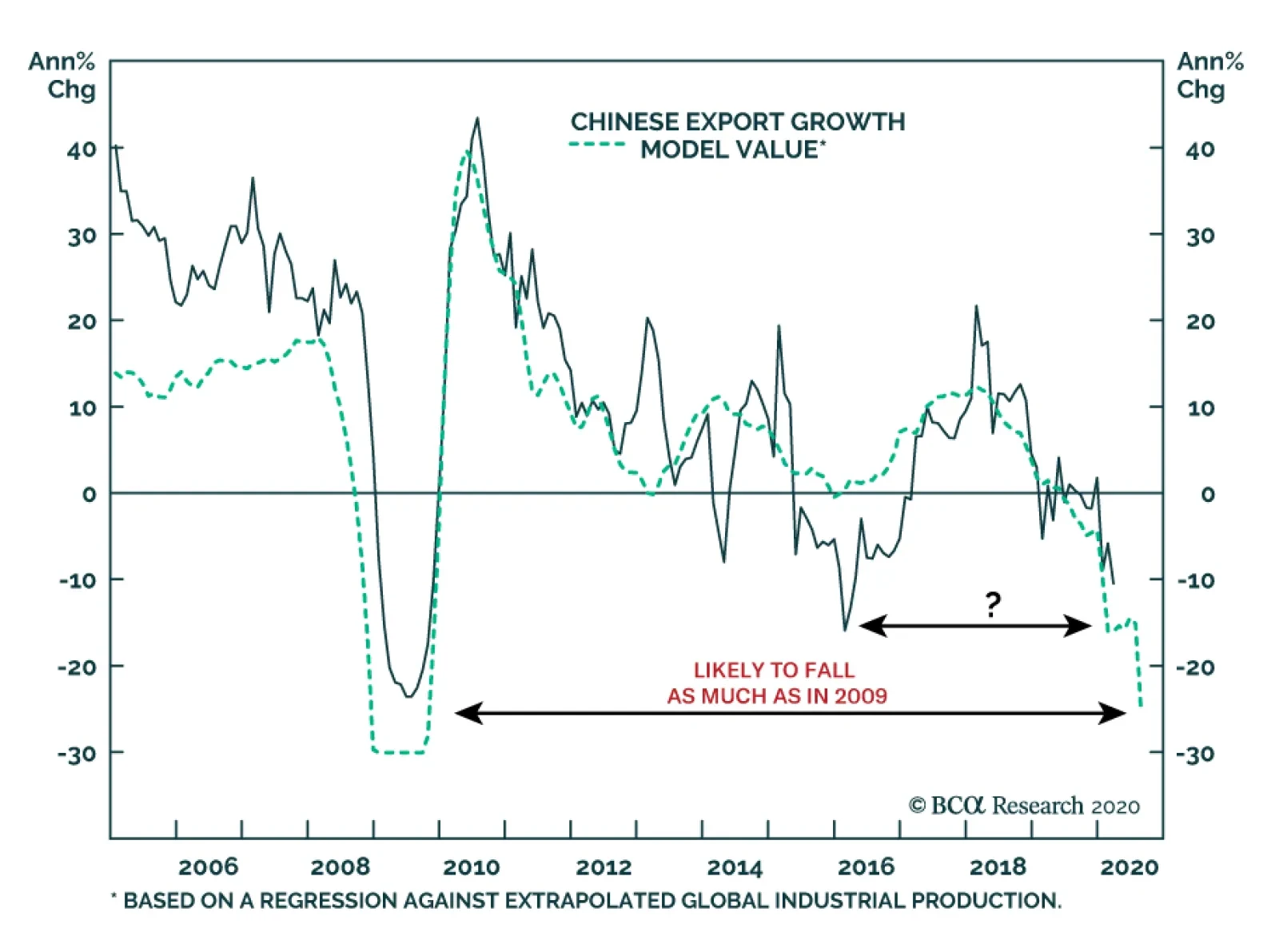

Furthermore, unlike the US, Chinese household consumption does not get a boost from cheaper oil. Food prices, rather than energy, drive the overall consumer price inflation in China (Chart 6). In addition, China’s domestic petrol market is heavily regulated and retail prices for energy are set by the Chinese government. China does not pass on the entire benefit of an energy price decline to its consumers, a rigid policy that has not been changed since 2016.2 As such, the current reduction in oil prices will not have the same “tax cut” benefit as it does for US consumers (Chart 7). Bottom Line: Low oil prices, accompanied by a strong dollar and depressed global trade, create a self-feeding deflationary feedback loop to China’s industrial sector, reducing the effects of the existing reflationary measures on its economy. Budding Signs Of Reflation A modest recovery in oil prices in Q3 will not be enough to return China's PPI to positive territory. Even when the global economy re-opens, the initial recovery in business activities and demand will likely be gradual, a situation China has experienced in the past two months (Chart 8). Thus, China’s domestic demand will bear most of the brunt to shore up inflation in produced goods, by propping up investment and consumption growth. We expect China’s substantial reflationary measures to start filtering into the real economy in H2. China’s industrial sector should get a boost from an acceleration in infrastructure investment and producer prices should turn moderately positive later in Q3 (Chart 9). Chart 8China’s Export Growth Set To Decline Further In Q2

China's Export Growth Set To Decline Further In Q2

China's Export Growth Set To Decline Further In Q2

Chart 9Huge Credit Wave Should Start Lifting Industrial Profits In H2

Huge Credit Wave Should Start Lifting Industrial Profits In H2

Huge Credit Wave Should Start Lifting Industrial Profits In H2

High-frequency data point to some early signs of a rebound in China’s domestic demand. The annual growth in the transaction volume of rebar steel rebounded from an 8% decline in March to 4% growth in the first three weeks in April.3 The contraction in passenger car sales also narrowed from -38% in March to -7.3% so far in April.4 China is ramping up its COVID-19 antibody testing to prevent a second-wave outbreak and is preparing for the National People’s Congress (NPC), which may take place in mid-May. Inter-provincial travel restrictions have limited the speed of recovery in business operations, but we expect such cautionary measures to be fully lifted in late May. The removal of logistic restrictions will help to accelerate a return to normal in both domestic production and demand. As we noted in our last week’s report,5 the April 17 Politburo meeting confirmed a policy shift to maximum reflation. President Xi’s new slogan, “The Six Stabilities and The Six Guarantees,” sets the tone that the government will increase investments to ensure that China’s post-pandemic economic growth is strong enough to stabilize employment. Bottom Line: Chinese business activities continue to inch up. The recovery in domestic demand should pick up momentum in H2 to offset imported deflationary pressures on China’s industrial profits. Investment Conclusions In the near term, a strong US dollar is a key risk to the recovery of China’s industrial profits. The greenback not only generates downward pressure on oil prices and global trade, but also puts the RMB in a poor position of depreciating against the dollar but at the same time appreciating against China’s export competitors (Chart 10). All are creating headwinds to China’s economic recovery. We recommend that investors stay on the sidelines in the near term until the dollar peaks and oil prices rebound, probably in Q3. However, on a cyclical time horizon, as the global economy re-opens and demands slowly recovers in H2, the flood of stimulus including China's own reflation efforts should help to restore investors’ risk appetite and lift the prices of risk assets. Although Chinese stocks have passively outperformed global stocks this year, the strong rebound in the SPX in recent weeks has made Chinese stocks slightly less overbought in relative terms (Chart 11). Chart 10A Tough Combination For The RMB

A Tough Combination For The RMB

A Tough Combination For The RMB

Chart 11Chinese Stocks: Slightly Less Overbought In Past Weeks

Chinese Stocks: Slightly Less Overbought In Past Weeks

Chinese Stocks: Slightly Less Overbought In Past Weeks

We expect China’s corporate profit growth to outpace global earnings growth this year, even as other economies re-open and start to recover. This warrants an overweight stance on Chinese stocks after near-term risks and market gyrations subside. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1Please see Commodity & Energy Strategy Weekly Report "USD Strength Restrains Commodity Recovery," dated April 23, 2020, available at ces.bcaresearch.com 2The floor for retail fuel prices is set at $40 a barrel to limit losses at China’s state-owned oil companies, which generally have average production costs in the range of $40-$50 per barrel. http://english.www.gov.cn/news/top_news/2016/01/13/content_281475271410529.htm 3Based on daily data from MySteel. 4Based on weekly data from China Passenger Car Association. 5Please see China Investment Strategy Weekly Report "Three Questions Following The Coronacrisis," dated April 23, 2020, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

China reported predictably terrible numbers for industrial profits in Q1: CNY 781 billion, down 36.7% year-on-year. Of the 41 industry categories, 39 saw profit declines, with petroleum and coal making an outright loss year-to-date. Moreover, there was little…

Highlights Kim Jong Un’s sickness or death is a matter of speculation and it is best to remain skeptical for now. If Kim dies or is incapacitated, it is a serious concern for North Korean and hence regional stability – and not only in the medium and long term. A North Korean power vacuum could trigger a major relapse in US-China relations. Even if Kim is healthy, his negotiations with President Trump could affect US-China relations or Trump’s reelection chances this year. US-China tensions could also break down separately this year – watch for yuan depreciation or for Trump to lose public approval. The South China Sea and Taiwan Strait are also non-negligible risks that could derail US-China relations before the US election. Feature If North Korean leader Kim Jong Un dies, it is a risk to global stability. We have no insight on Kim’s health or whereabouts but we do know that North Korea is relevant to global investors – it is no longer a joke – because US-China relations are no longer stable. Korean political risk has been on an uptrend since the second summit between Kim and President Trump in Hanoi, Vietnam was cut short without any agreement (Chart 1). Chart 1Korean Political Risk Already On An Uptrend Due To Pandemic, Recession, US-China Tensions

Korean Political Risk Already On An Uptrend Due To Pandemic, Recession, US-China Tensions

Korean Political Risk Already On An Uptrend Due To Pandemic, Recession, US-China Tensions

A dispute over North Korea could trigger a relapse in US-China relations that threatens the global equity rebound. Remain Skeptical As we go to press it is still unknown whether Kim is sick, well, living, or dying. What is known is that Kim failed to make a public appearance on Kim Il Sung Day, April 15, a noteworthy absence. China has sent a group of officials from the Communist Party’s Liaison Department, including medical doctors, according to Reuters – the most objective sign yet that something in North Korea has gone amiss. Japan’s Shukan Gendai on April 26 quoted an unnamed Chinese official saying that Kim was in a “vegetative state” after having stents put in his arteries after a heart attack. This corroborates (or repeats) the story that originally broke in South Korean newspaper Daily NK on April 21, saying that Kim was in grave condition after complications from heart surgery. Neither the Daily NK nor the Shukan Gendai are premium papers and the Daily NK also had to correct its original story which it attributed to “multiple” North Korean sources when in fact it only had one source. The US think tank 38 North on April 26 identified Kim’s elite passenger train at Wonsan but neither 38 North nor Reuters can confirm that Kim is actually in Wonsan. Kim was last seen in public on April 11 in Pyongyang, the day before Kim’s alleged surgery on April 12, but North Korean state press has reported on him conducting a range of activities since that date, albeit without video footage or anything that would disprove his incapacity. South Korean officials at the highest levels have repeatedly denied that they have intelligence of anything “special” happening in North Korea. South Korean assets are untroubled by the rumors (Chart 2). US President Donald Trump, and Pentagon officials, have also cast doubt on rumors that Kim is sick or dying – although various White House officials and Senator Lindsey Graham of South Carolina have implied something is wrong. Frequently it occurs that a temporary absence of autocratic leaders like Kim or Chinese President Xi Jinping causes the global media to speculate about illness, death, or intrigue. The lack of transparency of such regimes gives rise to a cottage industry of political watchers who interpret a leader’s every movement. Usually these rumor cycles amount to nothing. Absence of evidence (a leader’s failure to appear at an event) is not evidence of absence (the leader’s death). Still, the longer North Korea goes without offering definitive proof that Kim is alive, the greater the concerns will mount. One thing that we find unusual is the positioning of Kim’s sister, Kim Yo Jong. Kim Yo Jong was removed from the Politburo of the Korean Worker’s Party shortly after the failed Hanoi summit last year. She was reinstated as an alternate member on April 11 this year, in what was probably Kim Jong Un’s last credible public appearance. This gave rise to a surge of interest in her as a rising star, reflected in Google searches on April 12. These searches have spiked much more dramatically now that Kim Jong Un’s health is in question (Chart 3). Chart 2Korean Assets Not Responding Much To Kim Rumors

Korean Assets Not Responding Much To Kim Rumors

Korean Assets Not Responding Much To Kim Rumors

Chart 3Why Was Kim Yo-Jong Rehabilitated Just Before Kim’s Alleged Surgery?

North Korean Rumors: Significant ... If True

North Korean Rumors: Significant ... If True

The timing of her reinstatement, promptly followed by rumors about Kim’s health, is strange. North Korea’s political legitimacy is based on the Kim family dynasty. Her political recovery and promotion would be necessary to prepare her for any heightened role in the event of Kim’s incapacity or death. The purpose of the Politburo meeting was apparently to address the COVID-19 pandemic and delay a meeting of the legislature, the Supreme People’s Assembly. While rumors have focused on Kim’s cardiac event, we would not rule out the possibility that he has contracted COVID-19. Global leaders certainly are not immune to the disease, as evidenced by UK Prime Minister Boris Johnson. Reports also cite Kim's past periods of illness in 2012-14, although it is doubtful that his previous troubles with gout have any connection to a heart attack this month. What Is At Stake If Kim Exits The Scene For investors, the important thing to recognize is that North Korea is no longer irrelevant, no longer a geopolitical “red herring,” as we outlined in a series of reports in 2016 and 2017. Rather it is a critical moving part in a growing strategic conflict between the US and China. North Korea is a nuclear-armed state and a personalized autocracy with no clear succession plan, a stability risk on China’s border, and a national security risk to the United States and its allies Japan and South Korea. Pyongyang is in the midst of a multi-year, high-stakes diplomatic negotiation with its Northeast Asian neighbors and the United States. Diplomacy has not, thus far, gone off the rails. While Pyongyang has pushed the envelope with minor nuclear and missile activities, and by contesting Trump’s claims of exchanging letters, it has not abandoned negotiations with President Trump since 2017 by testing nuclear devices or intercontinental ballistic missiles, or by threatening to attack the US. South Korea’s legislative election on April 15 reinforced the leadership of President Moon Jae In and his left-leaning Democratic Party, marking a rebound for Moon due to his handling of the pandemic. This marks a boost to his “Moonshine” policy of diplomacy and economic integration with the North, another factor conducive to the continuation of diplomacy (Chart 4). However, any instability now would occur at a time of extreme vulnerability both within North Korea and abroad. North Korean growth is already facing a historic downturn unlike anything since the collapse of the Soviet Union (Chart 5). Chart 4Peaceniks Still Winning In South Korea

North Korean Rumors: Significant ... If True

North Korean Rumors: Significant ... If True

Chart 5North Korean Instability Is Likely Regardless Of Kim's Health

North Korean Instability Is Likely Regardless Of Kim's Health

North Korean Instability Is Likely Regardless Of Kim's Health

President Trump’s policy of “maximum pressure” sanctions has the North’s economy in a vise (Chart 6). For the past few years China has enforced sanctions on the North to cooperate with the United States. Beijing has reduced fuel exports and coal imports, according to official statistics (Chart 7). Chart 6Sanctions Have Damaged The Regime

Sanctions Have Damaged The Regime

Sanctions Have Damaged The Regime

Chart 7China's Sanctions Enforcement Is Critical

China's Sanctions Enforcement Is Critical

China's Sanctions Enforcement Is Critical

Even if China were not enforcing sanctions, North Korea’s economic conditions would be drastically deteriorating due to the COVID-19 pandemic, which has pushed China into what may well be the first recession since the 1970s (Chart 8). Thus if North Korea does end up having a leadership problem, investors should not assume that the regime will remain stable, in the near, medium, or long term. A power struggle broke out in China immediately upon Chairman Mao’s death in 1976. And when Kim Jong Un took power in December 2011, he struggled to consolidate power over the party, state, and military at first. He notoriously executed his uncle in December 2013 amid these internal struggles, which may have involved insubordinate military actions. His older brother Kim Jong Chol, or his sister Kim Yo Jong, would have more trouble consolidating power given that they were not Kim Jong Il’s choice for successor and would enter the supreme office in an extremely unstable time both at home and abroad. A succession process could also lead to external risks relatively quickly. North Korea’s historic surprise attack on the South Korean corvette, the Chonan, occurred in March 2010. Kim Jong Il was known to be preparing for his exit and for Kim Jong Un’s succession, so the regime sought to demonstrate strength while the world was distracted with a global financial crisis. If US-China relations were stable, there would be at least one substantial basis for believing that a North Korean crisis could be prevented from causing a crisis in other foreign relations. But US-China relations are not stable – they have deteriorated since the global financial crisis, as symbolized here by China’s diversifying away from US treasury holdings (Chart 9). The average US tariff rate on Chinese imports has risen from 5% to 15% under President Trump, who is threatening to impose additional punitive measures on China, such as export controls, as the two sides quarrel over the pandemic and recession. Chart 8Chinese Slowdown A Threat To Pyongyang

Chinese Slowdown A Threat To Pyongyang

Chinese Slowdown A Threat To Pyongyang

President Trump’s signature foreign policy initiative – as opposed to trade initiative – has consisted of negotiations with North Korea over denuclearization and eventual peace. If these negotiations fall apart, President Trump will suffer in a substantial way that will at least marginally harm his reelection chances on November 3. Chart 9US-China Relations Fundamentally Unstable

US-China Relations Fundamentally Unstable

US-China Relations Fundamentally Unstable

If the negotiations result in a “magnificent” deal this year, they could help those chances. Negotiations could face a test before that time, if either side abandons negotiations or gets cold feet before agreeing to a deal. Chart 10Brinkmanship Results In US Shows Of Force

Brinkmanship Results In US Shows Of Force

Brinkmanship Results In US Shows Of Force

Testing periods in the current relationship involve shows of US military strength, as in the summer of “fire and fury” in 2017, and as the US also showed in a similar summer of fire and fury with Iran in 2019 (Chart 10). Shows of force typically are a source of passing volatility, at best, in global financial markets. But in this year’s context the risk of broader US-China strategic competition would amplify that impact, even if it is transient. Investment Takeaways For global investors, what matters is if a North Korean crisis destabilizes the region and if US-China relations destabilize for this or any other reason. If Kim dies, we expect instability to ensue in North Korea eventually, if not immediately, and this would entail some degree of instability among the major powers. The US and China would seek to shape the outcome on the peninsula – China has already sent a team of officials. Washington and Beijing have a shared interest in preventing regime collapse, but they have a high level of distrust and different aims for the regime that might emerge in the aftermath. Tensions would get extremely high amid a power vacuum in North Korea. To gauge the durability of the US-China détente, the phase one trade deal signed in January, we are monitoring the CNY-USD exchange rate and President Trump’s approval rating (Chart 11). Renminbi depreciation is possible to ease pressure on China’s weak economy, but it would break the deal entirely, given that most other elements of the deal are either interrupted by the recession (goods purchases) or unverifiable (intellectual property protections). Chart 11Yuan Depreciation Or Falling Trump Approval Threaten Global Equities

Yuan Depreciation Or Falling Trump Approval Threaten Global Equities

Yuan Depreciation Or Falling Trump Approval Threaten Global Equities