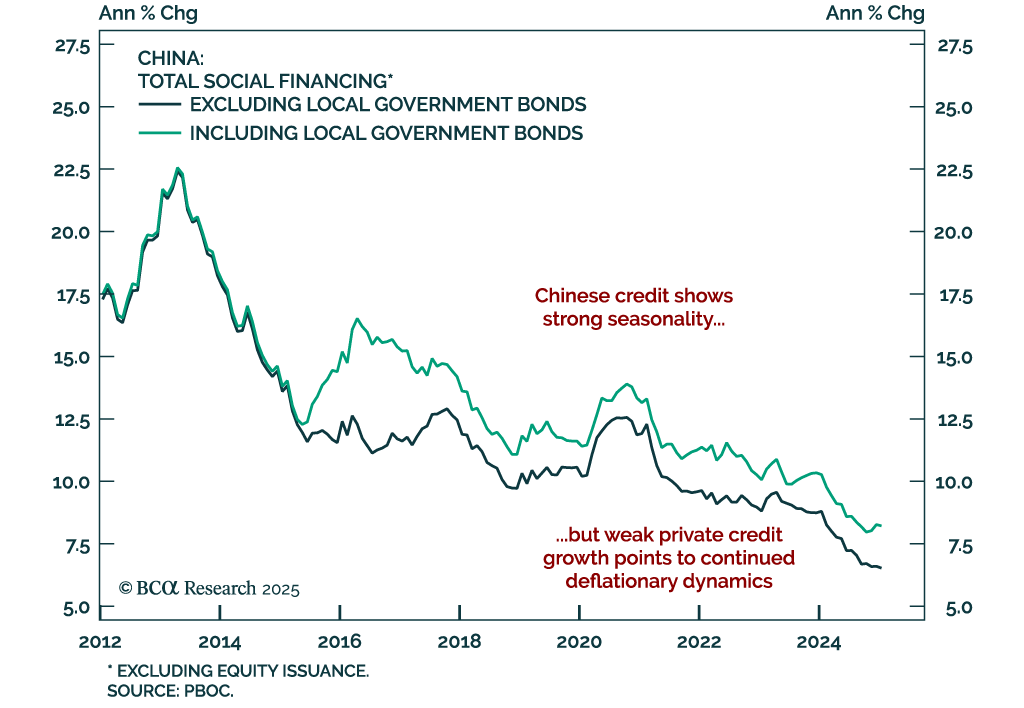

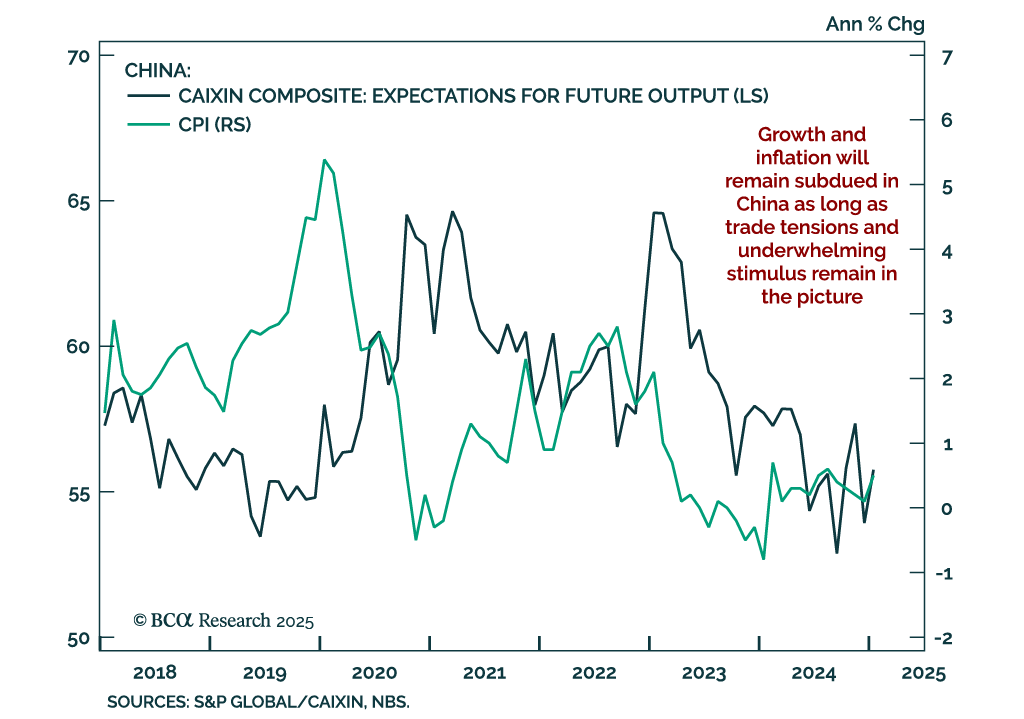

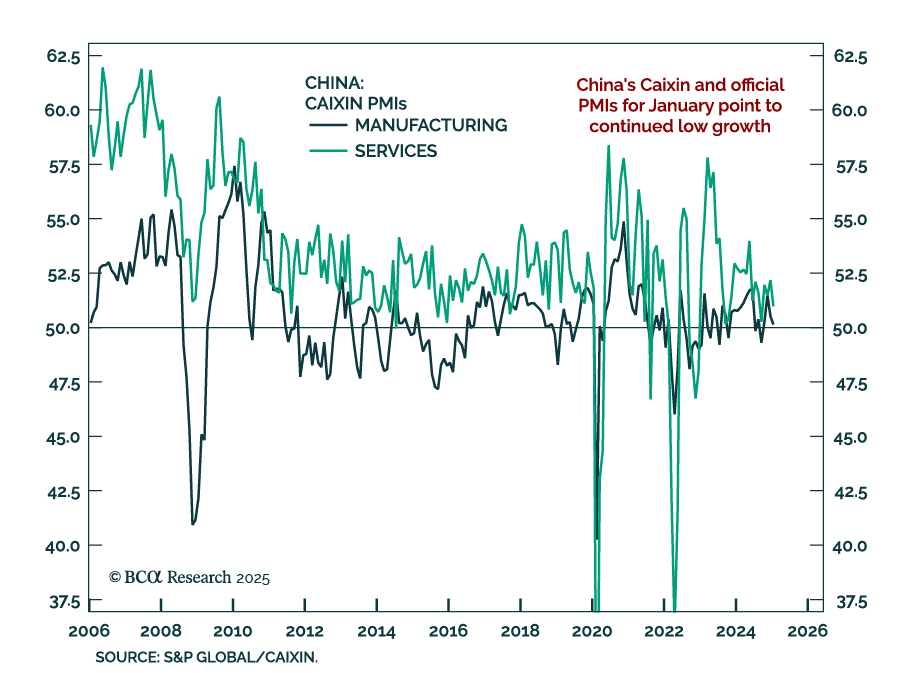

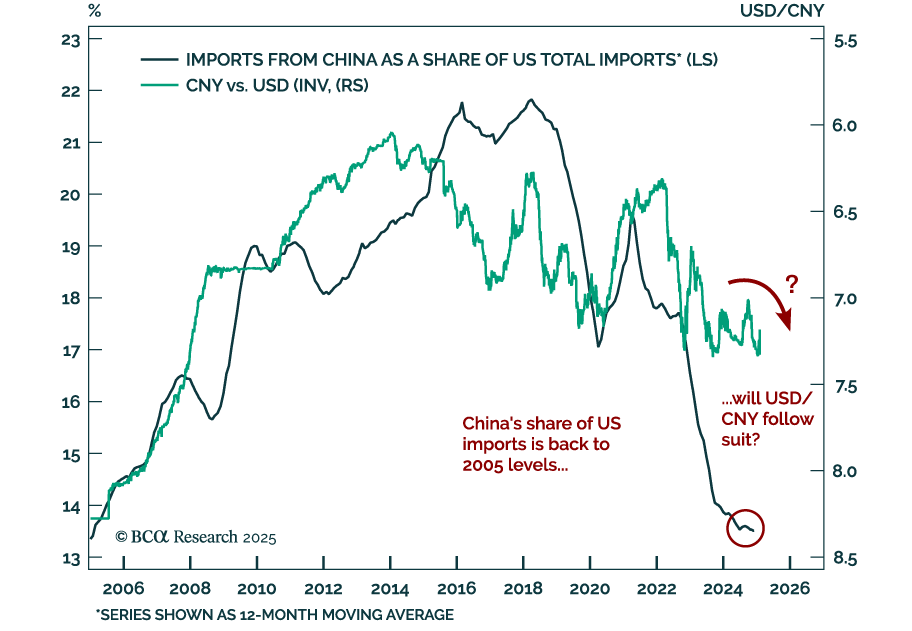

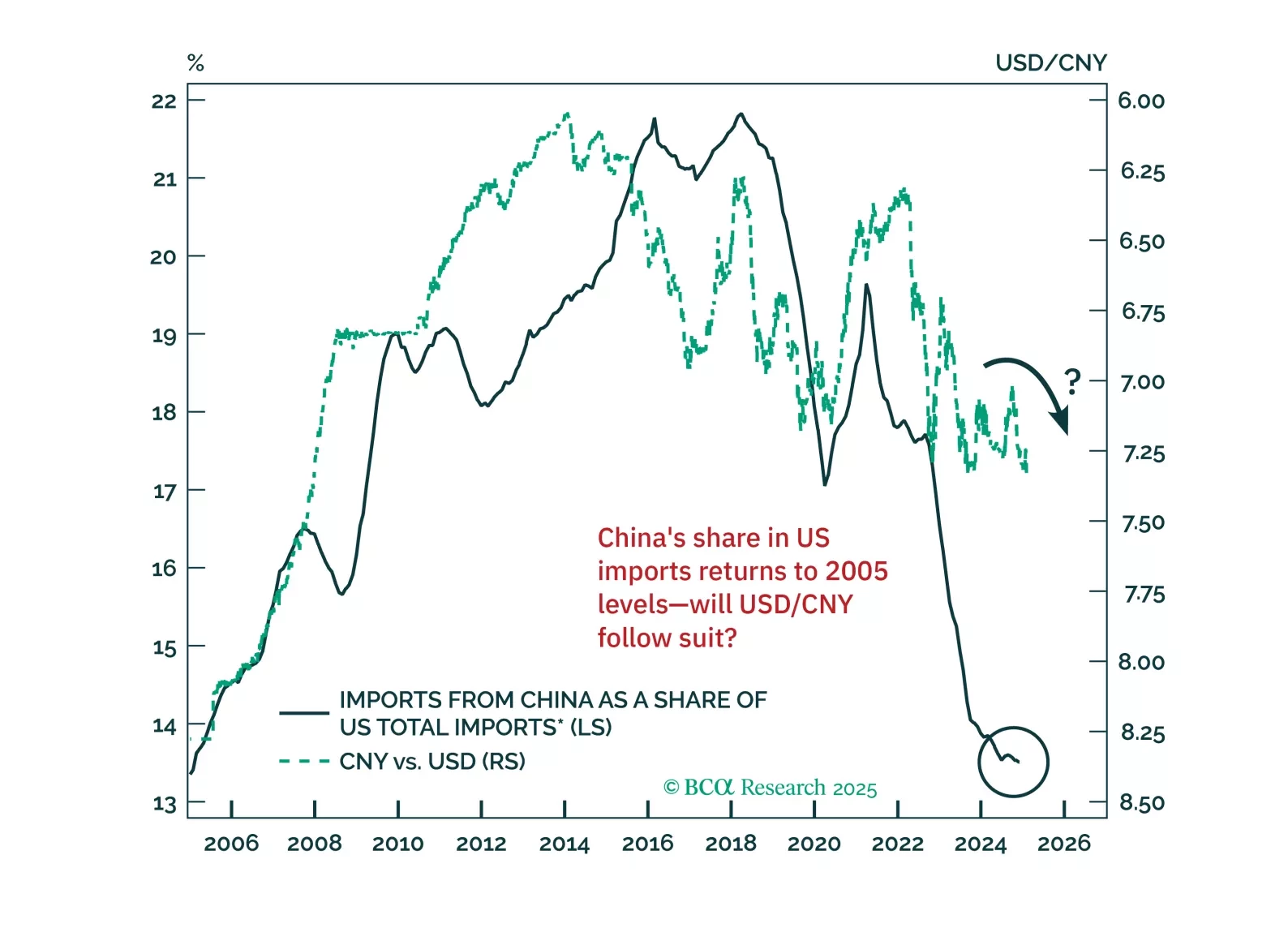

China

US growth has slowed in recent weeks. This can be seen in the weaker data on retail sales, consumer confidence, services PMIs, and a swath of housing releases (notably starts, existing home sales, homebuilder confidence, and stock prices). It can also be seen in the decline in GDP tracking estimates. The Atlanta Fed's GDPNow model projects growth of 2.3% in Q1, down from a peak of 3.9% on February 3. The Citi US Economic Surprise Index has also dipped into negative territory.

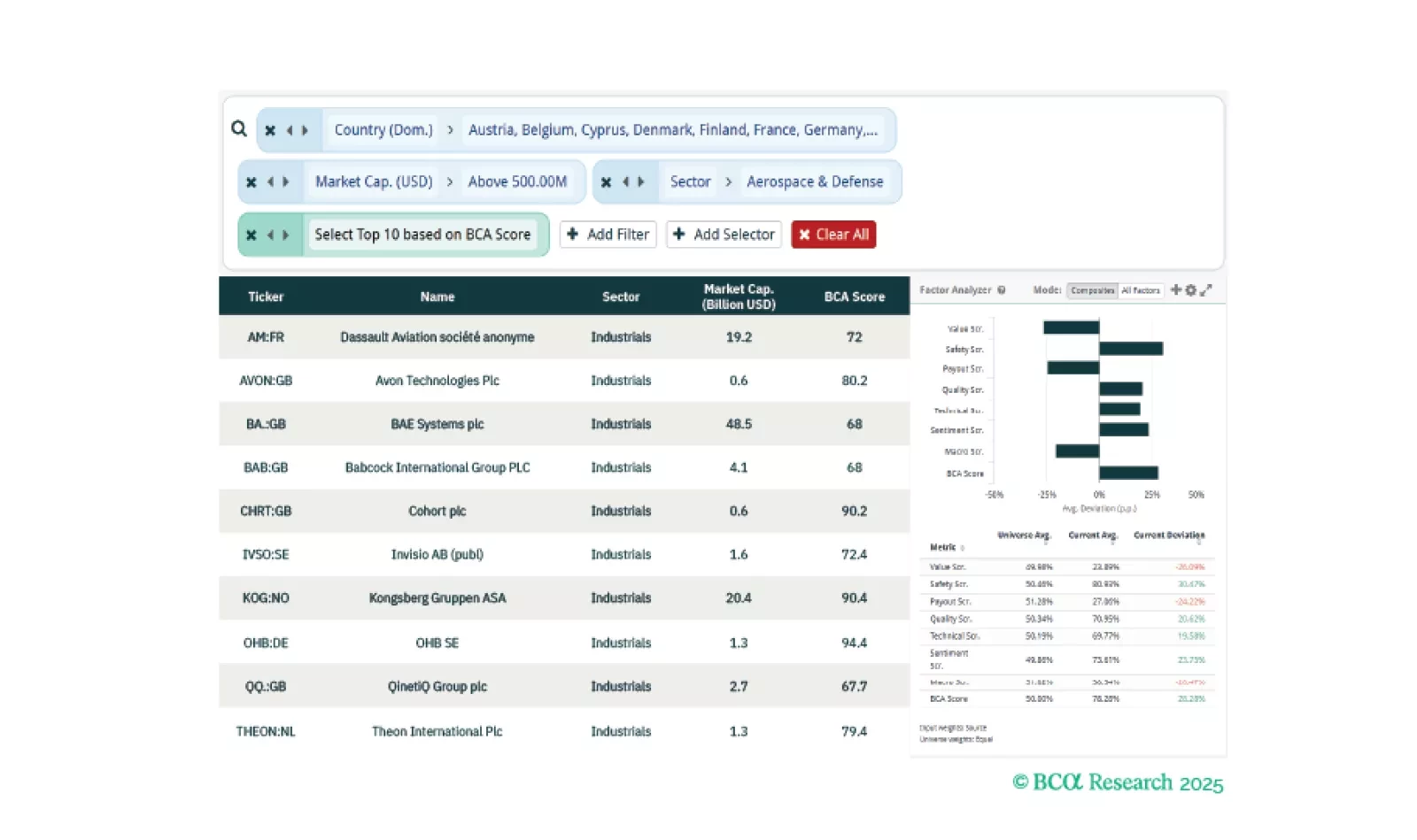

This week, our three screeners cover equity plays in European Defense, Chinese Tech, and “Boring Stocks”.

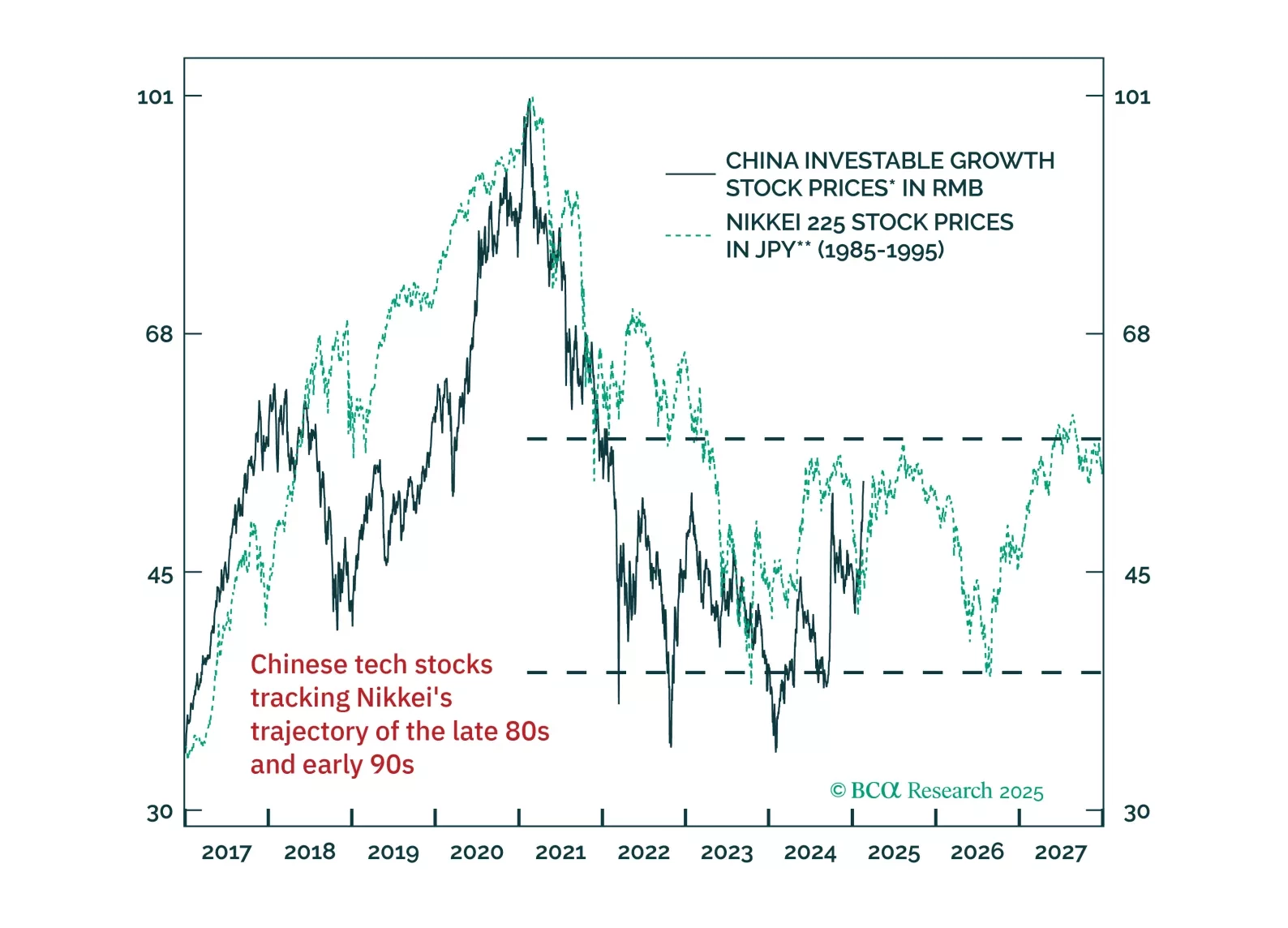

DeepSeek's AI breakthrough will likely enhance China’s productivity gains. But does it justify a re-valuation in Chinese tech stocks? Sustaining the Chinese tech rally will require corporate profits to overcome the pressures of China’s deflationary cycle. Meanwhile, DeepSeek’s innovations may fuel greater competition, intensifying price wars and putting further strain on Chinese tech companies’ profit margins.

In his latest Thoughts Of The Day, Peter Berezin discusses the different moving parts of the global economy today and the potential impact of Trump's policies.

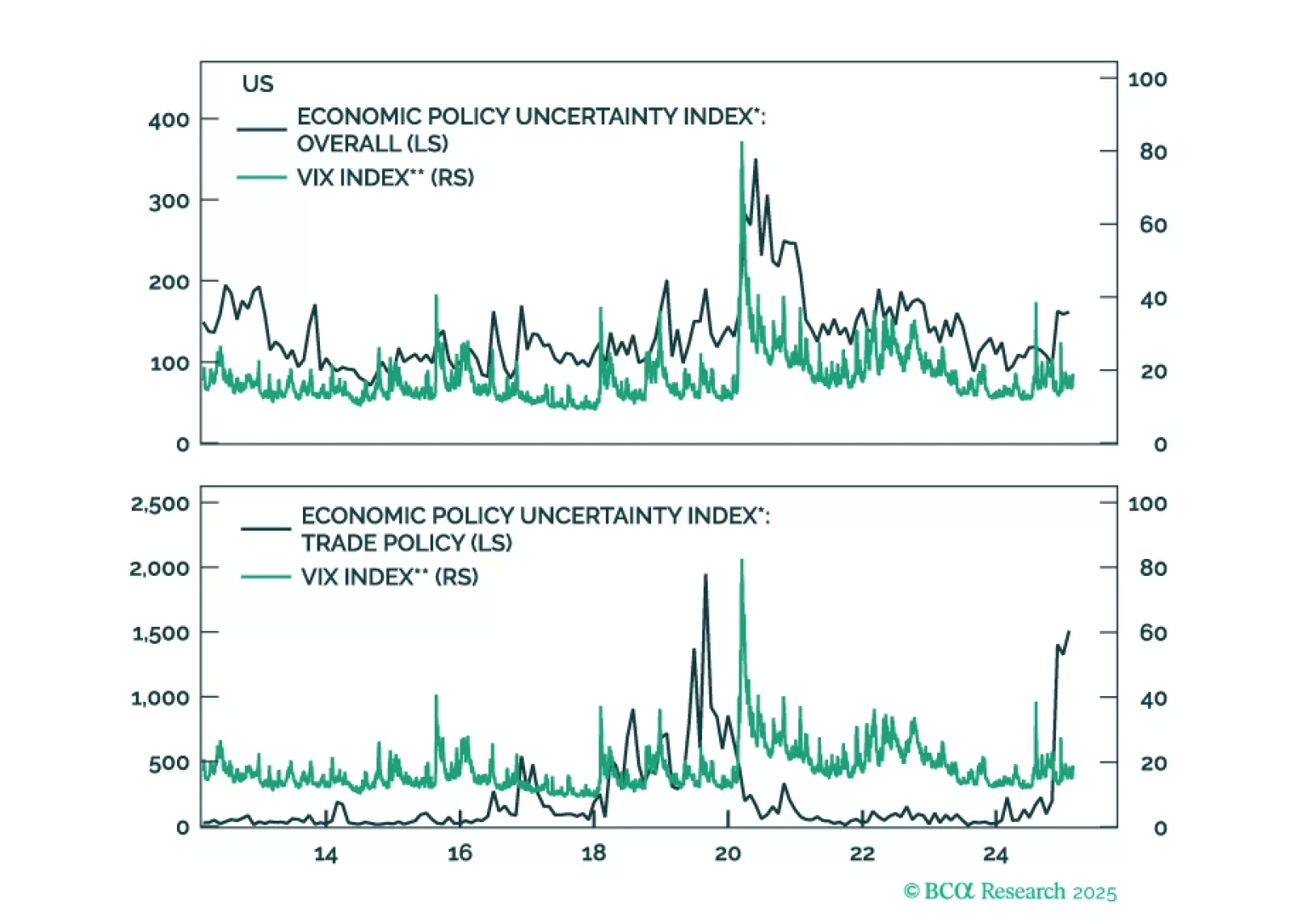

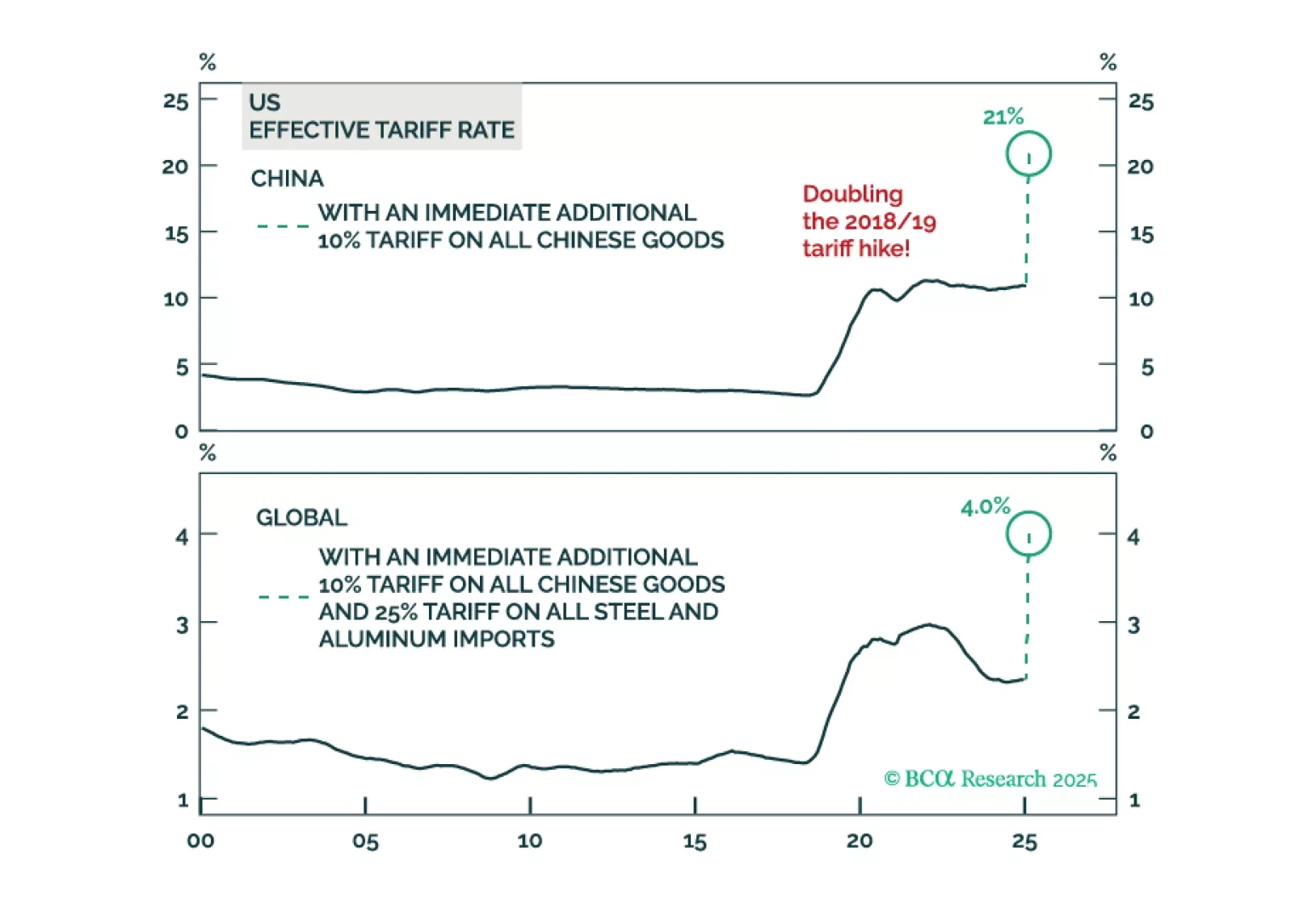

The 10% tariff hike announced on Saturday will likely serve as the opening salvo in a broader wave of protectionist measures. In this report, we assess the increase in US import tariffs on China. While the direct impact on China’s overall economy may be manageable, the country’s economy faces significant risks from potential disruptions in global trade.

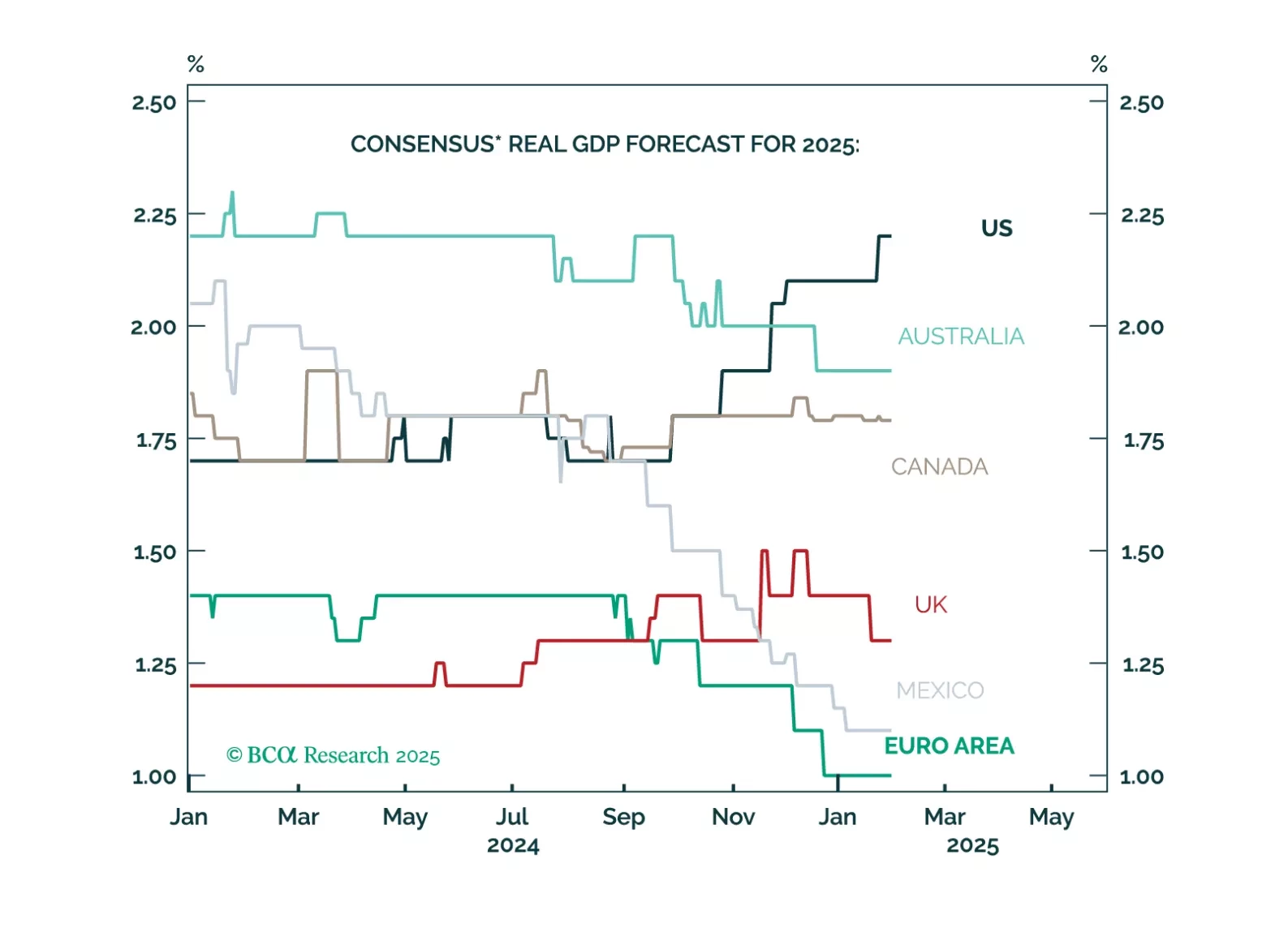

Markets and forecasters anticipate a “Golden Age” for Trump’s America, with US growth expectations soaring while the rest of the world lags. However, this extreme optimism means that there is a lot of room for disappointment. Cooling income growth, weak housing and less deficit spending than expected will result in US growth underperforming expectations. Maintain a modest underweight to equities and modest overweight to fixed income. US markets have become more expensive relative to the rest of the world even as quality differentials have stabilized. Prepare to downgrade US equities to underweight and to upgrade Euro Area and China to overweight. We will wait to pull the trigger until we have more clarity on trade policy and when the dollar's momentum turns negative.