China

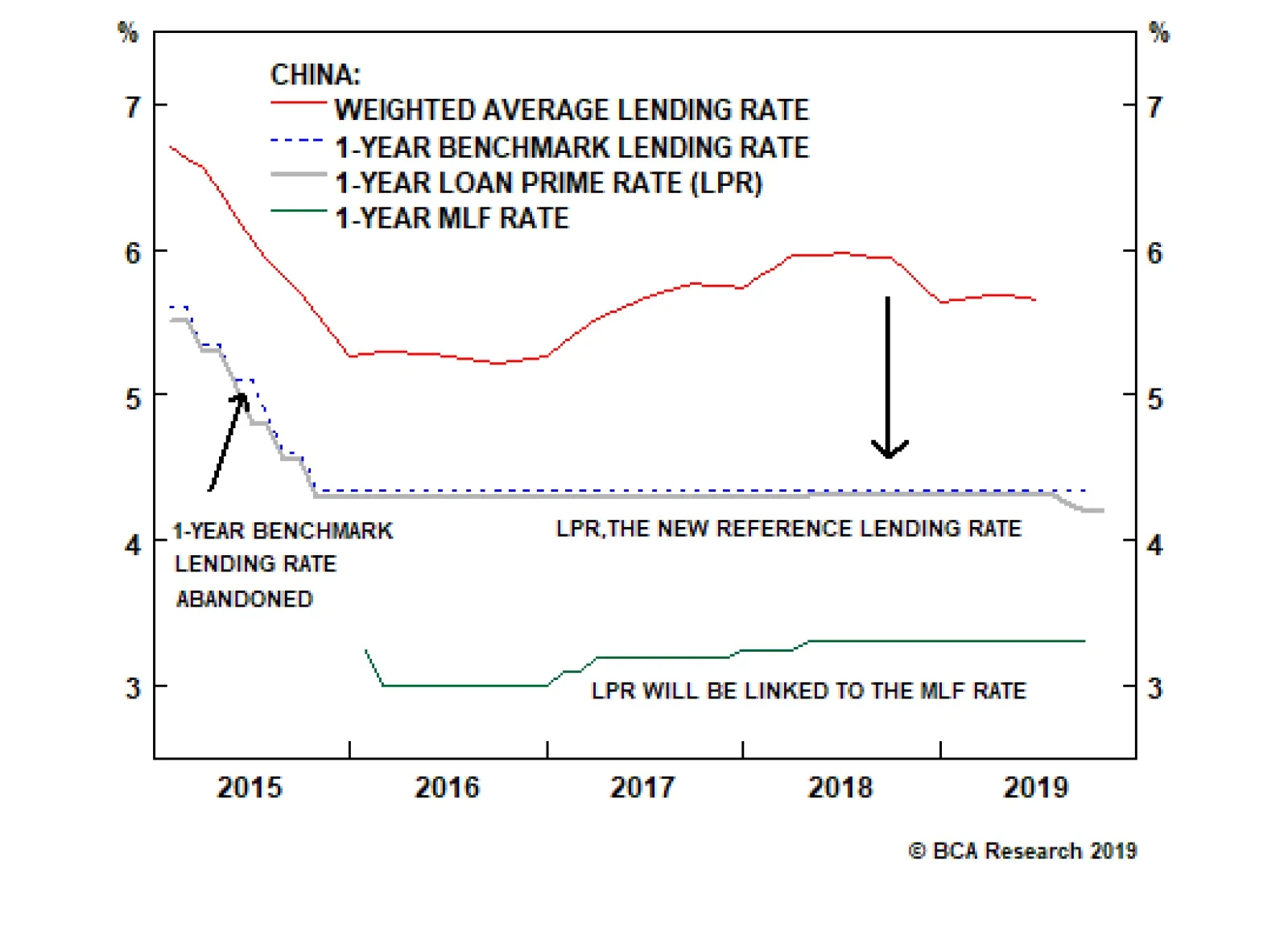

On August 20th, the PBoC launched a new loan prime rate (LPR) system, a revamped reference regime for setting bank loan interest rates. In September, the new LPR rate for one-year bank loans was lowered by five basis points. The new LPR reform is designed…

Analysis on Turkey is available below. Highlights A dovish Fed or robust U.S. growth does not constitute sufficient conditions for a bull market in EM. China’s business and credit cycles are much more important factors for EM than those of the U.S. A recovery in the Chinese economy and global manufacturing is not imminent. The common signal reverberating from various financial markets is that the risks to the global business cycle are still skewed to the downside. Feature Current investor perceptions of emerging markets are mixed. Some expect EM to benefit greatly from low U.S. interest rates. These investors view even a partial trade deal between the U.S. and China as sufficient for EM to embark on a bull market. BCA’s Emerging Markets Strategy team disagrees with this narrative. We deliberated the significance of the U.S.-China confrontation to EM in our September 19 report; therefore, we will not go over this subject here. Rather, in this report we discuss some of the more common misconceptions surrounding EM currently, and infer what these mean for investment strategies. Perception 1: The share of resource sectors (materials and energy) in the EM equity benchmark has declined substantially. This along with the expanded role of consumers and consumer stocks (Alibaba, Tencent and Baidu) in EM economies and equity markets has made their share prices less exposed to the global trade cycle and commodities prices. Reality: It is true that in many EM bourses, the weight of consumer stocks has been growing. Nevertheless, their financial markets in general, and equity markets in particular, remain very sensitive to the global trade cycle and commodities prices. Chart I-1 illustrates that the aggregate EM equity index has historically been and continues to be strongly correlated with the global basic materials stock index. The latter includes mining, steel and chemical companies. Global materials stocks also exhibit a very strong correlation with Chinese banks’ share prices. Moreover, global materials stocks also exhibit a very strong correlation with Chinese banks’ share prices (Chart I-2). The rationale for the high correlation is that both mainland banks’ profits and global demand for basic materials are driven by a common factor: China’s business cycle. Chart I-1EM And Global Materials Stocks Move Together

EM And Global Materials Stocks Move Together

EM And Global Materials Stocks Move Together

Chart I-2Chinese Bank And Global Materials Share Prices Are Highly Correlated

Chinese Bank And Global Materials Share Prices Are Highly Correlated

Chinese Bank And Global Materials Share Prices Are Highly Correlated

For example, construction in China is contracting (Chart I-3), which entails both higher NPLs for Chinese banks and lower demand for basic materials. China accounts for about 50% of global consumption of industrial metals, cement and many other basic materials. Finally, EM ex-China bank stocks also correlate strongly with global basic materials share prices. The basis is as follows: Many emerging economies export raw materials, and commodities price fluctuations impact their business cycle, exports and exchange rates. Chart I-3China: Construction Activity Is Contracting

China: Construction Activity Is Contracting

China: Construction Activity Is Contracting

Chart I-4High-Yielding EM: Currencies And Local Bond Yields

High-Yielding EM: Currencies And Local Bond Yields

High-Yielding EM: Currencies And Local Bond Yields

Historically, in high-yielding EM markets, currency depreciation has led to higher interest rates and lower bank share prices, and vice versa (Chart I-4). Lately, EM bond yields have not risen in response to EM currency depreciation. However, we believe this correlation will soon be re-established if EM currencies continue drifting lower. In short, China’s money/credit cycles drive not only the mainland’s business cycle, banking profits and NPLs, but also global trade and commodities prices. The latter two - via their impact on exchange rates and in turn interest rates - have historically explained credit and domestic demand cycles in high-yielding EM. Perception 2: EM stocks are a high-beta play on the S&P 500, i.e., EM equities outperform when the S&P 500 rallies, and vice versa. Reality: Since 2012, the beta for EM equity versus the S&P 500 has often been below one (Chart I-5). Furthermore, since 2012, EM share prices often failed to outpace their DM peers during global equity rallies. Indeed, EM relative equity performance versus DM, as well as the EM ex-China currency total return index, have been closely tracking the relative performance of global cyclicals versus global defensive stocks (Chart I-6). Chart I-5EM Equities Beta To The S&P 500

EM Equities Beta To The S&P 500

EM Equities Beta To The S&P 500

Chart I-6Global Cyclicals-To-Defensives Equity Ratio And EM

Global Cyclicals-To-Defensives Equity Ratio And EM

Global Cyclicals-To-Defensives Equity Ratio And EM

In short, EM equities and currencies have been, and will remain, sensitive to the global business cycle rather than the S&P 500. Since 2012, the latter has - on several occasions - decoupled from the global manufacturing and trade cycles. Perception 3: EM stocks, currencies and fixed-income markets are very sensitive to U.S. interest rates. Hence, a dovish Fed will lead to EM currency appreciation. Reality: Chart I-7 reveals that EM currencies, total returns on EM local currency bonds in U.S. dollar terms and EM sovereign credit spreads do not exhibit a strong relationship with U.S. Treasury yields. U.S. interest rate expectations have a much smaller impact on EM financial markets than commonly perceived by the investment community. Overall, U.S. interest rate expectations have a much smaller impact on EM financial markets than commonly perceived by the investment community. Chart I-7EM And U.S. Bond Yields: No Stable Correlation

bca.ems_wr_2019_10_10_s1_c7

bca.ems_wr_2019_10_10_s1_c7

Chart I-8China Cycle And EM Stocks Led U.S. Bond Yields

China Cycle And EM Stocks Led U.S. Bond Yields

China Cycle And EM Stocks Led U.S. Bond Yields

On the contrary, the declines in U.S. bond yields in both 2015/16 and in 2018/19 were due to the growth slowdown that emanated from China/EM. The top panel of Chart I-8 illustrates that Chinese import growth rolled over in December 2017, yet U.S. bond yields rolled over in October 2018. What is more, EM share prices have been leading U.S. bond yields in recent years, not the other way around (Chart I-8, bottom panel). Perception 4: If the U.S. avoids a recession, EM risk assets will recover. Chart I-9EM Profits Are Driven By Chinese Not U.S. Business Cycle

EM Profits Are Driven By Chinese Not U.S. Business Cycle

EM Profits Are Driven By Chinese Not U.S. Business Cycle

Reality: EM per-share earnings contracted in 2012-2014 and in 2019, despite reasonably robust growth in U.S. final demand (Chart I-9, top panel). This suggests that even if the U.S. economy avoids a recession, that will not be a sufficient condition to be bullish on EM. EM corporate profits are highly driven by China’s business cycle. The bottom panel of Chart I-9 illustrates that mainland domestic industrial orders have been the key driver of EM corporate profit cycles since 2008. Perception 5: EM equities, fixed-income markets and currencies are cheap. Reality: EM stocks are not cheap. They are fairly valued. Equity sectors with very poor fundamentals have very low multiples. Hence, they are “cheap” for a reason. These include Chinese banks, state-owned enterprises in various countries and resource companies. Equity segments with robust fundamentals are overpriced. Given that Chinese banks, state-owned enterprises in various countries, resource companies, and cyclical businesses have very large market caps, EM market-cap based equity valuation ratios are low – i.e., they appear cheap. To remove the impact of these large market cap segments, we constructed and have been publishing the following valuation ratios: median, 20% trimmed mean and equal-sub-sector weighted (Chart I-10). Each of these is calculated based on the average of trailing and forward P/E ratios, price-to-book value, price-to-cash earnings and price-to-dividend ratios. EM equities relative to DM are not cheap either. Chart I-11 demonstrates the same ratios – median, 20% trimmed-mean and equal-sub-sector weighted values for EM versus DM. Chart I-10EM Equities Are Not Cheap

bca.ems_wr_2019_10_10_s1_c10

bca.ems_wr_2019_10_10_s1_c10

Chart I-11Relative To DM EM Stocks Are Not Cheap

bca.ems_wr_2019_10_10_s1_c11

bca.ems_wr_2019_10_10_s1_c11

Further, when valuations are not at extremes as in the case of EM equities at the moment, the profit cycle holds the key to share price performance over a 6 to 12-month horizon. EM earnings are presently contracting in absolute terms, and underperforming DM EPS. Two currencies that offer value are the Mexican peso and Russian ruble. Chart I-12EM Local Yields Are Low In Absolute Terms And Relative To U.S.

EM Local Yields Are Low In Absolute Terms And Relative To U.S.

EM Local Yields Are Low In Absolute Terms And Relative To U.S.

In the fixed-income space, EM local bond yields are very low in absolute terms and relative to U.S. Treasury yields (Chart I-12). EM sovereign and corporate spreads are not wide either. As to exchange rates, the cheapest currencies are those with the worst fundamentals, such as the Argentine peso, Turkish lira and South African rand. The majority of other EM currencies are not very cheap. Two currencies that offer value are the Mexican peso and Russian ruble. Yet foreign investors are very long these currencies, and a combination of lower oil prices and portfolio outflows from broader EM will weigh on these exchange rates as well. Takeaways And Investment Strategy Chart I-13EM Currencies And Industrial Metals Prices

bca.ems_wr_2019_10_10_s1_c13

bca.ems_wr_2019_10_10_s1_c13

EM risk assets and currencies exhibit the strongest correlation with global trade and commodities prices. Chart I-13 indicates that the EM ex-China currency total return index closely tracks commodities prices. This corroborates the messages from Chart I-1 on page 1 and Chart I-6 on page 4. China’s business and credit cycles are much more important for EM than those of the U.S. A dovish Fed or strong U.S. growth are not sufficient reasons to bet on an EM bull market. A recovery in the Chinese economy and global manufacturing is not imminent. Individual EM countries’ domestic fundamentals such as return on capital, inflation, banking system health, competitiveness and politics drive individual EM performance. On these accounts, the outlook varies among EM. Readers can find analyses on specific EM economies in our Countries In-Depth page. Asset allocators should continue underweighting EM stocks, credit and currencies versus their DM counterparts. Absolute-return investors should outright avoid EM, or trade them on the short side. Within the EM equity space, our overweights are Mexico, Russia, Central Europe, Korea ex-tech, Thailand and the UAE. Our underweights are South Africa, Indonesia, Philippines, Hong Kong, Turkey and Colombia. The path of least resistance for the U.S. dollar is up. Continue shorting the following basket of EM currencies versus the dollar: ZAR, CLP, COP, IDR, MYR, PHP and KRW. We are also short the CNY versus the greenback. As always, the list of our country allocations for local currency bonds and sovereign credit markets is available at the end of our reports – please refer to page 16. Take Cues From These Markets We suggest investors take cues from the following financial market signals. They are unequivocally sending a downbeat message for global growth and risk assets: The ratio between Sweden and Swiss non-financial stocks in common currency terms is heading south (Chart I-14). Swedish non-financials include many companies leveraged to the global industrial cycle, while Swiss non-financials are dominated by defensive stocks. Hence, the persistent decline in this ratio presages a continued deterioration in the global industrial sector. Where is the next defense line for this ratio? To reach its 2002 and 2008 nadirs, it will need to drop by another 10%. In the interim, investors should maintain a defensive posture. Chart I-14A Message From Swedish And Swiss Equities

A Message From Swedish And Swiss Equities

A Message From Swedish And Swiss Equities

Chart I-15A Breakdown In The Making?

A Breakdown In The Making?

A Breakdown In The Making?

U.S. FAANG stocks appear to be cracking below their 200-day moving average. The relative performance of global cyclical versus global defensive stocks is relapsing below the three-year moving average that served as a support last December (Chart I-15). U.S. FAANG stocks appear to be cracking below their 200-day moving average (Chart I-16). If this support gives, the next one will be about 17% below current levels. Finally, U.S. high-beta share prices are on the verge of a breakdown (Chart I-17). The next technical support is 10% below current levels. Chart I-16FAANG Are On The Support Line

FAANG Are On The Support Line

FAANG Are On The Support Line

Chart I-17U.S. High-Beta Stocks Are On The Edge

U.S. High-Beta Stocks Are On The Edge

U.S. High-Beta Stocks Are On The Edge

Bottom Line: The common message reverberating from these financial markets corroborates our fundamental analysis that a global business cycle recovery is not imminent, and that global risk assets in general, and EM financial markets in particular, are at risk of selling off further. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Turkey: Is The Mean-Reversion Rally Over? Turkish financial markets have rebounded to their respective falling trend lines (Chart II-1). Are they set to break out or is a setback looming? Chart II-1Back To Falling Trend

Back To Falling Trend

Back To Falling Trend

Chart II-2TRY Is Cheap

TRY Is Cheap

TRY Is Cheap

Pros The economy has undergone a considerable real adjustment and many excesses have been purged: The current account balance has turned positive as imports have collapsed. Going forward, lower oil prices are likely to help the nation’s current account dynamics. The lira has become cheap (Chart II-2). According to the real effective exchange rate based on unit labor costs, the currency is one standard deviation below its fair value. Core and headline inflation have fallen, allowing the central bank to cut interest rates aggressively. However, the exchange rate still holds the key: if the currency depreciates anew, local bonds yields will rise and the ability of the central bank to reduce borrowing costs further will diminish. Finally, private credit and broad money growth have decelerated substantially and are contracting in inflation-adjusted terms (Chart II-3). Chart II-3Money & Credit Have Bottomed

Money & Credit Have Bottomed

Money & Credit Have Bottomed

Chart II-4Banks Have Been Aggressively Buying Government Bonds

Banks Have Been Aggressively Buying Government Bonds

Banks Have Been Aggressively Buying Government Bonds

The recent gap between broad money and private credit growth has been due to commercial banks buying government bonds (Chart II-4). When a commercial bank purchases a security from non-banks, a new deposit/new unit of money supply is created. Banks’ purchases of government bonds en masse have capped domestic bond yields. However, if pursued aggressively, such monetary expansion could weigh on the currency’s value. Cons Presently, potential sources of macro vulnerability in Turkey are: Foreign debt obligations (FDOs) – which are calculated as the sum of short-term claims, interest payments and amortization over the next 12 months – are at $168 billion, which is sizable. The annual current account surplus has reached only $4 billion and is sufficient to cover only 2.5% of FDOs, assuming the capital and financial account balance will be zero. Clearly, Turkey needs to both roll over most of its foreign debt coming due and attract foreign capital to finance a potential expansion in its imports if its domestic demand is to recover. Critically, $20 billion of net FX reserves, excluding gold, swap lines with foreign central banks and net of domestic banking and non-banking corporations’ foreign exchange deposits, are not adequate either to cover foreign debt obligations. Even though headline and core inflation measures have fallen, wage inflation remains rampant (Chart II-5). If wage inflation does not drop substantially very soon, rapidly rising unit labor costs will feed into inflation leading to negative ramifications for the exchange rate. This is especially crucial in Turkey given President Erdogan has undermined the central bank’s credibility and is resorting to populist measures to revive his popularity. Finally, Turkish banks remain under-provisioned. Currently, the banking regulator is requiring banks to boost their non-performing loans (NPL) ratio to 6.3% of total loans.This a far cry from the 2001 episode when the NPL ratio shot up to 25% (Chart II-6). Even though interest rates rose much more in 2001 than last year, the private credit penetration in the economy was very low in the early 2000s. A higher credit penetration usually implies weaker borrowers have borrowed money and heralds a higher NPL ratio. Typically, following a credit boom and bust, it is natural for the NPL ratio to exceed 10%. We do not think Turkish banks stocks, having rallied a lot from their lows, are pricing in such a scenario. Chart II-5Surging Wages Are A Risk

Surging Wages Are A Risk

Surging Wages Are A Risk

Chart II-6NPL Ratio Is Unrealistic

NPL Ratio Is Unrealistic

NPL Ratio Is Unrealistic

Investment Recommendation We recommend both absolute-return investors and asset allocators not to chase Turkish financial markets higher. Renewed market volatility lies ahead. Given we expect foreign capital outflows from EM, Turkish companies and banks will encounter difficulties in rolling over their external debt and attracting foreign capital into domestic markets. This will produce a new downleg in the exchange rate. In turn, currency depreciation will weigh on performance of local bonds as well as sovereign and corporate credit. Stay underweight. Andrija Vesic, Research Analyst andrijav@bcaresearch.com Footnotes Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights The Chinese economy is still slowing, and there is not yet enough evidence from forward-looking economic data to suggest a turnaround is imminent. Deflation has returned to China’s industrial sector. Even though overall price deceleration has been relatively mild, it is further squeezing already deteriorating industrial profit growth. We do not expect deflation to spiral into a 2015/2016-style episode, which removes at least one risk to our growth outlook. At the same time, a mild deceleration in prices will not provide enough incentive for Chinese policymakers to hit the stimulus button. The People’s Bank of China’s new interest rate-setting regime, the LPR, will not provide much in the way of stimulus over the next few months. But it has the potential to improve China’s monetary policy transmission mechanism over the coming year, increasing the odds that policymakers will succeed in stabilizing economic activity. Short-term downside risks to growth have not abated, and we remain tactically bearish on Chinese stocks. Cyclically, we continue to recommend an overweight stance, on the basis of an eventual reacceleration in economic activity. Feature Chart 1The Chinese Economy Is Still Slowing

The Chinese Economy Is Still Slowing

The Chinese Economy Is Still Slowing

China’s economy is at a critical juncture: “Half-measured” stimulus so far has been able to keep the domestic economy in better shape than in the 2015-2016 down cycle, but overall economic activity has not bottomed (Chart 1). The Sino-America trade talk has resumed at the moment, but the two sides have yet to make any substantive progress towards a deal. In the meantime, the global economy has also reached a critical point where the degree of economic weakness has the potential to feed on itself, possibly triggering a recession.1 This underscores our tactically bearish stance towards Chinese stocks versus the global equity benchmark. Barring more forceful stimulus or resolution on the trade front, any external shock and/or internal policy missteps could easily tip the Chinese economy into a deeper growth slowdown. Hence, downside risks remain elevated for Chinese stocks over the next 3- to 6-months. The “D” Word Returns, But Won’t Spur Aggressive Further Easing Chart 2Industrial Price Deflation Returns

Industrial Price Deflation Returns

Industrial Price Deflation Returns

Economic data over the past two months have provided mixed signals. Readings from both China’s National Bureau of Statistics (NBS) PMI and from the Caixin PMI show an improvement in the manufacturing sector. However, industrial deflation has returned to China: Three years after the country declared victory against a prolonged industrial destocking cycle, producer price inflation (PPI) relapsed into negative territory in July and declined further in August (Chart 2). While prices are typically lagging indicators and reflect lingering effects from past economic conditions, there is not enough evidence in forward-looking economic data right now to suggest a turnaround in the economy is imminent.2 A deflationary PPI is not a trivial source of concern for Chinese policymakers. Last time growth in China’s PPI turned negative, it took policymakers four and a half years and an annualized 28% of GDP worth of credit expansion to pull the industrial sector out of its deflationary cycle. Chart 3Deflation Threatens Recovery In Industrial Profit Growth

Deflation Threatens Recovery In Industrial Profit Growth

Deflation Threatens Recovery In Industrial Profit Growth

For investors, deflation has pernicious effects on profits, and we have received several client inquiries concerning the topic since PPI growth turned negative. The historical relationship suggests profit growth for both the A-share and investable markets is highly linked to fluctuations in producer prices (Chart 3), and China’s industrial sector profit growth has already been rapidly deteriorating over the past 12 months. The good news is that we do not expect the current episode of PPI deflation to become as protracted as it did in 2012-2016, or as severe as in 2015-2016. Two reasons underpin our view: Since early-2018, monetary policy has been much easier than during past deflationary episodes. Monetary policy in the past year and half has been much more accommodative than in the three years leading to the deep industrial deflationary cycle in 2015, particularly on the exchange rate front. The RMB was soft-pegged to a rising U.S. dollar before it was decoupled by the PBoC in August 2015, and was appreciating against its trading partners throughout most of 2012-2015. Bank lending rates were also kept at historically high levels during this period (Chart 4). This time, even though money and credit growth has not returned to the same pace as in 2015-2016, current ultra-loose monetary conditions should spur enough credit growth to keep prices from deflating aggressively. Chart 4Monetary Conditions Easier Than Last Cycle

Monetary Conditions Easier Than Last Cycle

Monetary Conditions Easier Than Last Cycle

Inventory levels are low, and capacity levels do not appear to be overly excessive. After years of industrial consolidation, China’s industrial capacity does not appear to be particularly excessive compared to the past cycle. This is distinctively different from the prolonged contraction in PPI between 2012 and 2016, when China’s industrial inventories were coming off a five-year-long destocking cycle, and capacity utilization fell markedly (Chart 5). This is not the case today. Moreover, even though final demand has been weak, production has retrenched even more, drawing down inventories to the point where the pace of inventory destocking may have reached a cyclical bottom (Chart 6). A re-stocking of industrial goods should boost producers’ pricing power. Chart 5Capacity Is Not Excessively Underutilized

Capacity Is Not Excessively Underutilized

Capacity Is Not Excessively Underutilized

Chart 6Inventory Destocking May Be Bottoming Out

Inventory Destocking May Be Bottoming Out

Inventory Destocking May Be Bottoming Out

But the bad news (for investors), is that contained, or mild producer price deflation will not be reason alone to spur aggressive further easing from policymakers. This means that the re-emergence of price deflation, even mild and short-lived, will weigh on earnings and investor sentiment. Bottom Line: This episode of producer price deflation is unlikely to become as pernicious as occurred in the past, but policymakers are thus unlikely to act aggressively to counter it. While this removes some of the downside risks for Chinese stocks, even mild deflation will weigh on earnings growth (and thus sentiment) which underscores our tactically bearish stance on Chinese stocks. Demystifying China’s New Loan Prime Rate: Not The Stimulus You Are Looking For On August 20th, the PBoC launched a new loan prime rate (LPR) system, a revamped reference regime for setting bank loan interest rates3 (Chart 7). In September, the new LPR rate for one-year bank loans was lowered by five basis points. Since then, the market has been fixated on predicting whether the PBoC will cut the Medium-Lending Facility (MLF) rate next, which would be perceived as a change in China’s monetary stance. Chart 7China's New LPR: A Shadow 'Tax Cut'

China's New LPR: A Shadow "Tax Cut"

China's New LPR: A Shadow "Tax Cut"

PBoC will increase its control of the pricing of credit, while tight financial regulations will restrict the size and speed of credit growth. The new LPR reform, in our view, is designed to force state-owned (and better-capitalized) commercial banks to hand out a “tax cut” to struggling small- and medium-sized enterprises (SMEs) by lowering bank lending rates. At the same time, it allows the PBoC to take back control of the pricing of credit from commercial banks, “killing two birds with one stone.” There are three main market implications from this approach: The new LPR is likely to gradually narrow the gap between corporate bond yields (i.e. “market rates”) and bank lending rates; A cut in the MLF rate in the near term should be interpreted as a “reward” to commercial banks rather than a stimulus for the economy; Most importantly, the new LPR system does not mean rapid credit expansion is in the cards. Quite the opposite, in the near term, banks may tighten their lending. The wide spread between the 3-month interbank repo rate and average bank lending rate illustrates the reason why the PBoC has introduced the LPR.4 This gap is also evident when comparing the yield of AAA-rated corporate bonds and the average bank lending rate (Chart 8). These gaps exist because Chinese commercial banks have largely manipulated the 1-year bank lending rate set by the PBoC when lending to their “preferred customers,” usually state-owned enterprises and real estate developers, by offering significantly discounted loan rates. Banks then charge substantial “risk premiums” on loans to the private sector, mostly SMEs, to make up for the narrower profit margins on loans to SOEs (Chart 9). Chart 8An Impaired Monetary Policy Transmission Mechanism

An Impaired Monetary Policy Transmission Mechanism

An Impaired Monetary Policy Transmission Mechanism

Chart 9Evidence Of Asymmetrical Lending Practices

Evidence Of Asymmetrical Lending Practices

Evidence Of Asymmetrical Lending Practices

The new LPR system is designed to minimize this discrepancy, since the new LPRs are more market based and are quoted based on the price of loans banks charge their prime clients. By design, the new LPR system should force the average bank lending rate closer to the rate companies borrow in the bond market. This means bank lending rates will be guided lower, including lending rates for SMEs. However, the new system will be implemented in phases, and the PBoC is likely to gradually guide LPRs lower to allow banks to readjust their pricing models. The LPR rate is essentially the MLF rate plus bank profit margins (the added basis points above the MLF rate). The market will guide the top line lending rate, while the PBoC will have control over the floor rate (MLF) through open market operations. The fact that the PBoC is keeping the MLF rate unchanged while allowing the LPR to drop (albeit slightly) sends an explicit message: The PBoC is forcing banks to lower lending rates first before boosting their now-narrowed profit margins by lowering the MLF rate. In contrast to expectations of market participants that the LPR system will ease credit conditions, banks may actually tighten their lending in the coming months. While the PBoC will increase its control of the pricing of bank loans by the rate reform plan, the strengthening in financial regulations that has occurred over the past year will restrict the size and speed of credit growth. This combination has created more room for monetary easing without unleashing “animal spirits.” Borrowing costs to risky institutions have been higher since the Baoshang Bank takeover and are likely to remain elevated even if interest rates are lower (Chart 10). More importantly, mortgage and real estate developer loans together account for nearly 30% of total bank credit. Unless policymakers ease the brakes on lending restrictions to the property sector, bank lending growth is unlikely to pick up meaningfully (Chart 11). In fact, the PBoC has explicitly excluded mortgage and property-related lending from benefitting from the LPR rate cut.5 Barring a significant worsening in economic data, we do not expect the PBoC to lower mortgage lending and real estate-related loan rates in the coming months. Chart 10Tightened Financial Regulations Will Keep Cost Of Risky Lending High

Tightened Financial Regulations Will Keep Cost Of Risky Lending High

Tightened Financial Regulations Will Keep Cost Of Risky Lending High

Chart 11Mortgage Rate Unlikely To Return To Its 2016 Low

Mortgage Rate Unlikely To Return To Its 2016 Low

Mortgage Rate Unlikely To Return To Its 2016 Low

Finally, in the next two- to three-quarter mandatory implementation period, banks will be readjusting their pricing and credit risk-assessing models. During the transition, we expect more cautious sentiment among both lenders and borrowers. Hence, in the short term, bank loan growth may actually moderate. Bottom Line: The new LPR system may lower China’s banking sector profits in the short term. But in the next 6- to 12-months, we expect the PBoC to compensate commercial banks by keeping ample liquidity in the interbank system and by eventually lowering the MLF rate. The new LPR system may slow bank credit growth in the next few months, but after its full implementation (by the second quarter of 2020), it will have the potential to make PBoC’s policy more effective. Investment Conclusions We expect two phases of Chinese equity relative performance over the coming year: one phase of flat-to-potentially seriously down performance to last from now until sometime in the first quarter of 2020 when the economy bottoms, and then a phase of outperformance. Our expectation that the economy will bottom in Q1 2020 rests on the existing reflationary response by Chinese policymakers and an improved monetary transmission mechanism. Chart 12We Expect The Chinese Economy To Bottom In Q1 2020

We Expect The Chinese Economy To Bottom In Q1 2020

We Expect The Chinese Economy To Bottom In Q1 2020

Our expectation that the economy will bottom in the first quarter of 2020 continues to rest on the existing reflationary response by Chinese policymakers (Chart 12), and the fact that China’s new LPR system has the potential to improve what is currently a seriously impaired monetary transmission mechanism beyond the next two or three quarters. But the existing response of policymakers has been considerably more measured when compared to past economic cycles, meaning that equity investors are unlikely to be as forward-looking as they otherwise might be. Weak producer price deflation will weigh on investor sentiment, and it is unlikely to be weak enough to spur aggressive further easing. The potential for further escalation of the U.S.-China trade war also compellingly argues against an overweight stance in the near-term, even if we expect economic growth to subsequently improve. Consequently, we remain tactically bearish and cyclically bullish towards Chinese stocks: medium-term investors who are already positioned in favor of China-related assets should stay long, whereas investors who have not yet moved to an overweight stance should wait for a better buying opportunity to emerge over the coming few months. Jing Sima China Strategist JingS@bcaresearch.com Footnotes 1 Please see Global Investment Strategy Outlook “Fourth Quarter 2019 Strategy Outlook: A “Show Me” Market”, dated October 4, 2019, available at gis.bcaresearch.com 2 Please see China Investment Strategy Weekly Report “China Macro And Market Review”, dated October 2, 2019, available at cis.bcaresearch.com 3 Announcement of the People’s Bank of China on Improving Loan Prime Rate (LPR) Formation Mechanism, August 19, 2019, available at http://www.pbc.gov.cn/en/3688110/3688172/3877490/index.html 4 PBC Official Answers Press Questions on Improving Loan Prime Rate (LPR) Formation Mechanism, August 20, 2019, available at http://www.pbc.gov.cn/en/3688110/3688172/3877865/index.html 5 Announcement of the People’s Bank of China No.16, August 27, 2019, available at http://www.pbc.gov.cn/en/3688110/3688172/3881177/index.html Cyclical Investment Stance Equity Sector Recommendations

The challenger power is not blameless. It senses weakness in the hegemon and begins to develop a regional sphere of influence. The problem is that regional hegemony is a perfect launching pad towards global hegemony. And while the challenger’s intentions may…

Speaking in the Reichstag in 1897, German Foreign Secretary Bernhard von Bülow proclaimed that it was time for Germany to demand “its own place in the sun.” The occasion was a debate on Germany’s policy towards East Asia. Bülow soon ascended to the…

Highlights The Cold War is a limited analogy for the U.S.-China conflict; In a multipolar world, complete bifurcation of trade is difficult if not impossible; History suggests that trade between rivals will continue, with minimal impediments; On a secular horizon, buy defense stocks, Europe, capex, and non-aligned countries. Feature There is a growing consensus that China and the U.S. are hurtling towards a Cold War. BCA Research played some part in this consensus – at least as far as the investment community is concerned – by publishing “Power and Politics in East Asia: Cold War 2.0?” in September 2012.1 For much of this decade, Geopolitical Strategy focused on the thesis that geopolitical risk was rotating out of the Middle East, where it was increasingly irrelevant, to East Asia, where it would become increasingly relevant. This thesis remains cogent, but it does not mean that a “Silicon Curtain” will necessarily divide the world into two bifurcated zones of capitalism. Trade, capital flows, and human exchanges between China and the U.S. will continue and may even grow. But the risk of conflict, including a military one, will not decline. In this report, we first review the geopolitical logic that underpins Sino-American tensions. We then survey the academic literature for clues on how that relationship will develop vis-à-vis trade and economic relations. The evidence from political theory is surprising and highly investment relevant. We then look back at history for clues as to what this means for investors. Our conclusion is that it is highly likely that the U.S. and China will continue to be geopolitical rivals. However, due to the geopolitical context of multipolarity, it is unlikely that the result will be “Bifurcated Capitalism.” Rather, we expect an exciting and volatile environment for investors where geopolitics takes its historical place alongside valuation, momentum, fundamentals, and macroeconomics in the pantheon of factors that determine investment opportunities and risks. The Thucydides Trap Is Real … Speaking in the Reichstag in 1897, German Foreign Secretary Bernhard von Bülow proclaimed that it was time for Germany to demand “its own place in the sun.”2 The occasion was a debate on Germany’s policy towards East Asia. Bülow soon ascended to the Chancellorship under Kaiser Wilhelm II and oversaw the evolution of German foreign policy from Realpolitik to Weltpolitik. While Realpolitik was characterized by Germany’s cautious balancing of global powers under Chancellor Otto von Bismarck, Weltpolitik saw Bülow and Wilhelm II seek to redraw the status quo through aggressive foreign and trade policy. Imperial Germany joined a long list of antagonists, from Athens to today’s People’s Republic of China, in the tragic play of human history dubbed the “Thucydides Trap.”3 Chart 1Imperial Overstretch

Imperial Overstretch

Imperial Overstretch

The underlying concept is well known to all students of world history. It takes its name from the Greek historian Thucydides and his seminal History of the Peloponnesian War. Thucydides explains why Sparta and Athens went to war but, unlike his contemporaries, he does not moralize or blame the gods. Instead, he dispassionately describes how the conflict between a revisionist Athens and established Sparta became inevitable due to a cycle of mistrust. Graham Allison, one of America’s preeminent scholars of international relations, has argued that the interplay between a status quo power and a challenger has almost always led to conflict. In 12 out of the 16 cases he surveyed, actual military conflict broke out. Of the four cases where war did not develop, three involved transitions between countries that shared a deep cultural affinity and a respect for the prevailing institutions.4 In those cases, the transition was a case of new management running largely the same organizational structure. And one of the four non-war outcomes was nothing less than the Cold War between the Soviet Union and the U.S. The fundamental problem for a status quo power is that its empire or “sphere of influence” remains the same size as when it stood at the zenith of power. However, its decline in a relative sense leads to a classic problem of “imperial overstretch.” The hegemonic or imperial power erroneously doubles down on maintaining a status quo that it can no longer afford (Chart 1). The challenger power is not blameless. It senses weakness in the hegemon and begins to develop a regional sphere of influence. The problem is that regional hegemony is a perfect jumping off point towards global hegemony. And while the challenger’s intentions may be limited and restrained (though they often are ambitious and overweening), the status quo power must react to capabilities, not intentions. The former are material and real, whereas the latter are perceived and ephemeral. The challenging power always has an internal logic justifying its ambitions. In China’s case today, there is a sense among the elite that the country is merely mean-reverting to the way things were for many centuries in China’s and Asia’s long history (Chart 2). In other words, China is a “challenger” power only if one describes the status quo as the past three hundred years. It is the “established” power if one goes back to an earlier state of affairs. As such, the consensus in China is that it should not have to pay deference to the prevailing status quo given that the contemporary context is merely the result of western imperialist “challenges” to the established Chinese and regional order. Chart 2China’s Mean Reverting Narrative

Back To The Nineteenth Century

Back To The Nineteenth Century

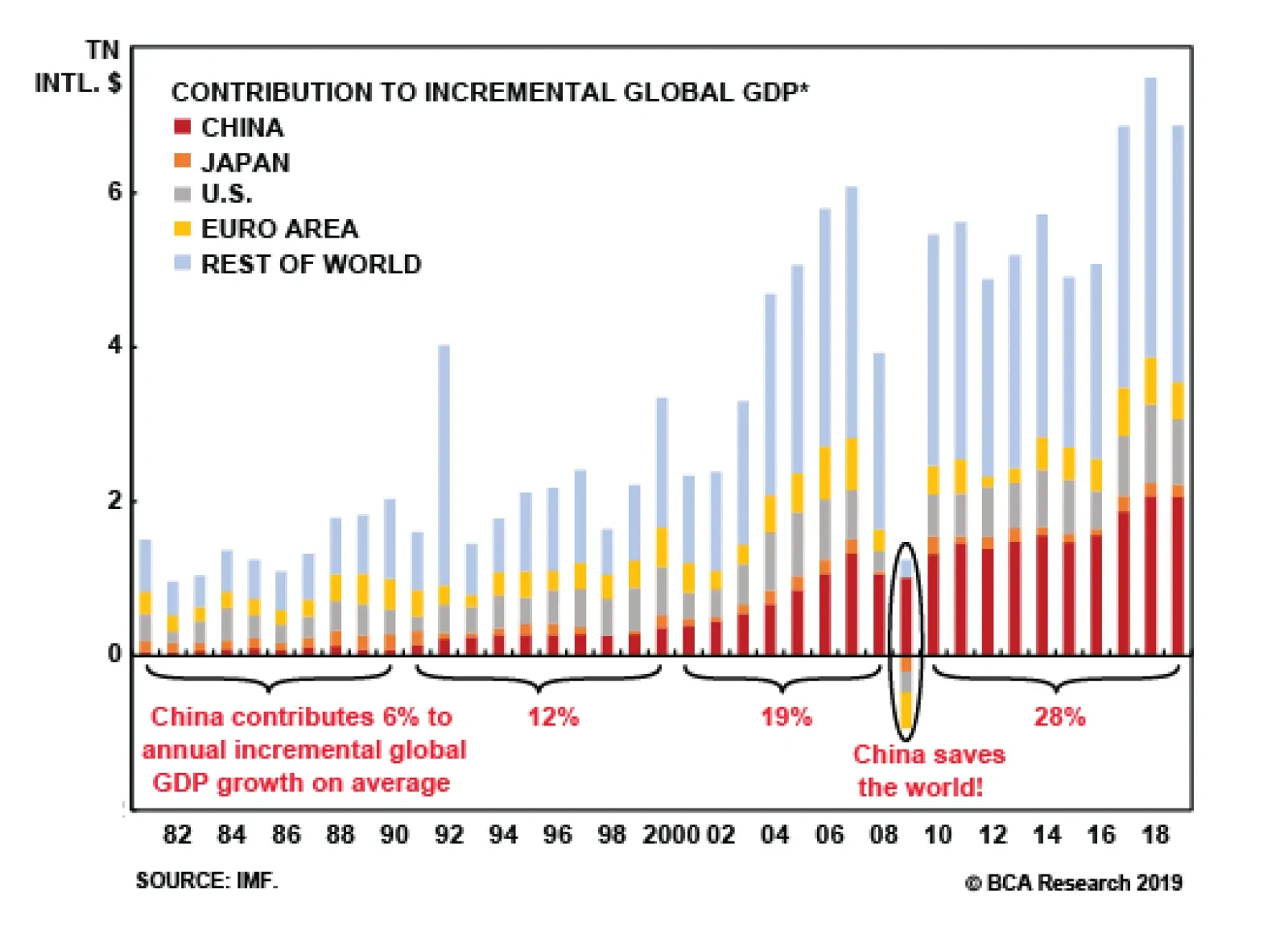

In addition, China has a legitimate claim that it is at least as relevant to the global economy as the U.S. and therefore deserves a greater say in global governance. While the U.S. still takes a larger share of the global economy, China has contributed 23% to incremental global GDP over the past two decades, compared to 13% for the U.S. (Chart 3). Chart 3The Beijing Consensus

Back To The Nineteenth Century

Back To The Nineteenth Century

Bottom Line: The emerging tensions between China and the U.S. fit neatly into the theoretical and empirical outlines of the Thucydides Trap. We do not see any way for the two countries to avoid struggle and conflict on a secular or forecastable horizon. What does this mean for investors? For one, the secular tailwinds behind defense stocks will persist. But what beyond that? Is the global economy destined to witness complete bifurcation into two armed camps separated by a Silicon Curtain? Will the Alibaba and Amazon Pacts suspiciously glare at each other the way that NATO and Warsaw Pacts did amidst the Cold War? The answer, tentatively, is no. … But It Will Not Lead to Economic Bifurcation President Trump’s aggressive trade policy also fits neatly into political theory, to a point. Realism in political science focuses on relative gains over absolute gains in all relationships, including trade. This is because trade leads to economic prosperity, prosperity to the accumulation of economic surplus, and economic surplus to military spending, research, and development. Two states that care only about relative gains due to rivalry produce a zero-sum game with no room for cooperation. It is a “Prisoner’s Dilemma” that can lead to sub-optimal economic outcomes in which both actors chose not to cooperate. The U.S.-China conflict will not lead to complete bifurcation of the global economy. Diagram 1 illustrates the effects of relative gain calculations on the trade behavior of states. In the absence of geopolitics, demand (Q3) is satisfied via trade (Q3-Q0) due to the inability of domestic production (Q0) to meet it. Diagram 1Trade War In A Bipolar World

Back To The Nineteenth Century

Back To The Nineteenth Century

However, geopolitical externality – a rivalry with another state – raises the marginal social cost of imports – i.e. trade allows the rival to gain more out of trade and “catch up” in terms of geopolitical capabilities. The trading state therefore eliminates such externalities with a tariff (t), raising domestic output to Q1, while shrinking demand to Q2, thus reducing imports to merely Q2-Q1, a fraction of where they would be in a world where geopolitics do not matter. The dynamic of relative gains can also have a powerful pull on the hegemon as it begins to weaken and rethink its originally magnanimous trade relations. As political scientist Duncan Snidal argued in a 1991 paper, When the global system is first set up, the hegemon makes deals with smaller states. The hegemon is concerned more with absolute gains, smaller states are more concerned with relative, so they are tougher negotiators. Cooperative arrangements favoring smaller states contribute to relative hegemonic decline. As the unequal distribution of benefits in favor of smaller states helps them catch up to the hegemonic actor, it also lowers the relative gains weight they place on the hegemonic actor. At the same time, declining relative preponderance increases the hegemonic state’s concern for relative gains with other states, especially any rising challengers. The net result is increasing pressure from the largest actor to change the prevailing system to gain a greater share of cooperative benefits.5 The reason small states are initially more concerned with relative gains is because they are far more concerned with national security than the hegemon. The hegemon has a preponderance of power and is therefore more relaxed about its security needs. This explains why Presidents George Bush Sr., Bill Clinton, and George Bush Jr. all made “bad deals” with China. Writing nearly thirty years ago, Snidal cogently described the current U.S.-China trade war. Snidal thought he was describing a coming decade of anarchy. But he and fellow political scientists writing in the early 1990s underestimated American power. The “unipolar moment” of American supremacy was not over, it was just beginning! As such, the dynamic Snidal described took thirty years to come to fruition. When thinking about the transition away from U.S. hegemony, most investors anchor themselves to the Cold War as it is the only world they have known that was not unipolar. Moreover the Cold War provides a simple, bipolar distribution of power that is easy to model through game theory. If this is the world we are about to inhabit, with the U.S. and China dividing the whole planet into spheres like the U.S. and Soviet Union, then the paragraph we lifted from Snidal’s paper would be the end of it. America would abandon globalization in totality, impose a draconian Silicon Curtain around China, and coerce its allies to follow suit. But most of recent human history has been defined by a multipolar distribution of power between states, not a bipolar one. The term “cold war” is applicable to the U.S. and China in the sense that comparable military power may prevent them from fighting a full-blown “hot war.” But ultimately the U.S.-Soviet Cold War is a poor analogy for today’s world. In a multipolar world, Snidal concludes, “states that do not cooperate fall behind other relative gains maximizers that cooperate among themselves. This makes cooperation the best defense (as well as the best offense) when your rivals are cooperating in a multilateral relative gains world.” Snidal shows via formal modeling that as the number of players increases from two, relative-gains sensitivity drops sharply.6 The U.S.-China relationship does not occur in a vacuum — it is moderated by the global context. Today’s global context is one of multipolarity. Multipolarity refers to the distribution of geopolitical power, which is no longer dominated by one or two great powers (Chart 4). Europe and Japan, for instance, have formidable economies and military capabilities. Russia remains a potent military power, even as India surpasses it in terms of overall geopolitical power. Chart 4The World Is No Longer Bipolar

The World Is No Longer Bipolar

The World Is No Longer Bipolar

A multipolar world is the least “ordered” and the most unstable of world systems (Chart 5). This is for three reasons: Chart 5Multipolarity Is Messy

Multipolarity Is Messy

Multipolarity Is Messy

Math: Multipolarity engenders more potential “conflict dyads” that can lead to conflict. In a unipolar world, there is only one country that determines norms and rules of behavior. Conflict is possible, but only if the hegemon wishes it. In a bipolar world, conflict is possible, but it must align along the axis of the two dominant powers. In a multipolar world, alliances are constantly shifting and producing novel conflict dyads. Lack of coordination: Global coordination suffers in periods of multipolarity as there are more “veto players.” This is particularly problematic during times of stress, such as when an aggressive revisionist power uses force or when the world is faced with an economic crisis. Charles Kindleberger has argued that it was exactly such hegemonic instability that caused the Great Depression to descend into the Second World War in his seminal The World In Depression.7 Mistakes: In a unipolar and bipolar world, there are a very limited number of dice being rolled at once. As such, the odds of tragic mistakes are low and can be mitigated with complex formal relationships (such as U.S.-Soviet Mutually Assured Destruction, grounded in formal modeling of game theory). But in a multipolar world, something as random as an assassination of a dignitary can set in motion a global war. The multipolar system is far more dynamic and thus unpredictable. In a multipolar world, the U.S. will not be able to exclude China from the global system. Diagram 2 is modified for a multipolar world. Everything is the same, except that we highlight the trade lost to other great powers. The state considering using tariffs to lower the marginal social cost of trading with a rival must account for this “lost trade.” In the context of today’s trade war with China, this would be the sum of all European Airbuses and Brazilian soybeans sold to China in the place of American exports. For China, it would be the sum of all the machinery, electronics, and capital goods produced in the rest of Asia and shipped to the United States. Diagram 2Trade War In A Multipolar World

Back To The Nineteenth Century

Back To The Nineteenth Century

Could Washington ask its allies – Europe, Japan, South Korea, Taiwan, etc. – not to take advantage of the lucrative trade (Q3-Q0)-(Q2-Q1) lost due to its trade tiff with China? Sure, but empirical research shows that they would likely ignore such pleas for unity. Alliances produced by a bipolar system produce a statistically significant and large impact on bilateral trade flows, a relationship that weakens in a multipolar context. This is the conclusion of a 1993 paper by Joanne Gowa and Edward D. Mansfield.8 The authors draw their conclusion from an 80-year period beginning in 1905, which captures several decades of global multipolarity. Unless the U.S. produces a wholehearted diplomatic effort to tighten up its alliances and enforce trade sanctions – something hardly foreseeable under the current administration – the self-interest of U.S. allies will drive them to continue trading with China. The U.S. will not be able to exclude China from the global system; nor will China be able to achieve Xi Jinping’s vaunted “self-sufficiency.” A risk to our view is that we have misjudged the global system, just as political scientists writing in the early 1990s did. To that effect, we accept that Charts 1 and 4 do not really support a view that the world is in a balanced multipolar state. The U.S. clearly remains the most powerful country in the world. The problem is that it is also clearly in a relative decline and that its sphere of influence is global – and thus very expensive – whereas its rivals have merely regional ambitions (for the time being). As such, we concede that American hegemony could be reasserted relatively quickly, but it would require a significant calamity in one of the other poles of power. For instance, a breakdown in China’s internal stability alongside the recovery of U.S. political stability. Bottom Line: The trade war between the U.S. and China is geopolitically unsustainable. The only way it could continue is if the two states existed in a bipolar world where the rest of the states closely aligned themselves behind the two superpowers. We have a high conviction view that today’s world is – for the time being – multipolar. American allies will cheat and skirt around Washington’s demands that China be isolated. This is because the U.S. no longer has the preponderance of power that it enjoyed in the last decade of the twentieth and the first decade of the twenty-first century. Insights presented thus far come from formal theory in political science. What does history teach us? Trading With The Enemy In 1896, a bestselling pamphlet in the U.K., “Made in Germany,” painted an ominous picture: “A gigantic commercial State is arising to menace our prosperity, and contend with us for the trade of the world.”9 Look around your own houses, author E.E. Williams urged his readers. “The toys, and the dolls, and the fairy books which your children maltreat in the nursery are made in Germany: nay, the material of your favorite (patriotic) newspaper had the same birthplace as like as not.” Williams later wrote that tariffs were the answer and that they “would bring Germany to her knees, pleading for our clemency.”10 By the late 1890s, it was clear to the U.K. that Germany was its greatest national security threat. The Germany Navy Laws of 1898 and 1900 launched a massive naval buildup with the singular objective of liberating the German Empire from the geographic constraints of the Jutland Peninsula. By 1902, the First Lord of the Royal Navy pointed out that “the great new German navy is being carefully built up from the point of view of a war with us.”11 There is absolutely no doubt that Germany was the U.K.’s gravest national security threat. As a result, London signed in April 1904 a set of agreements with France that came to be known as Entente Cordiale. The entente was immediately tested by Germany in the 1905 First Moroccan Crisis, which only served to strengthen the alliance. Russia was brought into the pact in 1907, creating the Triple Entente. In hindsight, the alliance structure was obvious given Germany’s meteoric rise from unification in 1871. However, one should not underestimate the magnitude of these geopolitical events. For the U.K. and France to resolve centuries of differences and formalize an alliance in 1904 was a tectonic shift — one that they undertook against the grain of history, entrenched enmity, and ideology.12 History teaches us that trade occurs even amongst rivals and during wartime. Political scientists and historians have noted that geopolitical enmity rarely produces bifurcated economic relations exhibited during the Cold War. Both empirical research and formal modeling shows that trade occurs even amongst rivals and during wartime.13 This was certainly the case between the U.K. and Germany, whose trade steadily increased right up until the outbreak of World War One (Chart 6). Could this be written off due to the U.K.’s ideological commitment to laissez-faire economics? Or perhaps London feared a move against its lightly defended colonies in case it became protectionist? These are fair arguments. However, they do not explain why Russia and France both saw ever-rising total trade with the German Empire during the same period (Chart 7). Either all three states were led by incompetent policymakers who somehow did not see the war coming – unlikely given the empirical record – or they simply could not afford to lose out on the gains of trade with Germany to each other. Chart 6The Allies Traded With Germany…

Back To The Nineteenth Century

Back To The Nineteenth Century

Chart 7… Right Up To WWI

Back To The Nineteenth Century

Back To The Nineteenth Century

Chart 8Japan And U.S. Never Downshifted Trade

Back To The Nineteenth Century

Back To The Nineteenth Century

A similar dynamic was afoot ahead of World War Two. Relations between the U.S. and Japan soured in the 1930s, with the Japanese invasion of Manchuria in 1931. In 1935, Japan withdrew from the 1922 Washington Naval Treaty – the bedrock of the Pacific balance of power – and began a massive naval buildup. In 1937, Japan invaded China. Despite a clear and present danger, the U.S. continued to trade with Japan right up until July 26, 1941, few days after Japan invaded southern Indochina (Chart 8). On December 7, Japan attacked the U.S. A skeptic may argue that precisely because policymakers sleepwalked into war in the First and Second World Wars, they will not (or should not) make the same mistake this time around. First, we do not make policy prescriptions and therefore care not what should happen. Second, we are highly skeptical of the view that policymakers in the early and mid-twentieth century were somehow defective (as opposed to today’s enlightened leaders). Our constraints-based framework urges us to seek systemic reasons for the behavior of leaders. Political science provides a clear theoretical explanation for why London and Washington continued to trade with the enemy despite the clarity of the threat. The answer lies in the systemic nature of the constraint: a multipolar world reduces the sensitivity of policymakers to relative gains by introducing a collective action problem thanks to changing alliances and the difficulty of disciplining allies’ behavior. In the case of U.S. and China, this is further accentuated by President Trump’s strategy of skirting multilateral diplomacy and intense focus on mercantilist measures of power (i.e. obsession with the trade deficit). An anti-China trade policy that was accompanied by a magnanimous approach to trade relations with allies could have produced a “coalition of the willing” against Beijing. But after two years of tariffs and threats against the EU, Japan, and Canada, the Trump administration has already signaled to the rest of the world that old alliances and coordination avenues are up for revision. There are two outcomes that we can see emerging over the course of the next decade. First, U.S. leadership will become aware of the systemic constraints under which they operate, and trade with China will continue – albeit with limitations and variations. However, such trade will not reduce the geopolitical tensions, nor will it prevent a military conflict. In facts, the probability of military conflict may increase even as trade between China and the U.S. remains steady. Second, U.S. leadership will fail to correctly assess that they operate in a multipolar world and will give up the highlighted trade gains from Diagram 2 to economic rivals such as Europe and Japan. Given our methodological adherence to constraint-based forecasting, we highly doubt that the latter scenario is likely. Bottom Line: The China-U.S. conflict is not a replay of the Cold War. Systemic pressures from global multipolarity will force the U.S. to continue to trade with China, with limitations on exchanges in emergent, dual-use technologies that China will nonetheless source from other technologically advanced countries. This will create a complicated but exciting world where geopolitics will cease to be seen as exogenous to investing. A risk to the sanguine conclusion is that the historical record is applicable to today, but that the hour is late, not early. It is already July 26, 1941 – when U.S. abrogated all trade with Japan – not 1930. As such, we do not have another decade of trade between U.S. and China remaining, we are at the end of the cycle. While this is a risk, it is unlikely. American policymakers would essentially have to be willing to risk a military conflict with China in order to take the trade war to the same level they did with Japan. It is an objective fact that China has meaningfully stepped up aggressive foreign policy in the region. But unlike Japan in 1941, China has not outright invaded any countries over the past decade. As such, the willingness of the public to support such a conflict is unclear, with only 21% of Americans considering China a top threat to the U.S. Investment Implications This analysis is not meant to be optimistic. First, the U.S. and China will continue to be rivals even if the economic relationship between them does not lead to global bifurcation. For one, China continues to be – much like Germany in the early twentieth century – concerned with access to external markets on which 19.5% of its economy still depend. China is therefore developing a modern navy and military not because it wants to dominate the rest of the world but because it wants to dominate its near abroad, much as the U.S. wanted to, beginning with the Monroe Doctrine. This will continue to lead to Chinese aggression in the South and East China Seas, raising the odds of a conflict with the U.S. Navy. Given that the Thucydides Trap narrative remains cogent, investors should look to overweight S&P 500 aerospace and defense stocks relative to global equity markets. An alternative way that one could play this thesis is by developing a basket of global defense stocks. Multipolarity may create constraints to trade protectionism, but it engenders geopolitical volatility and thus buoys defense spending. Second, we would not expect another uptick in globalization. Multipolarity may make it difficult for countries to completely close off trade with a rival, but globalization is built on more than just trade between rivals. Globalization requires a high level of coordination among great powers that is only possible under hegemonic conditions. Chart 9 shows that the hegemony of the British and later American empires created a powerful tailwind for trade over the past two hundred years. Chart 9The Apex Of Globalization Is Behind Us

The Apex Of Globalization Is Behind Us

The Apex Of Globalization Is Behind Us

The Apex of Globalization has come and gone – it is all downhill from here. But this is not a binary view. Foreign trade will not go to zero. The U.S. and China will not completely seal each other’s sphere of influence behind a Silicon Curtain. Instead, we focus on five investment themes that flow from a world that is characterized by the three trends of multipolarity, Sino-U.S. geopolitical rivalry, and apex of globalization: Europe will profit: As the U.S. and China deepen their enmity, we expect some European companies to profit. There is some evidence that the investment community has already caught wind of this trend, with European equities modestly outperforming their U.S. counterparts whenever trade tensions flared up in 2019 (Chart 10). Given our thesis, however, it is unlikely that the U.S. would completely lose market share in China to Europe. As such, we specifically focus on tech, where we expect the U.S. and China to ramp up non-tariff barriers to trade regardless of systemic pressures to continue to trade. A strategic long in the secularly beleaguered European tech companies relative to their U.S. counterparts may therefore make sense (Chart 11). Chart 10Europe: A Trade War Safe Haven

Europe: A Trade War Safe Haven

Europe: A Trade War Safe Haven

Chart 11Is Europe Really This Incompetent?

Is Europe Really This Incompetent?

Is Europe Really This Incompetent?

USD bull market will end: A trade war is a very disruptive way to adjust one’s trade relationship. It opens one to retaliation and thus the kind of relative losses described in this analysis. As such, we expect that U.S. to eventually depreciate the USD, either by aggressively reversing 2018 tightening or by coercing its trade rivals to strengthen their currencies. Such a move will be yet another tailwind behind the diversification away from the USD as a reserve currency, a move that should benefit the euro. Bull market in capex: The re-wiring of global manufacturing chains will still take place. The bad news is that multinational corporations will have to dip into their profit margins to move their supply chains to adjust to the new geopolitical reality. The good news is that they will have to invest in manufacturing capex to accomplish the task. One way to articulate this theme is to buy an index of semiconductor capital companies (AMAT, LRCX, KLAC, MKSI, AEIS, BRIKS, and TER). Given the highly cyclical nature of capital companies, we would recommend an entry point once trade tensions subside and green shoots of global growth appear. “Non-aligned” markets will benefit: The last time the world was multipolar, great powers competed through imperialism. This time around, a same dynamic will develop as countries seek to replicate China’s “Belt and Road Initiative.” This is positive for frontier markets. A rush to provide them with exports and services will increase supply and thus lower costs, providing otherwise forgotten markets with a boon of investments. India, and Asia-ex-China more broadly, stand as intriguing alternatives to China, especially with the current administration aggressively reforming to take advantage of the rewiring of global manufacturing chains. Capital markets will remain globalized: With interest rates near zero in much of the developed world and the demographic burden putting an ever-greater pressure on pension plans to generate returns, the search for yield will continue to be a powerful drive that keeps capital markets globalized. Limitations are likely to grow, especially when it comes to cross-border private investments in dual-use technologies. But a completely bifurcation of capital markets is unlikely. The world we are describing is one where geopolitics will play an increasingly prominent role for global investors. It would be convenient if the world simply divided into two warring camps, leaving investors with neatly separated compartments that enabled them to go back to ignoring geopolitics. This is unlikely. Rather, the world will resemble the dynamic years at the end of the nineteenth century, a rough-and-tumble era that required a multi-disciplinary approach to investing. Marko Papic, Consulting Editor, BCA Research Chief Strategist, Clocktower Group Marko@clocktowergroup.com Footnotes 1 Please see BCA Research Geopolitical Strategy, “Power And Politics In East Asia: Cold War 2.0?,” September 25, 2012, “Sino-American Conflict: More Likely Than You Think,” October 4, 2013, “The Great Risk Rotation,” December 11, 2013, and “Strategic Outlook 2014 – Stay The Course: EM Risk – DM Reward,” January 23, 2014, “Underestimating Sino-American Tensions,” November 6, 2015, “The Geopolitics Of Trump,” December 2, 2016, “How To Play The Proxy Battles In Asia,” March 1, 2017, and others available at gps.bcaresearch.com or upon request. 2 Please see German Historical Institute, “Bernhard von Bulow on Germany’s ‘Place in the Sun’” (1897), available at http://germanhistorydocs.ghi-dc.org/ 3 See Graham Allison, Destined For War: Can America and China Escape Thucydides’s Trap? (New York: Houghton Miffin Harcourt, 2017). 4 The three cases are Spain taking over from Portugal in the sixteenth century, the U.S. taking over from the U.K. in the twentieth century, and Germany rising to regional hegemony in Europe in the twenty-first century. 5 Duncan Snidal, “Relative Gains and the Pattern of International Cooperation,” The American Political Science Review, 85:3 (September 1991), pp. 701-726. 6 We do not review Snidal’s excellent game theory formal modeling in this paper as it is complex and detailed. However, we highly encourage the intrigued reader to pursue the study on their own. 7 See Charles P. Kindleberger, The World In Depression, 1929-1939 (Berkeley: University of California Press, 2013). 8 Joanne Gowa and Edward D. Mansfield, “Power Politics and International Trade,” The American Political Science Review, 87:2 (June 1993), pp. 408-420. 9 See Ernest Edwin Williams, Made in Germany (reprint, Ithaca: Cornell University Press), available at https://archive.org/details/cu31924031247830. 10 Quoted in Margaret MacMillan, The War That Ended Peace (Toronto: Allen Lane, 2014). 11 Peter Liberman, “Trading with the Enemy: Security and Relative Economic Gains,” international Security, 21:1 (Summer 1996), pp. 147-175. 12 Although France and Russia overcame even greater bitterness due to the ideological differences between a republic founded on a violent uprising against its aristocracy – France – and an aristocratic authoritarian regime – Russia. 13 See James Morrow, “When Do ‘Relative Gains’ Impede Trade?” The Journal of Conflict Resolution, 41:1 (February 1997), pp. 12-37; and Jack S. Levy and Katherine Barbieri, “Trading With the Enemy During Wartime,” Security Studies, 13:3 (December 2004), pp. 1-47.

Highlights MARKET FORECASTS

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Investment Strategy: Markets have entered a “show me” phase. Better economic data and meaningful progress on the trade negotiations will be necessary for stocks to move sustainably higher. We think both preconditions will be realized. Until then, risk assets could come under pressure. Global Asset Allocation: Investors should overweight stocks relative to bonds over a 12-month horizon, but maintain higher-than-normal cash positions in the near term as a hedge against downside risks. Equities: EM and European stocks will outperform once global growth bottoms out. Cyclical sectors, including financials, will also start to outperform defensives when the growth cycle turns. Bonds: Central banks will remain dovish, but yields will nevertheless rise modestly on the back of stronger global growth. Favor high-yield corporate credit over government bonds. Currencies: As a countercyclical currency, the U.S. dollar should peak later this year. Commodities: Oil and industrial metals prices will move higher. Gold prices have entered a holding pattern, but should shine again late next year or in 2021 when inflation finally breaks out. Feature Dear Client, In lieu of this report, I hosted a webcast on Monday, October 7th at 10:00 AM EDT, where I discussed the major investment themes and views I see playing out for the rest of the year and beyond. Best regards, Peter Berezin, Chief Global Strategist I. Global Macro Outlook A Testing Phase For The Global Economy The global economy has reached a critical juncture. Growth has been slowing since early 2018, reaching what many would regard as “stall speed.” This is the point where economic weakness begins to feed on itself, potentially triggering a recession. Will the growth slowdown worsen? Our guess is that it won’t. Global financial conditions have eased significantly over the past four months, thanks in part to the dovish pivot by most central banks. Looser financial conditions usually bode well for global growth (Chart 1). Our global leading indicator has hooked up, mainly due to a marginal improvement in emerging markets’ data (Chart 2). Chart 1Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

Chart 2Global LEI Has Moved Off Its Lows

Global LEI Has Moved Off Its Lows

Global LEI Has Moved Off Its Lows

An important question is whether the weakness in the manufacturing sector will spread to the much larger services sector. There is some evidence that this is happening, with yesterday’s weaker-than-expected ISM non-manufacturing release being the latest example. Nevertheless, the deceleration in service sector activity has been limited so far (Chart 3). Even in Germany, with its large manufacturing base, the service sector PMI remains in expansionary territory. This is a key difference with the 2001/02 and 2008/09 periods, when service sector activity collapsed in lockstep with manufacturing activity. Chart 3AThe Service Sector Has Softened Less Than Manufacturing (I)

The Service Sector Has Softened Less Than Manufacturing (I)

The Service Sector Has Softened Less Than Manufacturing (I)

Chart 3BThe Service Sector Has Softened Less Than Manufacturing (II)

The Service Sector Has Softened Less Than Manufacturing (II)

The Service Sector Has Softened Less Than Manufacturing (II)

The Drive-By Slowdown If one were to ask most investors the reasons behind the manufacturing slowdown, they would probably cite the trade war or the Chinese deleveraging campaign. These are both valid reasons, but there is a less well-known culprit: autos. According to WardsAuto, global auto sales fell by over 5% in the first half of the year, by far the biggest decline since the Great Recession (Chart 4). Production dropped by even more. Chart 4Weakness In The Auto Sector Has Exacerbated The Manufacturing Downturn

Weakness In The Auto Sector Has Exacerbated The Manufacturing Downturn

Weakness In The Auto Sector Has Exacerbated The Manufacturing Downturn

Chart 5U.S. Auto Demand Is Recovering

U.S. Auto Demand Is Recovering

U.S. Auto Demand Is Recovering

The weakness in the global auto sector reflects a variety of factors. New stringent emission requirements, expiring tax breaks, lagged effects from tighter auto loan lending standards, and trade tensions have all played a role. In addition, the decline in gasoline prices in 2015/16 probably brought forward some automobile purchases. This suggests that the 2015/16 global manufacturing downturn may have helped sow the seeds for the current one. The fact that automobile output is falling faster than sales is encouraging because it means that excess inventories are being worked off. U.S. auto loan lending standards have started to normalize, with banks reporting stronger demand for auto loans in the latest Senior Loan Officer Survey (Chart 5). In China, auto sales have troughed after having declined by as much as 14% earlier this year (Chart 6). The Chinese automobile ownership rate is a fifth of what it is in the U.S., a quarter of what it is in Japan, and a third of what it is in Korea (Chart 7). Given the low starting point, Chinese auto sales are likely to resume their secular uptrend. Chart 6Auto Sector In China Is Finding A Floor

Auto Sector In China Is Finding A Floor

Auto Sector In China Is Finding A Floor

Chart 7China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

China: Structural Outlook For Autos Is Bright

The Trade War: Tracking Towards A Détente? Chart 8A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

Manufacturing cycles typically last about three years – 18 months of slowing growth followed by 18 months of rising growth (Chart 8). To the extent that the global manufacturing PMI peaked in the first half of 2018, we should be nearing the end of the current downturn. Of course, much depends on policy developments. As we go to press, high-level negotiations between the U.S. and China have resumed. While it is impossible to predict the outcome of these talks, it does appear that both sides have an incentive to de-escalate the trade conflict. President Trump gets much better marks from voters on his management of the economy than on anything else, including his handling of trade negotiations with China (Chart 9). A protracted trade war would hurt U.S. growth, while weakening the stock market. Both would undermine Trump’s re-election prospects. Chart 9Trump Gets Reasonably High Marks On His Handling Of The Economy, But Not Much Else

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Chart 10Who Will Win The 2020 Democratic Nomination?

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

Fourth Quarter 2019 Strategy Outlook: A "Show Me" Market

China also wants to bolster growth. As difficult as it has been for the Chinese leadership to deal with Donald Trump, trying to secure a trade deal with him after he has been re-elected would be even more challenging. This would especially be the case if Trump thought that the Chinese had tried to sabotage his re-election bid. Even if Trump were to lose the election, it is not clear that China would end up with someone more pliant to deal with on trade matters. Does the Chinese government really want to negotiate over environmental standards and human rights with President Warren, who betting markets now think has a better chance of becoming the Democratic nominee than Joe Biden (Chart 10)? The Democrats’ initiative to impeach President Trump make a trade resolution somewhat more likely. First, it brings attention to Joe Biden’s (and his son’s) own dubious dealings in Ukraine, thus delivering a blow to China’s preferred U.S. presidential candidate. Second, it makes Trump more inclined to want to put the China spat behind him in order to focus his energies on domestic matters. More Chinese Stimulus? Strategically, China has a strong incentive to stimulate its economy in order to prop up growth and gain greater leverage in the trade negotiations. The Chinese credit impulse bottomed in late 2018. The impulse leads Chinese nominal manufacturing output and most other activity indicators by about nine months (Chart 11). So far, the magnitude of China’s credit/fiscal easing has come nowhere close to matching the stimulus that was unleashed on the economy both in 2015/16 and 2008/09. This is partly because the authorities are more worried about excessive debt levels today than they were back then, but it is also because the economy is in better shape. The shock from the trade war has not been nearly as bad as the Great Recession – recall that Chinese exports to the U.S. are only 2.7% of GDP in value-added terms. Unlike in 2015/16, when China lost over $1 trillion in external reserves, capital outflows have remained muted this time around (Chart 12). Chart 11Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Chinese Stimulus Should Boost Global Growth

Chart 12China: No Major Capital Outflows

China: No Major Capital Outflows

China: No Major Capital Outflows

Better-than-expected Chinese PMI data released earlier this week offers a glimmer of hope. Nevertheless, in light of the disappointing August activity numbers, China is likely to increase the pace of stimulus in the coming months. The authorities have already reduced bank reserve requirements. We expect them to cut policy rates further in the coming months. They will also front-load local government bond issuance, which should help boost infrastructure spending. European Growth Should Improve A pickup in global growth will help Europe later this year. Germany, with its trade-dependent economy, will benefit the most. Chart 13Spreads Have Come In Across Southern Europe

Spreads Have Come In Across Southern Europe

Spreads Have Come In Across Southern Europe

Chart 14Faster Money Growth Bodes Well For GDP Growth In The Euro Area

Faster Money Growth Bodes Well For GDP Growth In The Euro Area

Faster Money Growth Bodes Well For GDP Growth In The Euro Area