China

Highlights Global growth is poised to accelerate this year, although the spread of the coronavirus could dampen spending in the very short term. History suggests that the likelihood of a recession rises when unemployment falls to very low levels. Three channels have been proposed to explain why that is: 1) Low unemployment can prompt households and businesses to overextend themselves, making the economy more fragile; 2) Faster wage growth stemming from a tight labor market can compress profit margins, leading to less capital spending and hiring; 3) Shrinking spare capacity can fuel inflation, forcing central banks to raise rates. The first channel is highly relevant for some smaller, developed economies where housing bubbles have formed and household debt has reached very high levels. However, it is not an immediate concern in the US, Japan, and most of the euro area. We would downplay the importance of the second channel, as faster wage growth is also likely to raise aggregate demand and incentivize firms to increase capital spending on labor-saving technologies. The third channel poses the greatest long-term risk, but is unlikely to be market-relevant this year. Investors should remain bullish on global equities over the next 12-to-18 months. A more prudent stance will be warranted starting in the second half of 2021. Global Equities: Sticking With Bullish Global equities are vulnerable to a short-term correction after having gained 16% since their August lows. Nevertheless, we continue to maintain a positive outlook on stocks for the next 12 months due to our expectation that global growth will gather steam over the course of the year. The latest data on global manufacturing activity has generally been supportive of our constructive thesis. The New York Fed Manufacturing PMI beat expectations, while the Philly Fed PMI jumped nearly 15 points to the highest level in eight months. The business outlook (six months ahead) component of the Philly Fed index rose to its best level since May 2018. European manufacturing should also improve this year. Growth expectations for Germany in the ZEW index surged in January, rising to the highest level since July 2015 (Chart 1). The Sentix and IFO indices have also moved higher. Encouragingly, euro area car registrations rose by 22% year-over-year in December. In the UK, business confidence in the CBI survey of manufacturers surged from -44 in Q3 of 2019 to +23 in Q4, the largest increase in the 62-year history of the survey. Fiscal stimulus and diminished risk of a disorderly Brexit should also bolster growth this year. Chart 1Some Green Shoots Emerging In The Euro Area

Some Green Shoots Emerging In The Euro Area

Some Green Shoots Emerging In The Euro Area

Chart 2EM Asia Is Rebounding

EM Asia Is Rebounding

EM Asia Is Rebounding

The manufacturing and trade data in Asia have been improving. Following last week’s better Chinese trade data, Korean exports recovered on a rate-of-change basis for a fourth month in a row. Japanese exports to China increased for the first time since last February. In Taiwan, industrial production increased by more than expected in December, as did export orders. Our EM Asia Economic Diffusion Index has risen to the highest level since October 2018 (Chart 2). Coronavirus: Nothing To Sneeze At? The outbreak of the coronavirus represents a potential short-term threat to the budding global economic recovery. Conceptually, outbreaks can affect the economy in two ways. One, they can reduce demand by curtailing spending on travel, entertainment, restaurants, or anything that requires close proximity to others. Two, they can reduce supply by causing people to avoid going to work. In practice, the first effect usually dominates the second. As a result, such outbreaks tend to have a deflationary impact. The Brookings Institution estimates that the 2003 SARS epidemic shaved about one percentage point from Chinese growth that year.1 The fact that this outbreak is happening during the Chinese New Year celebrations, when over 400 million people will be on the move, has the potential to exacerbate the transmission of the virus, and in the process, amplify the economic damage. That said, while it is from the same class of zoonotic viruses, early indications suggest that this particular strain is less lethal than SARS. In addition, the Chinese authorities have moved faster to address the risks than they did during the SARS outbreak. The government has effectively quarantined Wuhan, a city of 11 million people, where the virus appears to have originated. They have also sequenced the virus and shared the information with the global medical community. This has allowed the US Centers for Disease Control (CDC) to develop a test for the virus, which is likely to become available over the coming weeks. The Dark Side Of Low Unemployment Provided the coronavirus outbreak is contained, stronger global growth should continue to soak up lingering labor market slack. This raises the question of whether, at some point, declining unemployment could become counterproductive. The outbreak of the coronavirus represents a potential short-term threat to the budding global economic recovery. The unemployment rate in the OECD currently stands at 5.1%, below the low of 5.5% set in 2007 (Chart 3). In the US, the unemployment rate has dropped to a 50-year low. Chart 3Unemployment Rates Are Below Their Pre-Crisis Lows In Most Economies

Who’s Afraid Of Low Unemployment?

Who’s Afraid Of Low Unemployment?

No one would deny that the decline in unemployment since the financial crisis has been a welcome development. However, it does carry one major risk: Historically, the likelihood of a recession has risen when unemployment has fallen to very low levels (Chart 4). Chart 4Recessions Become More Likely When The Labor Market Begins To Overheat

Who’s Afraid Of Low Unemployment?

Who’s Afraid Of Low Unemployment?

Three channels have been proposed to explain this positive correlation: 1) Low unemployment can prompt households and businesses to overextend themselves, making the economy more fragile; 2) Faster wage growth stemming from a tight labor market can compress profit margins, leading to less capital spending and hiring; 3) Shrinking spare capacity can fuel inflation. This can force central banks to raise rates, choking off growth. Let’s examine each in turn. Unemployment And Irrational Exuberance Chart 5Growing Housing Imbalances In Some Economies

Growing Housing Imbalances In Some Economies

Growing Housing Imbalances In Some Economies

A strong economy promotes risk-taking. While some risk-taking is essential for capitalism, an excessive amount can lead to the buildup of imbalances, thereby setting the stage for an eventual downturn. In Australia, New Zealand, Canada, and the Scandinavian economies, the combination of low interest rates and strong economic growth has stoked debt-fueled housing bubbles (Chart 5, panel 3). As we discussed last week, higher interest rates in those economies could sow the seeds for economic distress.2 In most other countries, financial imbalances are not severe enough to trigger recessions. Chart 6 shows that the private-sector financial balance – the difference between what the private sector earns and spends – still stands at a healthy surplus of 3.4% of GDP in advanced economies. In 2007, the private-sector financial balance fell to 0.4% in advanced economies, reaching a deficit of 2% in the US. The private-sector balance also deteriorated sharply in the lead-up to the 2001 recession (Chart 7). Chart 6The Private Sector Spends Less Than It Earns In Most Economies

Who’s Afraid Of Low Unemployment?

Who’s Afraid Of Low Unemployment?

Chart 7The Private-Sector Surplus Is Larger Than It Was Before The End Of Previous Expansions

The Private-Sector Surplus Is Larger Than It Was Before The End Of Previous Expansions

The Private-Sector Surplus Is Larger Than It Was Before The End Of Previous Expansions

In the US, the personal savings rate has risen to nearly 8%, much higher than one would expect based on the level of household net worth (Chart 8). Despite growing at around 2.5% in 2018/19, real personal consumption has increased at a slower pace than predicted by the level of consumer confidence. This suggests that households have maintained a fairly prudent disposition. Consistent with this, the ratio of household debt-to-disposable income has declined by 32 percentage points since 2008. Chart 8Households Are Saving More Than One Would Expect

Households Are Saving More Than One Would Expect

Households Are Saving More Than One Would Expect

Granted, some credit categories have seen large increases (Chart 9). Student debt has risen to 9% of disposable income. Auto loans have moved back to their pre-recession highs. We would not worry too much about the former, as the vast majority of student debt is guaranteed by the government. Auto loans are more of a concern. However, it is important to keep in mind that the auto loan market is less than one-sixth as large as the mortgage market. Moreover, after loosening lending standards for vehicle loans between 2011 and 2016, banks have since tightened them. This adjustment appears to be largely complete. Lending standards did not tighten any further in the latest Senior Loan Officer Survey, while demand for auto loans rose at the fastest pace in two years. The share of auto loans falling into delinquency has been trending lower, which suggests that delinquency rates are peaking (Chart 10). Chart 9US Household Debt Levels Have Fallen, Despite Increases in Student And Auto Loans

US Household Debt Levels Have Fallen, Despite Increases in Student And Auto Loans

US Household Debt Levels Have Fallen, Despite Increases in Student And Auto Loans

Chart 10Auto Loans: Monitoring Trends In Credit Standards And Delinquency Rates

Auto Loans: Monitoring Trends In Credit Standards And Delinquency Rates

Auto Loans: Monitoring Trends In Credit Standards And Delinquency Rates

Lastly, we would point out that despite all the hoopla over the state of the auto market, auto loan asset-backed securities have performed well (Chart 11). While default rates have risen, lenders have generally set interest rates high enough to absorb incoming losses. Chart 11Securitized Auto Loans Have Performed Well

Securitized Auto Loans Have Performed Well

Securitized Auto Loans Have Performed Well

Will Falling Profit Margins Derail The Expansion? Profit margins usually peak a few years before the onset of a recessions (Chart 12, top panel). This has led some to speculate that falling margins could usher in a recession by curbing companies’ willingness to hire workers and invest in new capacity. Chart 12A Peak In Profit Margins: An Ominous Sign?

A Peak In Profit Margins: An Ominous Sign?

A Peak In Profit Margins: An Ominous Sign?

While it is an interesting theory, it does not stand up to closer scrutiny. Surveys of business sentiment clearly show that capital spending intentions are positively correlated with plans to raise wages (Chart 13, left panel). Far from cutting capital expenditures in response to rising wages, firms are more likely to boost capex if they are also planning to increase labor compensation. Chart 13AFaster Wage Growth, Increased Hiring, And More Capex Go Hand In Hand (I)

Faster Wage Growth, Increased Hiring, And More Capex Go Hand In Hand (I)

Faster Wage Growth, Increased Hiring, And More Capex Go Hand In Hand (I)

Chart 13BFaster Wage Growth, Increased Hiring, And More Capex Go Hand In Hand (II)

Faster Wage Growth, Increased Hiring, And More Capex Go Hand In Hand (II)

Faster Wage Growth, Increased Hiring, And More Capex Go Hand In Hand (II)

One reason for this is that rising wages make automation more attractive. By definition, automation requires more capital spending. However, that is not the entire story because firms also tend to hire more workers during periods when wage growth is rising (Chart 13, right panel). This implies that a third factor – strong economic growth – is responsible for both accelerating wages and rising hiring intentions. The fact that real business sales are strongly correlated with both employment growth and nonresidential investment is evidence for this claim (Chart 12, bottom panel). Falling Margins: A Symptom Of A Problem The discussion above suggests that faster wage growth is unlikely to dissuade firms from either hiring more workers or boosting capital spending. Indeed, the opposite is probably true: Since workers normally spend more of every dollar of income than firms do, an increase in the share of national income flowing to workers will lift aggregate demand. So why do profit margins usually peak before recessions? The answer is that declining labor market slack tends to push up unit labor costs, forcing central banks to hike interest rates in an effort to stave off rising inflation. Thus, falling margins are just a symptom of an underlying problem: economic overheating. Don’t blame lower margins for recessions. Blame central banks. Inflation Is Not A Threat... Yet For now, unit labor cost inflation remains reasonably well contained in the major economies (Chart 14). However, there is little evidence to suggest that the historic relationship between labor market slack and wage growth has broken down (Chart 15). Barring a major surge in productivity growth, inflation is likely to accelerate eventually as companies try to pass on higher labor costs to their customers. Chart 14AUnit Labor Costs Are Well Behaved For Now (I)

Unit Labor Costs Are Well Behaved For Now (I)

Unit Labor Costs Are Well Behaved For Now (I)

Chart 14BUnit Labor Costs Are Well Behaved For Now (II)

Unit Labor Costs Are Well Behaved For Now (II)

Unit Labor Costs Are Well Behaved For Now (II)

Chart 15Correlation Between Labor Market Slack And Wage Growth Remains Intact

Correlation Between Labor Market Slack And Wage Growth Remains Intact

Correlation Between Labor Market Slack And Wage Growth Remains Intact

We do not know exactly when such a price-wage spiral will emerge. Inflation is a notoriously lagging indicator (Chart 16). Our best guess is that inflation could become a serious risk for investors in late 2021 or 2022. Thus, investors should remain overweight global equities for the next 12-to-18 months, but be prepared to turn more cautious in the second half of 2021. Chart 16Inflation Is A Lagging Indicator

Who’s Afraid Of Low Unemployment?

Who’s Afraid Of Low Unemployment?

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 Jong-Wha Lee and Warwick J. McKibbin, “Globalization and Disease: The Case of SARS,” Brookings Institution, dated February 2004. 2 Please see Global Investment Strategy Weekly Report, “Bond Yields: How High Is Too High?” dated January 17, 2020. Global Investment Strategy View Matrix

Who’s Afraid Of Low Unemployment?

Who’s Afraid Of Low Unemployment?

MacroQuant Model And Current Subjective Scores

Who’s Afraid Of Low Unemployment?

Who’s Afraid Of Low Unemployment?

Strategic Recommendations Closed Trades

As tensions from the US-China trade war abate, investors are starting to refocus on economic fundamentals. This year, Chinese policymakers will maintain their tight grip on local government spending and bank lending, and will continue to fine-tune policies…

We have been cyclically overweight Chinese stocks, because we expected the economy to bottom in the first quarter of 2020 and a trade deal to materialize eventually. In the past two weeks, these two possibilities became realities. Last week's small selloffs…

Highlights An analysis on India is available on page 12. There is extreme complacency in global financial markets. With currency markets’ implied volatility at a record low, we recommend going long EM currency volatility. The latter will rise in the next six month regardless the direction of global risk assets. For now, we remain long the EM MSCI equity index with a stop point at 1050. In India, nominal income growth has fallen below lending rates. The latter have not declined despite monetary easing. The authorities will force banks to reduce their lending rates, which will hurt bank stocks. Feature “…we have probably seen the end of the boom-bust cycle.” Bob Prince, Co-CIO of Bridgewater World Economic Forum, Davos January 22, 2020 Low Volatility = Complacency Chart I-1Go Long Currency Volatility

Go Long Currency Volatility

Go Long Currency Volatility

The comment above by co-CIO of the largest hedge fund declaring the end of boom-bust cycle is consistent with lingering complacency in global financial markets. Any time an influential person made a similar declaration in the past, it marked a major turning point in financial markets. Remarkably, implied volatility for the US dollar has plummeted to a record low, as it has for EM currencies and a wide range of equity markets. Chart I-1 illustrates the implied volatility for EM currencies and the US dollar. Such low levels of implied currency market volatility historically preceded major moves in currency markets and often led to a material selloff in broad EM financial markets. It does not mean that the world economy will crash but financial markets volatility in general and currency market volatility in particular are bound to rise considerably in the months ahead. The risk-reward profile of going long EM currency or US dollar volatility appears very attractive. Today we recommend investors to go long EM currency volatility. The latter will rise regardless the direction of global risk assets. Concerning overall strategy, EM financial markets are entering a testing period. How broader EM risk assets and currencies perform in the coming weeks will signal how durable and long-lasting the current EM rally will be. Given global risk assets are overbought, a correction or consolidation phase is overdue. If EM equities, currencies and credit markets outperform, or at least do not underperform their DM peers in the course of this indigestion phase, it will beckon more upside for EM risk assets in 2020. If during budding market turbulence EM risk assets and currencies underperform their DM peers, it will signal their vulnerability in 2020.Implied volatility for the US dollar has plummeted to a record low, as it has for EM currencies. Implied volatility for the US dollar has plummeted to a record low, as it has for EM currencies. For now, we remain long the EM MSCI equity index with a stop point at 1050. We will upgrade our EM equity and credit market allocations versus DM if the EM universe generally exhibits relative resilience in the coming weeks, and more of our indicators confirm China’s growth recovery. Hints Of Recovery… December economic data out of China were strong, and it seems that the credit and fiscal stimulus are finally beginning to lift growth: Chinese imports and nominal industrial output – among the most reliable measures of the Chinese business cycle – posted very robust growth numbers in December (Chart I-2). DRAM and NAND semiconductor prices are climbing, and China’s container freight index is also in revival mode (Chart I-3). These high-frequency (daily and weekly) data confirm improving business activity in both the global semiconductor sector and in overall world trade. Chart I-2China's December Economic Data Were Strong

China's December Economic Data Were Strong

China's December Economic Data Were Strong

Chart I-3Asia's Trade Is Recovering

Asia's Trade Is Recovering

Asia's Trade Is Recovering

There are tentative signs of amelioration in our proxies for marginal propensity to spend by households and enterprises in China (Chart I-4). A more decisive improvement in these indicators is needed to reinforce the positive outlook for China’s growth. …But Doubts Still Linger Despite the recent improvement in Chinese economic data and the rebound in China-related plays, there are a number of financial market indicators that are not yet confirming a sustainable business cycle recovery in China and global trade. In particular: First, apart from semiconductor stocks, global cyclical equity sectors and sub-sectors – industrials, materials, and freight and logistics – have begun, once again, underperforming defensive sectors (Chart I-5). Outperformance by these cyclical sectors against defensives is essential in confirming that global and Chinese capital spending – which were the primary sources of the most recent slowdown – are picking up again. Chart I-4China: Tentative Improvement In Household And Corporate Marginal Propensity To Spend

China: Tentative Improvement In Household And Corporate Marginal Propensity To Spend

China: Tentative Improvement In Household And Corporate Marginal Propensity To Spend

Chart I-5Global Equities: Cyclicals Are Again Underperforming Defensives

Global Equities: Cyclicals Are Again Underperforming Defensives

Global Equities: Cyclicals Are Again Underperforming Defensives

Notably, the relative performance of EM share prices to the global equity benchmark historically tracks the relative performance of global materials versus the global overall stock index.1 However, the two have recently diverged (Chart I-6). In short, global materials are not corroborating sustainability in the recent EM outperformance. If EM equities, currencies and credit markets outperform, or at least do not underperform their DM peers in the course of this indigestion phase, it will beckon more upside for EM risk assets in 2020. Second, the rebound in Chinese and EM shares prices is not corroborated by Chinese onshore government bond yields, which are dipping to new cyclical lows (Chart I-7). In other words, interest rate expectations in China are falling – i.e., they are not confirming a robust recovery. Chart I-6Unsustainable Decoupling

Unsustainable Decoupling

Unsustainable Decoupling

Chart I-7A Message From The Chinese Fixed-Income Market

A Message From The Chinese Fixed-Income Market

A Message From The Chinese Fixed-Income Market

Third, EM ex-China currencies have not yet broken out versus the US dollar (Chart I-8). Consistently, the broad trade-weighted US dollar has not yet broken down. Chart I-9 illustrates that the greenback’s advance-decline line has not yet fallen below its 200-day moving average, a condition that has historically been required to confirm the dollar’s cyclical bear market. Chart I-8EM Currencies: No Breakout Yet

EM Currencies: No Breakout Yet

EM Currencies: No Breakout Yet

Chart I-9The US Dollar Is At A Critical Juncture

The US Dollar Is At A Critical Juncture

The US Dollar Is At A Critical Juncture

We view these exchange rate patterns as a litmus test to validate turning points in the global business cycle. Finally, the technical profiles of the KOSPI, EM small cap stocks and copper prices are inconclusive (Chart I-10). These markets have rebounded but seem to be confronting a critical technical test. If they decisively break above these technical levels, it will be a sign that the EM bull market will be lasting and durable. Otherwise, caution is still warranted. Bottom Line: There is a good amount of complacency among global investors at a time when there are several market signals that are still challenging the view of enduring revival in China/EM growth. Corporate Profits Will Be The Arbiter Ultimately, economic growth and corporate profits will determine the direction of not only share prices but also EM sovereign and corporate credit spreads as well as their currencies. So far, the EM equity rebound of the past 12 months has been solely due to multiples expansion amid a deepening EM profit recession: Earnings per share in US dollar terms has been contracting by 10% from a year ago, and the rate of change has so far not turned around (Chart I-11). Chart I-10The KOSPI And Copper Are Facing A Resilience Test

The KOSPI And Copper Are Facing A Resilience Test

The KOSPI And Copper Are Facing A Resilience Test

Chart I-11EM Equities: A Profitless Rally?

EM Equities: A Profitless Rally?

EM Equities: A Profitless Rally?

Going forward, however, EM corporate profits growth is set to improve. Our indicator for semiconductor companies’ revenues is heralding a revival in semi sector profits (Chart I-12, top panel). The rate-of-change improvement in commodities prices is also foreshadowing potential amelioration in corporate earnings growth among energy producers and materials (Chart I-12, middle and bottom panels). Chart I-12EPS Growth In EM Technology, Energy And Materials

EPS Growth In EM Technology, Energy And Materials

EPS Growth In EM Technology, Energy And Materials

We are negative on EM bank profits due to their need to recognize and provision for non-performing loans as well as the authorities’ mounting pressures on them to reduce lending rates. The latter will shrink banks’ elevated net interest rate margins. The profit profile of other EM equity sectors is illustrated in Chart I-13A and I-13B. Chart I-13AEM EPS Growth By Sectors

EM EPS Growth By Sectors

EM EPS Growth By Sectors

Chart I-13BEM EPS Growth By Sectors

EM EPS Growth By Sectors

EM EPS Growth By Sectors

Provided technology, materials and energy stocks account for 33% of the MSCI EM aggregate equity index’s earnings (banks account for another 28% of total profits), it is safe to assume that the growth rate of EM EPS will move from -10% currently to zero or mildly positive territory by mid-2020. Nevertheless, beyond the next several months, our leading indicators on the EM profit outlook are not positive. China’s narrow money growth leads EM EPS by 12 months, and currently suggests the EPS recovery will be both muted and short-lived (Chart I-14). The technical profiles of the KOSPI, EM small cap stocks and copper prices are inconclusive. Further, China’s broad money impulse points to a peak in the credit impulse in the first half of the year (Chart I-15). Given that EM share prices bottomed a year ago, simultaneously with China’s credit impulse, odds are that EM equities could slump with a rollover in the latter. Chart I-14EM EPS: Marginal Improvement Ahead But No Robust Recovery

EM EPS: Marginal Improvement Ahead But No Robust Recovery

EM EPS: Marginal Improvement Ahead But No Robust Recovery

Chart I-15China: A Signpost Of A Potential Top In The Credit Impulse

China: A Signpost Of A Potential Top In The Credit Impulse

China: A Signpost Of A Potential Top In The Credit Impulse

Chart I-16DM Central Banks' Assets And EM Stocks And Currencies: No Stable Correlation

DM Central Banks' Assets And EM Stocks And Currencies: No Stable Correlation

DM Central Banks' Assets And EM Stocks And Currencies: No Stable Correlation

What if the current liquidity-driven rally continues? In our report last week titled A Primer On Liquidity, we elaborated at great length about the different liquidity measures and how they influence financial asset prices. Empirically, changes in DM central banks’ balance sheets have had no stable correlation with either EM share prices or EM local currency bonds, as demonstrated in Chart I-16. There have been periods over the past 10 years when EM risk assets and currencies have performed poorly, despite an accelerating pace of QE programs worldwide (Chart I-16). The true and critical driver for EM equity and currency performance has been EM’s own domestic fundamentals and China’s business cycle (please refer to Chart I-11 on page 7). To be sure, we are not suggesting that DM central bank policies have not affected global and EM financial markets at all. They have done so in spades. By purchasing and withdrawing about $9 trillion in high-quality securities from the marketplace, the monetary authorities have shrunk the stock of available financial assets. Consequently, even though QE programs have expanded broad money supply only modestly,2 the upshot has been that more money has been chasing fewer financial assets. Also, low interest rates reduce the opportunity cost of owning risk assets. These two phenomena have led investors to bid up prices of various securities, including EM ones. Nevertheless, despite the ongoing and indiscriminate global search for yield, EM share prices in US dollar terms and EM ex-China currencies (including carry, i.e. on a total-return basis) are still below their 2010 levels. Such poor performance of EM risk assets has been a corollary of just how bad EM fundamentals have been. Bottom Line: EM corporate profits will improve on a rate-of-change basis in the coming months. However, forward-looking indicators do not yet point to a robust recovery in EM corporate profits as occurred in 2017. Investment Conclusions We are maintaining our long EM equities position with a stop point at 1050 for the MSCI EM stock index (7% below the current level). If EM share prices, credit markets and currencies outperform their DM peers during a correction/consolidation phase, we will upgrade EM allocations to overweight in global equity and credit portfolios. At the moment, EM is confronting a resilience test. Within the EM equity universe, our overweights are Russia, Korea, Thailand, Mexico, UAE, Pakistan and central Europe. Our recommended equity underweights include Indonesia, the Philippines, Hong Kong domestic stocks, South Africa, Turkey and Colombia. In sovereign credit and local bond markets, our overweights are Mexico, Russia, Thailand, Malaysia, Pakistan and Ukraine. In turn, South Africa, Turkey, Philippines and Indonesia warrant an underweight stance. Today we are upgrading Indian bonds from neutral to overweight (see page 17). In the currency space, we continue holding a short position versus the US dollar in the following basket of currencies: BRL, ZAR, CLP, COP, IDR, PHP and KRW. As always, the full list of our positions is presented at the end of report (please refer to pages 18-19 and on our website). Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com India: Beware Of Private Banks And Consumer Perils Indian private banks and consumer staple stocks have been holding up the Indian equity market at a time when the rest of the bourse has been sluggish. Both sectors, however, are extremely expensive and thus tremendously sensitive to minor profit disappointments. Remarkably, private banks now trade at a price-to-earnings (P/E) ratio of 31 and price-to-book value (PBV) ratio of 4. Indian consumer staple stocks, on the other hand, trade at a P/E ratio of 41 (Chart II-1 and Chart II-2). Chart II-1Indian Private Bank Stocks Are Expensive

Indian Private Bank Stocks Are Expensive

Indian Private Bank Stocks Are Expensive

Chart II-2Indian Consumer Staple Stocks Are Very Pricey

Indian Consumer Staple Stocks Are Very Pricey

Indian Consumer Staple Stocks Are Very Pricey

Chart II-3A Credit Boom Among Indian Private Banks

A Credit Boom Among Indian Private Banks

A Credit Boom Among Indian Private Banks

Given that private banks have been specializing in both mortgages and non-mortgage consumer lending, the call on both private bank and consumer staple stocks is contingent on consumer financial health. The loan book of private banks has expanded tremendously: since 2010 it has grown at a compounded annual growth rate (CAGR) of 20% and 14% in nominal and real (inflation-adjusted) terms, respectively (Chart II-3).3 In turn, the share of household loans is reasonably large at around 52% of private banks total loan book. Unfortunately, India’s consumer sector appears to be fragile at the moment. Employment and wage growth have downshifted – the Manpower employment index is at a 14-year low (Chart II-4). Consequently, household disposable income growth has decelerated to 9% in nominal terms (Chart II-5). Critically, households’ ability to service debt has deteriorated as nominal disposable household income growth has fallen slightly below borrowing costs, i.e., bank lending rates (Chart II-5). This development is precarious not only because it makes it more difficult for consumers to service their debt – causing NPLs to rise – but it also dampens consumer credit demand. Consequently, private banks’ considerable exposure to consumers could reverse the fortunes of the former as consumers face increasing difficulties servicing their debt. Moreover, with borrowing costs above nominal income growth, banks in India could face adverse selection problem. The latter is a phenomenon when loan demand primarily comes from riskier borrowers who are in desperate need for funding. In such a case, non-performing loans are bound to mushroom. Chart II-4India's Labor Market Is In Doldrums

India's Labor Market Is In Doldrums

India's Labor Market Is In Doldrums

Chart II-5India: Household Nominal Income And Lending Rate

India: Household Nominal Income And Lending Rate

India: Household Nominal Income And Lending Rate

Overall, household spending is in the doldrums. Two- and three-wheeler and passenger car unit sales have all been contracting. In the meantime, consumer demand for non-durable goods has also weakened, as reflected by stalling non-durable consumer goods production. Residential property demand has plummeted. According to the Reserve Bank of India’s December Financial Stability Report – quoting data from PropTiger DataLabs – housing sales units contracted by 20% in September from a year ago. In turn, growth in house prices has been anemic (Chart II-6). Prices are now growing below core inflation, i.e. property prices are deflating in real terms. Households’ ability to service debt has deteriorated as nominal disposable household income growth has fallen slightly below borrowing costs. Going forward, odds are that employment and wage growth will remain weak in India. The basis is the corporate sector is also struggling and still reluctant to invest and hire. Chart II-7 illustrates that the number of investment projects has collapsed, while capital goods production and capital goods imports are both shrinking (Chart II-7). Chart II-6India: Housing Market Is Feeble

India: Housing Market Is Feeble

India: Housing Market Is Feeble

Chart II-7India: Companies Are Not Investing

India: Companies Are Not Investing

India: Companies Are Not Investing

Overall, the entire Indian economy is suffering from high borrowing costs in real (adjusted for inflation) terms (Chart II-8, top panel). Chart II-8Lending Rates Have Not Declined Despite Monetary Easing

Lending Rates Have Not Declined Despite Monetary Easing

Lending Rates Have Not Declined Despite Monetary Easing

Importantly, the monetary policy transmission mechanism has not been working effectively in India. Even though the central bank has cut its policy rate by 135 basis points in 2019, prime borrowing did not budge (Chart II-8, middle panel). Consequently, loan growth has decelerated sharply (Chart II-8, bottom panel). On the whole, for the economy to recover, it requires considerably lower borrowing costs or a substantial fiscal boost. Indian central and state fiscal aggregate budget deficit is already wide at 6% of GDP. With public debt-to-GDP ratio at 68%, there is some but not enormous room for boosting government expenditures drastically. This makes reducing commercial bank lending rates the most feasible mechanism to jump-start the economy. Consequently, the authorities will become more aggressive in forcing commercial banks to cut their lending rates. This seems to be taking place as in September 2019 the RBI asked Indian commercial banks to link lending rates on certain types of loans more closely to the central bank’s policy rate to ensure more effective monetary policy transmission. Yet doing so will squeeze down commercial banks’ net interest rate margins – which have widened – and will hit banks’ profits. Alternatively, if lending rates do not fall, non-performing loans (NPLs) will increase because only risky borrowers will be willing to borrow while existing debtors will struggle to service their debt at current elevated interest rates. This will also depress bank profits. These two negative scenarios are probably reflected in low valuations of public bank share prices, but they are not yet priced in among private banks stocks. Given the latter’s exuberant valuations, only a small drop in net interest rate margins or a small rise in NPLs, will be enough to drag their share prices lower. Investment Conclusions Chart II-9India Vs. EM Relative Equity Performance Is Often About Oil

India Vs. EM Relative Equity Performance Is Often About Oil

India Vs. EM Relative Equity Performance Is Often About Oil

Travails of the Indian economy will persist for now. Much more policy support is required to turn the business cycle around. EM equity investors should keep a neutral allocation to Indian stocks within an EM equity portfolio. Indian share prices often outperform their EM peers when oil prices drop and lag when crude prices rally (Chart II-9). Given our negative view on oil prices,4 we are reluctant to downgrade this bourse to underweight. Private banks are susceptible to a drawdown as either their net interest rate margins will drop or they will face rising non-performing loans. Consumer staples stocks are expensive and, hence, are vulnerable to marginal profit disappointments. We are upgrading our allocation to Indian domestic bonds from neutral to overweight within an EM local bond portfolio. Consistently, we are closing our yield curve steepening trade in India. This position has produced a 30 basis points gain since July 2016. Low inflation, weak real growth, a struggling credit system and ineffective transmission of monetary easing argue for even lower interest rates in India. The surge in food prices should be viewed as a relative price shock, not inflation. Higher food prices will curb the spending power of consumers and weaken their expenditures on non-food items. In addition, core inflation remains very low. Ayman Kawtharani Editor/Strategist ayman@bcaresearch.com Footnotes 1 Please click on the link to access EM: Perception versus Reality report. 2 Commercial banks’ reserves at central banks do not constitute and are not a part of narrow or broad money supply. 3 The calculation is based on the annual reports of four large Indian private banks: HDFC Bank, ICICI Bank, Kotak Mahindra Bank, and Axis Bank. 4 This is the Emerging Markets Strategy team’s view and it differs for BCA’s house view on oil. Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights The bank credit 6-month impulse is likely to drop sharply in Europe, drop modestly in the US, but remain positive in China. Hence, the momentum of first-half economic data is likely to be worse in Europe than in China – albeit the Wuhan coronavirus scare is an unknown risk to this view. Initiate long CNY/GBP on a 6-month horizon. Underweight banks and the cyclical-heavy Eurostoxx 50 versus other markets, again on a 6-month horizon. There will be a better time to enter these positions later in the year when 6-month impulses are improving. Long-term investors seeking value in Europe should focus on the main currencies and not on the main equity indexes. Fractal trade: long EUR/GBP. Europe And China Play A Role-Reversal In recent dispatches we have highlighted that the euro area bond yield 6-month impulse stands near +100 bps, posing the strongest headwind to growth for three years. To make matters worse, the impulse has flipped from a strong -100 bps tailwind last summer into the current strong headwind, equating to a marked deterioration in the weather. But in China, it is the opposite story. Last summer, the China bond yield 6-month impulse constituted a strong +80 bps headwind; today the headwind has disappeared. Indeed, it has morphed into a tailwind, albeit a very mild tailwind at just -10 bps. In this sense, Europe and China are now playing a role-reversal. The momentum of first-half economic data is likely to be worse in Europe than in China – albeit with the caveat that the Wuhan coronavirus scare is an unknown risk to this view (Chart of the Week). Chart of the WeekBond Yields In Europe And China Play A Role-Reversal

Bond Yields In Europe And China Play A Role-Reversal

Bond Yields In Europe And China Play A Role-Reversal

For the sake of completeness, we should address the world’s other large economy, the United States. Just as in the euro area, the US bond yield 6-month impulse has flipped from a strong -100 bps tailwind last summer into a current headwind. But the headwind, at +50 bps, is not as strong as it is in the euro area (Chart I-2). Chart I-2Headwind Impulses In The Euro Area And The US, But Not In China

Headwind Impulses In The Euro Area And The US, But Not In China

Headwind Impulses In The Euro Area And The US, But Not In China

The Four Impulse Framework For Short-Term Growth The bond yield 6-month impulse is the first component of our proprietary ‘four impulse framework’ for short-term growth. The bond yield 6-month impulse is important because it usually leads the framework’s second component, the bank credit 6-month impulse, by a few months. This relationship makes perfect sense as, at the margin, it is the price of credit that drives credit demand. Indeed, to the extent that monetary policy drives growth, this is the main mechanism by which it operates, albeit with a slight delay. The bond yield impulse usually leads the credit impulse. On this compelling theoretical and empirical evidence, the bank credit impulse is now likely to drop sharply in the euro area (Chart I-3), drop modestly in the US (Chart I-4), but remain positive in China (Chart I-5). Chart I-3The Credit 6-Month Impulse Is Likely To Drop Sharply In The Euro Area...

The Credit 6-Month Impulse Is Likely To Drop Sharply In The Euro Area...

The Credit 6-Month Impulse Is Likely To Drop Sharply In The Euro Area...

Chart I-4...Drop Modestly In ##br##The US...

...Drop Modestly In The US...

...Drop Modestly In The US...

Chart I-5...But Remain Positive In China

...But Remain Positive In China

...But Remain Positive In China

But we must also consider the other two impulses in our four impulse framework. In the case of the euro area, the third important impulse is the oil price 6-month impulse. This is because the euro area relies on oil imports whose volumes tend to be price inelastic. Hence, when the oil price falls it subtracts from imports, thereby adding to net exports and growth – and vice-versa when the oil price rises. In the middle of 2019, the oil price impulse constituted a very strong headwind which helps to explain the midyear sharp slowdown in Germany. Subsequently, the headwind eased, even reversing into a modest tailwind which facilitated a recovery. But the tailwind is now fading (Chart I-6). Chart I-6A Fading Tailwind From The Oil Price 6-Month Impulse

A Fading Tailwind From The Oil Price 6-Month Impulse

A Fading Tailwind From The Oil Price 6-Month Impulse

The fourth and final component of our four impulse framework is geopolitical risk. This is not an impulse in the strict mathematical sense, but it is the same broad idea applied to the flow of geopolitical tail-events, both negative and positive. Europe’s positive events came several months ago: first in early-August when Italy ousted the firebrand Matteo Salvini from government; then in early-October when the UK parliament legislated against a no-deal Halloween Brexit. The tailwind from these positive events has now likely faded. For China, a positive geopolitical event and potential mild tailwind has come more recently, with the signing of the phase one trade deal with the US. Against this, the Wuhan coronavirus scare is a new risk – though based on the latest information it is unlikely to impact a 6-month view. The tailwind from the oil price impulse is now fading. On the four impulse framework, the momentum of first-half economic data is likely to favour China over Europe. We have found that the best way of playing this is through the exchange rate (Chart I-7), though given recent moves our preferred expression is versus the pound rather than the euro. Hence, on a 6-month horizon, initiate long CNY/GBP. Chart I-7Play Relative Impulses Through Currencies

Play Relative Impulses Through Currencies

Play Relative Impulses Through Currencies

More generally, can the mild tailwind in China counter the headwinds in the West? No. Despite the improvement in China, the aggregate global bond yield impulse still constitutes a +50 bps headwind, which is almost certain to weigh down the global credit impulse through the early months of 2020 (Chart I-8). Chart I-8The Global Credit 6-Month Impulse Will Weaken In Early 2020

The Global Credit 6-Month Impulse Will Weaken In Early 2020

The Global Credit 6-Month Impulse Will Weaken In Early 2020

Therefore, as discussed last week in Strong Headwind Warrants Caution In H1, we recommend an underweight stance to banks and to the cyclical-heavy Eurostoxx 50 versus other markets, again on a 6-month horizon. This is not to say that these positions cannot do better on a 12-month view, as per the BCA house view. But if so, any outperformance will be back-end loaded, and there will be a better time to enter these positions later in the year when 6-month impulses are improving. Where Is The Value In Europe? One of the most common questions we get is: are European equities cheaper than US equities? Usually, this question comes from our US clients who are aware that their own stock market is expensive and wish that Europe might be less so. Unfortunately, the wishful thinking won’t make it come true! Major stock market indexes comprise multinational companies with global footprints. For these multinationals, there is no such thing as a ‘European’ company or a ‘US’ company. They are simply global companies that could list their shares on any major stock market. Now ask yourself this: is it really plausible that such a multinational would be cheaper if its primary listing was in Frankfurt as opposed to New York? Of course not. The valuation depends on the industry and company specifics, but it is highly unlikely to depend on whether the company is listed in Frankfurt or New York. It is not European equities that are cheap, it is European currencies that are cheap. But then why do companies with dual listings in Europe and outside Europe trade at a valuation discount in their European listing? For example, Carnival Cruises trades around 8 percent dearer in New York than in London (Chart I-9); and BHP Billiton trades around 15 percent dearer in Sydney than in London (Chart I-10). The answer is that the London listing is quoted in pounds, the New York listing is quoted in US dollars, the Sydney listing is quoted in Australian dollars, but Carnival’s and BHP’s sales and profits are denominated in a mix of international currencies. Chart I-9Carnival Cruises Trades Dearer In New York Than In London

Carnival Cruises Trades Dearer In New York Than In London

Carnival Cruises Trades Dearer In New York Than In London

Chart I-10BHP Trades Dearer In Sydney ##br##Than In London

BHP Trades Dearer In Sydney Than In London

BHP Trades Dearer In Sydney Than In London

Hence, Carnival and BHP are trading dearer in New York and Sydney because the market is expecting their mixed currency earnings to appreciate more in US dollar and Australian dollar terms respectively than in pound terms. Put another way, the market is expecting the pound to appreciate structurally versus the major non-European currencies. Therein lies the important message. It is not European equities that are cheap, it is European currencies that are cheap. For those of you still in doubt, just visit the ECB website. The central bank’s own currency valuation indicator admits that the trade-weighted euro is 10 percent undervalued (Chart I-11). Chart I-11The ECB Admits That The Euro Is 10 Percent Undervalued

The ECB Admits That The Euro Is 10 Percent Undervalued

The ECB Admits That The Euro Is 10 Percent Undervalued

Hence, investors seeking value in Europe should not focus on the main equity indexes. Instead, they should focus on the main currencies. That said, valuation based investing only works if you have a long enough time horizon, meaning at least two years. For shorter horizons, economic momentum and technical factors dominate. In this regard, the pound’s strong rally faces resistance once post-Brexit trade deal negotiations begin in earnest after January 31. As a tactical trade, go long EUR/GBP (see next section). Fractal Trading System* The Brexit deal unleashed a strong rally in the pound, but this is vulnerable to a countertrend setback once the trade deal negotiations begin in earnest. Accordingly, this week's recommendation is long EUR/GBP. Set a profit target at 2 percent with a symmetrical stop-loss. In other trades, long tin achieved its 5 percent profit target at which it was closed. The rolling 1-year win ratio stands at 62 percent. Chart I-12EUR/GBP

EUR/GBP

EUR/GBP

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Cyclical Recommendations Structural Recommendations

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Europe And China Play A Role-Reversal

Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

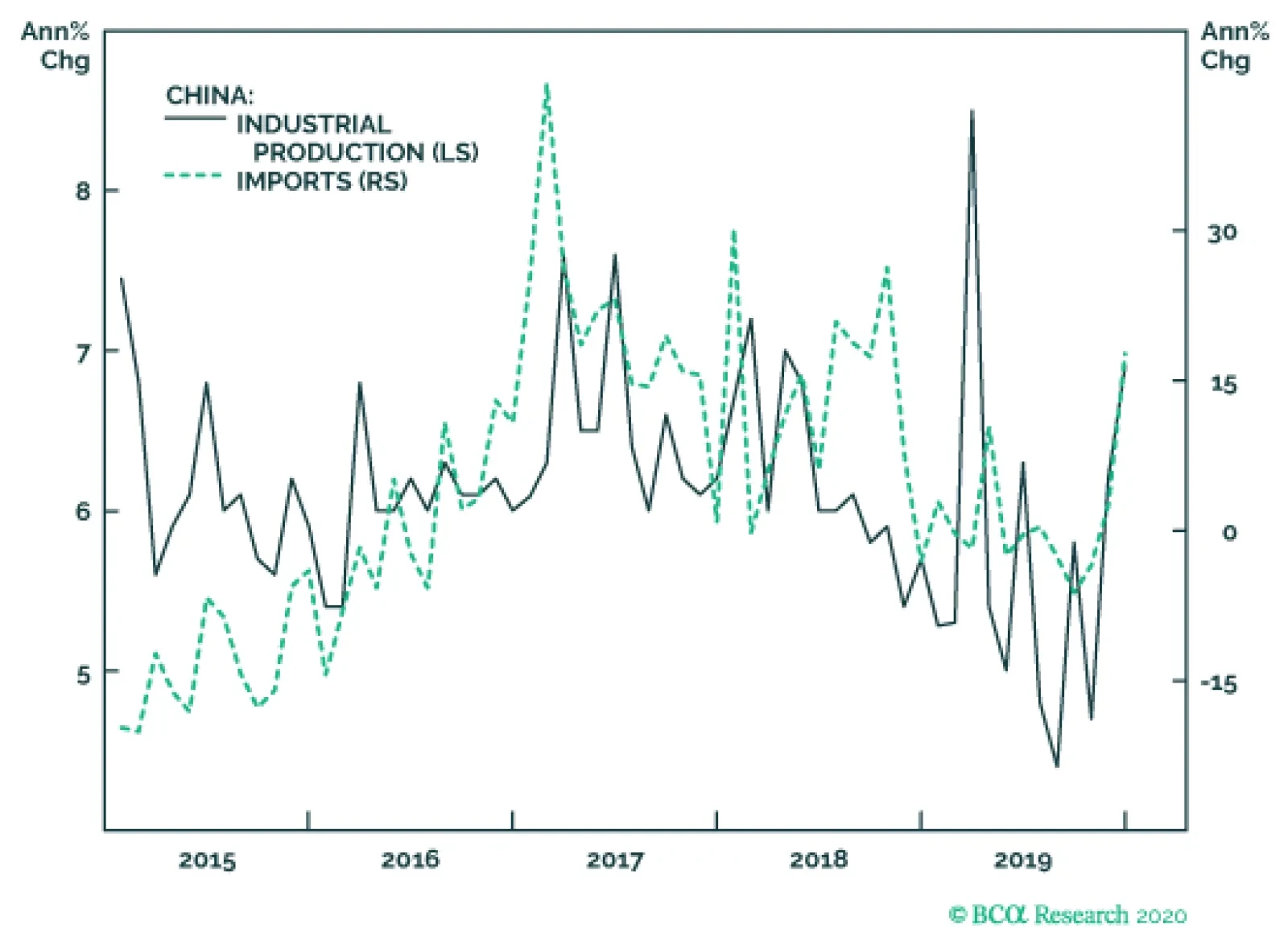

Highlights The recently signed Phase One deal is positive for China and global equity markets as it brings a temporary truce to the trade war. However, China is unlikely to change its current policy trajectory to create additional domestic demand to consume $200 billion in new imports from the US. China is likely to meet the commitment only half way in the next two years, and meet the 2020 import target from the US by a redistribution of its purchases overseas. The RMB will modestly appreciate in the next three to six months. On the monetary policy front, there is no sign of further monetary easing from the PBoC. We continue to recommend an overweight stance towards Chinese stocks in the next six months, relative to the global benchmark. Feature Economic data released last week, including Q4 GDP growth, December industrial production, fixed-asset investment and trade data, all suggest that the Chinese economy bottomed before the end of 2019. The Phase One trade deal between China and the US marks a significant de-escalation in a two-year trade war. The RMB appreciated by 1.4% against the greenback since the beginning of the year, pushing USD-CNY firmly below the key psychological 7 mark. The performance of equities in China’s onshore and offshore markets confirms that the economy has bottomed. Since December 11, 2019, Chinese cyclical sectors have outperformed defensives and both the investable and domestic markets have broken above their respective 200-day moving averages versus global stocks (Chart 1A and 1B). Chart 1ABoth Onshore And Offshore Equities Signal A Bottoming In China's Economy

Both Onshore And Offshore Equities Signal A Bottoming In China's Economy

Both Onshore And Offshore Equities Signal A Bottoming In China's Economy

Chart 1BCyclicals Have Significantly Outperformed Defensives Lately

Cyclicals Have Significantly Outperformed Defensives Lately

Cyclicals Have Significantly Outperformed Defensives Lately

We continue to recommend a cyclical long stance on Chinese stocks. We expect pro-growth policy support to accelerate in the first quarter, economic recovery to further solidify, and the Phase One trade deal to reduce economic and financial market volatility until the November 2020 US presidential election. All of these factors should support an outperformance in Chinese stocks relative to their global peers. Some Inconvenient Truth To The Truce China’s commitment to purchase an additional $200 billion in goods from the US was more than market participants anticipated. We do not think China will honor this commitment to its full extent. Moreover, we also do not think this will change China’s domestic economic policy trajectory for 2020. Details in Chapter 6 of the Phase One trade agreement titled “Expanding Trade”1 include: In the next 2 years, China is committed to purchase an additional $200 billion worth of goods and services from the US, from the 2017 baseline. The additional $200 billion amount is split over the next two years: China will need to add no less than $77 billion of imports from the US in 2020, and $123 billion in 2021. This amounts to a 41% increase in 2020 and a 66% increase in 2021, from the 2017 baseline of $186 billion (Chart 2). The text from Chapter 6 of the Phase One deal also specifies that, between January 2020 and December 2021, China will add a total of $77.7 billion in purchases of manufactured goods (including aircraft components), $32 billion in agricultural products, $52.4 billion in energy and $37.9 billion in services from the US (Chart 3). Chart 2Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Chart 3Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

China’s annual import growth from the US in 2017 was the highest one in the past ten years. If we assume that China will simply add $200 billion of new imports in the next two years from the US to this high starting point, it will need to boost domestic demand to accommodate at least a 4-6% increase in total imports in the next two years from 2019.2 In contrast, growth in China’s total imports in 2019 contracted by 3% from 2018, and averaged at only 2% in the last five years. In other words, in 2020 and 2021, even if China does not increase imports from other countries, just the commitment from purchases of US goods alone would require a sizable boost in China’s domestic demand. However, the assumption above is overly simplified and optimistic. Even though Chinese leadership may have shifted their policy priority from financial deleveraging to supporting economic growth this year, we do not think they will fully abandon the battle against systemic risks in the financial sector. Therefore, China is unlikely to significantly deviate from its current policy trajectory and stimulate aggressively to create additional domestic demand to consume the agreed $200 billion in new imports from the US. It is equally unlikely that China will absorb the $200 billion additional imports from the US, at the expense of its domestic production. A more plausible approach, which is our base case scenario, is that China will meet a large portion of the 2020 import target before November, to show good faith. After the US presidential election, China will face the challenge of either a re-escalation from the Phase Two trade talk with a re-elected President Trump, or a new US president with his/her own political agenda. In either case, at this point China is unlikely to have the intention to meet the import target for 2021. Chart 4China Likely To Shift Agro And Energy Import Suppliers To The US

Managing Expectations

Managing Expectations

In 2020, to absorb a $77 billion additional imports from the US, China will likely shift some of its imports, such as agriculture and energy products, from other countries to suppliers in the US. China currently imports $150 billion of agriculture goods and $298 billion of energy related products on an annual basis, so the pie is large enough to absorb some of increased import commitments by shifting the sources of imports (Chart 4). The same logic goes for the manufactured goods category in the trade agreement, which includes cars, airplanes, steel, industrial machinery, and so on.3 China is likely to choose to shift its import suppliers of these goods to the US, while increasing its own share of intermediate goods supplies to the US manufacturers. Almost all of the eight subcategories under the manufactured goods category in the Phase One trade agreement are deeply integrated in the global supply chain. For example, foreign value-added share accounts for 23% of the total output value of the US automobile industry.4 In other words, if a “Made in America” car is worth $20,000, $4,600 is produced by foreign suppliers of intermediate goods. Since China has been the leading source of this foreign value-added in the US automobile industry, a sizeable slice of these additional imports will likely benefit Chinese manufacturers. In this scenario, we expect an increase in bilateral trade between China and the US in 2020, at the expense of other players in the global supply chain. Lastly, while this is not our base case scenario, it is possible the Phase One trade agreement was set up for failure, if China is simply hoping to delay the imposition of additional tariffs as part of a gamble that President Trump will not be re-elected. In this scenario, China might not make any meaningful additional purchases from the US even in 2020 (while claiming that they will be made closer to the election), implying that bilateral trade between China and the US will only revert to its historical average this year, at best. Bottom Line: Chinese policymakers are unlikely willing to alter their existing policy trajectory when accommodating more imports of US goods. China will, at best, reshuffle its supply chain to absorb a portion of the commitment before November 2020. The RMB And Monetary Policy: A Refocus On The Economic Fundamentals As tensions from the US-China trade war abate, investors are starting to refocus on economic fundamentals. The RMB has appreciated by 1.4% against the USD since the beginning of this year (Chart 5). The recent appreciation in the currency is a reversal to its fair value, which reflects an ongoing economic recovery (Chart 6). In the next three to six months, the improvement in China’s economic fundamentals and market sentiment should support a continuation in the RMB’s reversal to its structural trend. Chart 5USD/CNY Has Durably Fallen Below 7

USD/CNY Has Durably Fallen Below 7

USD/CNY Has Durably Fallen Below 7

Chart 6The Recent Appreciation In RMB Is A Reversal To Its Fair Value

The Recent Appreciation In RMB Is A Reversal To Its Fair Value

The Recent Appreciation In RMB Is A Reversal To Its Fair Value

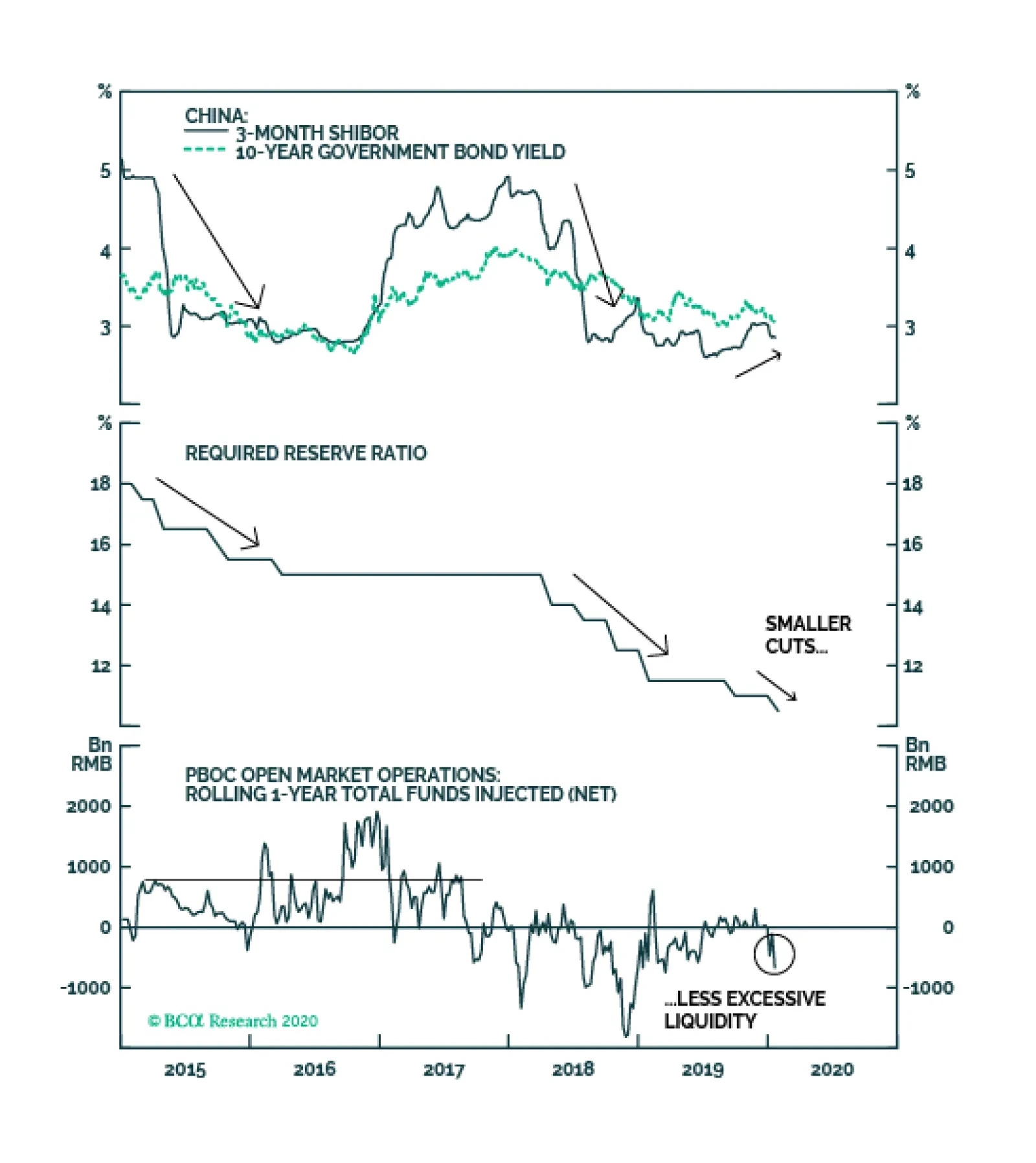

But Chinese leadership’s cautious approach to boosting domestic demand will also cap the upside potential in the RMB appreciation. We think Chinese policymakers will maintain their tight grip this year on local government spending and bank lending, and will continue to fine-tune policies based on economic conditions. This will limit the magnitude in both the stimulus and economic recovery. Baring a major re-escalation in the trade war, the RMB should oscillate within a relatively narrow band through the third quarter of this year. For that reason, the PBoC is unlikely to intervene in the RMB exchange rate by significantly altering its monetary stance (Chart 7). The 3-month interbank lending rate, China’s de facto policy rate, remains low compared with the 2015-16 easing cycle. There is no sign that the PBoC will allow the rate to fall much more. The recent bank reserve requirement ratio (RRR) rate cut provides additional liquidity to the interbank system, but on a net basis liquidity does not seem excessive (Chart 8). Chart 7PBoC Unlikely To Alter Monetary Policy To Intervene RMB Exchange Rate This Year

PBoC Unlikely To Alter Monetary Policy To Intervene RMB Exchange Rate This Year

PBoC Unlikely To Alter Monetary Policy To Intervene RMB Exchange Rate This Year

Chart 8No Sign Of Meaningful Monetary Easing From PBoC

No Sign Of Meaningful Monetary Easing From PBoC

No Sign Of Meaningful Monetary Easing From PBoC

Historically, the 3-month interbank lending rate only falls significantly and durably when the PBoC places consecutive RRR rate cuts (in both 2015 and mid-2018) and/or keeps net fund injections positive through the open market for a prolonged period (such as in the 2015/16 easing cycle). Chart 8 suggests the current monetary environment does not indicate that such an extremely easy stance is in place, as PBoC net fund injections through the open market remain negative. Furthermore, neither the 3-month interbank lending rate nor the 10-year government bond yield has fallen below its most recent lows in the third quarter of last year. Bottom Line: While the current environment supports a stronger RMB, the upside potential in RMB appreciation is capped by a modest scale of economic recovery. There is no sign that the PBoC is easing its monetary stance by lowering the policy rate. Investment Conclusions We have been cyclically overweight Chinese stocks on the basis of a bottoming in the economy in the first quarter of 2020, and the likelihood of an eventual trade deal. These two factors were confirmed in the past two weeks. Last week’s small selloffs in both onshore and offshore Chinese equity markets were likely technical corrections and pre-Chinese New Year profit taking, rather than a fundamental shift in investors’ sentiment towards Chinese stocks (Chart 9). We expect Chinese stocks to resume an upward trajectory after the Chinese New Year. Chart 9Small Corrections Following A 14% Gain Since Dec 2019

Small Corrections Following A 14% Gain Since Dec 2019

Small Corrections Following A 14% Gain Since Dec 2019

Chart 10Offshore Stocks Still Showing More Upside Potential Than Onshore

Offshore Stocks Still Showing More Upside Potential Than Onshore

Offshore Stocks Still Showing More Upside Potential Than Onshore

China’s economic conditions and corporate earnings should continue to improve, with investable stocks showing more upside potential than their domestic counterparts (Chart 10). As growth supporting measures continue to work their way through the economy and solidify an economic recovery, China’s leadership may pull back the scale of the stimulus in the second half of the year. Therefore, the relative outperformance in both markets may be front loaded and subsequently subside in the second half of 2020. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1 https://assets.bwbx.io/documents/users/iqjWHBFdfxIU/rVaHxDBUtdew/v0 2 China’s total imports of goods and services in 2019 was $2604 billion, including $168 billion imports from the US. If China was to fully meet the $200 billion target of additional imports from the US, assuming no change to imports from other countries in 2020 from 2019, China’s total imports would jump to $2699 billion in 2020 and $2745 billion in 2021. 3 The eight subcategories of Manufacturing Goods listed in the Annex 6.1 of the Phase One Trade agreement include: Industrial Machinery, Electrical Equipment and Machinery, Pharmaceutical Products, Aircraft, Vehicles, Optical and Medical Instruments, Iron and Steel, Other Manufactured Goods including solar-grade polysilicon and other organic and inorganic chemicals, hardwood lumber, integrated circuits (manufactured in US), and chemical products. 4 WIOD Data, 2016 release and OECD Input-Output Tables (IOTs), 2015 release. Cyclical Investment Stance Equity Sector Recommendations

While Chinese authorities are most likely targeting “around 6%” in 2020, the authorities may allow an undershoot in the 5.5%-5.9% range. They will argue that the GDP target for 2020 has already been met on a compound growth rate basis. They may see less need…

Highlights We continue to have a positive view on global equities over the next 12 months, but see heightened risks of a near-term correction. Despite dwindling spare capacity, government bond yields are still lower today than they were shortly after the financial crisis. Many investors argue that bond yields cannot rise much because asset values would plunge if yields rose sharply, while debt burdens would quickly become unsustainable. We disagree. We think there is greater scope for yields to rise than is widely believed. Investors should maintain below-benchmark duration in fixed-income portfolios, favoring inflation-linked over nominal bonds and positioning for steeper yield curves. Gold should also do well next year. As long as bond yields are rising in response to stronger growth, as will be the case for the next two years, equities will fare well. The stock market will buckle, however, once stagflation sets in around 2022. Stocks Need To Work Off Overbought Conditions Before Moving Higher Again In last week’s report, entitled “Time For A Breather,” we downgraded our tactical three-month view on global equities from overweight to neutral on the grounds that stocks had run up too hard, too fast. Net long positions in equity futures among asset managers and levered funds are now at levels that have historically preceded corrections (Chart 1). Chart 1Stocks Are At A Heightened Risk Of A Correction

Stocks Are At A Heightened Risk Of A Correction

Stocks Are At A Heightened Risk Of A Correction

Chart 2Breadth Is Quite Narrow

Breadth Is Quite Narrow

Breadth Is Quite Narrow

Chart 3The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

The rally has been lopsided, characterized by very narrow breadth. The top five stocks in the S&P 500 (Apple, Microsoft, Alphabet, Amazon, and Facebook) now comprise 18% of market cap, a higher share than in the late 1999/early 2000s (Chart 2). As my colleague, Anastasios Avgeriou, has pointed out, Apple’s $30 billion one day market cap gain on January 9th was greater than the market cap of the median stock in the S&P 500 index. Despite our near-term concerns, we continue to maintain a positive 12-month view on global equities. Easier financial conditions, a turn in the global inventory cycle, modestly looser fiscal policy in the UK and euro area, and re-upped fiscal/credit stimulus in China should all support global growth this year. Faster growth, in turn, will lift corporate earnings. The equity risk premium also remains quite high, particularly outside the US (Chart 3). A Fragile Trade Truce A de-escalation in the trade war should provide a further tailwind to equities. The “phase one” agreement signed on Wednesday features a commitment by China to purchase an additional $200 billion in US goods and services over the next two years relative to 2017 levels. In return, the US will halve tariffs, to 7.5%, on the $120 billion tranche in Chinese imports and suspend any further tariff hikes. No firm schedule exists to begin “phase two” talks, and at this point, it is quite likely that no negotiations will take place until after the US presidential election. Nevertheless, the tail risk of an out-of-control trade war has receded for the time being, which is positive for stocks. Better Chinese Trade Data Adding to growing optimism over the global economy and diminished trade tensions, Chinese trade data surprised on the upside this week. Exports rose 7.6% in December, well above the consensus estimate of 2.9%. Imports surged 16.3%, easily surpassing the consensus estimate of 9.6%. While base effects explain some of the improvement, the overall tone of the trade data is consistent with the strengthening Chinese PMIs and improvement in industrial production and retail sales (Chart 4). Chart 4Chinese Trade Data Is Improving

Chinese Trade Data Is Improving

Chinese Trade Data Is Improving

Chart 5Better News Out Of China Has Propelled The Yuan Higher Versus The US Dollar

Better News Out Of China Has Propelled The Yuan Higher Versus The US Dollar

Better News Out Of China Has Propelled The Yuan Higher Versus The US Dollar

Better news out of China has pushed the yuan to the strongest level against the US dollar since last summer (Chart 5). The Chinese currency is the most important driver of other EM currencies. If the yuan continues to strengthen, as we expect, EM assets – particularly EM stocks and local-currency bonds – should do well this year. How High Can Bond Yields (Realistically) Go? Despite rising over the past few months, global government bond yields are lower today than they were shortly after the financial crisis ended (Chart 6). The decline in yields has occurred alongside dwindling spare capacity. In most countries, the unemployment rate today is below 2007/08 lows (Chart 7). Many investors argue that bond yields cannot rise much from current levels because asset values would plunge if yields rose sharply, while debt burdens would quickly become unsustainable. If such an unfortunate turn of events were to occur, central bankers would have to shelve any tightening plans, just as Jay Powell had to do in late 2018. Chart 6Bond Yields Are Lower Today Than They Were After The Great Recession

Bond Yields Are Lower Today Than They Were After The Great Recession

Bond Yields Are Lower Today Than They Were After The Great Recession

Chart 7Unemployment Rates Are Below Their Pre-Recession Lows In Most Economies

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

Convexity Fears One argument often heard these days is that asset prices have become hypersensitive to changes in interest rates. There is some basis for thinking this. As Box 1 explains, the relationship between asset returns and interest rates tends to be “convex,” meaning that any given change in interest rates will have a bigger effect on returns if rates are low to begin with, as they are today. The effect is particularly pronounced for long duration assets such as long-term bonds, equities, or real estate. Nevertheless, while the theoretical presence of convexity in asset returns is crystal clear, many commentators overstate its practical importance. As Chart 8 shows, the average maturity of government debt stands at seven years. At that level of maturity, the effects of convexity tend to be quite small.1 Chart 8Average Debt Maturity Is Below 10 Years In Most Countries

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

Granted, the overall stock of debt has increased in relation to GDP. However, much of that additional debt has been absorbed by central banks, reducing the amount of government debt available for the private sector. What about equities? The ratio of stock market capitalization-to-GDP has risen to 59%, up from a low of 24% in 2009, and close to its 2000 highs (Chart 9). Does that mean that stocks will sink if yields rise from current levels? Not necessarily. Remember that the discount rate is not the only thing that affects the present value of a stream of income. The expected growth rate of that income also matters. In fact, in the standard dividend discount model, it is simply the difference between the discount rate and the growth rate of dividends that determines how much a stock is worth. If higher bond yields coincide with rising growth expectations, stock prices do not need to fall at all. Chart 9Equity Market Cap Is Approaching Previous Highs

Equity Market Cap Is Approaching Previous Highs

Equity Market Cap Is Approaching Previous Highs

Chart 10 shows that the monthly correlation between equity returns and bond yields remains as high as ever. This suggests that favorable economic news, to the extent that it leads investors to revise up the expected growth rate for earnings, usually more than compensates for a rising discount rate (Chart 11). Chart 10Correlation Between Equity Returns And Bond Yields Remains High

Correlation Between Equity Returns And Bond Yields Remains High

Correlation Between Equity Returns And Bond Yields Remains High

Chart 11Earnings Estimates Tend To Move In Sync With Swings In Bond Yields

Earnings Estimates Tend To Move In Sync With Swings In Bond Yields

Earnings Estimates Tend To Move In Sync With Swings In Bond Yields

So why are so many investors worried that higher bond yields will undercut stocks? The answer has less to do with convexity and more to do with the fear that bond yields will reach a level that chokes off growth. The combination of a rising discount rate and a falling growth rate would be toxic for equities and other risk assets. Debt Worries Likewise, it is not so much that corporate bond investors are worried that rising yields will cause interest payments to swell. After all, interest costs are still quite low as a share of cash flows for most firms (Chart 12). Rather, the fear is that higher yields will imperil growth, causing those cash flows to evaporate. Government debt is also much less of a problem than often assumed, at least in countries that issue bonds in their own currencies. The standard rule for debt sustainability says that the debt-to-GDP ratio will always converge to a stable level if the interest rate is below the growth rate of the economy.2 This is easily the case in almost all economies today (Chart 13). Chart 12US Corporate Sector: Interest Payments Are Not A Worry

US Corporate Sector: Interest Payments Are Not A Worry

US Corporate Sector: Interest Payments Are Not A Worry

Chart 13Bond Yield Minus GDP Growth: Please Mind The Gap

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

The only places where central banks are severely constrained in raising rates are in economies such as Canada, Sweden, and Australia where debt-financed housing bubbles have formed (Chart 14). However, even in these countries, the quality of mortgage underwriting has generally been strong, implying that a banking crisis would likely be avoided. Chart 14Canada, Sweden, And Australia Stand Out As Having Very Frothy Housing Markets

Canada, Sweden, And Australia Stand Out As Having Very Frothy Housing Markets

Canada, Sweden, And Australia Stand Out As Having Very Frothy Housing Markets

It’s Really About The Neutral Rate The discussion above suggests that the main constraint to higher bond yields is the economy itself. If bond yields rise enough, the interest rate-sensitive sectors of the economy will weaken, and a recession will ensue. As long as bond yields are rising in response to stronger growth, as will be the case for the next two years, equities will be fine. Unfortunately, no one knows where the neutral rate – the interest rate demarcating the boundary between expansionary and contractionary monetary policy – really lies. Chart 15Rising Labor Share Of Income Occurring Alongside Labor Market Tightening

Rising Labor Share Of Income Occurring Alongside Labor Market Tightening

Rising Labor Share Of Income Occurring Alongside Labor Market Tightening