China

Highlights So What? Economic stimulus will encourage key nations to pursue their self-interest – keeping geopolitical risk high. Why? The U.S. is still experiencing extraordinary strategic tensions with China and Iran … simultaneously. The Trump-Xi summit at the G20 is unlikely to change the fact that the United States is threatening China with total tariffs and a technology embargo. The U.S. conflict with Iran will be hard to keep under wraps. Expect more fireworks and oil volatility, with a large risk of hostilities as long as the U.S. maintains stringent oil sanctions. All of our GeoRisk indicators are falling except for those of Germany, Turkey and Brazil. This suggests the market is too complacent. Maintain tactical safe-haven positioning. Feature “That’s some catch, that Catch-22,” he observed. “It’s the best there is,” Doc Daneeka agreed. -Joseph Heller, Catch-22 (1961) One would have to be crazy to go to war. Yet a nation has no interest in filling its military’s ranks with lunatics. This is the original “Catch-22,” a conundrum in which the only way to do what is individually rational (avoid war) is to insist on what is collectively irrational (abandon your country). Or the only way to defend your country is to sacrifice yourself. This is the paradox that U.S. President Donald Trump faces having doubled down on his aggressive foreign policy this year: if he backs away from trade war to remove an economic headwind that could hurt his reelection chances, he sacrifices the immense leverage he has built up on behalf of the United States in its strategic rivalry with China. “Surrender” would be a cogent criticism of him on the campaign trail: a weak deal will cast him as a pluto-populist, rather than a real populist – one who pandered to China to give a sop to Wall Street and the farm lobby just like previous presidents, yet left America vulnerable for the long run. Similarly, if President Trump stops enforcing sanctions against Iranian oil exports to reduce the threat of a conflict-induced oil price shock that disrupts his economy, then he reduces the United States’s ability to contain Iran’s nuclear and strategic advances in the wake of the 2015 nuclear deal that he canceled. The low appetite for American involvement in the region will be on full display for the world to see. Iran will have stared down the Great Satan – and won. In both cases, Trump can back down. Or he can try to change the subject. But with weak polling and yet a strong economy, the point is to direct voters’ attention to foreign policy. He could lose touch with his political base at the very moment that the Democrats reconnect with their own. This is not a good recipe for reelection. More important – for investors – why would he admit defeat just as the Federal Reserve is shifting to countenance the interest rate cuts that he insists are necessary to increase his economic ability to drive a hard bargain with China? Why would he throw in the towel as the stock market soars? And if Trump concludes a China deal, and the market rises higher, will he not be emboldened to put more economic pressure on Mexico over border security … or even on Europe over trade? The paradox facing investors is that the shift toward more accommodative monetary policy (and in some cases fiscal policy) extends the business cycle and encourages political leaders to pursue their interests more intently. China is less likely to cave to Trump’s demands as it stimulates. The EU does not need to fear a U.K. crash Brexit if its economy rebounds. This increases rather than decreases the odds of geopolitical risks materializing as negative catalysts for the market. Similarly, if geopolitical risk falls then the need for stimulus falls and the market will be disappointed. The result is still more volatility – at least in the near term. The G20 And 2020 As we go to press the Democratic Party’s primary election debates are underway. The progressive wave on display highlights the overarching takeaway of the debates: the U.S. election is now an active political (and geopolitical) risk to the equity market. A truly positive surprise at the G20 would be a joint statement by Trump and Xi plus some tariff rollback. Whenever Trump’s odds of losing rise, the U.S. domestic economy faces higher odds of extreme policy discontinuity and uncertainty come 2021, with the potential for a populist-progressive agenda – a negative for financials, energy, and probably health care and tech.

Chart 1

Yet whenever Trump’s odds of winning rise, the world faces higher odds of an unconstrained Trump second term focusing on foreign and trade policy – a potentially extreme increase in global policy uncertainty – without the fiscal and deregulatory positives of his first term. We still view Trump as the favored candidate in this race (at 55% chance of reelection), given that U.S. underlying domestic demand is holding up and the labor market has not been confirmed to be crumbling beneath the consumer’s feet. Still Chart 1 highlights that Trump’s shift to more aggressive foreign and trade policy this spring has not won him any additional support – his approval rating has been flat since then. And his polling is weak enough in general that we do not assign him as high of odds of reelection as would normally be afforded to a sitting president on the back of a resilient economy. This raises the question of whether the G20 will mark a turning point. Will Trump attempt to deescalate his foreign conflicts? Yes, and this is a tactical opportunity. But we see no final resolution at hand. With China, Trump’s only reason to sign a weak deal would be to stem a stock market collapse. With Iran, Trump is no longer in the driver’s seat but could be forced to react to Iranian provocations. Bottom Line: Trump’s polling has not improved – highlighting the election risk – but weak polling amid a growing economy and monetary easing is not a recipe for capitulating to foreign powers. The Trump-Xi Summit On China the consensus on the G20 has shifted toward expecting an extension of talks and another temporary tariff truce. If a new timetable is agreed, it may be a short-term boon for equities. But we will view it as unconvincing unless it is accompanied with a substantial softening on Huawei or a Trump-Xi joint statement outlining an agreement in principle along with some commitment of U.S. tariff rollback. Otherwise the structural dynamic is the same: Trump is coercing China with economic warfare amid a secular increase in U.S.-China animosity that is a headwind for trade and investment. Table 1 shows that throughout the modern history of U.S.-China presidential-level summits, the Great Recession marked a turning point: since then, bilateral relations have almost always deteriorated in the months after a summit, even if the optics around the summit were positive. Table 1U.S.-China Leaders Summits: A Chronology

The G20 Catch-22 ... GeoRisk Indicators Update: June 28, 2019

The G20 Catch-22 ... GeoRisk Indicators Update: June 28, 2019

The last summit in Buenos Aires was no exception, given that the positive aura was ultimately followed by a tariff hike and technology-company blacklistings. Of course, the market rallied for five months in between. Why should this time be the same? First, the structural factors undermining Sino-American trust are worse, not better, with Trump’s latest threats to tech companies. Second, Trump will ultimately resent any decision to extend the negotiations. China’s economy is rebounding, which in the coming months will deprive Trump of much of the leverage he had in H2 2018 and H1 2019. He will be in a weaker position if they convene in three months to try to finalize a deal. Tariff rollback will be more difficult in that context given that China will be in better shape and that tariffs serve as the guarantee that any structural concessions will be implemented. Bottom Line: Our broader view regarding the “end game” of the talks – on the 2020 election horizon – remains that China has no reason to implement structural changes speedily for the United States until Trump can prove his resilience through reelection. Yet President Trump will suffer on the campaign trail if he accepts a deal that lacks structural concessions. Hence we expect further escalation from where we are today, knowing full well that the G20 could produce a temporary period of improvement just as occurred on December 1, 2018. The Iran Showdown Is Far From Over Disapproval of Trump’s handling of China and Iran is lower than his disapproval rating on trade policy and foreign policy overall, suggesting that despite the lack of a benefit to his polling, he does still have leeway to pursue his aggressive policies to a point. A breakdown of these opinions according to key voting blocs – a proxy for Trump’s ability to generate support in Midwestern swing states – illustrates that his political base is approving on the whole (Chart 2).

Chart 2

Yet the conflict with Iran threatens Trump with a hard constraint – an oil price shock – that is fundamentally a threat to his reelection. Hence his decision, as we expected, to back away from the brink of war last week (he supposedly canceled air strikes on radar and missile installations at the last minute on June 21). He appears to be trying to control the damage that his policy has already done to the 2015 U.S.-Iran equilibrium. Trump has insisted he does not want war, has ruled out large deployments of boots on the ground, and has suggested twice this week that his only focus in trying to get Iran back into negotiations is nuclear weapons. This implies a watering down of negotiation demands to downplay Iran’s militant proxies in the region – it is a retreat from Secretary of State Mike Pompeo’s more sweeping 12 demands on Iran and a sign of Trump’s unwillingness to get embroiled in a regional conflict with a highly likely adverse economic blowback. The Iran confrontation is not over yet – policy-induced oil price volatility will continue. This retreat lacks substance if Trump does not at least secretly relax enforcement of the oil sanctions. Trump’s latest sanctions and reported cyberattacks are a sideshow in the context of an attempted oil embargo that could destabilize Iran’s entire economy (Charts 3 and 4). Similarly, Iran’s downing of a U.S. drone pales in comparison to the tanker attacks in Hormuz that threatened global oil shipments. What matters to investors is the oil: whether Iran is given breathing space or whether it is forced to escalate the conflict to try to win that breathing space.

Chart 3

Chart 4Iran’s Rial Depreciated Sharply

Iran's Rial Depreciated Sharply

Iran's Rial Depreciated Sharply

The latest data suggest that Iran’s exports have fallen to 300,000 barrels per day, a roughly 90% drop from 2018, when Trump walked away from the Iran deal. If this remains the case in the wake of the brinkmanship last week then it is clear that Iran is backed into a corner and could continue to snarl and snap at the U.S. and its regional allies, though it may pause after the tanker attacks. Chart 5More Oil Volatility To Come

More Oil Volatility To Come

More Oil Volatility To Come

Tehran also has an incentive to dial up its nuclear program and activate its regional militant proxies in order to build up leverage for any future negotiation. It can continue to refuse entering into negotiations with Trump in order to embarrass him – and it can wait until Trump’s approach is validated by reelection before changing this stance. After all, judging by the first Democratic primary debate, biding time is the best strategy – the Democratic candidates want to restore the 2015 deal and a new Democratic administration would have to plead with Iran, even to get terms less demanding than those in 2015. Other players can also trigger an escalation even if Presidents Trump and Rouhani decide to take a breather in their conflict (which they have not clearly decided to do). The Houthi rebels based in Yemen have launched another missile at Abha airport in Saudi Arabia since Trump’s near-attack on Iran, an action that is provocative, easily replicable, and not necessarily directly under Tehran’s control. Meanwhile OPEC is still dragging its feet on oil production to compensate for the Iranian losses, implying that the cartel will react to price rises rather than preempt them. The Saudis could use production or other means to stoke conflict. Bottom Line: Given our view on the trade war, which dampens global oil demand, we expect still more policy-induced volatility (Chart 5). We do not see oil as a one-way bet … at least not until China’s shift to greater stimulus becomes unmistakable. North Korea: The Hiccup Is Over Chart 6China Ostensibly Enforces North Korean Sanctions

China Ostensibly Enforces North Korean Sanctions

China Ostensibly Enforces North Korean Sanctions

The single clearest reason to expect progress between the U.S. and China at the G20 is the fact that North Korea is getting back onto the diplomatic track. North Korea has consistently been shown to be part of the Trump-Xi negotiations, unlike Taiwan, the South China Sea, Xinjiang, and other points of disagreement. General Secretary Xi Jinping took his first trip to the North on June 20 – the first for a Chinese leader since 2005 – and emphasized the need for historic change, denuclearization, and economic development. Xi is pushing Kim to open up and reform the economy in exchange for a lasting peace process – an approach that is consistent with China’s past policy but also potentially complementary with Trump’s offer of industrialization in exchange for denuclearization. President Trump and Kim Jong Un have exchanged “beautiful” letters this month and re-entered into backchannel discussions. Trump’s visit to South Korea after the G20 will enable him and President Moon Jae-In to coordinate for a possible third summit between Trump and Kim. Progress on North Korea fits our view that the failed summit in Hanoi was merely a setback and that the diplomatic track is robust. Trump’s display of a credible military threat along with Chinese sanctions enforcement (Chart 6) has set in motion a significant process on the peninsula that we largely expect to succeed and go farther than the consensus expects. It is a long-term positive for the Korean peninsula’s economy. It is also a positive factor in the U.S.-China engagement based on China’s interest in ultimately avoiding war and removing U.S. troops from the peninsula. From an investment point of view, an end to a brief hiatus in U.S.-North Korean diplomacy is a very poor substitute for concrete signs of U.S.-China progress on the tech front or opening market access. There has been nothing substantial on these key issues since Trump hiked the tariff rate in May. As a result, it is perfectly possible for the G20 to be a “success” on North Korea but, like the Buenos Aires summit on December 1, for markets to sell the news (Chart 7). Chart 7The Last Trade Truce Didn't Stop The Selloff

The Last Trade Truce Didn't Stop The Selloff

The Last Trade Truce Didn't Stop The Selloff

Chart 8China Needs A Final Deal To Solve This Problem

China Needs A Final Deal To Solve This Problem

China Needs A Final Deal To Solve This Problem

Bottom Line: North Korea is not a basis in itself for tariff rollback, but only as part of a much more extensive U.S.-China agreement. And a final agreement is needed to improve China’s key trade indicators on a lasting basis, such as new export orders and manufacturing employment, which are suffering amid the trade war. We expect economic policy uncertainty to remain elevated given our pessimistic view of U.S.-China trade relations (Chart 8). What About Japan, The G20 Host?

Chart 9

Japan faces underrated domestic political risk as Prime Minister Abe Shinzo approaches a critical period in his long premiership, after which he will almost certainly be rendered a “lame duck,” likely by the time of the 2020 Tokyo Olympics. The question is when will this process begin and what will the market impact be? If Abe loses his supermajority in the July House of Councillors election, then it could begin as early as next month. This is a real risk – because a two-thirds majority is always a tall order – but it is not extreme. Abe’s polling is historically remarkable (Chart 9). The Liberal Democratic Party and its coalition partner Komeito are also holding strong and remain miles away from competing parties (Chart 10). The economy is also holding up relatively well – real wages and incomes have improved under Abe’s watch (Chart 11). However, the recent global manufacturing slowdown and this year’s impending hike to the consumption tax in October from 8% to 10% are killing consumer confidence. Chart 10Japan's Ruling Coalition Is Strong

Japan's Ruling Coalition Is Strong

Japan's Ruling Coalition Is Strong

The collapse in consumer confidence is a contrary indicator to the political opinion polling. The mixed picture suggests that after the election Abe could still backtrack on the tax hike, although it would require driving through surprise legislation. He can pull this off in light of global trade tensions and his main objective of passing a popular referendum to revise the constitution and remilitarize the country. Chart 11Japanese Wages Up, But Consumer Confidence Diving

Japanese Wages Up, But Consumer Confidence Diving

Japanese Wages Up, But Consumer Confidence Diving

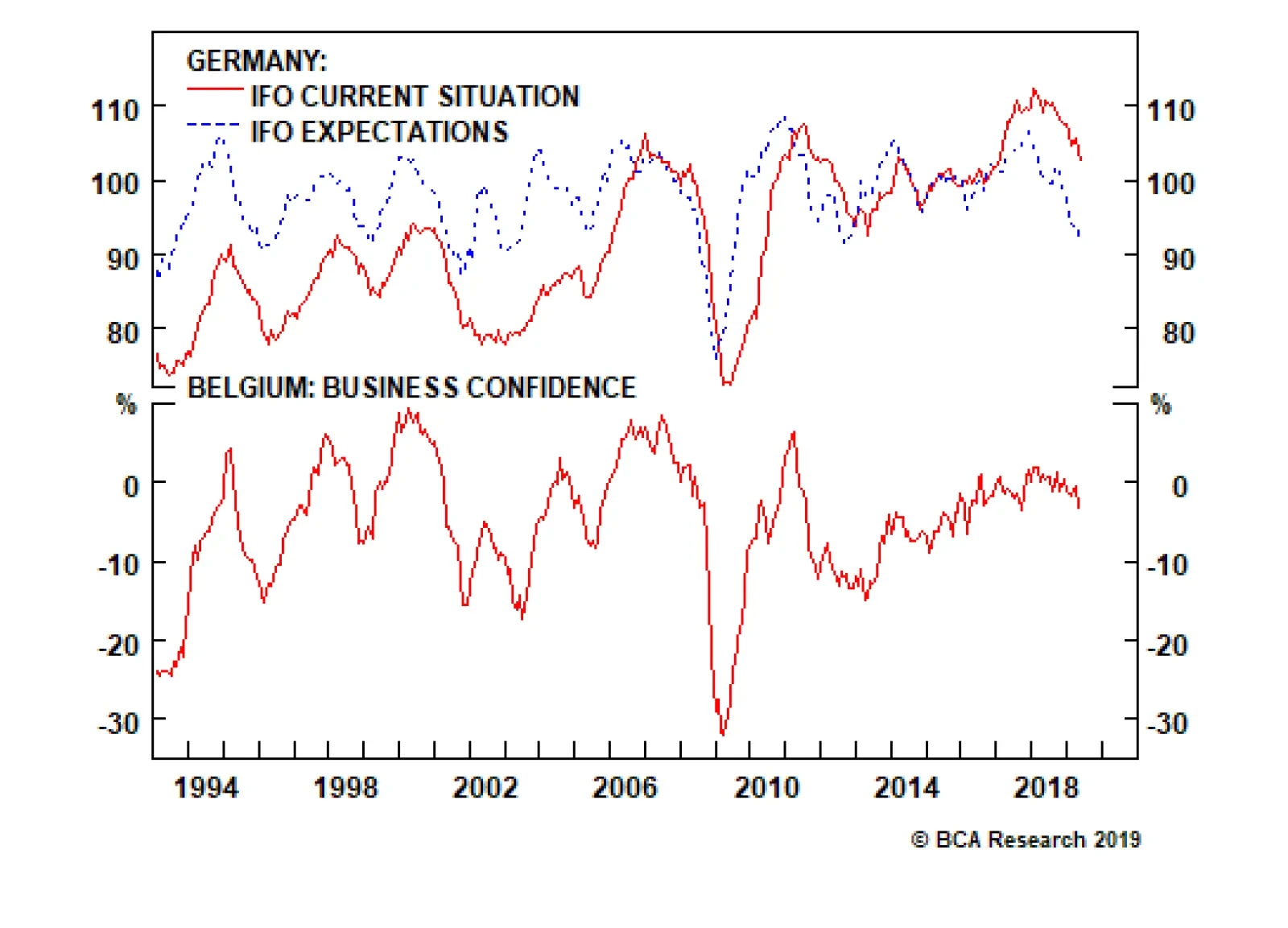

We would not be surprised if Japan secured a trade deal with the U.S. prior to China. Because Abe and the United States need to enhance their alliance, we continue to downplay the risk of a U.S.-Japan trade war. Bloomberg recently reported that President Trump was threatening to downgrade the U.S.-Japan alliance, with a particular grievance over the ever-controversial issue of the relocation of troops on Okinawa. We view this as a transparent Trumpian negotiating tactic that has no applicability – indeed, American military and diplomatic officials quickly rejected the report. We do see a non-trivial risk that Trump’s rhetoric or actions will hurt Japanese equities at some point this year, either as Trump approaches his desired August deadline for a Japan trade deal or if negotiations drag on until closer to his decision about Section 232 tariffs on auto imports on November 14. But our base case is that there will be either no punitive measures or only a short time span before Abe succeeds in negotiating them away. We would not be surprised if the Japanese secured a deal prior to any China deal as a way for the Trump administration to try to pressure China and prove that it can get deals done. This can be done because it could be a thinly modified bilateral renegotiation of the Trans-Pacific Partnership, which had the U.S. and Japan at its center. Bottom Line: Given the combination of the upper house election, the tax hike and its possible consequences, a looming constitutional referendum which poses risks to Abe, and the ongoing external threat of trade war and China tensions, we continue to see risk-off sentiment driving Japanese and global investors to hold then yen. We maintain our long JPY/USD recommendation. The risk to this view is that Bank of Japan chief Haruhiko Kuroda follows other central banks and makes a surprisingly dovish move, but this is not warranted at the moment and is not the base case of our Foreign Exchange Strategy. GeoRisk Indicators Update: June 28, 2019 Our GeoRisk indicators are sending a highly complacent message given the above views on China and Iran. All of our risk measures, other than our German, Turkish, and Brazilian indicators, are signaling a decrease geopolitical tensions. Investors should nonetheless remain cautious: Our German indicator, which has proven to be a good measure of U.S.-EU trade tensions, has increased over the first half of June (Chart 12). We expect Germany to continue to be subject to risk because of Trump’s desire to pivot to European trade negotiations in the wake of any China deal. The auto tariff decision was pushed off until November. We assign a 45% subjective probability to auto tariffs on the EU if Trump seals a final China deal. The reason it is not our base case is because of a lack of congressional, corporate, or public support for a trade war with Europe as opposed to China or Mexico, which touch on larger issues of national interest (security, immigration). There is perhaps a 10% probability that Trump could impose car tariffs prior to securing a China deal. Chart 12U.S.-EU Trade Tensions Hit Germany

U.S.-EU Trade Tensions Hit Germany

U.S.-EU Trade Tensions Hit Germany

Chart 13German Greens Overtaking Christian Democrats!

German Greens Overtaking Christian Democrats!

German Greens Overtaking Christian Democrats!

Germany is also an outlier because it is experiencing an increase in domestic political uncertainty. Social Democrat leader Andrea Nahles’ resignation on June 2 opened the door to a leadership contest among the SPD’s membership. This will begin next week and conclude on October 26, or possibly in December. The result will have consequences for the survivability of Merkel’s Grand Coalition – in case the SPD drops out of it entirely. Both Merkel and her party have been losing support in recent months – for the first time in history the Greens have gained the leading position in the polls (Chart 13). If the coalition falls apart and Merkel cannot put another one together with the Greens and Free Democrats, she may be forced to resign ahead of her scheduled 2021 exit date. The implication of the events with Trump and Merkel is that Germany faces higher political risk this year, particularly in Q4 if tariff threats and coalition strains coincide. Meanwhile, Brazilian pension reform has been delayed due to an inevitable breakdown in the ability to pass major legislation without providing adequate pork barrel spending. As for the rest of Europe, since European Central Bank President Mario Draghi’s dovish signal on June 18, all of our European risk indicators have dropped off. Markets rallied on the news of the ECB’s preparedness to launch another round of bond-buying monetary stimulus if needed, easing tensions in the region. Italian bond spreads plummeted, for instance. The Korean and Taiwanese GeoRisk indicators, our proxies for the U.S.-China trade war, are indicating a decrease in risk as the two sides moved to contain the spike in tensions in May. While Treasury Secretary Steve Mnuchin notes that the deal was 90% complete in May before the breakdown, there is little evidence yet that any of the sticking points have been removed over the past two weeks. These indicators can continue to improve on the back of any short-term trade truce at the G20. The Russian risk indicator has been hovering in the same range for the past two months. We expect this to break out on the back of increasing mutual threats between the U.S. and Russia. The U.S. has recently agreed to send an additional 1000 rotating troops to Poland, a move that Russia obviously deems aggressive. The Russian upper chamber has also unanimously supported President Putin’s decree to suspend the Intermediate Nuclear Forces treaty, in the wake of the U.S. decision to do so. This would open the door to developing and deploying 500-5500 km range land-based and ballistic missiles. According to the deputy foreign minister, any U.S. missile deployment in Europe will lead to a crisis on the level of the Cuban Missile Crisis. Russia has also sided with Iran in the latest U.S.-Iran tension escalation, denouncing U.S. plans to send an additional 1000 troops to the Middle East and claiming that the shot-down U.S. drone was indeed in Iranian airspace. We anticipate the Russian risk indicator to go up as we expect Russia to retaliate in some way to Poland and to take actions to encourage the U.S. to get entangled deeper into the Iranian imbroglio, which is ultimately a drain on the U.S. and a useful distraction that Russia can exploit. In Turkey, both domestic and foreign tensions are rising. First, the re-run of the Istanbul mayoral election delivered a big defeat for Turkey’s President Erdogan on his home turf. Opposition representative Ekrem Imamoglu defeated former Prime Minister Binali Yildirim for a second time this year on June 23 – increasing his margin of victory to 9.2% from 0.2% in March. This was a stinging rebuke to Erdogan and his entire political system. It also reinforces the fact that Erdogan’s Justice and Development Party (AKP) is not as popular as Erdogan himself, frequently falling short of the 50% line in the popular vote for elections not associated directly with Erdogan (Chart 14). This trend combined with his personal rebuke in the power base of Istanbul will leave him even more insecure and unpredictable.

Chart 14

Second, the G20 summit is the last occasion for Erdogan and Trump to meet personally before the July 31 deadline on Erdogan’s planned purchase of S-400 missile defenses from Russia. Erdogan has a chance to delay the purchase as he contemplates cabinet and policy changes in the wake of this major domestic defeat. Yet if Erdogan does not back down or delay, the U.S. will remove Turkey from the F-35 Joint Strike Fighter program, and may also impose sanctions over this purchase and possibly also Iranian trade. The result will hit the lira and add to Turkey’s economic woes. Geopolitically, it will create a wedge within NATO that Russia could exploit, creating more opportunities for market-negative surprises in this area. Finally, we expect our U.K. risk indicator to perk up, as the odds of a no-deal Brexit are rising. Boris Johnson will likely assume Conservative Party leadership and the party is moving closer to attempting a no-deal exit. We assign a 21% probability to this kind of Brexit, up from our previous estimate of 14%. It is more likely that Johnson will get a deal similar to Theresa May’s deal passed or that he will be forced to extend negotiations beyond October. Matt Gertken, Vice President Geopolitical Strategist mattg@bcaresearch.com Ekaterina Shtrevensky, Research Analyst ekaterinas@bcaresearch.com France: GeoRisk Indicator

France: GeoRisk Indicator

France: GeoRisk Indicator

U.K.: GeoRisk Indicator

U.K.: GeoRisk Indicator

U.K.: GeoRisk Indicator

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

What's On The Geopolitical Radar?

Chart 25

Section III: Geopolitical Calendar

Highlights Like in any currency board, Hong Kong dollar money supply is not fully backed by foreign currency (FX) reserves. Yet, the Hong Kong authorities have large FX reserves to defend the currency peg for now. Regardless, mounting capital outflows and the ensuing currency defense will lead to higher interest rates. Contrary to Hong Kong, Singapore has a flexible exchange rate regime and will begin easing monetary policy soon. Interest rates in Singapore will drop relative to Hong Kong. We are therefore reiterating our short Hong Kong / long Singaporean property stocks strategy. Feature The recent popular protests in Hong Kong against the extradition bill will likely mark a regime shift – not only in the territory’s socio-political dynamics but also in its financial outlook. It seems the local authorities are still considering an adoption of the extradition bill. For now, the bill has been suspended, but it has not been withdrawn outright. In light of elevated political uncertainty over the one-country, two-systems model, it is reasonable to assume that capital outflows from Hong Kong will rise in the coming year or so. In light of elevated political uncertainty over the one-country, two-systems model, it is reasonable to assume that capital outflows from Hong Kong will rise in the coming year or so. The question therefore becomes whether or not the Hong Kong Monetary Authority (HKMA) has sufficient foreign currency (FX) reserves to defend the Hong Kong dollar’s peg. Even though Hong Kong's broad money supply is not fully backed by FX reserves, we see no major risk to the currency peg at the moment. That said, mounting capital outflows will necessitate higher interest rates, as least relative to U.S. ones, to defend the peg. This is negative for Hong Kong’s property market and share prices. Are Hong Kong Dollars Fully Backed By FX Reserves? Hong Kong operates a linked-exchange rate system, which stipulates that its monetary base must be fully backed by FX reserves. The monetary base includes (Table I-1): The balance of the clearing accounts of banks kept with the HKMA (called the Aggregate Balance, which represents commercial banks’ excess reserves). Exchange Fund bills and notes – securities issued by the Exchange Fund to manage excess reserves/liquidity in the interbank market. Certificates of Indebtedness which are equivalent to currency in circulation. These certificates are held by note-issuing banks in exchange for their FX deposits at the Exchange Fund. The Exchange Fund is a balance sheet vehicle of the HKMA. Government-issued coins in circulation.

Chart I-

Presently, Hong Kong’s FX reserves-to-monetary base ratio is 2.2 (Chart I-1on page 1). This ratio is well above the stipulated currency board rule of one: a unit of monetary base can be issued only when it is backed by an equivalent foreign currency asset. Chart I-1HK: FX Coverage Of Monetary Base Is Well Above 1

HK: FX Coverage Of Monetary Base Is Well Above 1

HK: FX Coverage Of Monetary Base Is Well Above 1

The reason the ratio is currently more than double where it technically should be is because the HKMA’s foreign exchange reserves also include the fiscal authorities’ foreign currency deposits at the Exchange Fund. Hence, the large pool of fiscal assets converted into foreign currency and sitting in the Exchange Fund has pushed the monetary base’s coverage ratio above two. As of December 31, 2018, the Exchange Fund’s foreign currency assets consisted of HK$743 billion of its own foreign currency reserves (net FX reserves), HK$1.17 trillion of the fiscal authorities’ foreign currency deposits, and HK$485 billion of foreign currency deposits by money issuing commercial banks (Table I-1). However, broad money supply in Hong Kong is not fully backed by foreign currency reserves (Chart I-2). At 0.45, this coverage ratio entails that each HK dollar of broad money supply is backed by 0.45 USD foreign currency reserves within the Exchange Fund. Broad money supply includes currency in circulation, demand, savings and time deposits, and negotiable certificates of deposits (NCDs) issued by licensed banks. Chart I-2HK: FX Coverage Of HK Dollars Is Only 0.45

HK: FX Coverage Of HK Dollars Is Only 0.45

HK: FX Coverage Of HK Dollars Is Only 0.45

Crucially, broad money supply does not include commercial banks’ reserves at the central bank in any economy, including Hong Kong. The pertinent measure of any exchange rate backing is the ratio of FX reserves to broad money supply (all local currency deposits plus cash in circulation). The motive is that households and companies can use not only cash in circulation but also their deposits to acquire foreign currency. With the ratio standing at 0.45, the Hong Kong monetary authorities do not have sufficient amounts of U.S. dollars to guarantee the exchange of each unit of local currency (cash in circulation and all deposits) into U.S. dollars in the event of a full-blown flight out of HK dollars. It is essential to clarify that the monetary authorities in Hong Kong have not deviated from the original framework of the currency board. This exchange rate mechanism was devised in 1983 in such a way that only the monetary base – not broad money supply – was supposed to be backed by foreign currency. In short, any currency board entails that only the monetary base – not broad money supply - is backed by FX reserves. Hong Kong is not an exception. Nevertheless, there is widespread perception in the financial community and among economists that all Hong Kong dollars are backed by foreign currency reserves, which is incorrect. Like in any banking system, when commercial banks in Hong Kong grant loans or buy assets from non-banks, they create local currency deposits “out of thin air.” These deposits are not backed by foreign currency, and commercial banks that create these deposits are not obliged to deposit FX reserves at the Exchange Fund. The credit boom in Hong Kong has accelerated since 2009 (Chart I-3, top panel). Consistently, since that time, the amount of local currency deposits has mushroomed – these deposits are not backed by foreign currency (Chart I-3, bottom panel). Chart I-3Banks' Loans And Deposit Growth Go Hand-In-Hand

Banks' Loans And Deposit Growth Go Hand-In-Hand

Banks' Loans And Deposit Growth Go Hand-In-Hand

On the whole, the currency board system in Hong Kong and elsewhere cannot guarantee full convertibility of broad money supply (all types of deposits). Therefore, these currency regimes are ultimately based on confidence. If and when confidence in the exchange rate plummets and economic agents rush to exchange a large share of their local currency cash in circulation and deposits into foreign currency, the monetary authorities’ FX reserves will not be sufficient. That said, there is presently no basis to argue that close to 45% of Hong Kong broad money supply (cash and coins in circulation and deposits of all types) is poised to panic-flood the currency market. Hence, we do not foresee a de-pegging of the HKD exchange rate for now. The currency will continue to trade within its HKD/USD 7.75-7.85 band. Bottom Line: Like in any currency board, the Hong Kong dollars are not fully backed by its FX reserves. However, the Hong Kong authorities have large FX reserves to defend the currency peg for some time. Liquidity Strains? According to the Impossible Trinity thesis, in an economy with an open capital account, the monetary authorities can control either interest rates or the exchange rate, but not both simultaneously. Provided Hong Kong has both an open capital account and a fixed exchange rate, the monetary authorities have little control over interest rates. Balance-of-payment (BoP) dynamics determine whether the HKMA has to buy or sell foreign currency to preserve the exchange rate peg. When the BoP is in surplus, the HKMA accumulates FX reserves, and vice versa. The odds are rising that Hong Kong will begin experiencing capital outflows due to heightening political uncertainty over the one-country, two-systems model. Consistently, the BoP will swing from recurring surpluses to deficits and the HKMA will have to finance them by selling FX reserves (Chart I-4). By doing so, the monetary authorities will drain banks’ excess reserves, thereby tightening interbank liquidity. Chart I-4Balance Of Payments And FX Reserves

Balance Of Payments And FX Reserves

Balance Of Payments And FX Reserves

Chart I-5Falling Excess Reserves = Higher Interbank Rates

Falling Excess Reserves = Higher Interbank Rates

Falling Excess Reserves = Higher Interbank Rates

Notably, the HKMA’s FX reserves have plateaued, commercial banks’ excess reserves (the Aggregate Balance at the HKMA) have shrunk and money market rates have risen since 2016 (Chart I-5). Importantly, the latter has continued, even as U.S. interest rates have dropped over the past six months (Chart I-5, bottom panel). These dynamics are set to continue. To defend the HKD’s fixed exchange rate, interest rates in Hong Kong should rise and stay above those in the U.S. This will be the equivalent of pricing in a risk premium in Hong Kong rates due to higher political uncertainty in domestic politics as well as the ongoing U.S.-China trade confrontation. To defend the HKD’s fixed exchange rate, interest rates in Hong Kong should rise and stay above those in the U.S. On a positive note, the HKMA has ample room to mitigate liquidity strains resulting from FX interventions. In years when the BoP was in surplus, to prevent HKD appreciation the authorities purchased substantial amounts of U.S. dollars. As a result, the aggregate balance/excess reserves swelled, and Exchange Fund bills and notes were issued to absorb excess reserves (Chart I-6). Chart I-6HK Authorities Have Large Liquidity Firepower

HK Authorities Have Large Liquidity Firepower

HK Authorities Have Large Liquidity Firepower

Going forward, with capital outflows causing tightening liquidity, the HKMA can redeem its own bills and notes to replenish the Aggregate Balance. This will ease interbank liquidity and preclude interest rates from shooting up dramatically. The HKMA’s liquidity firepower is sizable: the amount of Exchange Fund bills and notes is more than HK$1 trillion. This compares with aggregate balance (excess reserves) of HK$55 billion. Hence, potential interbank liquidity is HK$1.1 trillion (the Aggregate Balance plus the Exchange Fund’s bills and notes) (Chart I-6, top panel). There is no way to guesstimate potential capital outflows from Hong Kong. Hence, it is difficult to know what the equilibrium level of the interest rate spread over U.S. rates will be. The market will be re-balancing continuously, and the interest rate differential will fluctuate – i.e., it will be a moving target that ensures the fixed value of the currency. Bottom Line: Odds are that market-based interest rates in Hong Kong have to rise and stay above the U.S. ones for now. Heading Into Recession? With non-financial private sector debt close to 300% of GDP (Chart I-7) and property/construction and financial services sectors accounting for a large share of the economy, the Hong Kong economy is extremely sensitive to interest rates. Chart I-7Hong Kong: Leverage And Debt Servicing

Hong Kong: Leverage And Debt Servicing

Hong Kong: Leverage And Debt Servicing

Chart I-8HK Economy Is In A Cyclical Downtrend

HK Economy Is In A Cyclical Downtrend

HK Economy Is In A Cyclical Downtrend

Economic conditions have already been worsening, and any further rise in interest rates will escalate the economic downtrend: Private credit growth has decelerated and is probably heading into contraction (Chart I-8, top panel). The property market is one of the most expensive in the world. Property transactions have plunged and real estate prices will likely deflate (Chart I-8, middle panels). China’s weakening economy and subsiding Hong Kong business and investor confidence will hurt domestic demand. Retail sales volumes are already contracting (Chart I-8, bottom panel). Investment Implications The interest rate differential between Hong Kong and the U.S. has recently become positive after two and a half years of lingering below zero (Chart I-9). Odds are that it will remain positive at least over the next couple years. Therefore, even if U.S. interest rates decline further, Hong Kong rates will not. This has major investment ramifications: Hong Kong stocks will likely underperform U.S. and EM equity benchmarks, as its interest rate differential with the U.S. stays on the positive side and widens further (Chart I-10). Chart I-9HK Interest Rate Spread Over U.S. Will Rise And Stay Positive

HK Interest Rate Spread Over U.S. Will Rise And Stay Positive

HK Interest Rate Spread Over U.S. Will Rise And Stay Positive

Chart I-10Higher HK Interest Rates Herald HK Equity Underperformance

Higher HK Interest Rates Herald HK Equity Underperformance

Higher HK Interest Rates Herald HK Equity Underperformance

The MSCI Hong Kong stock index is composed of financials (36% of market cap) and property stocks (26% of market cap). Therefore, domestic stocks are very sensitive to interest rates. Hong Kong companies are also very exposed to mainland growth. A recovery in the latter is not yet imminent. As a market neutral trade, we are reiterating our short Hong Kong property / long Singapore property stocks strategy. Chart I-11Favor Singapore Stocks Versus Hong Kong Ones

Favor Singapore Stocks Versus Hong Kong Ones

Favor Singapore Stocks Versus Hong Kong Ones

All of this leads us to maintain our underweight stance on Hong Kong domestic stocks versus U.S. and EM equity indexes (Chart I-10). As a market neutral trade, we are reiterating our short Hong Kong property / long Singapore property stocks strategy. Hong Kong interest rates will rise above Singapore’s, leading to the former’s equity underperformance versus the latter across property, banks and probably the overall stock index (Chart I-11). For a more detailed discussion of Singapore, please see below. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Lin Xiang, Research Analyst linx@bcaresearch.com Footnotes

Highlights U.S. consumption remains robust despite the recent intensification of global growth headwinds. The G-20 meeting will not result in an escalation nor a major resolution of Sino-U.S. tensions. Kicking the can down the road is the most likely outcome. China’s reflationary efforts will intensify, impacting global growth in the second half of 2019. Fearful of collapsing inflation expectations, global central banks are easing policy, which is supporting global liquidity conditions and growth prospects. Bond yields have upside, especially inflation expectations. Equities have some short-term downside, but the cyclical peak still lies ahead. The equity rally will leave stocks vulnerable to the inevitable pick-up in interest rates later this cycle. Gold stocks may provide an attractive hedge for now. A spike in oil prices creates a major risk to our view. Stay overweight oil plays. Feature Global growth has clearly deteriorated this year, and bond yields around the world have cratered. German yields have plunged below -0.3% and U.S. yields briefly dipped below 2%. Even if the S&P 500 remains near all-time highs, the performance of cyclical sectors relative to defensive ones is corroborating the message from the bond market. Bonds and stocks are therefore not as much in disagreement as appears at first glance. To devise an appropriate strategy, now more than ever investors must decide whether or not a recession is on the near-term horizon. Answering yes to this question means bond prices will continue to rise, the dollar will rally further, stocks will weaken, and defensive stocks will keep outperforming cyclical ones. Answering no, one should sell bonds, sell the dollar, buy stocks, and overweight cyclical sectors. The weak global backdrop can still capsize the domestic U.S. economy. We stand in the ‘no’ camp: We do not believe a recession is in the offing and, while the current growth slowdown has been painful, it is not the end of the business cycle. Logically, we are selling bonds, selling the dollar and maintaining a positive cyclical stance on stocks. We also expect international equities to outperform U.S. ones, and we are becoming particularly positive on gold stocks. Oil prices should also benefit from the upcoming improvement in global growth. Has The U.S. Economy Met Its Iceberg? Investors betting on a recession often point to the inversion of the 3-month/10-year yield curve and the performance of cyclical stocks. However, we must also remember Paul Samuelson’s famous quip that “markets have predicted nine of the five previous recessions.” In any case, these market moves tell us what we already know: growth has weakened. We must decide whether it will weaken further. A simple probit model based on the yield curve slope and the new orders component of the ISM Manufacturing Index shows that there is a 40% probability of recession over the next 12 months. We need to keep in mind that in 1966 and 1998, this model was flagging a similar message, yet no recession followed over the course of the next year (Chart I-1). This means we must go back and study the fundamentals of U.S. growth. Chart I-1The Risk Of A Recession Has Risen, But It Is Not A No Brainer

The Risk Of A Recession Has Risen, But It Is Not A No Brainer

The Risk Of A Recession Has Risen, But It Is Not A No Brainer

Chart I-2Lower Rates Will Help Residential Investment

Lower Rates Will Help Residential Investment

Lower Rates Will Help Residential Investment

On the purely domestic front, the U.S. economy is not showing major stresses. Last month, we argued that we are not seeing the key symptoms of tight monetary policy: Homebuilders remain confident, mortgage applications for purchases are near cyclical highs, homebuilder stocks have been outperforming the broad market for three quarters, and lumber prices are rebounding.1 Moreover, the previous fall in mortgage yields is already lifting existing home sales, and it is only a matter of time before residential investment follows (Chart I-2). Households remain in fine form. Real consumer spending is growing at a 2.8% pace, and despite rising economic uncertainty, the Atlanta Fed GDPNow model expects real household spending to expand at a 3.9% rate in the second quarter (Chart I-3). This is key, as consumers’ spending and investment patterns drive the larger trends in the economy.2 Chart I-3Consumers Are Spending

Consumers Are Spending

Consumers Are Spending

Chart I-4The Labor Market Is Still Doing Fine...

The Labor Market Is Still Doing Fine...

The Labor Market Is Still Doing Fine...

Going forward, we expect consumption to stay the course. Despite its latest dip, consumer confidence remains elevated, household debt levels have fallen from 134% of disposable income in 2007 to 99% today, and debt-servicing costs only represent 9.9% of after-tax income, a multi-generational low. In this context, stronger household income growth should support spending. The May payrolls report is likely to have been an anomaly. Layoffs are still minimal, initial jobless claims continue to flirt near 50-year lows, the Conference Board’s Leading Credit index shows no stress, and the employment components of both the manufacturing and non-manufacturing ISM are at elevated levels (Chart I-4). If these leading indicators of employment are correct, both the employment-to-population ratio for prime-age workers and salaries have upside (Chart I-5), especially as productivity growth is accelerating. Despite these positives, the weak global backdrop can still capsize the domestic U.S. economy, and force the ISM non-manufacturing PMI to converge toward the manufacturing index. If global growth worsens, the dollar will strengthen, quality spreads will widen and stocks will weaken, resulting in tighter financial conditions. Since economic and trade uncertainty is still high, further deterioration in external conditions will cause U.S. capex to collapse. Employment would follow, confidence suffer and consumption fall. Global growth still holds the key to the future.

Chart I-5

Following The Chinese Impulse As the world’s foremost trading nation, Chinese activity lies at the center of the global growth equation. The China-U.S. trade war remains at the forefront of investors’ minds. The meeting between U.S. President Donald Trump and Chinese President Xi Jinping over the next two days is important. It implies a thawing of Sino-U.S. trade negotiations. However, an overall truce is unlikely. An agreement to resume the talks is the most likely outcome. No additional tariffs will be levied on the remaining $300 billion of untaxed Chinese exports to the U.S., but the previous levies will not be meaningfully changed. Removing this $300 billion Damocles sword hanging over global growth is a positive at the margin. However, it also means that the can has been kicked down the road and that trade will remain a source of headline risk, at least until the end of the year. Chart I-6The Rubicon Has Been Crossed

The Rubicon Has Been Crossed

The Rubicon Has Been Crossed

Trade uncertainty will nudge Chinese policymakers to ease policy further. In previous speeches, Premier Li Keqiang set the labor market as a line in the sand. If it were to deteriorate, the deleveraging campaign could be put on the backburner. Today, the employment component of the Chinese PMI is at its lowest level since the Great Financial Crisis (Chart I-6). This alone warrants more reflationary efforts by Beijing. Adding trade uncertainty to this mix guarantees additional credit and fiscal stimulus. More Chinese stimulus will be crucial for Chinese and global growth. Historically, it has taken approximatively nine months for previous credit and fiscal expansions to lift economic activity. We therefore expect that over the course of the summer, the imports component of the Chinese PMI should improve further, and the overall EM Manufacturing PMI should begin to rebound (Chart I-7, top and second panel). More generally, this summer should witness the bottom in global trade, as exemplified by Asian or European export growth (Chart I-7, third and fourth panel). The prospect for additional Chinese stimulus means that the associated pick-up in industrial activity should have longevity. Global central banks are running a brand new experiment. We are already seeing one traditional signpost that Chinese stimulus is having an impact on growth. Within the real estate investment component of GDP, equipment purchases are growing at a 30% annual rate, a development that normally precedes a rebound in manufacturing activity (Chart I-8, top panel). We are also keeping an eye out for the growth of M1 relative to M2. When Chinese M1 outperforms M2, it implies that demand deposits are growing faster than savings deposits. The inference is that the money injected in the economy is not being saved, but is ready to be deployed. Historically, a rebounding Chinese M1 to M2 ratio accompanies improvements in global trade, commodities prices, and industrial production (Chart I-8, bottom panel). Chart I-7The Turn In Chinese Credit Will Soon Be Felt Around The World

The Turn In Chinese Credit Will Soon Be Felt Around The World

The Turn In Chinese Credit Will Soon Be Felt Around The World

Chart I-8China's Stimulus Is Beginning To Have An Impact

China's Stimulus Is Beginning To Have An Impact

China's Stimulus Is Beginning To Have An Impact

To be sure, China is not worry free. Auto sales are still soft, global semiconductor shipments remain weak, and capex has yet to turn the corner. But the turnaround in credit and in the key indicators listed above suggests the slowdown is long in the tooth. In the second half of 2019, China will begin to add to global growth once again. Advanced Economies’ Central Banks: A Brave New World Chart I-9The Inflation Expectations Panic

The Inflation Expectations Panic

The Inflation Expectations Panic

While China is important, it is not the only game in town. Global central banks are running a brand new experiment. It seems they have stopped targeting realized inflation and are increasingly focused on inflation expectations. The collapse in inflation expectations is worrying central bankers (Chart I-9). Falling anticipated inflation can anchor actual inflation at lower levels than would have otherwise been the case. It also limits the downside to real rates when growth slows, and therefore, the capacity of monetary policy to support economic activity. Essentially, central banks fear that permanently depressed inflation expectations renders them impotent. The change in policy focus is evident for anyone to see. As recently as January 2019, 52% of global central banks were lifting interest rates. Now that inflation expectations are collapsing, other than the Norges Bank, none are doing so (Chart I-10). Instead, the opposite is happening and the RBA, RBNZ and RBI are cutting rates. Moreover, as investors are pricing in lower policy rates around the world, G-10 bond yields are collapsing, which is easing global liquidity conditions. Indeed, as Chart I-11 illustrates, when the share of economies with falling 2-year forward rates is as high as it is today, the BCA Global Leading Indicator rebounds three months later. Chart I-10Central Banks Are In Easing Mode, Everywhere

Central Banks Are In Easing Mode, Everywhere

Central Banks Are In Easing Mode, Everywhere

The European Central Bank stands at the vanguard of this fight. As we argued two months ago, deflationary pressures in Europe are intact and are likely to be a problem for years to come.3 The ECB is aware of this headwind and knows it needs to act pre-emptively. Four months ago, it announced a new TLRTO-III package to provide plentiful funding for stressed banks in the European periphery. On June 6th, ECB President Mario Draghi unveiled very generous financing terms for the TLTRO-III. Last week, at the ECB’s Sintra conference in Portugal, ECB Vice President Luis de Guindos professed that the ECB could cut rates if inflation expectations weaken. The following day, Draghi himself strongly hinted at an upcoming rate cut in Europe and a potential resumption of the ECB QE program. These measures are starting to ease financial conditions where Europe needs it most: Italy. An important contributor to the contraction in the European credit impulse over the past 21 months was the rapid tightening in Italian financial conditions that followed the surge in BTP yields from May 2018. Now that the ECB is becoming increasingly dovish, Italian yields have fallen to 2.1%, and are finally below the neutral rate of interest for Europe. BTP yields are again at accommodative levels. Chart I-11This Much Of An Easing Bias Boosts Growth Prospects

This Much Of An Easing Bias Boosts Growth Prospects

This Much Of An Easing Bias Boosts Growth Prospects

With financial conditions in Europe easing and exports set to pick up in response to Chinese growth, European loan demand should regain some vigor. Meanwhile, the TLTRO-III measures, which are easing bank funding costs, should boost banks’ willingness to lend. The European credit impulse is therefore set to move back into positive territory this fall. European growth will rebound, and contribute to improving global growth conditions. The Fed’s Patience Is Running Out

Chart I-12

The Federal Reserve did not cut interest rates last week, but its intentions to do so next month were clear. First, the language of the statement changed drastically. Gone is the Fed’s patience; instead, there is an urgency to “act as appropriate to sustain the expansion.” Second, the fed funds rate projections from the Summary of Economic Projections were meaningfully revised down. In March, 17 FOMC participants expected the Fed to stay on hold for the remainder of 2019, while six foresaw hikes. Today, eight expect a steady fed funds rate, but seven are calling for two rate cuts this year. Only one member is still penciling in a hike. Moreover, nine out of 17 participants anticipate that rates will be lower in 2020 than today (Chart I-12). The FOMC’s unwillingness to push back very dovish market expectations signals an imminent interest rate cut. Like other advanced economy central banks, the Fed’s sudden dovish turn is aimed at reviving moribund inflation expectations (Chart I-13). In order to do so, the Fed will have to keep real interest rates at low levels, at least relative to real GDP growth. Even if the real policy rate goes up, so long as it increases more slowly than GDP growth, it will signify that money supply is growing faster than money demand.4 TIPS yields are anticipating these dynamics and will likely remain soft relative to nominal interest rates. Chart I-13...As Inflation Expectations Plunge

...As Inflation Expectations Plunge

...As Inflation Expectations Plunge

Since the Fed intends to conduct easy monetary policy until inflation expectations have normalized to the 2.3% to 2.5% zone, our liquidity gauges will become more supportive of economic activity and asset prices over the coming two to three quarters: Our BCA Monetary indicator has not only clearly hooked up, it is now above the zero line, in expansionary territory (see Section III, page 41). Excess money growth, defined as money-of-zero-maturity over loan growth, is once again accelerating. This cycle, global growth variables such as our Global Nowcast, BCA’s Global Leading Economic Indicator, or worldwide export prices have all reliably followed this variable (Chart I-14). After collapsing through 2018, our U.S. Financial Liquidity Index is rebounding sharply, and the imminent end of the Fed’s balance sheet runoff will only solidify this progress. This indicator gauges how cheap and plentiful high-powered money is for global markets. Its recovery suggests that commodities, globally-traded goods prices, and economic activity are all set to improve (Chart I-15). Chart I-14Excess Money Has Turned Up

Excess Money Has Turned Up

Excess Money Has Turned Up

Chart I-15Improving Liquidity Conditions Argue That Nominal Growth Will Pick Up...

Improving Liquidity Conditions Argue That Nominal Growth Will Pick Up...

Improving Liquidity Conditions Argue That Nominal Growth Will Pick Up...

The dollar is losing momentum and should soon fall, which will reinforce the improvement in global liquidity conditions. A trough in our U.S. Financial Liquidity Index is often followed by a weakening dollar (Chart I-16). Moreover, the Greenback’s strength has been turbocharged by exceptional repatriations of funds by U.S. economic agents (Chart I-17). The end of the repatriation holiday along with a more dovish Fed and the completion of the balance sheet runoff will likely weigh on the dollar. Once the Greenback depreciates, the cost of borrowing for foreign issuers of dollar-denominated debt will decline, along with the cost of liquidity, especially if the massive U.S. repatriation flows are staunched. This will further support global growth conditions. Chart I-16...And That The Dollar Will Turn Down...

...And That The Dollar Will Turn Down...

...And That The Dollar Will Turn Down...

Trade relations are unlikely to deteriorate further, China is likely to stimulate more aggressively; and easing central banks around the world, including the Fed, are responding to falling inflation expectations. This backdrop points to a rebound in global growth in the second half of the year. As a corollary, the deflationary patch currently engulfing the world should end soon after. As a result, this growing reflationary mindset should delay any recession until late 2021 if not 2022. However, as the business cycle extends further, greater inflationary pressures will build down the road and force the Fed to lift rates – even more than it would have done prior to this wave of easing. Chart I-17...Especially If Repatriation Flows Slow

...Especially If Repatriation Flows Slow

...Especially If Repatriation Flows Slow

Investment Implications Bonds BCA’s U.S. Bond Strategy service relies on the Golden Rule of Treasury Investing. This simple rule states that when the Fed turns out to be more dovish than anticipated by interest rate markets 12 months prior, Treasurys outperform cash. If the Fed is more hawkish than was expected by market participants, Treasurys underperform (Chart I-18). Today, the Treasury market’s outperformance is already consistent with a Fed generating a very dovish surprise over the next 12 months. However, the interest rate market is already pricing in a 98% probability of two rates cuts this year, and the December 2020 fed funds rate futures imply a halving of the policy rate. The Fed is unlikely to clear these very tall dovish hurdles as global growth is set to rebound, the fed funds rate is not meaningfully above neutral and the household sector remains resilient. Chart I-18Treasurys Already Anticipate Large Dovish Surprises

Treasurys Already Anticipate Large Dovish Surprises

Treasurys Already Anticipate Large Dovish Surprises

Reflecting elevated pessimism toward global growth, the performance of transport relative to utilities stocks is as oversold as it gets. The likely rebound in this ratio should push yields higher, especially as foreign private investors are already aggressively buying U.S. government securities (Chart I-19). As occurred in 1998, Treasury yields should rebound soon after the Fed begins cutting rates. Moreover, with all the major central banks focusing on keeping rates at accommodative levels, the selloff in bonds should be led by inflation breakevens, also as occurred in 1998 (Chart I-20), especially if the dollar weakens. Chart I-19Yields Will Follow Transportation Relative To Utilities Stocks

Yields Will Follow Transportation Relative To Utilities Stocks

Yields Will Follow Transportation Relative To Utilities Stocks

Chart I-201998: Yields Rebounded As Soon As The Fed Began Cutting

1998: Yields Rebounded As Soon As The Fed Began Cutting

1998: Yields Rebounded As Soon As The Fed Began Cutting

Equities A global economic rebound should provide support for equities on a cyclical horizon. The tactical picture remains murky as the stock market may have become too optimistic that Osaka will deliver an all-encompassing deal. However, this short-term downside is likely to prove limited compared to the cyclical strength lying ahead. This is particularly true for global equities, where valuations are more attractive than in the U.S. Chart I-21Easier Liquidity Conditions Lead To Higher Stock Prices

Easier Liquidity Conditions Lead To Higher Stock Prices

Easier Liquidity Conditions Lead To Higher Stock Prices

Even if the S&P 500 isn’t the prime beneficiary of the recovery in global growth, it should nonetheless generate positive absolute returns on a cyclical horizon. As Chart I-21 illustrates, a pickup in our U.S. Financial Liquidity Index often precedes a rally in U.S. stocks. Since the U.S. Financial Liquidity Index has done a superb job of forecasting the weakness in stocks over the past 18 months, it is likely to track the upcoming strength as well. A weaker dollar should provide an additional tailwind to boost profit growth, especially as U.S. productivity is accelerating. This view is problematic for long-term investors. The cheapness of stocks relative to bonds is the only reason why our long-term valuation index is not yet at nosebleed levels Chart I-22). If we are correct that the current global reflationary push will build greater inflationary pressures down the road and will ultimately result in even higher interest rates, this relative undervaluation of equities will vanish. The overall valuation index will then hit near-record highs, leaving the stock market vulnerable to a very sharp pullback. Long-term investors should use this rally to lighten their strategic exposure to stocks, especially when taking into account the risk that populism will force a retrenchment in corporate market power, an issue discussed in Section II. Gone is the Fed’s patience; instead, there is an urgency to “act as appropriate to sustain the expansion.” In this environment, gold stocks are particularly attractive. Central banks are targeting very accommodative policy settings, which will limit the upside for real rates. Moreover, generous liquidity conditions and a falling dollar should prove to be great friends to gold. These fundamentals are being amplified by a supportive technical backdrop, as gold prices have broken out and the gold A/D line keeps making new highs (Chart I-23). Chart I-22Beware What Will Happen To Valuations Once Rates Rise Again

Beware What Will Happen To Valuations Once Rates Rise Again

Beware What Will Happen To Valuations Once Rates Rise Again

Chart I-23Strong Technical Backdrop For The Gold

Strong Technical Backdrop For The Gold

Strong Technical Backdrop For The Gold

Structural forces reinforce these positives for gold. EM reserve managers are increasingly diversifying into gold, fearful of growing geopolitical tensions with the U.S. (Chart I-24). Meanwhile, G-10 central banks are not selling the yellow metal anymore. This positive demand backdrop is materializing as global gold producers have been focused on returning cash to shareholders instead of pouring funds into capex. This lack of investment will weigh on output growth going forward. Chart I-24EM Central Banks Are Diversifying Into Gold

EM Central Banks Are Diversifying Into Gold

EM Central Banks Are Diversifying Into Gold

This emphasis on returning cash to shareholders makes gold stocks particularly attractive. Gold producers are trading at a large discount to the market and to gold itself as investors remain concerned by the historical lack of management discipline. However, boosting dividends, curtailing debt levels and only focusing on the most productive projects ultimately creates value for shareholders. A wave of consolidation will only amplify these tailwinds. Our overall investment recommendation is to overweight stocks over bonds on a cyclical horizon while building an overweight position in gold equities. Our inclination to buy gold stocks transcends our long-term concerns for equities, as rising long-term inflation should favor gold as well. The Key Risk: Iran The biggest risk to our view remains the growing stress in the Middle East. BCA’s Geopolitical Strategy team assigns a less than 40% chance that tensions between the U.S. and Iran will deteriorate into a full-fledged military conflict. The U.S.’s reluctance to respond with force to recent Iranian provocations may even argue that this probability could be too high. Nonetheless, if a military conflict were to happen, it would involve a closing of the Strait of Hormuz, a bottleneck through which more than 20% of global oil production transits. In such a scenario, Brent prices could easily cross above US$150/bbl. Chart I-25Oil Inventories Are Set To Decline

Oil Inventories Are Set To Decline

Oil Inventories Are Set To Decline

To mitigate this risk, we recommend overweighting oil plays in global portfolios. Not only would such an allocation benefit in the event of a blow-up in the Persian Gulf, oil is supported by positive supply/demand fundamentals and Brent should end the year $75/bbl. After five years of limited oil capex, Wood Mackenzie estimates that the supply of oil will be close to 5 million barrels per day smaller than would have otherwise been the case. Moreover, OPEC and Russia remain disciplined oil producers, which is limiting growth in crude output today. Meanwhile, in light of the global growth deceleration, demand for oil has proved surprisingly robust. Demand is likely to pick up further when global growth reaccelerates in the second half of the year. As a result, BCA’s Commodity and Energy Strategy currently expects additional inventory drawdowns that will only push oil prices higher in an environment of growing global reflation (Chart I-25). A falling dollar would accentuate these developments. Mathieu Savary Vice President The Bank Credit Analyst June 27, 2019 Next Report: July 25, 2019 II. The Productivity Puzzle: Competition Is The Missing Ingredient Productivity growth is experiencing a cyclical rebound, but remains structurally weak. The end of the deepening of globalization, statistical hurdles, and the possibility that today’s technological advances may not be as revolutionary as past ones all hamper productivity. On the back of rising market power and concentration, companies are increasing markups instead of production. This is depressing productivity and lowering the neutral rate of interest. For now, investors can generate alpha by focusing on consolidating industries. Growing market power cannot last forever and will meet a political wall. Structurally, this will hurt asset prices. “We don’t have a free market; don’t kid yourself. (…) Businesspeople are enemies of free markets, not friends (…) businesspeople are all in favor of freedom for everybody else (…) but when it comes to their own business, they want to go to Washington to protect their businesses.” Milton Friedman, January 1991. Despite the explosion of applications of growing computing power, U.S. productivity growth has been lacking this cycle. This incapacity to do more with less has weighed on trend growth and on the neutral rate of interest, and has been a powerful force behind the low level of yields at home and abroad. In this report, we look at the different factors and theories advanced to explain the structural decline in productivity. Among them, a steady increase in corporate market power not only goes a long way in explaining the lack of productivity in the U.S., but also the high level of profit margins along with the depressed level of investment and real neutral rates. A Simple Cyclical Explanation The decline in productivity growth is both a structural and cyclical story. Historically, productivity growth has followed economic activity. When demand is strong, businesses can generate more revenue and therefore produce more. The historical correlation between U.S. nonfarm business productivity and the ISM manufacturing index illustrates this relationship (Chart II-1). Chart II-1The Cyclical Behavior Of Productivity

The Cyclical Behavior Of Productivity

The Cyclical Behavior Of Productivity

Chart II-2Deleveraging Hurts Productivity

Deleveraging Hurts Productivity

Deleveraging Hurts Productivity

Since 2008, as households worked off their previous over-indebtedness, the U.S. private sector has experienced its longest deleveraging period since the Great Depression. This frugality has depressed demand and contributed to lower growth this cycle. Since productivity is measured as output generated by unit of input, weak demand growth has depressed productivity statistics. On this dimension, the brief deleveraging experience of the early 1990s is instructive: productivity picked up only after 1993, once the private sector began to accumulate debt faster than the pace of GDP growth (Chart II-2). The recent pick-up in productivity reflects these debt dynamics. Since 2009, the U.S. non-financial private sector has stopped deleveraging, removing one anchor on demand, allowing productivity to blossom. Moreover, the pick-up in capex from 2017 to present is also helping productivity by raising the capital-to-workers ratio. While this is a positive development for the U.S. economy, the decline in productivity nonetheless seems structural, as the five-year moving average of labor productivity growth remains near its early 1980s nadir (Chart II-3). Something else is at play.

Chart II-3

The Usual Suspects Three major forces are often used to explain why observed productivity growth is currently in decline: A slowdown in global trade penetration, the fact that statisticians do not have a good grasp on productivity growth in a service-based economy, and innovation that simply isn’t what it used to be. Slowdown In Global Trade Penetration Two hundred years ago, David Ricardo argued that due to competitive advantages, countries should always engage in trade to increase their economic welfare. This insight has laid the foundation of the argument that exchanges between nations maximizes the utilization of resources domestically and around the world. Rarely was this argument more relevant than over the past 40 years. On the heels of the supply-side revolution of the early 1980s and the fall of the Berlin Wall, globalization took off. The share of the world's population participating in the global capitalist system rose from 30% in 1985 to nearly 100% today. The collapse in new business formation in the U.S. is another fascinating development. Generating elevated productivity gains is simpler when a country’s capital stock is underdeveloped: each unit of investment grows the capital-to-labor ratio by a greater proportion. As a result, productivity – which reflects the capital-to-worker ratio – can grow quickly. As more poor countries have joined the global economy and benefitted from FDI and other capital inflows, their productivity has flourished. Consequently, even if productivity growth has been poor in advanced economies over the past 10 years, global productivity has remained high and has tracked the share of exports in global GDP (Chart II-4). Chart II-4The Apex Of Globalization Represented The Summit Of Global Productivity Growth

The Apex Of Globalization Represented The Summit Of Global Productivity Growth

The Apex Of Globalization Represented The Summit Of Global Productivity Growth

This globalization tailwind to global productivity growth is dissipating. First, following an investment boom where poor decisions were made, EM productivity growth has been declining. Second, with nearly 100% of the world’s labor supply already participating in the global economy, it is increasingly difficult to expand the share of global trade in global GDP and increase the benefit of cross-border specialization. Finally, the popular backlash in advanced economies against globalization could force global trade into reverse. As economic nationalism takes hold, cross-border investments could decline, moving the world economy further away from an optimal allocation of capital. These forces may explain why global productivity peaked earlier this decade. Productivity Is Mismeasured Recently deceased luminary Martin Feldstein argued that the structural decline in productivity is an illusion. As the argument goes, productivity is not weak; it is only underestimated. This is pure market power, and it helps explain the gap between wages and productivity. A parallel with the introduction of electricity in the late 19th century often comes to mind. Back then, U.S. statistical agencies found it difficult to disentangle price changes from quantity changes in the quickly growing revenues of electrical utilities. As a result, the Bureau Of Labor Statistics overestimated price changes in the early 20th century, which depressed the estimated output growth of utilities by a similar factor. Since productivity is measured as output per unit of labor, this also understated actual productivity growth – not just for utilities but for the economy as a whole. Ultimately, overall productivity growth was revised upward. Chart II-5Plenty Of Room To Mismeasure Real Output Growth

Plenty Of Room To Mismeasure Real Output Growth

Plenty Of Room To Mismeasure Real Output Growth

In today’s economy, this could be a larger problem, as 70% of output is generated in the service sector. Estimating productivity growth is much harder in the service sector than in the manufacturing sector, as there is no actual countable output to measure. Thus, distinguishing price increases from quantity or quality improvements is challenging. Adding to this difficulty, the service sector is one of the main beneficiaries of the increase in computational power currently disrupting industries around the world. The growing share of components of the consumer price index subject to hedonic adjustments highlight this challenge (Chart II-5). Estimating quality changes is hard and may bias the increase in prices in the economy. If prices are unreliably measured, so will output and productivity. Chart II-6A Multifaceted Decline In Productivity

A Multifaceted Decline In Productivity

A Multifaceted Decline In Productivity

Pushing The Production Frontier Is Increasingly Hard Another school of thought simply accepts that productivity growth has declined in a structural fashion. It is far from clear that the current technological revolution is much more productivity-enhancing than the introduction of electricity 140 years ago, the development of the internal combustion engine in the late 19th century, the adoption of indoor plumbing, or the discovery of penicillin in 1928. It is easy to overestimate the economic impact of new technologies. At first, like their predecessors, the microprocessor and the internet created entirely new industries. But this is not the case anymore. For all its virtues, e-commerce is only a new method of selling goods and services. Cloud computing is mainly a way to outsource hardware spending. Social media’s main economic value has been to gather more information on consumers, allowing sellers to reach potential buyers in a more targeted way. Without creating entirely new industries, spending on new technologies often ends up cannibalizing spending on older technologies. For example, while Google captures 32.4% of global ad revenues, similar revenues for the print industry have fallen by 70% since their apex in 2000. If new technologies are not as accretive to production as the introduction of previous ones were, productivity growth remains constrained by the same old economic forces of capex, human capital growth and resource utilization. And as Chart II-6 shows, labor input, the utilization of capital and multifactor productivity have all weakened. Some key drivers help understand why productivity growth has downshifted structurally.

Chart II-7

Chart II-8Demographics Are Hurting Productivity

Demographics Are Hurting Productivity

Demographics Are Hurting Productivity